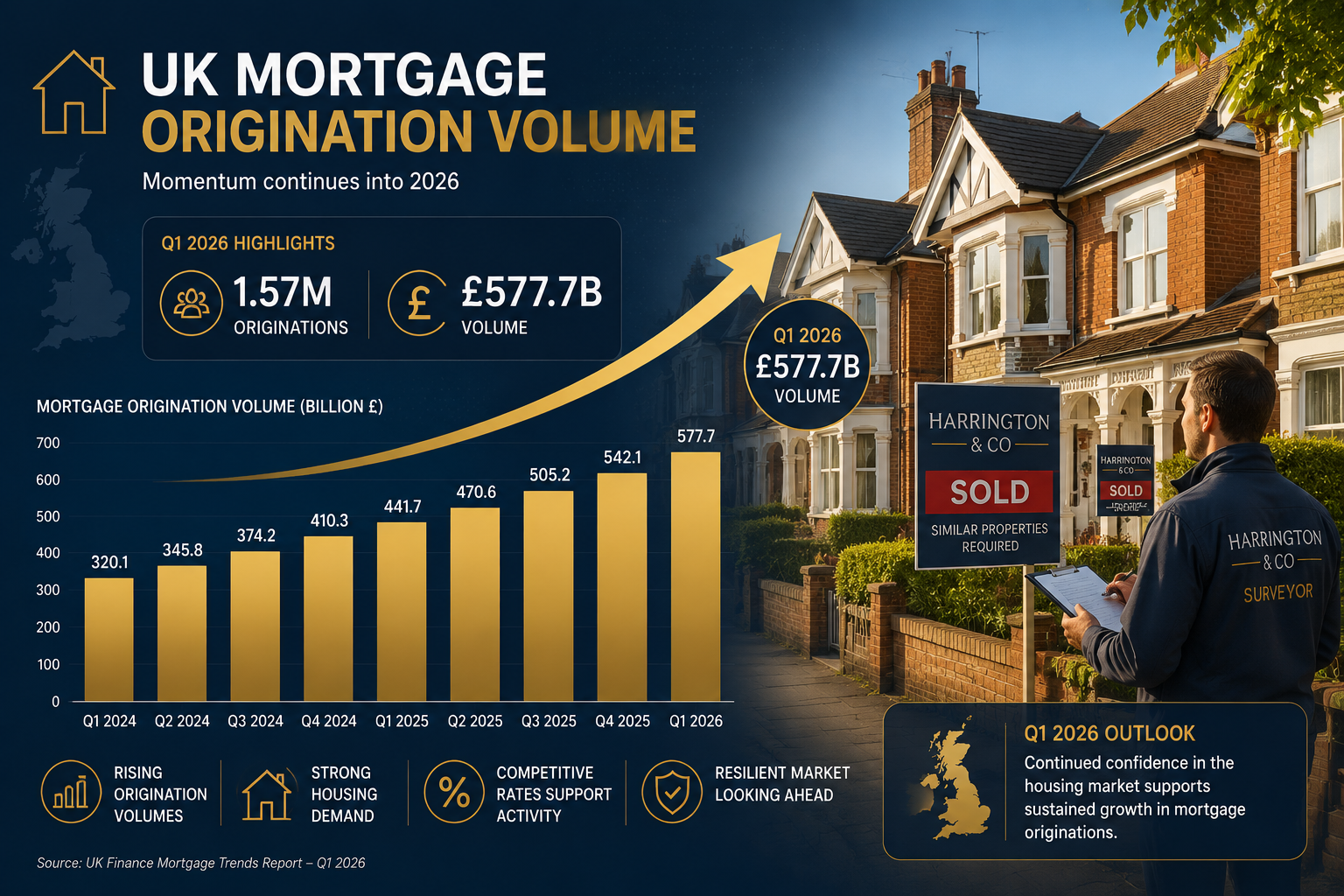

Mortgage originations in Q1 2026 reached 1.57 million transactions totalling $577.7 billion in loan volume — a 5% year-on-year increase that signals a genuine, if uneven, market recovery [3]. Where lending volumes grow, so do the disputes that follow. Valuation disagreements between lenders, borrowers, and insurers are rising in step with transaction activity, making expert witness preparation for mortgage valuation disputes in recovering 2026 lending volumes one of the most pressing professional challenges for chartered surveyors and property valuation specialists today.

This article examines the market forces driving that dispute uptick, the RICS standards now under revision, and the practical steps expert witnesses must take to deliver credible, court-ready opinions in a stabilising but still volatile property environment.

Key Takeaways

- Recovering 2026 lending volumes are generating a higher frequency of mortgage valuation disputes, increasing demand for qualified expert witnesses.

- The Royal Institution of Chartered Surveyors (RICS) launched a consultation in April 2026 for its fifth edition expert witness standard — the first update since 2014 — covering AI integration, conditional fees, and global applicability [2].

- An expert witness's primary duty is to the court, not to the instructing party; independence and transparency are non-negotiable.

- Robust documentation, comparable evidence, and methodology disclosure are the pillars of a defensible expert valuation report.

- Foreclosure activity rose 30.6% in 2025 and continues to climb in 2026, creating a secondary wave of valuation-related litigation [4].

The 2026 Lending Landscape and Why Disputes Are Rising

Understanding the dispute environment requires a clear picture of the market itself. The Mortgage Bankers Association projects total single-family mortgage originations to increase 8% to $2.2 trillion in 2026, with purchase originations rising 7.7% to $1.46 trillion [5]. Fannie Mae anticipates mortgage rates falling below 6% by year-end, a threshold widely expected to unlock pent-up buyer demand [6].

Yet recovery is not the same as stability. Home purchase loans in Q1 2026 fell 19% from the previous quarter, hitting their lowest quarterly level since Q1 2014 [3]. Elevated home prices and residual rate sensitivity are compressing affordability even as headline origination figures improve. S&P Global notes that tight housing inventory and elevated prices will continue to challenge purchase activity throughout the year, even as nonbank lender profitability strengthens [7].

The dispute arithmetic is straightforward: more transactions at stretched valuations, combined with rising foreclosure activity (59,160 new foreclosures in Q1 2026 alone [4]), means more occasions on which a lender, borrower, or insurer will challenge the original property valuation. Americans currently hold $13.19 trillion in mortgage debt, representing 70.2% of all consumer debt [4]. Even a fractional increase in contested valuations translates into thousands of active disputes.

Key Dispute Triggers in 2026

The following factors are most commonly cited as triggers for mortgage valuation disputes in the current market:

| Trigger | Description |

|---|---|

| Rapid price correction | Values assigned at peak now challenged against lower current comparables |

| Thin comparable evidence | Low transaction volumes make like-for-like comparisons difficult |

| Lender down-valuations | Mortgage offers reduced after formal valuation, disputed by buyers |

| Foreclosure-related disputes | Borrowers contest valuations used to justify repossession and sale price |

| Leasehold and tenure complexity | Short leases or unusual tenure structures inflate valuation uncertainty |

For surveyors instructed as expert witnesses, each of these triggers demands a different evidential approach — but all share a common requirement for methodological rigour.

RICS Standards Governing Expert Witness Preparation for Mortgage Valuation Disputes in Recovering 2026 Lending Volumes

In April 2026, RICS initiated a consultation for the fifth edition of its expert witness standard [2]. This is the first substantive revision since 2014 and reflects how significantly the practice environment has changed. Three themes dominate the consultation:

- Artificial intelligence integration — How AI-assisted valuation tools should be disclosed and tested in expert reports.

- Conditional fee arrangements — Clarifying whether and how success-linked fees affect an expert's independence.

- Global applicability — Aligning the standard with international court and tribunal requirements beyond England and Wales.

For practitioners, the consultation signals that the bar for expert witness preparation is rising. Reports produced under the existing fourth edition standard remain valid, but surveyors who are not engaging with the proposed changes risk producing work that falls short of emerging expectations.

The Overriding Duty to the Court

Regardless of which edition of the RICS standard applies, one principle is immovable: the expert witness's primary duty is to the court, not to the party that instructed them [1]. This means:

- Opinions must be genuinely held and capable of withstanding cross-examination.

- Contrary evidence must be acknowledged and addressed, not omitted.

- The expert must not act as an advocate for their instructing party's commercial position.

Valuation expert witnesses translate complex financial analyses into conclusions that a judge, arbitrator, or tribunal can apply to a legal outcome [1]. The credibility of that translation depends entirely on perceived and actual independence.

"An expert who is seen to favour the instructing party's position will find their evidence discounted or disregarded. Independence is not just an ethical requirement — it is a practical necessity for effective testimony."

Red Book Compliance and Departure Protocols

Mortgage valuation disputes almost always involve a challenge to whether the original valuation complied with RICS Valuation — Global Standards (the Red Book). Expert witnesses must be thoroughly conversant with the relevant edition in force at the date of the original valuation, not the current edition. Where the original valuer departed from Red Book methodology, the expert must assess whether that departure was disclosed and justified.

For properties in London and the South East, where price volatility is particularly acute, understanding when a Red Book valuation is required and the precise scope of the instruction is foundational to any expert opinion.

Practical Steps for Expert Witness Preparation for Mortgage Valuation Disputes in Recovering 2026 Lending Volumes

Preparation quality is the single greatest determinant of expert witness effectiveness. The following framework reflects current best practice for valuation disputes in the 2026 market.

Step 1: Define the Scope of the Expert Instruction Precisely

Before any analysis begins, the expert must confirm:

- The precise question(s) the court or tribunal requires answering.

- The valuation date — critical in a volatile market where values may have moved significantly.

- The basis of value (Market Value, Mortgage Lending Value, or another defined basis).

- Any limitations on the evidence available.

Ambiguity in the instruction is a common cause of expert reports being challenged or excluded. Clarifying scope in writing before commencing work protects both the expert and the instructing solicitor.

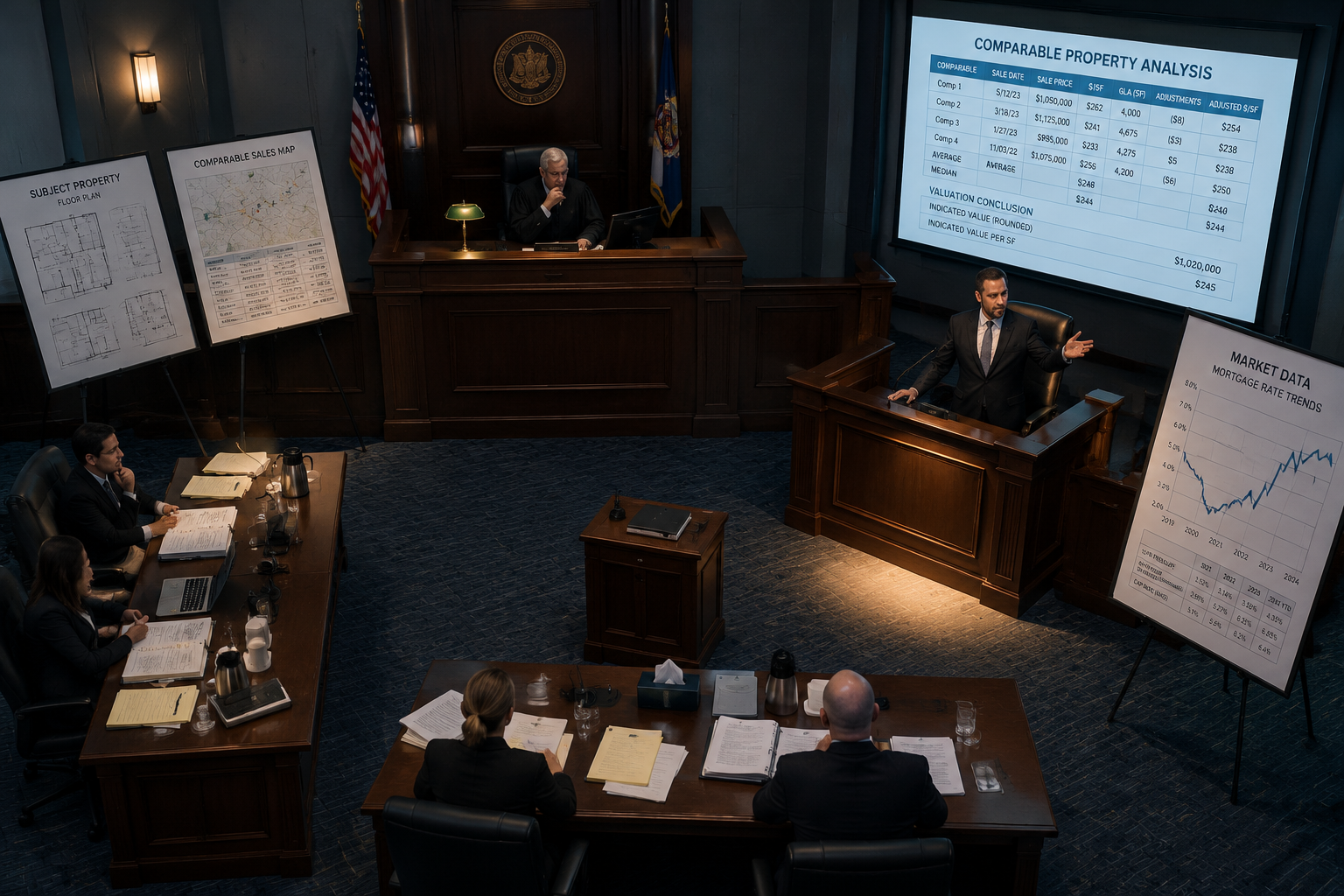

Step 2: Assemble and Scrutinise the Comparable Evidence

In a recovering market with thin transaction volumes, finding genuinely comparable sales evidence is harder than it was during peak activity. Expert witnesses should:

- Cast a wider geographic net where local comparables are insufficient, while clearly explaining the adjustments made for location differences.

- Weight time-adjusted comparables carefully, particularly where the valuation date falls in a period of rapid price movement.

- Document every comparable considered and rejected, not just those relied upon. Courts are alert to cherry-picked evidence.

- Cross-reference automated valuation model (AVM) outputs against traditional comparable analysis, noting where they diverge and why.

The RICS homebuyers report and structural survey options provide a useful reference point for understanding the physical condition factors that legitimate valuers must incorporate — condition defects that were missed or underweighted by the original valuer are frequently central to dispute claims.

Step 3: Construct a Transparent Methodology Statement

The methodology section of an expert report is where credibility is won or lost. It must explain:

- Which valuation approach was adopted (sales comparison, income capitalisation, depreciated replacement cost) and why.

- How adjustments were derived and quantified.

- What weight was given to each comparable and the rationale for that weighting.

- How market conditions at the valuation date were assessed and applied.

Avoid vague language. Phrases such as "in the expert's professional judgement" without supporting reasoning are routinely challenged. Every conclusion should be traceable to evidence.

Step 4: Address the Original Valuer's Methodology Directly

A common structural error in expert reports is to present the expert's own opinion without engaging substantively with the original valuation. Courts expect the expert to:

- Identify specifically where the original valuation methodology was sound or flawed.

- Quantify the impact of any identified errors on the concluded value.

- Acknowledge where reasonable valuers could legitimately differ.

This last point matters. The question in most mortgage valuation disputes is not whether the expert would have reached a different figure, but whether the original valuation fell outside the range within which a competent valuer could reasonably have concluded. That range — sometimes called the "bracket" — is a concept expert witnesses must explain clearly and apply rigorously.

Step 5: Prepare for Cross-Examination

Written reports are only part of the process. Expert witnesses in contested hearings will face cross-examination designed to expose:

- Inconsistencies between the written report and oral evidence.

- Comparables or market data that the expert did not consider.

- Potential conflicts of interest or prior instructions for the same party.

- Overstatement of certainty in a market where professional disagreement is legitimate.

Preparation for cross-examination should include a thorough review of the opposing expert's report, identification of points of agreement (which should be conceded readily), and rehearsal of the key points on which the expert's opinion genuinely differs.

Structural and Physical Condition Factors in Valuation Disputes

Physical defects are a recurring source of dispute, particularly where a lender argues that the original valuation failed to identify or adequately reflect a material defect. Expert witnesses instructed in these cases need working knowledge of common defect types and their valuation impact.

Subsidence risk, for example, is frequently underweighted in original mortgage valuations. Understanding whether garden trees may be causing subsidence is the kind of technical knowledge that expert witnesses in property valuation disputes must be able to deploy. Similarly, damp-related defects — a common source of post-purchase complaint — require the expert to assess whether the original valuer's inspection standard was adequate given the visible evidence at the time.

For cases involving boundary disputes that have affected value, the costs associated with boundary disputes are a relevant consideration when quantifying loss. Leasehold properties present their own complexity; short-lease premiums and the impact of informal lease extension arrangements on market value are areas where expert opinion is frequently sought.

Emerging Issues: AI, Data Bias, and the Integrity of Valuation Evidence

The RICS consultation's focus on AI is timely. A May 2026 study identified persistent racial and gender disparities in U.S. mortgage lending data, highlighting the need for fair data preprocessing in algorithmic decision-making [9]. For expert witnesses, this raises a practical question: if an original valuation was assisted or informed by an AVM that embedded biased training data, does that affect the validity of the concluded figure?

The honest answer is that the profession does not yet have settled guidance on this point. What is clear is that expert witnesses who rely on AI-assisted analysis in their own reports must be able to explain the tool's methodology, its limitations, and the steps taken to verify its outputs against independent evidence. Blind reliance on algorithmic outputs will not survive cross-examination.

KBRA's forecast of $160 billion in RMBS issuance in 2026 — a 15% increase from 2025 — signals growing institutional appetite for securitised mortgage products [8]. As that market expands, disputes about the accuracy of the underlying property valuations used in securitisation pools are likely to increase. Expert witnesses with experience in bulk portfolio valuation methodology will find that specialism increasingly in demand.

Checklist: Expert Witness Report Quality Standards

Before filing any expert report in a mortgage valuation dispute, confirm the following:

- Instruction scope confirmed in writing with instructing solicitor

- Valuation date, basis of value, and applicable standards clearly stated

- All comparables considered documented, with reasons for rejection where applicable

- Methodology explained in plain language accessible to a non-specialist tribunal

- Original valuer's methodology addressed directly and specifically

- Points of agreement with opposing expert identified and conceded where appropriate

- AI or AVM tools disclosed and their outputs independently verified

- Conflicts of interest declaration completed

- Report reviewed for compliance with current RICS expert witness standard

For surveyors seeking to understand the full scope of professional survey standards before accepting an expert instruction, reviewing what to do before an RICS home survey provides useful context on the inspection standards against which original valuers will be measured.

Conclusion

Expert witness preparation for mortgage valuation disputes in recovering 2026 lending volumes demands a combination of market awareness, methodological rigour, and procedural discipline that goes well beyond producing a revised valuation figure. The 2026 market presents a specific challenge: recovery is real but uneven, comparable evidence is thin in many segments, and the regulatory framework governing expert evidence is itself in transition.

Actionable next steps for practitioners:

- Engage with the RICS fifth edition consultation now, before the standard is finalised. Practitioners who shape the standard will be better positioned to apply it.

- Audit your comparable evidence methodology against the thinner transaction volumes of 2026. Document every comparable considered, not just those relied upon.

- Develop a clear AI disclosure protocol for any valuation work that incorporates AVM outputs, anticipating cross-examination on algorithmic methodology.

- Review your independence declarations in light of the consultation's focus on conditional fees and prior instructions.

- Build physical defect knowledge — subsidence, damp, structural condition, and leasehold complexity are the most common grounds on which original valuations are challenged.

The credibility of expert valuation evidence ultimately rests on independence, transparency, and the ability to explain complex analysis in terms a non-specialist decision-maker can apply. In a recovering market where the stakes attached to each valuation opinion are rising, those qualities have never been more commercially and professionally important.

References

[1] The Role Of A Valuation Expert Witness In Litigation – https://legalclarity.org/the-role-of-a-valuation-expert-witness-in-litigation/?utm_source=openai

[2] Expert Witness Preparation For 2026 UK Valuation Disputes RICS Standards In A Recovering Market – https://www.canterburysurveyors.com/blog/expert-witness-preparation-for-2026-uk-valuation-disputes-rics-standards-in-a-recovering-market/?utm_source=openai

[3] Q1 2026 Loan Origination Report – https://www.attomdata.com/news/market-trends/mortgage-origination/q1-2026-loan-origination-report/?utm_source=openai

[4] U.S. Mortgage Market Statistics – https://www.lendingtree.com/home/mortgage/u-s-mortgage-market-statistics/?utm_source=openai

[5] MBA Forecast Total Single Family Mortgage Originations To Increase 8 Percent To 2.2 Trillion In 2026 – https://www.mba.org/news-and-research/newsroom/news/2025/10/19/mba-forecast–total-single-family-mortgage-originations-to-increase-8-percent-to–2.2-trillion-in-2026?utm_source=openai

[6] Mortgage Rates Expected Move Below 6 Percent End 2026 – https://www.fanniemae.com/newsroom/fannie-mae-news/mortgage-rates-expected-move-below-6-percent-end-2026?utm_source=openai

[7] Nonbank Consumer Auto And Mortgage Lending Sector View 2026 Resilience Amid Pressures – https://www.spglobal.com/ratings/en/regulatory/article/nonbank-consumer-auto-and-mortgage-lending-sector-view-2026-resilience-amid-pressures-s101665477?utm_source=openai

[8] KBRA Releases Research 2026 U.S. RMBS Sector Outlook Normalizing Credit And Growing Issuance – https://www.kbra.com/publications/SVGrRYDM/kbra-releases-research-2026-u-s-rmbs-sector-outlook-normalizing-credit-and-growing-issuance?format=web&utm_source=openai

[9] Discriminatory Patterns in Mortgage Lending Research – https://arxiv.org/abs/2606.12435?utm_source=openai