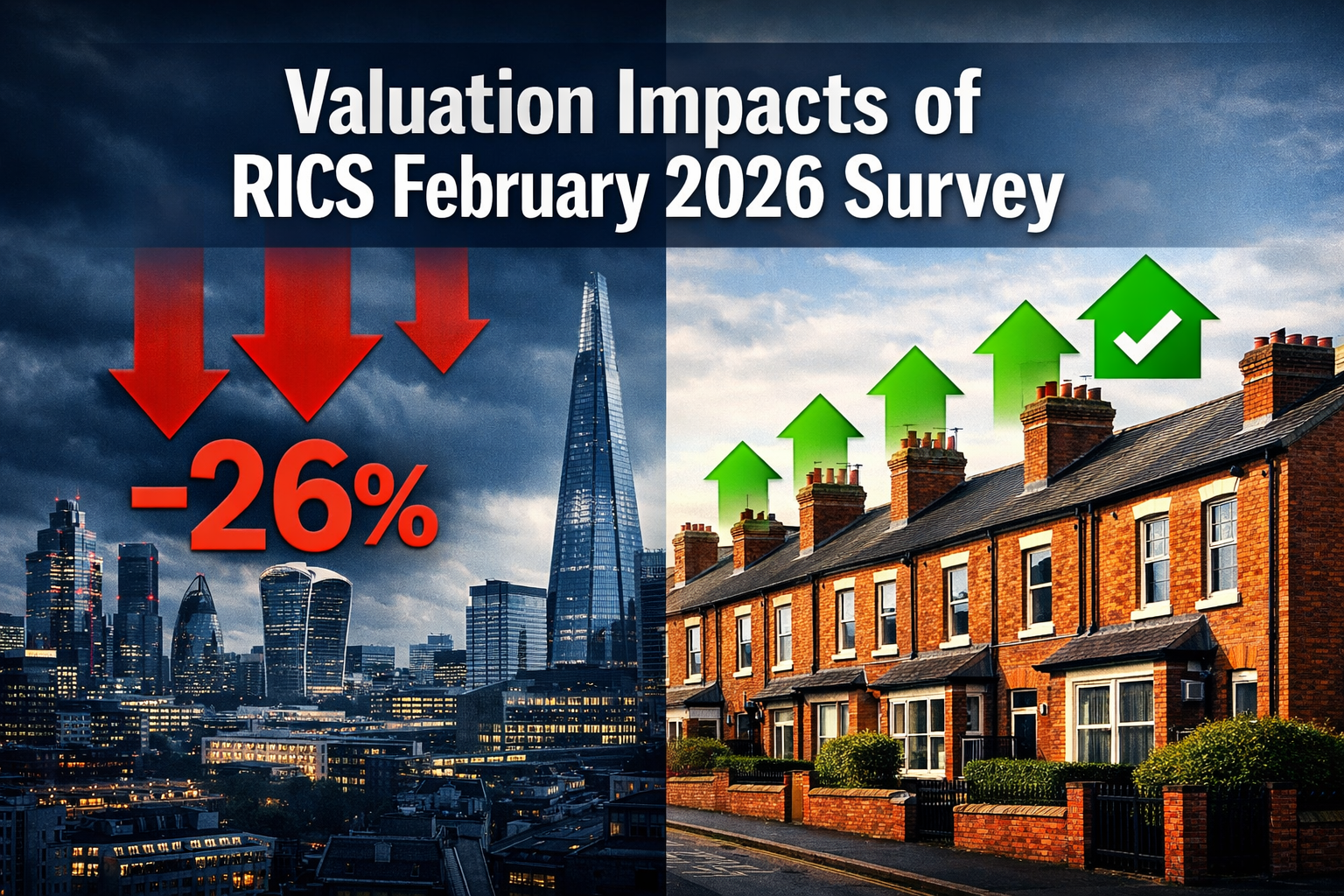

A single month erased months of cautious optimism: buyer enquiries collapsed to a net balance of -26% in February 2026, down sharply from -15% in January — a deterioration that demands immediate recalibration from every valuation professional operating across UK regional markets [1].

The Valuation Impacts of RICS February 2026 Survey: Adjusting for -26% Buyer Enquiry Dip in Cautious Regional Markets cannot be addressed with a single national adjustment figure. London's price balance crashed to -40%, while Northern Ireland and Scotland held comparatively firm. For valuers, lenders, and buyers navigating Q2 2026, understanding where the weakness is concentrated — and how to respond — is now the central professional challenge [1][4].

This article unpacks the February 2026 RICS data, translates the headline numbers into actionable valuation methodology, and provides region-by-region guidance for practitioners adjusting assessments in a rapidly shifting market.

Key Takeaways 📌

- Buyer enquiries fell to -26% in February 2026, reversing early-year improvements and signalling a fresh demand shock across UK housing markets [1]

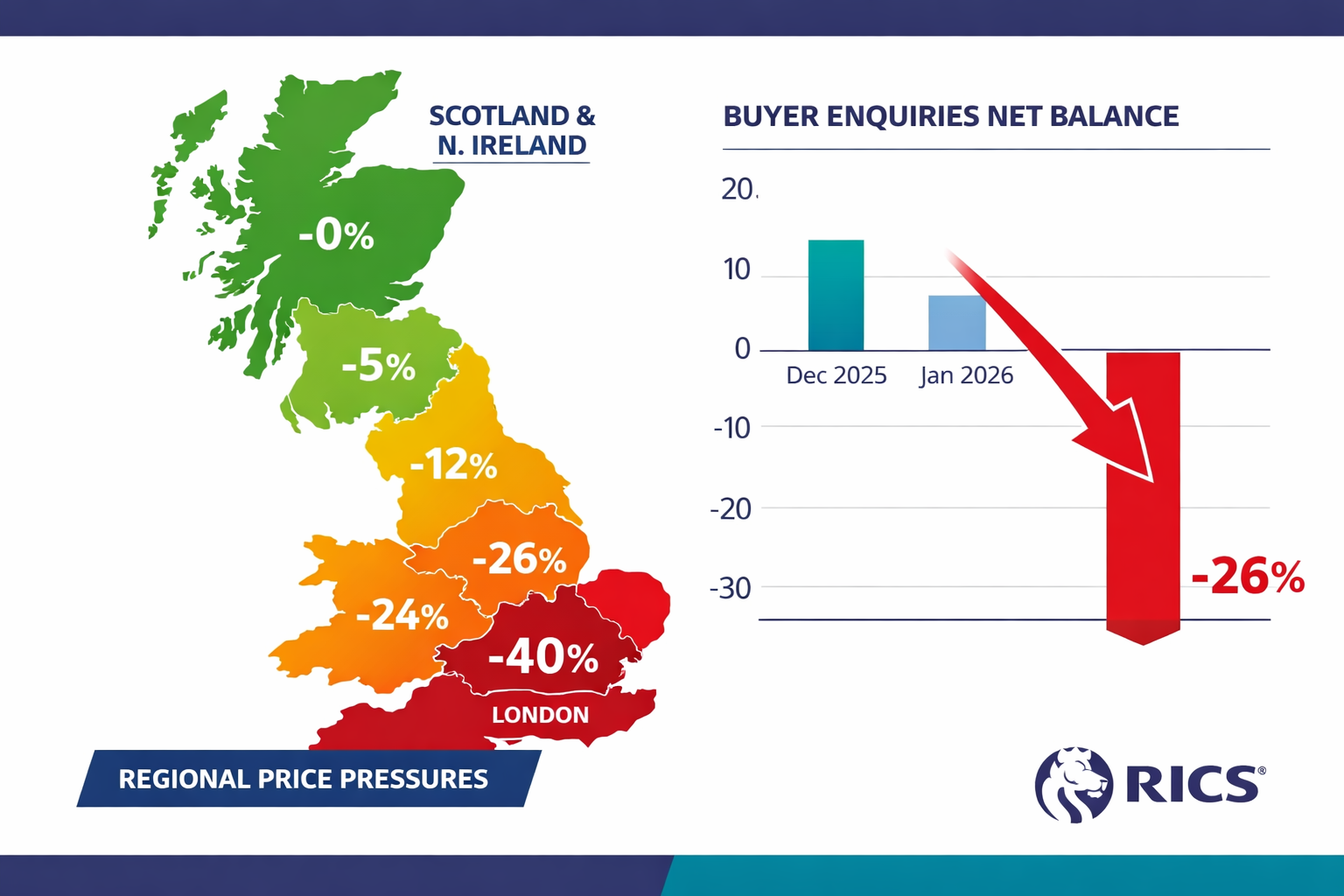

- Regional divergence is extreme: London (-40%), East Anglia (-26%), and the South East (-24%) face the sharpest downward price pressure, while northern regions remain comparatively resilient [1]

- Near-term price expectations dropped to -18%, requiring valuers to apply short-term downward adjustments, especially in southern markets [1][3]

- Macroeconomic headwinds — elevated mortgage rates, rising energy prices, and geopolitical uncertainty — are suppressing buyer sentiment beyond seasonal norms [1]

- 12-month price expectations remain positive at +33%, suggesting medium-term recovery is anticipated, but timing uncertainty has grown significantly [1][3]

Understanding the February 2026 RICS Data: What the Numbers Really Mean

The Buyer Enquiry Collapse in Context

The February 2026 RICS UK Residential Market Survey delivered a stark message. New buyer enquiries registered a net balance of -26%, representing a significant acceleration of the decline from January's -15% [1][3]. This is not a minor statistical blip — it reflects a genuine pullback in buyer confidence across the country.

💬 "The February 2026 survey documented a market reversal that caught many industry observers off-guard after modest improvements seen in December and January." [2]

To understand the severity, consider the trajectory:

| Month | Buyer Enquiry Net Balance | Agreed Sales Net Balance |

|---|---|---|

| December 2025 | Modest improvement | Tentative recovery |

| January 2026 | -15% | -9% |

| February 2026 | -26% | -12% |

Agreed sales also weakened to -12% in February, down from -9% in January [3]. Transaction momentum is softening in tandem with demand — a combination that creates compounding pressure on valuations.

Price Expectations: Short-Term Pain, Medium-Term Caution

The near-term price outlook deteriorated sharply. The 3-month price expectation balance fell to -18%, down from -6% in January [1][3]. This is a critical signal for valuers: the professional consensus now anticipates continued price weakness in the short term.

Meanwhile, 12-month price expectations moderated to +33% from +43% in January [1][3]. Recovery is still anticipated, but with less conviction and a less defined timeline. Near-term sales expectations weakened to -2%, compared to more optimistic readings earlier in the year [1].

What this means for valuers:

- Short-term (0–3 months): Apply downward adjustments, particularly in affected regions

- Medium-term (3–12 months): Maintain cautious optimism but avoid over-relying on 2025 comparable evidence

- Long-term: The +17% 12-month forward sales expectation suggests the market has not fundamentally broken down [1]

The Macroeconomic Drivers Behind the Dip

The February deterioration was not random. Rising oil and energy prices during the month increased the probability that mortgage rates will remain elevated for longer than previously anticipated [1]. Geopolitical concerns added a further layer of uncertainty that suppressed buyer sentiment beyond typical seasonal patterns.

This matters for RICS property valuations because affordability constraints directly affect the pool of active buyers — and a smaller, more cautious buyer pool changes the evidence base valuers must work with.

Valuation Impacts of RICS February 2026 Survey: Regional Divergence and Adjustment Strategies

The Regional Picture: A Market of Stark Contrasts

RICS identified regional divergence as the most striking feature of the February 2026 data [4]. The national headline figures mask enormous variation that requires differentiated professional strategies.

Regional Price Balance Summary — February 2026:

| Region | Price Net Balance | Pressure Level |

|---|---|---|

| 🔴 London | -40% | Severe |

| 🟠 East Anglia | -26% | High |

| 🟠 South East | -24% | High |

| 🟡 National Average | -12% | Moderate |

| 🟢 Northern Ireland | Positive | Firm |

| 🟢 Scotland | Positive | Firm |

| 🟢 North West England | Positive | Firm |

Source: RICS UK Residential Market Survey, February 2026 [1]

This divergence is not new, but its magnitude in February 2026 is exceptional. A London valuation and a Manchester valuation cannot be approached with the same methodology or the same comparable selection criteria.

Adjusting Valuations in High-Pressure Southern Markets

For practitioners working in London, the South East, and East Anglia, the February 2026 data requires specific adjustments:

1. Comparable Evidence Weighting

Sales evidence from Q3–Q4 2025 should be treated with caution. With a -40% price balance in London and a -18% near-term expectation nationally [1][3], comparables older than 3–4 months may overstate current market value. Weight recent evidence more heavily, even if the sample size is smaller.

2. Time Adjustments

Apply negative time adjustments to comparables from periods of stronger sentiment. The shift from January to February 2026 alone represents a meaningful deterioration — valuers should not assume a stable market when adjusting for time.

3. Marketing Period Assumptions

A -26% buyer enquiry balance means fewer active buyers. Valuers should extend assumed marketing period estimates in affected regions, which in turn affects average price reduction after survey negotiations and the likelihood of price reductions post-survey.

4. Caveat Language

Given the pace of change, valuations in high-pressure markets should include explicit caveats noting the rapidly shifting market conditions and the potential for further adjustment if conditions deteriorate before exchange.

Maintaining Rigour in Resilient Northern Markets

Northern Ireland, Scotland, and the North West of England present a different challenge: avoiding the temptation to apply national pessimism to locally firm markets [1].

For valuers in these regions:

- Comparable selection should prioritise local evidence over national trend data

- Positive price balances do not mean unlimited upside — apply standard prudence

- Monitor whether southern weakness eventually transmits northward, as it historically has done with a lag

Understanding why RICS surveyors are the benchmark for professional standards becomes especially important when regional conditions diverge so sharply from national narratives.

The Midlands and Transitional Markets

Markets sitting between the southern pressure zones and northern resilience — including parts of the Midlands and Yorkshire — require particular care. These transitional markets may show mixed signals within the same postcode area. Valuers should:

- Segment comparable evidence by sub-market rather than broad regional averages

- Engage with local agents to understand current buyer enquiry volumes at the micro level

- Cross-reference RICS data with local transaction data from HM Land Registry

Valuation Impacts of RICS February 2026 Survey: Practical Methodology for Q2 2026

Adapting Survey and Valuation Practice to Weak Demand Conditions

The Valuation Impacts of RICS February 2026 Survey: Adjusting for -26% Buyer Enquiry Dip in Cautious Regional Markets extend beyond price adjustments. The survey data should inform the entire professional approach to property assessment in Q2 2026.

Strengthening the Evidence Base

In a market where sentiment shifts rapidly, the quality of comparable evidence matters more than ever. Valuers should:

- ✅ Use a minimum of 5 comparables where possible, with at least 3 from the past 90 days

- ✅ Clearly document any time adjustments applied and their rationale

- ✅ Note the buyer enquiry environment at the time of comparable sales

- ✅ Cross-reference asking prices with achieved prices — the gap is widening in southern markets

A thorough homebuyers report provides the physical condition context that underpins defensible valuations, particularly when market conditions are volatile.

The Role of Condition in a Buyer-Cautious Market

When buyer enquiries fall sharply, property condition becomes a more powerful valuation driver. Cautious buyers in a -26% enquiry environment are selective — they discount heavily for defects that might have been overlooked in a competitive market.

This amplifies the importance of thorough physical inspection. Issues such as damp, structural movement, or roof condition that might have attracted modest adjustments in a buoyant market can now trigger disproportionate buyer resistance. Valuers should:

- Apply larger condition-related adjustments in markets with high buyer caution

- Reflect the reduced pool of buyers willing to take on properties requiring significant work

- Consider whether properties with known defects are genuinely marketable at assessed values within a reasonable timeframe

For properties with specific condition concerns, a condition survey report provides the detailed evidence base that supports robust valuation adjustments.

Communicating Uncertainty to Clients

One of the most important — and often underemphasised — aspects of valuation practice in volatile conditions is clear communication of uncertainty. RICS standards require valuers to reflect market conditions accurately [6], and February 2026's data creates a genuine obligation to communicate:

- The direction and pace of market change

- The specific regional context of the valuation

- The limitations of comparable evidence in a rapidly shifting market

- The potential for value to differ materially if conditions change before transaction completion

💬 "Valuers operating in extreme or rapidly shifting conditions must ensure their reports reflect the evidential limitations of the current market environment." [5]

Clients — whether lenders, buyers, or sellers — deserve to understand that a February 2026 valuation in London carries greater uncertainty than a valuation in a stable market. This is not a weakness in professional practice; it is a mark of rigour.

Choosing the Right Survey Type in a Cautious Market

In a market where buyer caution is elevated and condition-related discounts are amplified, the choice of survey type matters significantly. Buyers considering properties in affected regions should understand the difference between survey levels and choose accordingly.

A homebuyers report or building survey comparison is especially relevant in Q2 2026: a more comprehensive building survey provides the detailed condition evidence that supports confident negotiation in a market where sellers may resist price reductions despite weakening demand.

Lender Valuation Considerations

For mortgage valuations specifically, the February 2026 data creates additional obligations:

- Loan-to-value sensitivity: In markets with -18% near-term price expectations, LTV assessments should reflect the possibility of further short-term decline

- Reinspection triggers: Consider whether market movement warrants reinspection provisions in long-dated mortgage offers

- Portfolio valuations: Lenders with significant London or South East exposure should review portfolio assumptions against the -40% London price balance

The Bigger Picture: What February 2026 Tells Us About Q2 and Beyond

A Market at a Crossroads

The February 2026 RICS survey data presents a market that is neither in freefall nor on a clear recovery path. The +17% 12-month forward sales expectation [1] suggests industry professionals believe activity will improve — but the collapse in near-term sentiment to -2% indicates that improvement is not imminent.

For valuation professionals, this creates a specific operating environment:

- Short-term: Defensive, evidence-heavy, regionally differentiated valuations

- Medium-term: Monitor monthly RICS releases closely for signs of stabilisation

- Long-term: The structural undersupply of UK housing has not changed — medium-term recovery remains the base case

Regional Strategy Summary

| Region | Valuation Approach | Key Adjustment |

|---|---|---|

| London | Defensive; weight recent evidence heavily | Significant downward time adjustments |

| South East / East Anglia | Cautious; extended marketing period | Moderate-to-significant adjustments |

| Midlands / Yorkshire | Mixed signals; sub-market analysis essential | Selective adjustments |

| North West / Scotland / N. Ireland | Maintain local evidence primacy | Minimal national trend adjustments |

Staying Current with RICS Standards

In rapidly changing conditions, adherence to RICS home survey standards [6] is not just a compliance requirement — it is the professional framework that protects both clients and practitioners. Valuers should review their reporting templates to ensure caveat language and market commentary sections adequately reflect February 2026 conditions.

Conclusion: Actionable Next Steps for Valuation Professionals in Q2 2026

The Valuation Impacts of RICS February 2026 Survey: Adjusting for -26% Buyer Enquiry Dip in Cautious Regional Markets demand a structured, regionally differentiated response. The February data is not a reason for panic — but it is a clear signal that the valuation methodology applied in late 2025 or early January 2026 needs recalibration.

Immediate actions for valuation professionals:

- 🗺️ Segment your practice by region — apply the RICS regional breakdown to your own instruction pipeline and identify which markets require the most significant adjustments

- 📊 Update comparable databases — flag all comparables older than 90 days for time adjustment review, particularly in London and the South East

- 📝 Strengthen caveat language — ensure all valuation reports issued in Q2 2026 explicitly reference current market conditions and the limitations of the evidence base

- 🤝 Engage with local agents — the RICS survey provides macro signals; local agent intelligence provides the micro-level buyer enquiry data that sharpens regional adjustments

- 📅 Monitor monthly RICS releases — the March 2026 survey will be critical in confirming whether February was an outlier or the beginning of a sustained deterioration

- 🏠 Advise clients on survey depth — in a cautious market, recommending a more comprehensive survey type protects both the client and the professional relationship

The UK property market in Q2 2026 rewards precision. Valuers who apply national averages to regional realities will produce reports that serve neither their clients nor their professional obligations. Those who engage rigorously with the regional evidence — and communicate uncertainty honestly — will deliver the quality of assessment that this complex market demands.

References

[1] UK Residential Survey February 2026 – https://www.rics.org/news-insights/uk-residential-survey-february-2026

[2] Valuation Challenges in Weak Buyer Demand RICS February 2026 Survey Analysis and Surveyor Strategies – https://nottinghillsurveyors.com/blog/valuation-challenges-in-weak-buyer-demand-rics-february-2026-survey-analysis-and-surveyor-strategies

[3] UK Residential Market Survey February 2026 – https://www.rics.org/content/dam/ricsglobal/documents/market-surveys/uk-residential-market-survey/UK-Residential-Market-Survey_February-2026.pdf

[4] Valuation Impacts of February 2026 RICS Survey Strategies for Regional Price Divergence in UK Markets – https://nottinghillsurveyors.com/blog/valuation-impacts-of-february-2026-rics-survey-strategies-for-regional-price-divergence-in-uk-markets

[5] Real Estate Valuation Extreme Conditions – https://ww3.rics.org/uk/en/journals/property-journal/real-estate-valuation-extreme-conditions.html

[6] Home Survey Standards – https://www.rics.org/profession-standards/rics-standards-and-guidance/sector-standards/building-surveying-standards/home-surveys/home-survey-standards