Total construction spending is projected to reach $2.27 trillion in 2026, representing 5.1% year-on-year growth, yet beneath these headline figures lies a dramatically shifting landscape [2]. While buyer enquiries remain subdued in Q2 2026, property surveyors who understand which property types demonstrate resilience can position themselves strategically for the stabilization ahead. Building survey demand forecasting in cautious markets: identifying property types with resilience as buyer enquiries stabilise has become essential for surveyors navigating this complex environment.

The residential market outlook has been revised downward to just 2.3% growth for 2026—a stark contrast to the previously projected 9.7%—while nonresidential building construction has been upgraded to 6.5% growth [2]. This divergence signals fundamental shifts in where survey demand will concentrate, making accurate forecasting not just valuable but critical for business planning.

Key Takeaways

- Property type resilience varies dramatically: Data centers, civil infrastructure, and specific residential categories show exceptional strength while traditional residential markets face headwinds

- Survey demand follows construction cycles: Understanding which property types are attracting investment helps predict where RICS building survey demand will concentrate

- Market stabilization creates opportunities: Subdued enquiries in Q2 2026 mask longer-term positive expectations, rewarding surveyors who position proactively

- Regional variations matter significantly: Community counts rising 11% year-over-year indicate geographic shifts in where survey activity will concentrate [3]

- Forecasting accuracy drives competitive advantage: Surveyors who anticipate demand shifts can optimize resource allocation and marketing strategies

Understanding the Current Market Context for Building Survey Demand Forecasting

The Paradox of Cautious Optimism

The 2026 property market presents a fascinating paradox. While approximately 70% of builders describe market conditions as weaker than expected, new home sales in 2025 remained essentially in line with 2024 levels, demonstrating underlying resilience [3]. This disconnect between sentiment and performance creates both challenges and opportunities for building survey professionals.

Buyer enquiries have stabilized rather than collapsed, suggesting the market has found a temporary equilibrium. However, this stability requires significantly more sales effort per transaction [3], meaning each property moving toward completion faces more scrutiny. This environment naturally increases demand for thorough property assessments, particularly homebuyers reports and building surveys that provide buyers with confidence in uncertain conditions.

Structural Market Improvements Despite Headwinds

Community counts—the number of actively selling developments—have risen for 10 consecutive months with an 11% year-over-year increase [3]. This metric reveals that builders are positioning with broader geographic footprints and more active selling projects, even while maintaining cautious approaches to speculative construction.

For surveyors, this translates to:

✅ More diverse geographic demand across regions

✅ Sustained baseline survey volume from ongoing transactions

✅ Opportunities in emerging development areas where builders are expanding

✅ Increased need for local market expertise across multiple boroughs

The geographic expansion of building activity creates natural demand for surveyors with presence in areas like Stratford, Southwark, and Paddington, where development activity continues despite broader market caution.

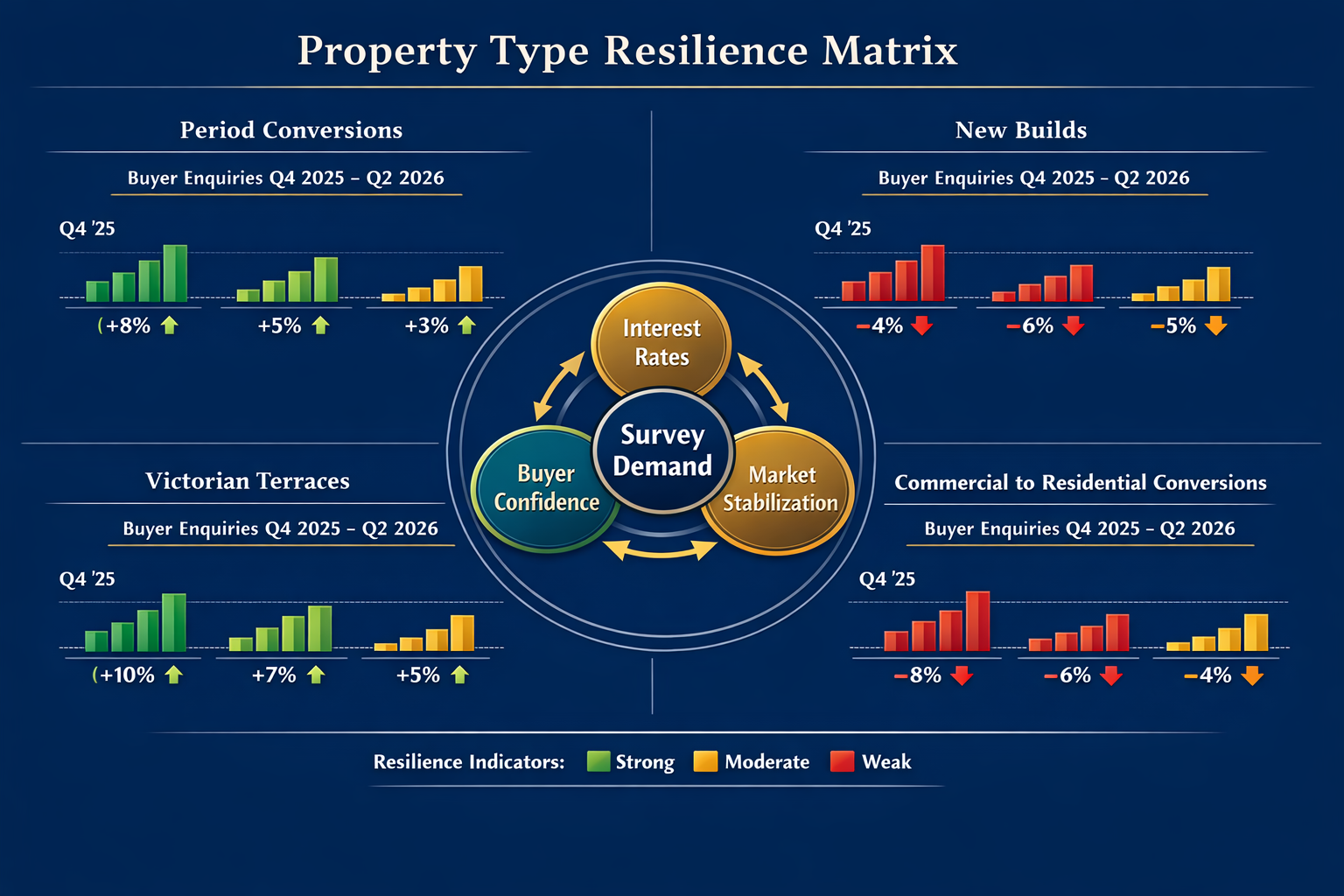

Building Survey Demand Forecasting in Cautious Markets: Property Types Showing Exceptional Resilience

Data Centers and Technology Infrastructure

The most dramatic resilience story in 2026 construction involves data centers and technology infrastructure. Private office spending—primarily driven by data centers—is expected to surge 25.2% in 2026, reaching a cumulative $659.3 billion through 2030 [2]. This represents an AI-fueled "investment supercycle" that shows no signs of slowing.

Survey Implications:

While data centers require specialized commercial survey expertise, the ripple effects extend to residential markets in proximity to these developments. Areas experiencing data center construction often see:

- Increased housing demand from technology workers

- Commercial-to-residential conversion opportunities

- Infrastructure upgrades benefiting surrounding properties

- Enhanced property values requiring updated valuations

Surveyors positioned near emerging technology hubs should anticipate sustained demand for both commercial assessments and residential surveys in adjacent areas.

Civil Engineering and Infrastructure Projects

Civil construction demonstrates remarkable strength, with 8.1% growth expected in 2026 and five-year spending forecast reaching $666 billion by 2030 (representing 33% cumulative increase) [2]. Infrastructure investment creates multiple survey demand channels:

| Infrastructure Type | Survey Demand Driver | Opportunity Scale |

|---|---|---|

| Transportation corridors | Property valuations for acquisitions | High |

| Utilities expansion | Easement and boundary surveys | Moderate |

| Public facilities | Pre-construction assessments | Moderate |

| Flood defenses | Property impact assessments | Growing |

Infrastructure projects often require specific defect surveys for properties potentially affected by construction, creating sustained demand throughout project timelines that can span multiple years.

Nonresidential Building with Selective Strength

Nonresidential building construction has been upgraded to 6.5% growth for 2026 [2], but this aggregate figure masks significant variation. Commercial properties demonstrate cautious optimism, with data center and energy infrastructure providing sustained momentum, while office, retail, and mixed-use properties face moderate, regionally-driven growth [4].

Resilient Nonresidential Categories:

🏢 Healthcare facilities: Demographic trends support sustained construction

🏭 Industrial and logistics: E-commerce infrastructure continues expanding

🏫 Educational institutions: Deferred maintenance and modernization projects

⚡ Energy infrastructure: Renewable energy and grid modernization investments

For surveyors, nonresidential resilience creates opportunities for diversification beyond traditional residential work, particularly for those with commercial survey capabilities or willingness to develop them.

Residential Market Segments with Relative Strength

While overall residential growth projections have been revised downward, specific segments demonstrate resilience worth targeting:

Period Properties and Conversions

Victorian and Edwardian properties requiring comprehensive building surveys continue attracting buyers seeking character and long-term value. These properties inherently require detailed assessments, creating consistent demand for RICS building surveys regardless of broader market conditions.

New Builds Requiring Independent Assessment

Despite flat housing starts outlook [3], buyers increasingly recognize the value of independent surveys even for new construction. The question "do you need a building survey for a new build" is being answered affirmatively more often as buyers seek protection beyond developer warranties.

Properties Requiring Specialist Surveys

Certain property conditions create non-discretionary survey demand:

- Properties with visible damp issues requiring specialist assessment

- Older properties where mortgage lenders mandate surveys

- Properties with structural concerns requiring expert evaluation

- Leasehold properties where comprehensive assessment protects buyers

Implementing Effective Building Survey Demand Forecasting Strategies

Geographic Market Intelligence

Effective forecasting begins with understanding where construction activity and buyer interest are concentrating. The 11% year-over-year increase in community counts [3] indicates geographic dispersion of development activity, creating opportunities for surveyors who track these patterns.

Actionable Geographic Strategies:

- Monitor planning applications in your service areas to anticipate future survey demand

- Track infrastructure investment announcements that signal emerging hotspots

- Analyze transaction volume trends by borough and property type

- Establish presence in multiple locations to capture geographically diverse demand

Surveyors serving diverse areas—from Knightsbridge to Bromley, Fulham to Hackney—position themselves to capture demand regardless of where market activity concentrates.

Leading Indicators for Survey Demand

Building survey demand doesn't occur in isolation—it follows predictable leading indicators that enable forecasting:

Primary Leading Indicators:

📊 Mortgage approval volumes: Typically lead survey demand by 2-4 weeks

🏗️ Planning permission approvals: Signal future construction and survey needs

📈 Property listing volumes: Increased inventory eventually drives transactions

💷 Interest rate expectations: Influence buyer confidence and market entry timing

🔍 Search activity on property portals: Indicates buyer interest before enquiries

By monitoring these indicators, surveyors can anticipate demand shifts before they materialize in enquiry volumes, enabling proactive resource planning and marketing adjustments.

Repair and Remodel Surge Opportunity

One of the most significant opportunities for 2026 involves repair and remodel spending, which is expected to increase mid-single digits in 2026 versus 2025, then accelerate to high single-digit growth in 2027 as deferred projects accumulate [3].

This trend creates multiple survey opportunities:

- Pre-renovation condition surveys establishing baseline property state

- Structural assessments for properties requiring significant alterations

- Party wall surveys for properties undergoing extensions or conversions

- Post-renovation inspections verifying work quality

Surveyors who position themselves to capture this repair and remodel wave can offset potential weakness in traditional transaction-driven survey demand.

Technology-Enhanced Forecasting

Modern surveying practices increasingly incorporate technology for demand forecasting:

Forecasting Technology Tools:

- CRM systems tracking enquiry patterns and conversion rates over time

- Geographic information systems (GIS) mapping demand concentration

- Predictive analytics identifying seasonal and cyclical patterns

- Market intelligence platforms aggregating multiple data sources

Technology enables surveyors to move from reactive scheduling to proactive capacity planning, optimizing resource allocation and identifying growth opportunities before competitors.

Building Survey Demand Forecasting in Cautious Markets: Strategic Positioning for Stabilization

Communicating Value in Uncertain Markets

When buyer enquiries stabilize at subdued levels, the surveyors who thrive are those who effectively communicate value. Buyers in cautious markets are more risk-averse and require more reassurance [3], creating natural demand for professional property assessments.

Value Communication Strategies:

✨ Emphasize risk mitigation: Position surveys as insurance against costly surprises

📋 Showcase comprehensive reporting: Demonstrate thoroughness that justifies investment

🎯 Highlight negotiation leverage: Quantify how survey findings enable price adjustments

⏱️ Stress long-term protection: Frame surveys as protecting decade-long investments

Understanding whether clients need a homebuyers report or structural survey and guiding them appropriately builds trust and positions surveyors as advisors rather than mere service providers.

Diversification Across Property Types

The divergence between residential (2.3% growth) and nonresidential (6.5% growth) construction in 2026 [2] argues strongly for diversification. Surveyors exclusively focused on residential work may face headwinds, while those with capabilities across property types can capture opportunities wherever they emerge.

Diversification Pathways:

- Develop commercial survey capabilities to access nonresidential growth

- Expand geographic service areas to capture regional variations

- Offer specialist surveys (damp, structural, party wall) beyond standard assessments

- Target emerging property types including conversions and renovations

Diversification doesn't require abandoning core competencies—it means strategically expanding to capture demand across the resilient property types identified in forecasting.

Building Strategic Partnerships

Cautious markets reward collaboration. Strategic partnerships enable surveyors to access demand channels and expertise beyond their direct capabilities:

High-Value Partnership Categories:

🤝 Estate agents and property portals: Direct access to buyers at decision points

🏦 Mortgage brokers and lenders: Referrals for required surveys

🔨 Builders and developers: Ongoing relationships for new construction

⚖️ Solicitors and conveyancers: Integration into transaction processes

🏢 Commercial property consultants: Access to nonresidential opportunities

Partnerships create resilience by diversifying enquiry sources, reducing dependence on any single demand channel that might weaken in cautious markets.

Capacity Planning for Longer-Term Growth

While 2026 presents challenges, mid and far-term forecasts anticipate consecutive years of 8% residential growth through 2029 [2]. This longer-term positive outlook argues for maintaining capacity and capability even during temporary weakness.

Capacity Planning Considerations:

- Retain skilled surveyors rather than contracting during temporary weakness

- Invest in training and technology positioning for anticipated growth

- Maintain marketing presence to capture market share when conditions improve

- Build financial reserves enabling sustained operations through cautious periods

Surveyors who maintain strategic perspective during temporary market caution position themselves to capture disproportionate share when growth accelerates.

Regional Variations and Local Market Dynamics

London Market Specifics

London's property market demonstrates unique characteristics requiring specialized forecasting approaches. The capital's market segmentation—from prime central London to outer boroughs—creates vastly different demand dynamics.

London-Specific Considerations:

Areas like Kensington and Notting Hill maintain resilience through international buyer interest, while areas like Barking and Newham demonstrate strength through first-time buyer activity and regeneration projects.

Surveyors serving London must recognize these variations and forecast demand at granular geographic levels rather than treating the capital as a homogeneous market.

Emerging Suburban and Regional Markets

The sustained increase in community counts [3] reflects builders expanding into suburban and regional markets where affordability and space attract buyers. Areas previously considered secondary markets are experiencing development activity that drives survey demand.

Emerging Market Indicators:

- Infrastructure investment announcements (rail, roads, utilities)

- Major employer relocations or expansions

- Planning policy changes encouraging development

- Demographic shifts toward specific regions

Surveyors willing to expand service areas into emerging markets can capture growth unavailable in saturated central locations.

Conclusion

Building survey demand forecasting in cautious markets: identifying property types with resilience as buyer enquiries stabilise represents both challenge and opportunity for property surveyors in 2026. While overall residential growth projections have been revised downward to 2.3%, significant opportunities exist for surveyors who understand where resilience concentrates.

Key Strategic Imperatives:

The data reveals clear winners: data centers and technology infrastructure (25.2% growth), civil engineering projects (8.1% growth), and nonresidential building (6.5% growth) demonstrate exceptional resilience [2]. Residential markets show selective strength in period properties, specialist survey requirements, and repair/remodel activity expected to accelerate through 2027 [3].

Actionable Next Steps:

- Audit your current client mix against resilient property types identified

- Develop geographic market intelligence systems tracking leading indicators

- Invest in capabilities enabling diversification beyond traditional residential work

- Build strategic partnerships accessing multiple demand channels

- Communicate value effectively to risk-averse buyers requiring reassurance

- Maintain long-term perspective recognizing 8% annual growth projections through 2029

The surveyors who thrive in 2026's cautious market will be those who recognize that subdued enquiries don't equal absent opportunity—they simply require more strategic positioning. By focusing resources on resilient property types, maintaining geographic flexibility, and communicating value effectively, building survey professionals can not only navigate current caution but position themselves advantageously for the growth ahead.

The market has stabilized, not collapsed. For informed surveyors, stabilization creates the foundation for strategic growth.

References

[1] Survey Reveals Demand Uncertainty Is Changing 2026 Homebuilding Strategy – https://www.housingwire.com/articles/survey-reveals-demand-uncertainty-is-changing-2026-homebuilding-strategy/

[2] U.s. Put In Place Construction Forecast Report Spring 2026 Highlights – https://news.constructconnect.com/u.s.-put-in-place-construction-forecast-report-spring-2026-highlights

[3] 2026 Housing Market Outlook Sales Starts Trends – https://www.bldr.com/resources/blog/2026-housing-market-outlook-sales-starts-trends

[4] Engineering And Construction Industry Outlook – https://www.deloitte.com/us/en/insights/industry/engineering-and-construction/engineering-and-construction-industry-outlook.html