Buyer demand plummeted to -26% net balance in February 2026, marking one of the sharpest contractions in recent surveying history and forcing property valuers across the UK to fundamentally reconsider their assessment methodologies[1]. This dramatic shift, revealed in the latest RICS residential market survey, represents far more than a temporary market blip—it signals a profound transformation in how professional surveyors must approach valuations throughout Q2 2026 and beyond. The Valuation Strategy Shifts in Q2 2026: Interpreting RICS February Survey Data Amid Geopolitical Uncertainty and Regional Divergence have created an unprecedented challenge for property professionals navigating what has become a deeply fragmented market landscape.

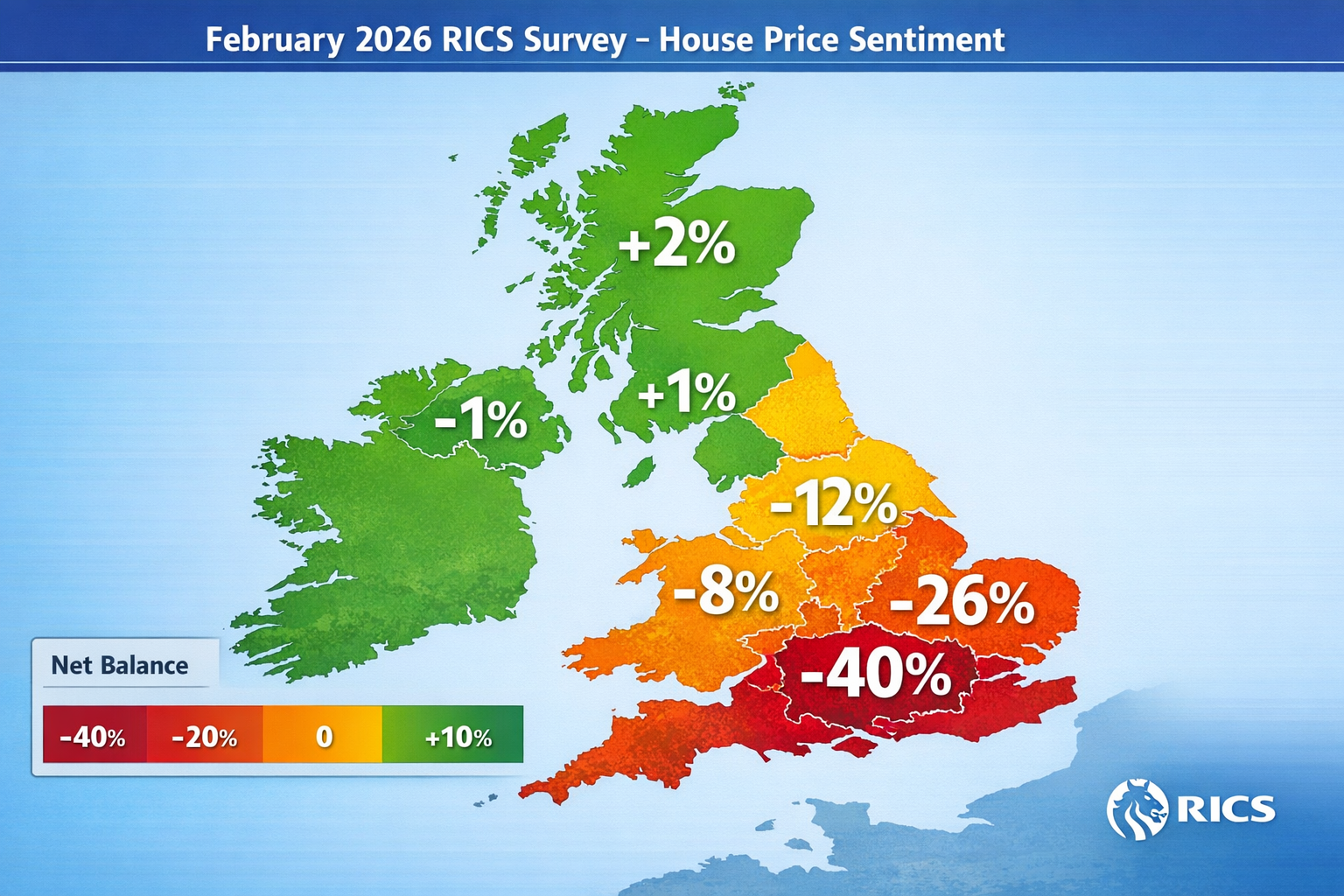

The February 2026 RICS survey data exposes a critical reality: London's property market cooled at -40% net balance while northern regions maintained relative stability, creating a valuation environment where national averages obscure more than they reveal[1]. For surveyors conducting RICS building surveys and valuations, this regional divergence demands immediate strategic recalibration.

Key Takeaways

- Buyer demand contracted sharply to -26% net balance in February 2026, creating significant challenges for comparable evidence reliability in property valuations[1]

- Regional price divergence reached extreme levels, with London experiencing -40% net balance while Northern Ireland, Scotland, and North West England showed resilience[1]

- Geopolitical uncertainty and interest rate concerns directly dampened buyer sentiment throughout February, requiring valuers to incorporate heightened risk adjustments[2]

- Transaction volume weakness at -12% net balance for agreed sales undermines the availability of recent comparable data, forcing greater reliance on alternative valuation methodologies[5]

- Forward-looking sentiment bifurcation between near-term Q2 weakness and longer-term stabilization expectations necessitates dual-horizon valuation frameworks[1]

Understanding the February 2026 RICS Survey Context

The Royal Institution of Chartered Surveyors (RICS) residential market survey for February 2026 presents a sobering picture of market conditions entering the second quarter. The headline figures reveal systematic weakness across multiple indicators, but the true story lies beneath these national averages.

National Market Indicators

Buyer demand fell to -26% net balance in February, representing a significant deterioration from January's -15% reading[1]. By March 2026, this figure had declined further to -39%, indicating accelerating weakness rather than stabilization[1]. This contraction creates immediate challenges for valuers who rely on active buyer interest to validate comparable evidence.

Agreed sales activity remained subdued at -12% net balance, reflecting the direct consequence of weakened demand[5]. When transaction volumes decline, the pool of recent comparable sales shrinks, forcing valuers to look further back in time or expand geographic search parameters—both approaches that introduce additional uncertainty.

National house prices registered a -12% net balance in February, representing only marginal negative movement compared to demand indicators[5]. This relative price stability amid collapsing demand suggests sellers have not yet fully adjusted expectations to market realities, creating potential valuation discrepancies.

Supply-Side Dynamics

Interestingly, new property instructions remained stable at +2% net balance, indicating a broadly neutral flow of fresh listings[5]. This supply stability contrasts sharply with demand weakness, typically a precursor to eventual price adjustments as inventory accumulates.

The rental market showed pronounced divergence: landlord instructions fell to -27% net balance, yet +20% of surveyors expected rental prices to rise over the coming three months[5]. This disconnect between transaction volume and price expectations reflects the structural undersupply in the rental sector, a factor that influences residential investment valuations.

Regional Divergence: The Critical Variable in Valuation Strategy Shifts in Q2 2026

Perhaps the most significant finding for valuation professionals is the pronounced regional asymmetry in price sentiment. The February 2026 RICS data reveals a market that can no longer be understood through national averages alone[1].

London and the South: Pronounced Cooling

London experienced the strongest downward pressure at -40% net balance, nearly double the national average[1]. For surveyors conducting valuations in areas like Wimbledon or Knightsbridge, this represents a fundamental shift in market dynamics that must be reflected in valuation assumptions.

East Anglia followed with -26% net balance, while the South East recorded -24%[1]. This southern concentration of weakness likely reflects several factors:

- 🏠 Higher absolute price levels making affordability constraints more binding

- 💼 Greater exposure to financial services employment affected by economic uncertainty

- 📊 Larger price gains during 2020-2022 creating more room for correction

- 🌍 International buyer withdrawal amid geopolitical tensions

Northern Regions: Relative Resilience

In stark contrast, Northern Ireland, Scotland, and the North West of England reported firmer price trends[1]. This resilience reflects different market fundamentals:

- More affordable entry points maintaining first-time buyer accessibility

- Less speculative activity during the previous boom cycle

- Regional economic diversification reducing vulnerability to specific sector shocks

- Lower international exposure insulating from global uncertainty

For valuers working across multiple regions, this divergence necessitates location-specific valuation frameworks rather than standardized national approaches. A valuation methodology appropriate for Islington may be wholly inappropriate for properties in Barnet or northern markets.

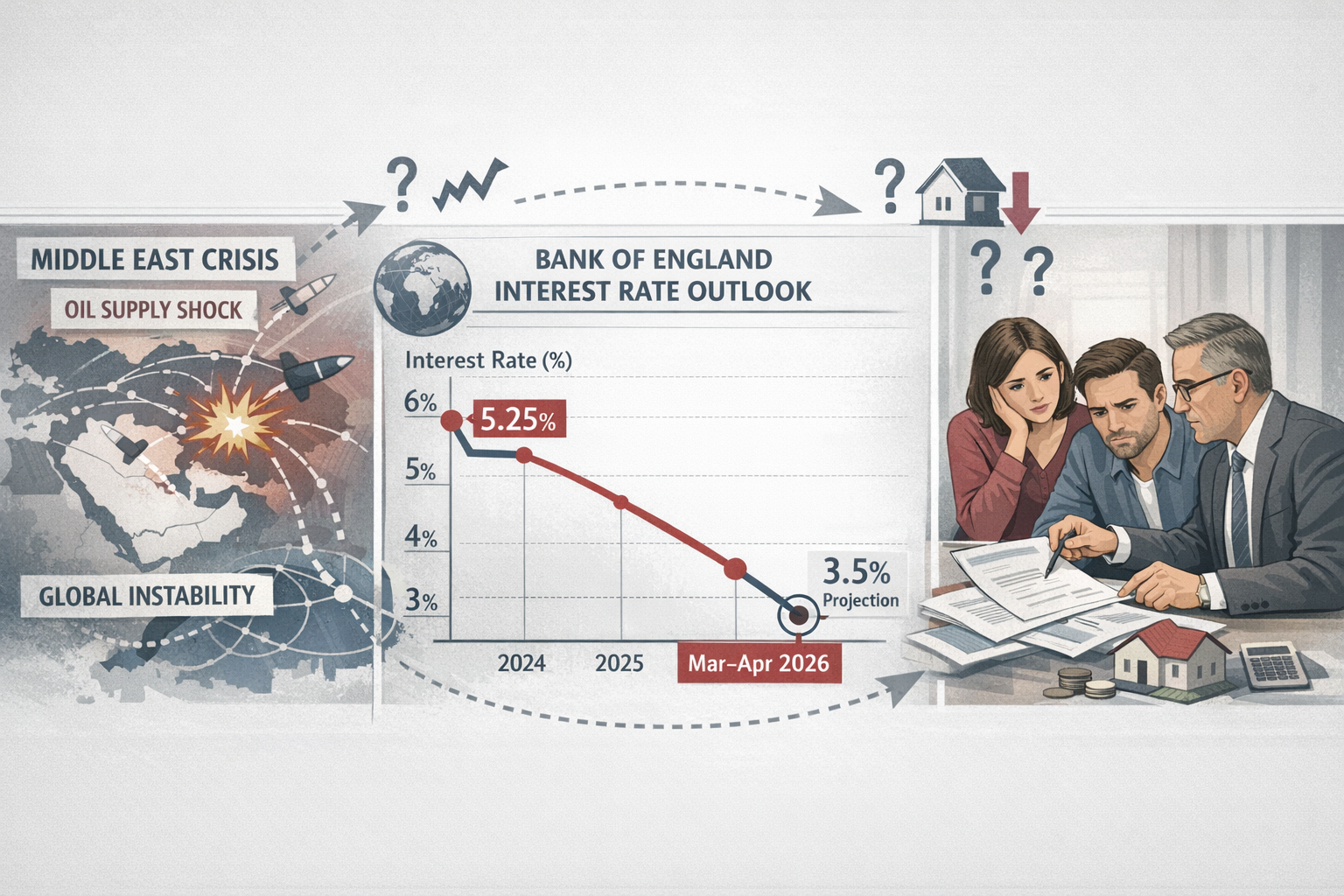

Geopolitical Uncertainty and Its Direct Impact on Valuation Methodologies

The February 2026 RICS survey explicitly identifies geopolitical uncertainty, particularly Middle East events, as a direct factor dampening buyer sentiment[2]. This represents a relatively unusual finding in residential market surveys, which typically focus on domestic economic factors.

Incorporating Geopolitical Risk into Valuations

For professional valuers, geopolitical uncertainty creates several specific challenges:

1. Increased Discount Rates

When conducting Red Book valuations, valuers must consider whether current market uncertainty justifies increased discount rates in income capitalization approaches. Geopolitical instability typically increases required returns, reducing present values.

2. Comparable Evidence Reliability

Transactions completed during periods of heightened uncertainty may not represent equilibrium market conditions. Valuers must exercise judgment in determining whether February-March 2026 comparables reflect temporary sentiment shocks or fundamental value shifts[4].

3. Forward-Looking Assumptions

Geopolitical uncertainty complicates growth rate assumptions in valuation models. The bifurcation between near-term weakness and longer-term expectations requires dual-horizon frameworks that explicitly model different scenarios[1].

Interest Rate Outlook Complexity

The Monetary Policy Committee's consideration of rate cuts to potentially 3.5% in March or April 2026 adds another layer of complexity[6]. Interest rate expectations affect valuations through multiple channels:

- Mortgage affordability calculations that determine buyer purchasing power

- Discount rate selection in income-based valuation approaches

- Investment property yield requirements as alternative investments become more or less attractive

- Development viability assessments where financing costs significantly impact residual land values

The challenge for valuers in Q2 2026 is that interest rate direction appears clear (downward), but timing and magnitude remain uncertain. This uncertainty itself becomes a valuation input, potentially justifying wider valuation ranges or explicit scenario modeling.

Practical Valuation Strategy Adjustments for Q2 2026

Given the market conditions revealed in the RICS February survey, professional valuers should consider several specific strategic adjustments for Q2 2026 work.

Enhanced Comparable Evidence Scrutiny

With buyer demand at -26% net balance, the reliability of comparable evidence faces specific challenges[4]. Valuers should:

Expand temporal search parameters cautiously: While recent comparables are scarce, reaching too far back risks capturing different market conditions. Consider weighting schemes that balance recency against sample size.

Increase geographic search radius selectively: Regional divergence means expanding search areas may introduce more variability than it resolves. Document the rationale for geographic boundaries clearly.

Weight adjusted comparables more heavily: Properties requiring significant adjustments may actually provide better evidence than superficially similar properties from different micro-markets.

Incorporate multiple valuation methods: When comparable evidence is weak, triangulation using income capitalization, cost approach, or automated valuation model (AVM) benchmarking provides validation[4].

Regional Stratification Requirements

The pronounced regional divergence documented in the February survey demands explicit regional stratification in valuation approaches:

| Region | Net Balance | Valuation Adjustment |

|---|---|---|

| London | -40% | Apply heightened caution; consider 5-10% uncertainty range expansion |

| East Anglia | -26% | Moderate downward pressure; standard uncertainty ranges |

| South East | -24% | Moderate downward pressure; monitor transaction volumes |

| Northern Ireland | Positive | Relative stability; standard approaches appropriate |

| Scotland | Positive | Relative stability; standard approaches appropriate |

| North West | Positive | Relative stability; standard approaches appropriate |

For firms operating across multiple regions, standardized national valuation templates may no longer be appropriate. Consider developing region-specific valuation frameworks that explicitly account for local market dynamics.

Client Communication Enhancement

The complexity revealed in the Valuation Strategy Shifts in Q2 2026: Interpreting RICS February Survey Data Amid Geopolitical Uncertainty and Regional Divergence requires enhanced client communication. Valuers should:

✅ Explicitly discuss market uncertainty in valuation reports, referencing RICS survey data to contextualize findings

✅ Provide scenario analysis where appropriate, showing valuation sensitivity to key assumptions

✅ Explain regional context clearly, particularly when national media coverage may not reflect local conditions

✅ Document methodology choices more thoroughly, explaining why specific approaches were selected given current market conditions

✅ Recommend revaluation triggers, identifying circumstances that would warrant reassessment

This enhanced communication approach aligns with professional standards while managing client expectations in an uncertain environment.

Alternative Valuation Methodologies

When transaction-based comparable evidence proves insufficient, valuers should consider greater reliance on alternative approaches:

Income Capitalization Method: For investment properties, this approach may provide more stable valuation anchors when transaction volumes are weak. However, capitalize rates must reflect current market risk perceptions.

Cost Approach: While typically a method of last resort for residential properties, the cost approach provides a useful floor value in markets with limited transaction evidence.

Automated Valuation Models (AVMs): While not suitable as primary valuation methods for formal purposes, AVMs can provide useful benchmarking and validation, particularly when they incorporate recent market trend data.

Hedonic Pricing Models: Statistical approaches that decompose property values into component attributes may help interpolate values when direct comparables are scarce.

The key is methodological transparency—clearly documenting which approaches were used, why they were selected, and how they were weighted in reaching final value conclusions.

Forward-Looking Considerations for Q2 2026 and Beyond

The RICS February 2026 survey reveals bifurcated sentiment between near-term weakness and longer-term expectations. Near-term sales expectations softened to -2%, yet twelve-month expectations remained positive[1]. This bifurcation creates specific challenges for valuers.

Dual-Horizon Valuation Frameworks

Professional valuers should consider adopting dual-horizon frameworks that explicitly distinguish between:

Near-term valuations (Q2-Q3 2026): Reflect current market weakness, limited transaction evidence, and heightened uncertainty. Apply conservative assumptions and wider valuation ranges.

Medium-term expectations (12+ months): Incorporate anticipated interest rate cuts, potential geopolitical stabilization, and market normalization. Use for investment analysis and strategic planning purposes.

This bifurcation should be made explicit in valuation reports, helping clients understand that current market values may not reflect medium-term equilibrium conditions.

Monitoring Key Indicators

Valuers should establish systematic monitoring of key indicators that would signal material changes requiring valuation reassessment:

📊 Monthly RICS survey releases: Track whether demand and price indicators stabilize, deteriorate further, or begin recovering

📊 Bank of England policy decisions: Monitor actual interest rate changes versus market expectations

📊 Regional transaction volume data: Watch for signs of regional divergence narrowing or widening

📊 Geopolitical developments: Track whether Middle East tensions escalate, stabilize, or resolve

📊 Economic growth indicators: Monitor UK GDP, employment, and wage growth data that affect housing affordability

Professional Development Priorities

The market complexity revealed in the Valuation Strategy Shifts in Q2 2026: Interpreting RICS February Survey Data Amid Geopolitical Uncertainty and Regional Divergence highlights several professional development priorities for valuers:

- Advanced statistical methods for handling limited comparable evidence

- Regional market analysis capabilities to understand local dynamics

- Scenario modeling techniques for incorporating uncertainty explicitly

- Alternative valuation methodologies beyond simple comparable sales approaches

- Risk communication skills for explaining complex market conditions to clients

Firms should consider whether their valuation teams have adequate training in these areas, particularly for junior staff who may have limited experience valuing in challenging market conditions.

Integration with Broader Survey and Valuation Services

The valuation challenges identified in the RICS February 2026 data don't exist in isolation—they interact with broader RICS survey services that property professionals provide.

Building Survey Implications

When conducting building surveys, the current market environment affects several considerations:

Repair cost negotiations: Weak buyer demand strengthens purchaser negotiating positions when defects are identified. Surveyors should provide clear repair cost estimates that buyers can use effectively. Research shows significant average price reductions after surveys are achievable.

Survey level recommendations: Market uncertainty may justify recommending more comprehensive Level 3 surveys over Level 2 reports, providing buyers with maximum information to support confident decision-making.

Timing considerations: With transaction volumes weak, buyers have more time for thorough due diligence. Surveyors can provide more detailed investigations without delaying competitive purchase timelines.

Specialized Survey Services

Certain specialized services become particularly relevant in uncertain markets:

Stock condition surveys: For portfolio owners, understanding maintenance liabilities becomes critical when property values face downward pressure.

Monitoring surveys: Structural movement concerns may receive heightened attention when buyers are more cautious and risk-averse.

Schedule of condition: Documenting property condition becomes more important when market uncertainty increases the likelihood of disputes.

Cost Transparency and Value Communication

In a market where buyers are cautious and transaction volumes are weak, clear communication about property survey expenses and the value surveys provide becomes essential. Surveyors should emphasize how professional surveys can save money by identifying defects before purchase completion.

Understanding which home survey is right for specific circumstances helps clients make informed decisions about survey investment levels appropriate to their risk tolerance and property characteristics.

Conclusion: Navigating Q2 2026 with Strategic Clarity

The Valuation Strategy Shifts in Q2 2026: Interpreting RICS February Survey Data Amid Geopolitical Uncertainty and Regional Divergence represent more than temporary market turbulence—they signal a fundamental recalibration of the UK residential property market. The February 2026 RICS survey data reveals a market characterized by sharp demand contraction (-26% net balance), pronounced regional divergence (London at -40% versus northern resilience), and heightened uncertainty from geopolitical tensions and interest rate expectations[1][2].

For professional valuers, these conditions demand immediate strategic adjustments: enhanced comparable evidence scrutiny, explicit regional stratification, alternative valuation methodology deployment, and improved client communication frameworks. The bifurcation between near-term weakness and longer-term stabilization expectations requires dual-horizon valuation approaches that help clients understand current market values may not reflect medium-term equilibrium conditions.

Actionable Next Steps

For valuation professionals:

- Review and update valuation templates to incorporate regional stratification and enhanced uncertainty documentation

- Establish systematic monitoring of RICS monthly survey releases and key economic indicators

- Invest in professional development focused on alternative valuation methodologies and statistical techniques

- Enhance client communication protocols to explain market complexity and valuation uncertainty clearly

- Document methodology choices more thoroughly, explaining rationale given current market conditions

For property buyers and investors:

- Engage qualified surveyors with demonstrated understanding of current market dynamics and regional variations

- Request scenario analysis in valuation reports to understand sensitivity to key assumptions

- Consider comprehensive building surveys to maximize information in an uncertain market

- Understand regional context rather than relying on national market commentary

- Establish revaluation triggers to identify when reassessment becomes necessary

The complexity revealed in the February 2026 RICS survey underscores the critical value that professional surveyors provide in uncertain markets. By adapting valuation strategies to reflect current realities—regional divergence, geopolitical uncertainty, and transaction volume weakness—valuers can continue delivering reliable, defensible valuations that serve client needs and maintain professional standards throughout Q2 2026 and beyond.

References

[1] Uk Residential Survey February 2026 – https://www.rics.org/news-insights/uk-residential-survey-february-2026

[2] Uk Rics Residential Market Survey Feb 2026 – https://www.capitaleconomics.com/publications/uk-housing-market-update/uk-rics-residential-market-survey-feb-2026

[3] Valuation Impacts Of February 2026 Rics Survey Strategies For Regional Price Divergence In Uk Markets – https://nottinghillsurveyors.com/blog/valuation-impacts-of-february-2026-rics-survey-strategies-for-regional-price-divergence-in-uk-markets

[4] Valuation Challenges In Uncertain Markets Using Rics February 2026 Data To Adjust Valuations Amid Geopolitical Volatility And Interest Rate Concerns – https://nottinghillsurveyors.com/blog/valuation-challenges-in-uncertain-markets-using-rics-february-2026-data-to-adjust-valuations-amid-geopolitical-volatility-and-interest-rate-concerns

[5] Uk Residential Market Survey February 2026 – https://www.rics.org/content/dam/ricsglobal/documents/market-surveys/uk-residential-market-survey/UK-Residential-Market-Survey_February-2026.pdf

[6] Uk Economy Property Update February 2026 – https://www.rics.org/content/dam/ricsglobal/documents/market-surveys/uk-economy-property-update-february-2026.pdf