The spring selling season stumbled at the starting line. The UK house prices March 2026 Halifax index recorded a 0.5% monthly fall — reversing February's modest 0.3% rise — pushing the national average to £299,677 and slowing annual growth to just 0.8%. For homeowners and buyers in Wimbledon and South West London, where property values sit well above the national average, this shift in momentum demands careful attention.

This article unpacks what the latest Halifax data really means, how it compares with Nationwide's figures, what's driving the slowdown, and — critically — what you should do next if you're considering a sale or purchase in the current climate.

Key Takeaways 📌

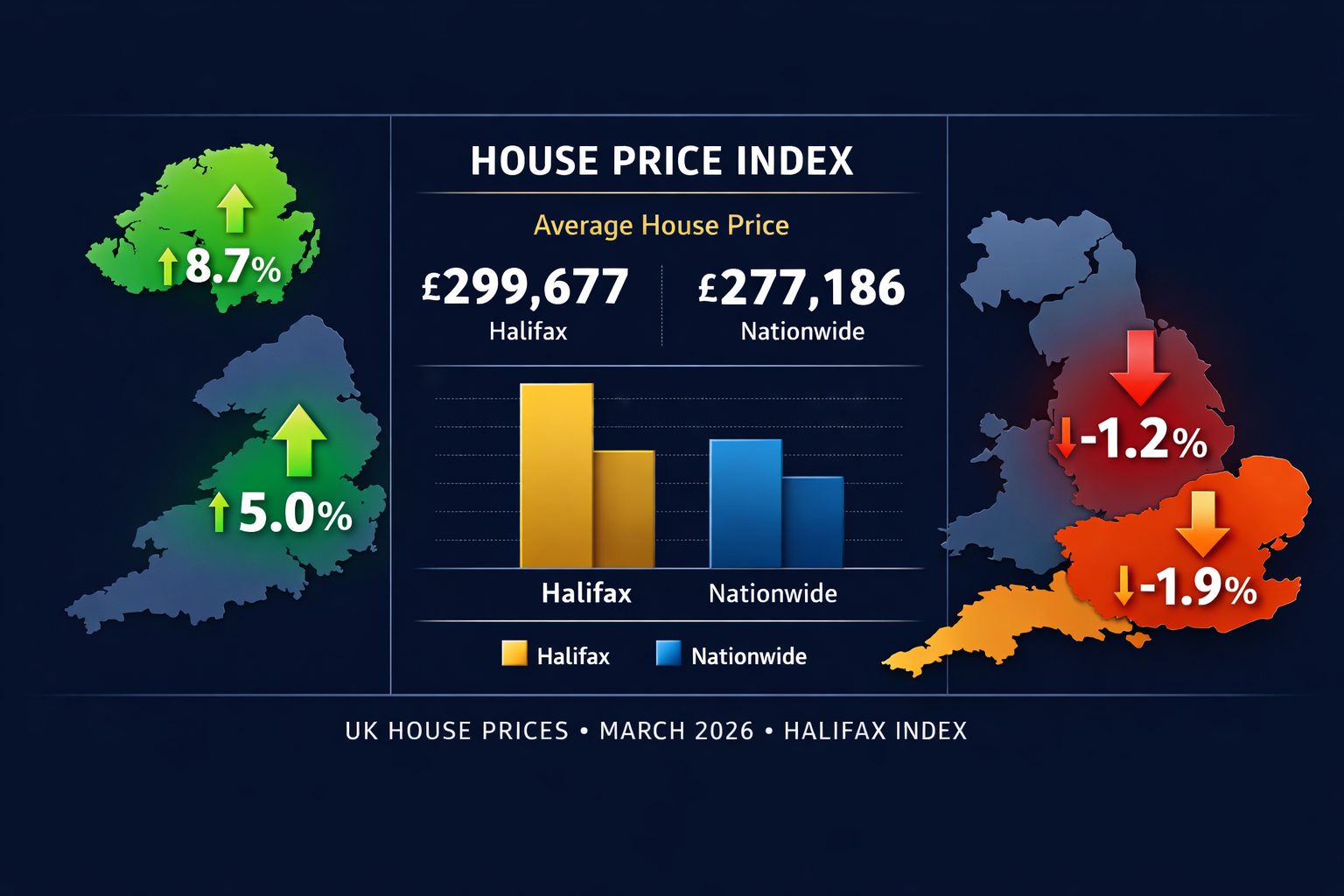

- Halifax HPI March 2026: Average UK house price £299,677; monthly fall of 0.5%; annual growth slowed to 0.8%

- Nationwide's March 2026 figure puts the average at £277,186 — a notable £22,491 gap reflecting different methodologies

- London fell 1.2% annually to £536,751; the South East dropped 1.9% — southern markets are underperforming northern regions significantly

- Mortgage volatility, linked partly to Middle East conflict and oil price pressures, is dampening buyer confidence

- A professional RICS survey is more valuable than ever in a softening market — both for buyers negotiating price and sellers protecting their asking price

What the UK House Prices March 2026 Halifax Index Actually Shows

The Halifax House Price Index is one of the UK's most closely watched property barometers, drawing on mortgage approval data from one of Britain's largest lenders. The March 2026 reading delivered a clear message: the market is losing steam.

| Metric | March 2026 |

|---|---|

| Monthly change | -0.5% |

| Annual change | +0.8% |

| Average UK price (Halifax) | £299,677 |

| Average UK price (Nationwide) | £277,186 |

| London average | £536,751 |

| South East average | £383,573 |

Annual growth decelerated sharply from 1.2% in February to 0.8% in March — a two-month slide that signals more than a seasonal blip. Completed transactions did rise 5% in the period, reaching their highest level since early 2025, but analysts caution that this activity largely reflects deals agreed before economic uncertainty intensified.

The North–South Divide Widens

The regional picture is stark. Northern Ireland led all UK regions with 8.7% annual growth, with average prices at £224,809. The North East followed at 5.0% growth (£184,119), Scotland at 4.4% (£222,716), and the North West at 3.1% (£247,442).

Southern England tells the opposite story. London prices fell 1.2% annually to £536,751, while the South East dropped 1.9% to £383,573 — the sharpest regional decline in the index. Wales recorded modest 1.6% growth at £230,909.

For Wimbledon and South West London homeowners, this regional context matters enormously. Your property sits in one of the most resilient micro-markets in the capital, but the broader London softening is a headwind you cannot ignore.

Halifax vs Nationwide: Why the £22,491 Gap Matters

The Nationwide Building Society's equivalent March 2026 figure puts the average UK house price at £277,186 — some £22,491 below Halifax's £299,677. This isn't an error; it reflects fundamental differences in methodology.

💬 "Neither index is wrong — they measure different things. Halifax captures a broader range of mortgage products; Nationwide focuses on its own lending book. Both are directionally useful, but neither should be treated as a precise valuation of your specific property."

For practical purposes, what matters to Wimbledon homeowners is local comparable evidence — recent sales in your street, your property's condition, and a professional valuation. National averages are context, not conclusions.

The Macro Backdrop: Why Is the Market Softening?

Three forces are converging to suppress buyer confidence in early 2026:

1. Mortgage rate volatility 🏦

Ongoing instability in global financial markets — partly driven by the Iran conflict and its effect on oil prices — has fed through to swap rates and, in turn, mortgage pricing. Lenders have repriced products multiple times in recent weeks, making it harder for buyers to plan with certainty.

2. Geopolitical uncertainty 🌍

The Middle East conflict has introduced a risk premium into financial markets. Energy costs remain elevated, squeezing household budgets and reducing the disposable income that fuels housing demand.

3. Affordability pressure in the South

Even after modest price falls, London and South East properties remain deeply unaffordable relative to incomes. The South East's 1.9% annual price decline reflects this structural constraint — prices had simply outrun earnings.

What This Means for Wimbledon Homeowners Considering a Sale

If you own property in Wimbledon or the surrounding South West London area, the March 2026 data raises several practical questions.

Should You Sell Now or Wait?

A 0.5% monthly fall is not a crash. In absolute terms, the national average has moved by roughly £1,500 in a single month. But the direction of travel matters — and sellers who act without preparation risk leaving money on the table.

Here's what the data suggests for your strategy:

- Price realistically from day one. Overpriced properties are sitting longer as buyer caution grows

- Presentation and condition are now more important than at any point in the past two years

- Buyers are conducting more due diligence — expect survey-led renegotiations to increase

Understanding how an RICS survey can help you negotiate the price of your property is essential reading whether you're on the buying or selling side of a transaction right now.

The Survey Factor in a Softening Market

When prices are rising, buyers sometimes skip or downgrade surveys to move quickly. In a softer market, that calculation reverses. Buyers are more cautious, more likely to commission a thorough inspection, and more willing to use survey findings to renegotiate. Research consistently shows that the average price reduction after a building survey can be significant — particularly on older South West London stock.

Wimbledon's housing stock is predominantly Victorian and Edwardian. These properties carry inherent risks: damp, roof deterioration, subsidence, and timber decay are all common findings. If you're buying, a thorough survey is not optional — it's financial protection.

RICS Level 2 vs Level 3: Choosing the Right Survey for Your Wimbledon Property

Not all surveys are equal, and choosing the wrong level can be a costly mistake. Our guide to home survey levels 2 vs level 3 walks through the differences in detail, but here's a quick summary:

| Survey Type | Best For | What It Covers |

|---|---|---|

| RICS Level 2 (HomeBuyer Report) | Modern or well-maintained properties | Condition ratings, visible defects, mortgage valuation |

| RICS Level 3 (Building Survey) | Older, larger, or altered properties | Full structural inspection, detailed defect analysis, repair cost guidance |

For most Wimbledon properties — particularly anything pre-1960 — a Level 3 Building Survey is the appropriate choice. The additional cost is invariably recovered through informed negotiation or avoided remedial bills.

You can download an example HomeBuyer Report to understand exactly what to expect before commissioning your survey.

Specific Issues to Watch in South West London Properties

Beyond the headline survey choice, certain defects are particularly prevalent in Wimbledon and surrounding areas:

- 🏠 Roof condition — clay tile roofs on Victorian terraces are a frequent source of problems; our guide to checking the roof when buying in Wimbledon explains what to look for

- 💧 Damp — rising and penetrating damp affect a high proportion of older London properties; understanding damp survey costs and what a report contains helps you budget appropriately

- 🌳 Subsidence — London clay is notorious for movement, especially near mature trees; our guide to subsidence covers the risks in detail

Conclusion: Act on Evidence, Not Anxiety

The UK house prices March 2026 Halifax index paints a picture of a market catching its breath — not collapsing, but clearly recalibrating. A 0.5% monthly fall and 0.8% annual growth tell us that the frenzied conditions of recent years have passed. For Wimbledon and South West London, where London's 1.2% annual price decline applies broadly, the message is clear: informed decisions will outperform reactive ones.

Your actionable next steps:

- ✅ If you're buying — commission a RICS Level 2 or Level 3 survey before exchange; use the findings to negotiate confidently

- ✅ If you're selling — get a professional valuation and address any known defects before listing

- ✅ If you're undecided — speak to a local RICS-qualified surveyor who understands the South West London market

Our Wimbledon property surveyors team provides RICS Level 2 HomeBuyer Reports and Level 3 Building Surveys across Wimbledon and South West London. Get a quote today and make your next property decision with complete confidence.