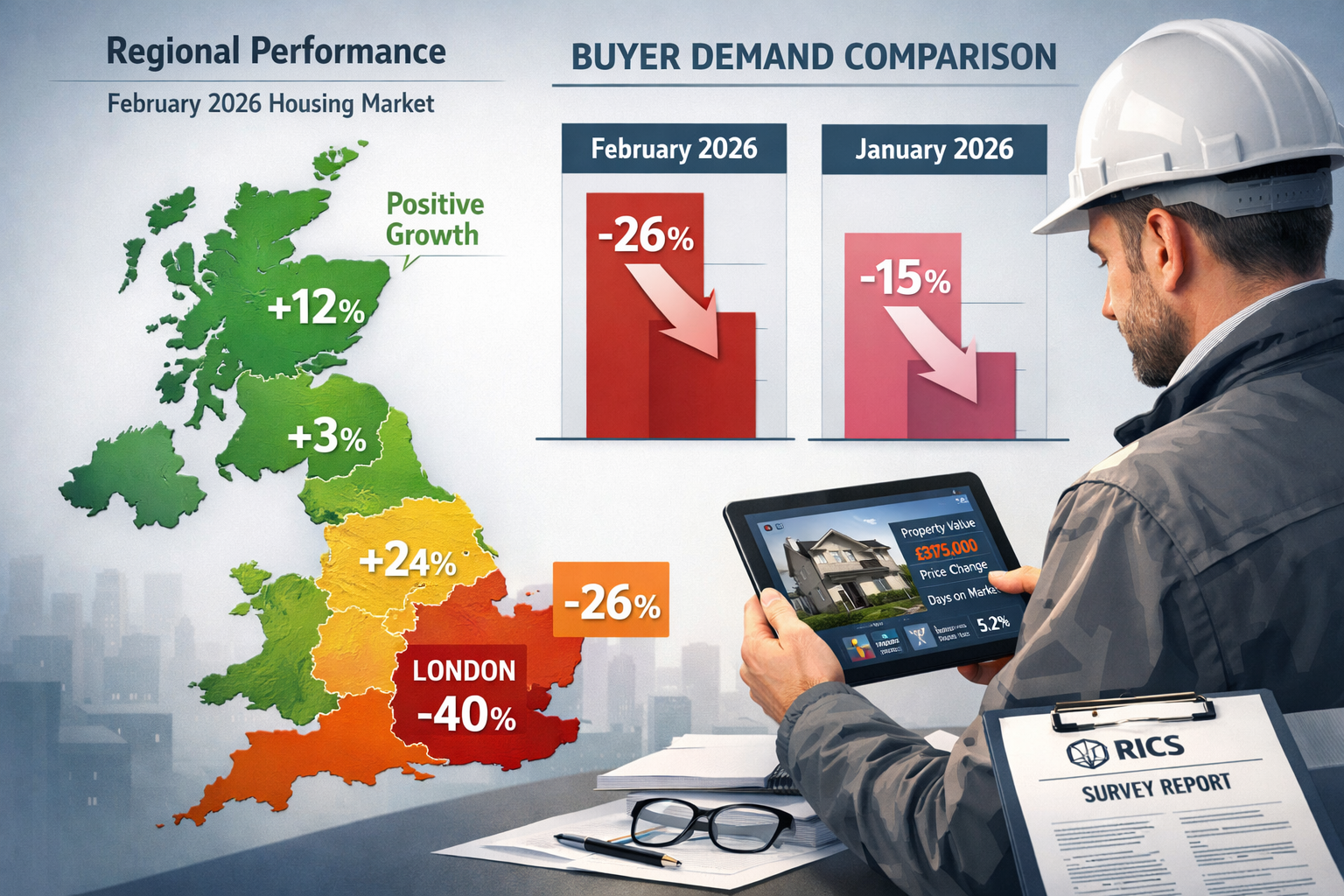

The RICS February 2026 residential market survey reveals a stark reality: buyer demand plummeted to a net balance of -26%, marking the sharpest decline since early 2024 and signaling a fundamental shift in market sentiment as Q2 approaches[1]. For valuation surveyors navigating these cautious markets, the data exposes a critical challenge—London's property confidence collapsed to -40% while northern regions maintain resilience, creating unprecedented regional divergence that demands sophisticated adjustment strategies[1]. Understanding the Valuation Adjustments in Q2 2026 Cautious Markets: RICS February Survey Insights for Regional Divergence becomes essential for professionals defending their reports amid geopolitical uncertainty and volatile buyer sentiment.

Key Takeaways

- 📉 Buyer demand dropped to -26% in February 2026, down from -15% in January, representing the most significant monthly decline in recent quarters

- 🏙️ London experienced a -40% net balance, the steepest regional correction, while northern regions showed relative stability and firmer price trends

- 📊 Near-term price expectations fell to -18%, yet 12-month outlook remains positive at +33%, creating valuation complexity for chartered surveyors

- 🏠 Rental supply crisis persists at -27% landlord instructions, with +20% expecting rent increases, impacting investment property valuations

- 🎯 Regional divergence requires tailored valuation approaches, with southern markets demanding conservative adjustments while northern areas justify more optimistic assessments

Understanding the February 2026 Market Shift and Its Valuation Implications

The February 2026 RICS survey data presents a sobering picture for property professionals. The -26% net balance in new buyer enquiries represents more than just a statistical decline—it signals a fundamental recalibration of market expectations as economic uncertainty and geopolitical tensions weigh on consumer confidence[1]. This sharp deterioration from January's -15% reading caught many market observers off guard, particularly given the early-year optimism that characterized January's modest improvement.

For chartered surveyors conducting valuations, this shift creates immediate practical challenges. When RICS surveyors prepare reports, they must balance current market sentiment against longer-term value trends. The February data suggests that agreed sales weakened to -12%, marginally worse than January's -9%, indicating that transactions are not just slowing in enquiry stages but failing to convert at higher rates[1].

National Price Trends Versus Regional Realities

The headline national house price net balance of -12% masks significant regional variation that demands careful analysis[1]. While this figure suggests broadly flat conditions at the national level—only slightly weaker than January's -10%—the regional breakdown reveals a market splitting into distinct performance zones.

Southern England's Correction:

- London: -40% net balance (most severe regional decline)

- South East: -24% net balance

- East Anglia: -26% net balance

These figures represent substantial downward pressure concentrated in traditionally high-value markets. For surveyors preparing condition survey reports in London, these metrics necessitate more conservative comparable selection and adjustment factors.

Northern Resilience:

- Northern Ireland: Firmer price trends

- Scotland: Positive momentum

- North West England: Outperforming national average

This regional divergence creates a complex landscape for valuation professionals. A surveyor in Kingston faces entirely different market dynamics than a colleague in Enfield, despite both operating within Greater London's broader market.

Valuation Adjustments in Q2 2026 Cautious Markets: Tactical Approaches for Surveyors

The Valuation Adjustments in Q2 2026 Cautious Markets: RICS February Survey Insights for Regional Divergence require surveyors to adopt more nuanced methodologies than in stable market conditions. Traditional comparable-based approaches must incorporate heightened uncertainty factors and regional performance differentials.

Defending Valuation Reports in Volatile Conditions

When market sentiment shifts as dramatically as the February 2026 data suggests, valuation reports face increased scrutiny from lenders, buyers, and legal representatives. Surveyors must strengthen their defensibility through:

Enhanced Comparable Analysis 🔍

- Prioritize transactions completed within the most recent 3-month window rather than standard 6-month periods

- Apply time adjustments more aggressively to account for rapid sentiment shifts

- Weight recent sales more heavily in reconciliation processes

- Document market conditions explicitly in valuation narratives

Regional Adjustment Factors

Given London's -40% sentiment versus northern stability, surveyors must quantify regional risk premiums. A property in Southwark requires different adjustment considerations than one in Barnet, even when comparable property characteristics align.

Incorporating Geopolitical Uncertainty Into Valuations

The RICS guidance on valuation issues associated with conflicts provides a framework for addressing external uncertainty factors[4]. In Q2 2026, surveyors must consider:

- Market liquidity constraints: The -26% buyer demand figure suggests reduced transaction velocity, impacting marketability assessments

- Financing availability: Lender caution in uncertain markets affects achievable prices

- Insurance and risk premiums: Geopolitical tensions may influence property insurance costs and buyer risk tolerance

Professional surveyors should explicitly reference market uncertainty in their reports while avoiding speculation. Statements like "current market conditions reflect heightened caution as evidenced by RICS February 2026 survey data showing -26% buyer demand" provide factual context without undermining valuation conclusions.

Adjusting for Short-Term Versus Long-Term Expectations

One of the most striking aspects of the February 2026 data is the divergence between near-term and 12-month price expectations. Near-term expectations fell to -18%, representing significant pessimism about immediate market prospects[1]. However, 12-month expectations remain positive at +33%, suggesting surveyors and market participants anticipate recovery beyond current volatility[1].

This creates a valuation paradox: Should reports reflect current pessimism or longer-term optimism? The answer depends on valuation purpose:

| Valuation Purpose | Recommended Approach | Timeframe Weight |

|---|---|---|

| Mortgage lending | Conservative, near-term focused | 70% current, 30% 12-month |

| Investment analysis | Balanced, cycle-aware | 40% current, 60% 12-month |

| Probate/taxation | Current market value | 90% current, 10% forward |

| Development appraisal | Forward-looking | 30% current, 70% 12-month |

For professionals conducting homebuyer reports, the emphasis should remain on current market value while noting potential recovery trajectories in market commentary sections.

Regional Divergence Strategies: London's Collapse Versus Northern Momentum

The most critical insight from the Valuation Adjustments in Q2 2026 Cautious Markets: RICS February Survey Insights for Regional Divergence is the unprecedented gap between London's performance and northern regions. London's 12-month price expectations collapsed to +7% from +56% in the previous month—a staggering 49-percentage-point decline that signals fundamentally altered confidence among market participants[1].

London and Southeast Valuation Considerations

For surveyors operating in Fulham, Richmond, or Battersea, the February data demands heightened conservatism:

Price Adjustment Tactics:

- Apply 5-10% downward adjustments to comparable sales completed before December 2025

- Increase scrutiny of asking prices versus achieved prices

- Weight withdrawn listings and price reductions more heavily in market analysis

- Consider "days on market" trends as liquidity indicators

Market Commentary Requirements:

Professional reports should explicitly reference the -40% sentiment reading and explain its implications for value conclusions. When preparing reports that may be used to negotiate property prices, this data provides powerful leverage for buyers while requiring sellers' surveyors to justify valuations more rigorously.

Northern England and Scotland: Capitalizing on Resilience

Surveyors operating in northern regions face the opposite challenge—justifying stronger valuations in a national climate of pessimism. The RICS data shows these areas maintaining firmer price trends despite national weakness[1], creating opportunities for evidence-based optimism.

Supporting Stronger Valuations:

- Emphasize local employment trends and economic fundamentals

- Reference regional RICS data explicitly to counter national negative sentiment

- Highlight supply constraints in specific submarkets

- Document buyer competition levels in comparable transactions

The key is avoiding overconfidence. While northern regions outperform London, they operate within a national context of -26% buyer demand and -18% near-term price expectations. Valuations should reflect relative strength without ignoring broader market caution.

Micro-Market Analysis Within Regions

Even within struggling regions like London, micro-market performance varies significantly. A surveyor valuing property in Knightsbridge faces different dynamics than one in Woolwich. Prime central London often exhibits different cycle timing than outer boroughs.

Micro-Market Factors to Analyze:

- Local employment centers and commuting patterns

- School catchment areas and family buyer demand

- Transport infrastructure developments

- Neighborhood regeneration initiatives

- Local supply levels relative to historic norms

Surveyors should resist applying regional averages uniformly. Detailed local market knowledge separates competent valuations from exceptional ones, particularly in divergent market conditions.

Rental Market Dynamics and Investment Property Valuations

The February 2026 RICS survey reveals that while sales markets struggle, rental markets face acute supply constraints. Landlord instructions remained at -27% net balance, indicating persistent shortages of rental stock[1]. Simultaneously, +20% of survey participants expect rents to rise over the coming three months[1], creating a unique valuation environment for investment properties.

Adjusting Investment Valuations for Rental Growth

For surveyors valuing buy-to-let properties or multi-unit residential investments, the rental market data provides critical inputs for income capitalization approaches. The combination of supply constraints and expected rent growth suggests:

Yield Compression Potential 📈

- Rental growth expectations may support lower capitalization rates

- However, broader market caution (-26% buyer demand) suggests maintaining conservative yields

- Balance rental strength against sales market weakness in final yield selection

Cash Flow Projections

When preparing valuations for investment purposes, incorporate the +20% rent growth expectation cautiously:

- Apply growth rates of 2-4% annually rather than aggressive projections

- Consider regional variations (London rental growth may differ from northern markets)

- Account for potential regulatory changes affecting landlord returns

- Factor in void periods and management costs conservatively

First-Time Buyer Implications

The rental supply crisis has significant implications for first-time buyer activity. As rents rise due to supply constraints, more potential buyers may be motivated to purchase despite challenging market conditions. Recent analysis of spring 2026 market recovery and building survey demand suggests that improved lender volumes could support first-time buyer activity even as overall demand remains subdued[5].

Surveyors conducting valuations for first-time buyer purchases should:

- Consider rent-versus-buy calculations in market commentary

- Acknowledge that rising rents may support price floors

- Recognize that first-time buyer segments may show different demand patterns than overall market

Supply Dynamics: New Instructions and Market Inventory

The February 2026 survey shows new instructions at +2% net balance—essentially neutral[1]. This stability in new listings contrasts with the sharp decline in buyer demand, creating a supply-demand imbalance that influences valuation approaches.

Inventory Levels and Time on Market

When supply remains stable while demand falls by 11 percentage points (from -15% to -26%), properties inevitably remain on the market longer. For valuation purposes, this suggests:

Increased Marketing Periods

- Adjust marketability assessments upward (properties will take longer to sell)

- Consider seasonal factors more carefully (spring market may not provide usual boost)

- Weight recent sales more heavily than older comparables that sold in stronger demand conditions

Negotiation Leverage Shifts

The supply-demand imbalance favors buyers, affecting achievable prices. Surveyors must consider:

- Are comparable sales prices reflecting full asking prices or negotiated discounts?

- How have "subject to survey" renegotiations trended in recent months?

- What proportion of agreed sales are falling through?

Strategic Listing Timing Advice

While valuations must reflect current market conditions, surveyors often provide informal guidance to clients about market timing. The February 2026 data suggests:

For Sellers:

- Consider delaying non-urgent sales until market sentiment improves

- Price realistically given -26% buyer demand and -18% near-term expectations

- Prepare for longer marketing periods and potential renegotiation

For Buyers:

- Current conditions favor negotiation leverage

- Consider that 12-month expectations remain positive (+33%), suggesting limited downside risk

- Focus on properties with motivated sellers or extended marketing periods

Practical Valuation Report Adjustments for Q2 2026

Translating the Valuation Adjustments in Q2 2026 Cautious Markets: RICS February Survey Insights for Regional Divergence into practical report modifications requires specific tactical changes:

Market Conditions Section Enhancements

Every valuation report should include a robust market conditions section. For Q2 2026, this should explicitly reference:

"The RICS February 2026 Residential Market Survey indicates buyer demand at a net balance of -26%, representing a significant decline from -15% in January. Near-term price expectations have softened to -18%, though 12-month expectations remain positive at +33%. [Regional specific data: London -40%, Southeast -24%, etc.] These conditions suggest [increased/decreased] market caution and [shorter/longer] anticipated marketing periods."

Comparable Selection Criteria

Tighten comparable selection standards:

- Recency: Prioritize sales completed within 90 days over older transactions

- Verification: Confirm achieved prices rather than relying on asking prices

- Adjustment transparency: Document all adjustments with clear rationale

- Regional relevance: Ensure comparables reflect micro-market conditions

Uncertainty and Assumptions Statements

Given heightened market volatility, strengthen uncertainty disclosures:

- Explicitly state that valuations reflect conditions as of the valuation date

- Note that market conditions are changing rapidly

- Reference specific RICS survey data as evidence of market state

- Consider including sensitivity analysis showing value ranges under different scenarios

Professional Indemnity Considerations

In uncertain markets, valuation challenges and disputes increase. Protect professional standing through:

- Comprehensive documentation: Maintain detailed work files showing analysis depth

- Conservative assumptions: When uncertain, err toward conservatism

- Clear limitations: State explicitly what the valuation does and doesn't cover

- Regular CPD: Stay current with market developments and valuation standards

Conclusion: Navigating Q2 2026's Divergent Markets with Confidence

The Valuation Adjustments in Q2 2026 Cautious Markets: RICS February Survey Insights for Regional Divergence present both challenges and opportunities for property professionals. The February 2026 data—showing -26% buyer demand, London's -40% sentiment collapse, and persistent northern resilience—demands sophisticated, regionally-aware valuation approaches that balance current caution against longer-term recovery expectations.

Successful surveyors will distinguish themselves through rigorous analysis that acknowledges market complexity rather than applying simplistic national averages. The 49-percentage-point collapse in London's 12-month expectations from +56% to +7% represents one of the most dramatic sentiment shifts in recent market history, requiring London-based professionals to fundamentally recalibrate their approaches[1].

Actionable Next Steps for Valuation Professionals

Immediate Actions (This Week):

- ✅ Review all pending valuation reports to incorporate February 2026 RICS data

- ✅ Update comparable databases with most recent transaction evidence

- ✅ Revise standard market commentary templates to reflect current conditions

- ✅ Schedule client communications explaining market shifts and valuation implications

Short-Term Strategies (Next Month):

- 📊 Develop regional adjustment matrices based on RICS regional performance data

- 📊 Enhance comparable analysis procedures to weight recent transactions more heavily

- 📊 Create sensitivity analysis templates showing value ranges under different market scenarios

- 📊 Strengthen documentation practices to support valuations in potential disputes

Long-Term Positioning (Q2-Q3 2026):

- 🎯 Monitor monthly RICS survey releases for early signs of sentiment recovery

- 🎯 Build expertise in specific regional markets to capitalize on divergence opportunities

- 🎯 Develop rental market valuation capabilities as investment focus potentially shifts

- 🎯 Maintain conservative professional standards that protect reputation through market cycles

The rental market's -27% landlord instruction shortage combined with +20% rent growth expectations suggests that investment property valuations may offer more stability than owner-occupied residential work in coming months[1]. Diversifying service offerings to include comprehensive property evaluation approaches positions practices for success regardless of sales market trajectory.

Ultimately, the February 2026 RICS survey data confirms what experienced professionals understand: property markets move in cycles, regional performance diverges, and valuation excellence requires adapting methodologies to current conditions while maintaining professional standards. Surveyors who embrace the complexity revealed in the Valuation Adjustments in Q2 2026 Cautious Markets: RICS February Survey Insights for Regional Divergence will emerge as trusted advisors capable of guiding clients through uncertain times with evidence-based confidence.

References

[1] Uk Residential Survey February 2026 – https://www.rics.org/news-insights/uk-residential-survey-february-2026

[2] Surveyor Strategies For Landlord Instructions Shortage Valuations In Tight Lettings Markets Per Rics February 2026 – https://nottinghillsurveyors.com/blog/surveyor-strategies-for-landlord-instructions-shortage-valuations-in-tight-lettings-markets-per-rics-february-2026

[3] Uk Residential Market Survey February 2026 – https://www.rics.org/content/dam/ricsglobal/documents/market-surveys/uk-residential-market-survey/UK-Residential-Market-Survey_February-2026.pdf

[4] Valuation Issues Associated With The Conflict In The Middle East – https://www.rics.org/news-insights/valuation-issues-associated-with-the-conflict-in-the-middle-east

[5] Spring 2026 Market Recovery Building Survey Demand Surge And First Time Buyer Assessments Amid Improved Lender Volumes – https://nottinghillsurveyors.com/blog/spring-2026-market-recovery-building-survey-demand-surge-and-first-time-buyer-assessments-amid-improved-lender-volumes