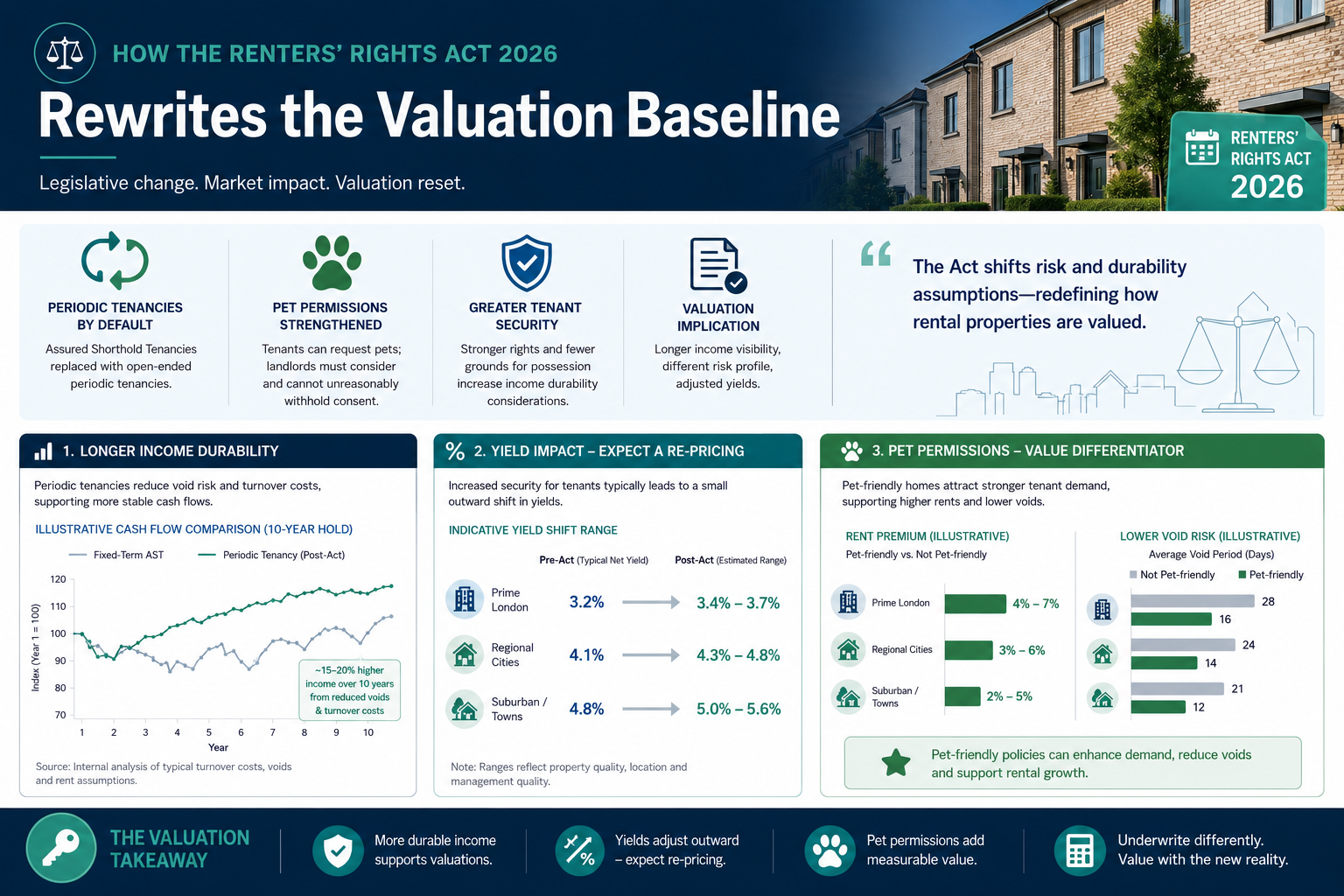

The UK private rented sector underwent its most significant structural overhaul in a generation on 1 May 2026, when the Renters' Rights Act 2025 came into full force. Within weeks, surveyors and investors were grappling with a fundamental question: how do you price a buy-to-let asset when the legal ground beneath it has shifted so dramatically? Valuing rental properties post-Renters' Rights Act 2026, with its impact of periodic tenancies and pet permissions, is no longer a matter of applying a standard yield and moving on. It demands a rebuilt framework that accounts for legislative risk, compressed income flexibility, and new categories of physical wear.

Key Takeaways

- All assured shorthold tenancies converted to assured periodic tenancies on 1 May 2026, removing fixed end dates and increasing landlord uncertainty over property turnover.

- The abolition of Section 21 "no-fault" evictions lengthens and complicates possession proceedings, introducing a new risk premium into investment valuations.

- Properties with sitting tenants are now attracting valuation discounts of 10-20% below vacant possession value in cautious markets.

- Surveyors are advised to raise capitalisation rates from around 5% to 5.5-6% to reflect the additional legislative and income risks introduced by the Act.

- Pet permissions, now a near-statutory right for tenants, create measurable physical risk to properties that must be factored into condition assessments and yield calculations.

How the Renters' Rights Act 2026 Rewrites the Valuation Baseline

Before 1 May 2026, a standard buy-to-let valuation rested on relatively predictable inputs: a fixed-term tenancy with a defined end date, a clear pathway to vacant possession via Section 21, and a landlord's ability to plan refurbishment or sale cycles. All three of those inputs have now changed.

The End of Fixed-Term Tenancies

Every assured shorthold tenancy (AST) in England automatically converted to an assured periodic tenancy (APT) on 1 May 2026 [1]. New tenancies created after that date also begin as APTs from day one. There are no fixed end dates. A tenancy rolls forward indefinitely on a monthly or weekly basis until either the landlord establishes a statutory ground for possession or the tenant gives two months' notice to leave [1].

For investors, this removes the ability to plan for vacant possession at a known point in time. Refurbishment windows, sale timing, and portfolio restructuring all become harder to schedule. Lenders, too, are reassessing how they treat rental income projections on properties encumbered by APTs, since the income stream is theoretically permanent but the landlord's control over it is reduced.

Section 21 Abolished: The Possession Risk Premium

The abolition of Section 21 "no-fault" evictions is the single change with the greatest direct impact on valuation [2]. Landlords must now rely entirely on the statutory grounds set out in Schedule 2 of the Housing Act 1988, as amended. Establishing those grounds takes longer, costs more in legal fees, and carries greater uncertainty of outcome than a Section 21 notice ever did.

This shift introduces what valuers are beginning to call a possession risk premium: an additional discount applied to reflect the time and cost a landlord might face if they need to recover a property. In practical terms, this feeds directly into the yield adjustment discussed below.

Rent Increase Restrictions and Income Capping

Rent increases under APTs are limited to once per year and cannot occur within the first 12 months of any tenancy [1]. Landlords who previously relied on annual rent reviews timed to market conditions now face a more constrained income trajectory. In high-demand London markets, where rents have historically risen sharply, this cap compresses the upside that investors factor into discounted cash flow models.

For RICS property valuations, the practical effect is that projected rental income growth must be modelled more conservatively. A property that might previously have been valued on an assumption of 4-5% annual rent growth may now be modelled at 2-3%, directly reducing the present value of future income streams.

Yield Adjustments and Sitting Tenant Discounts: The Surveyor's New Toolkit

The core mechanics of valuing rental properties post-Renters' Rights Act 2026, with its impact of periodic tenancies and pet permissions, require surveyors to revisit three interconnected tools: capitalisation rates, sitting tenant discounts, and liquidity risk premiums.

Raising Capitalisation Rates

RICS-aligned guidance now recommends that surveyors apply higher capitalisation rates to private rented sector (PRS) properties to reflect the additional risks introduced by the Act [4]. Where a standard buy-to-let property might previously have been valued on a 5% yield, the adjusted range is now 5.5-6%, depending on property type, location, and tenant profile [4].

The table below illustrates how this shift affects a hypothetical property generating £18,000 per year in rental income:

| Capitalisation Rate | Implied Capital Value |

|---|---|

| 5.0% (pre-Act) | £360,000 |

| 5.5% (post-Act, moderate risk) | £327,273 |

| 6.0% (post-Act, higher risk) | £300,000 |

A move from 5% to 6% represents a capital value reduction of £60,000 on a single property. Across a portfolio, the aggregate effect is substantial. Surveyors must document the reasoning behind any rate adjustment clearly, particularly where valuations are being used for mortgage security or dispute resolution purposes.

Sitting Tenant Discounts

Properties sold with sitting tenants have always attracted a discount relative to vacant possession value. Under the new regime, that discount has widened. Current market evidence suggests discounts of 10-20% below vacant possession value are now being applied, reflecting the reduced flexibility and increased risks for landlords who acquire a tenanted property [4].

The precise discount depends on several factors:

- Tenancy duration: A long-standing tenant is harder to move on than a recent one.

- Rent level relative to market: A significantly below-market rent creates a larger income gap.

- Property condition: Poor condition increases the urgency of regaining possession for refurbishment.

- Tenant conduct history: Any history of arrears or disputes increases possession risk.

For buyers considering a tenanted investment purchase, commissioning a RICS HomeBuyer Survey before exchange is essential. Understanding the physical condition of the property is as important as understanding the legal position of the tenancy.

Liquidity Risk Premiums

The buyer pool for tenanted investment properties has narrowed since 1 May 2026. Owner-occupiers cannot easily purchase a property with a sitting APT tenant, and even professional investors are pricing in the additional complexity. A narrower buyer pool means reduced liquidity, and reduced liquidity justifies an additional premium in the valuation [4].

Surveyors are increasingly applying a liquidity risk premium of 1-3% on top of the standard yield adjustment for properties where the tenancy structure significantly restricts the realistic buyer pool. This is particularly relevant in secondary markets outside major cities, where the pool of specialist investors is smaller.

"The removal of Section 21 has not just changed the law. It has changed the risk profile of every tenanted property in England, and valuers who fail to reflect that in their numbers are producing figures that do not represent market reality."

Pet Permissions, Property Condition, and the Valuation Consequences

The pet provisions of the Renters' Rights Act 2026 have attracted less attention than the tenancy reforms, but their impact on property valuation is real and growing. Valuing rental properties post-Renters' Rights Act 2026, with its impact of periodic tenancies and pet permissions, requires surveyors to treat the pet question as a material valuation factor rather than a minor administrative detail.

What the Law Now Requires

Tenants now have a statutory right to request consent to keep a pet. Landlords cannot unreasonably refuse, and crucially, they cannot charge additional fees or deposits specifically for pets beyond the standard deposit cap [3]. The only financial protection available to landlords is the right to require pet insurance, where the tenant agrees to it.

This creates an asymmetry: the physical risk of pet occupation falls on the landlord, but the financial tools to offset that risk have been constrained by law.

Physical Damage and Condition Survey Evidence

The categories of damage associated with pet occupation are well-documented in the surveying profession:

- Scratched and stained flooring, particularly hardwood and laminate

- Urine contamination of subfloors, carpets, and skirting boards

- Damaged door frames, skirting boards, and internal joinery

- Garden deterioration from digging and fouling

- Odour penetration into plasterwork and soft furnishings

For landlords and buyers, a thorough condition survey before and after any tenancy involving pets is now essential evidence in any dilapidations claim. The dilapidations survey process has become a critical tool for landlords seeking to recover legitimate costs at the end of a pet tenancy.

Where a property is being valued with a sitting tenant who has an approved pet, surveyors must assess the current condition of the property and apply a maintenance cost adjustment to the income-based valuation. This is not speculative: it reflects the higher probability of end-of-tenancy remediation costs.

Valuation Adjustments for Pet-Permitted Properties

The valuation adjustment for pet permissions is not a fixed number. It depends on the type of pet, the property specification, and the duration of the tenancy. However, surveyors are now building the following into their models:

- Increased maintenance reserves: An additional 0.5-1% of property value per year added to the operational cost assumption.

- Reduced residual value at tenancy end: Particularly for high-specification properties where the cost of restoring finishes is disproportionately high.

- Shorter effective depreciation cycle for floor coverings: Carpets and soft flooring are now modelled with a shorter replacement cycle in properties where pets are present.

For landlords considering whether to accept a pet, the financial calculus has changed. The inability to charge a pet premium or a larger deposit means that the decision must be weighed against the baseline rental income and the property's resilience to wear.

Compliance Costs and the Decent Homes Standard

Beyond pets, the Act introduces broader compliance obligations. The extension of the Decent Homes Standard to the private rented sector means that properties must meet a defined minimum condition threshold [6]. Landlords who fail to meet this standard face enforcement action, and the cost of bringing properties up to standard must be factored into any investment valuation.

For properties that are currently borderline compliant, surveyors should recommend a building condition assessment to establish the remediation cost before any valuation is finalised. Ignoring this step risks producing a valuation that overstates the net income position of the property.

Sector-Specific Impacts: Student Accommodation and Expert Witness Valuations

Student Accommodation: A Structural Mismatch

Purpose-built student accommodation (PBSA) operators face a particular challenge under the APT regime [5]. The academic calendar runs on fixed cycles: students need rooms from September and vacate in June or July. Under fixed-term ASTs, operators could align tenancy end dates with the academic year. Under APTs, a student tenant could theoretically remain in occupation indefinitely, or give only two months' notice at any point, disrupting room availability planning.

This structural mismatch is already affecting the valuation of PBSA assets. Investors are applying additional operational risk discounts, and lenders are scrutinising income projections more carefully. The sector is lobbying for a specific exemption or modification to the APT rules, but as of mid-2026, no such carve-out has been confirmed.

Expert Witness Valuations in Disputes

The new legislative framework has created a growing category of valuation dispute in which the periodic tenancy structure and rent controls are themselves the source of conflict [7]. In tribunal proceedings and county court litigation, expert witnesses are being asked to value properties where the tenancy terms are disputed, the rent level is challenged, or the grounds for possession are contested.

In these cases, the expert must rebuild the evidentiary framework from the ground up, accounting for the statutory rent controls, the APT structure, and the possession risk premium [7]. Standard comparable evidence drawn from pre-Act transactions is of limited value, because the legal environment that produced those comparables no longer exists.

Surveyors acting as expert witnesses must be explicit about the legislative adjustments they are making and must be able to defend those adjustments under cross-examination. This is a higher bar than was previously required, and it reflects the genuine complexity that the Act has introduced into the valuation process.

For landlords involved in possession disputes or rent challenges, commissioning a specialist RICS property valuation that explicitly addresses the post-Act framework is now a practical necessity, not an optional extra.

Practical Steps for Landlords and Investors in 2026

Given the scale of the changes, landlords and investors need a clear action plan. The following steps reflect the current state of the market and the evolving RICS guidance:

-

Commission updated valuations: Any valuation conducted before 1 May 2026 should be treated as outdated. The Act has materially changed the risk profile of tenanted properties.

-

Conduct condition surveys at tenancy start and end: This is now essential evidence for dilapidations claims, particularly where pets are involved. Consider a Level 2 or Level 3 survey depending on the property's age and complexity.

-

Review income projections: Rental income growth assumptions must be revised downward to reflect the annual increase cap and the 12-month restriction on new tenancy increases.

-

Apply appropriate yield adjustments: Work with a RICS-qualified surveyor to determine the correct capitalisation rate for each property, taking into account location, tenant profile, and possession risk.

-

Document pet consent decisions carefully: Any agreement to allow a pet should be recorded in writing, with a clear description of the animal, the condition of the property at the time of consent, and any agreed maintenance obligations.

-

Assess compliance with the Decent Homes Standard: Properties that fall short of the standard face enforcement risk, which must be reflected in the valuation as a contingent liability.

-

Seek specialist advice for student accommodation: PBSA operators should obtain legal and valuation advice specific to their portfolio structure, as the standard APT framework creates particular challenges for this asset class.

For landlords and investors across London and the South East, local surveying expertise is invaluable. Whether the property is in Battersea, Richmond, Islington, or Bromley, a surveyor with knowledge of the local PRS market will be better placed to apply the correct risk adjustments and produce a defensible valuation.

Conclusion

Valuing rental properties post-Renters' Rights Act 2026, with its impact of periodic tenancies and pet permissions, is a discipline that has been fundamentally reset. The abolition of fixed-term tenancies and Section 21 evictions, combined with statutory pet permissions and rent increase restrictions, has introduced a new layer of legislative risk that must be priced into every investment decision.

The key actionable steps are clear. Landlords should commission fresh RICS valuations that explicitly apply post-Act yield adjustments. Investors acquiring tenanted properties should budget for sitting tenant discounts of 10-20% and factor in higher capitalisation rates of 5.5-6%. Condition surveys must be treated as essential evidence, not administrative formality, particularly where pets are involved. And anyone operating in the student accommodation sector should seek specialist advice without delay.

The market will adapt, as it always does. But the adaptation requires accurate information, rigorous methodology, and professional guidance from surveyors who understand both the legal changes and their financial consequences. Acting on outdated assumptions in 2026 is not just a valuation error. It is a financial risk that could take years to unwind.

References

[1] Renters Rights Act 2025 Prs Tenancy Reform Round Up – https://www.dentons.com/en/insights/articles/2026/april/24/renters-rights-act-2025-prs-tenancy-reform-round-up

[2] United Kingdom Renters Rights Act 2025 – https://www.bakermckenzie.com/en/insight/publications/2026/01/united-kingdom-renters-rights-act-2025

[3] Valuation Impacts Of Renters Rights Act 2026 Pet Rules And Ombudsman On Prs Properties Rics Adjustment Frameworks – https://wimbledonsurveyors.com/valuation-impacts-of-renters-rights-act-2026-pet-rules-and-ombudsman-on-prs-properties-rics-adjustment-frameworks/

[4] Valuing Rental Properties Under The Renters Rights Act 2026 Surveyor Adjustments For Section 21 Abolition – https://www.canterburysurveyors.com/blog/valuing-rental-properties-under-the-renters-rights-act-2026-surveyor-adjustments-for-section-21-abolition/

[5] Alerts Realestate Impacts Of The Renters Rights Act – https://www.goodwinlaw.com/en/insights/publications/2026/01/alerts-realestate-impacts-of-the-renters-rights-act

[6] Renters Rights Act 2026 Implications For Condition Surveys Landlord Valuations And Dispute Evidence – https://www.canterburysurveyors.com/blog/renters-rights-act-2026-implications-for-condition-surveys-landlord-valuations-and-dispute-evidence/

[7] Expert Witness Valuations In Renters Rights Act Disputes Building Cases When Periodic Tenancies And Rent Controls Create Valuation Conflicts – https://www.canterburysurveyors.com/blog/expert-witness-valuations-in-renters-rights-act-disputes-building-cases-when-periodic-tenancies-and-rent-controls-create-valuation-conflicts/