The Private Rented Sector now accounts for 19% of all UK households — 4.6 million properties — and every single one of them is subject to the most sweeping tenancy reform in a generation [5]. From May 1, 2026, the Renters' Rights Act fundamentally reshapes how landlords manage tenants, pets, and disputes. For chartered surveyors and property investors, the Valuation Impacts of Renters' Rights Act 2026 Pet Rules and Ombudsman on PRS Properties: RICS Adjustment Frameworks are no longer a theoretical concern — they are an active, data-driven challenge requiring immediate professional recalibration.

This article examines how the Act's pet consent rules, fee restrictions, possession changes, and the incoming PRS Ombudsman combine to alter risk profiles, yield assumptions, and market value assessments for buy-to-let and PRS assets across England.

Key Takeaways 📋

- From May 1, 2026, tenants have a statutory right to request pet consent, and landlords cannot unreasonably refuse or charge pet-specific fees — reshaping landlord risk exposure.

- Section 21 abolition removes the fastest eviction route, extending possession timelines to 2–4 months and directly affecting valuation yield assumptions.

- The PRS Ombudsman won't launch until late 2026, creating a compliance gap where pet disputes lack formal resolution channels.

- RICS guidance requires valuers to reassess the vacant possession assumption and reflect market impact in all PRS valuations from May 2026 onward.

- Rent increase restrictions — no increases in the first 12 months, one annual increase thereafter — compress projected income growth and affect investment-grade valuations.

The Renters' Rights Act 2026: What Changed and When

The Renters' Rights Act received Royal Assent on October 27, 2025, with implementation structured across three phases [3]:

| Phase | Date | Key Changes |

|---|---|---|

| Phase 1 | May 1, 2026 | Section 21 abolished, ASTs replaced, pet rights active, rent advance capped |

| Phase 2 | Late 2026 | PRS Ombudsman launches, mandatory dispute resolution begins |

| Phase 3 | 2035–2037 | Decent Homes Standard for PRS, further enforcement upgrades |

Phase 1: The Valuation-Critical Reforms

Phase 1 is where the most immediate valuation pressure concentrates. From May 1, 2026 [3]:

- Fixed-term Assured Shorthold Tenancies (ASTs) are replaced by monthly periodic tenancies

- Section 21 "no-fault" evictions are abolished entirely

- Rent in advance is capped at one month

- Annual rent increases are restricted — no increase permitted in the first 12 months, then only one per year at market value

Each of these changes feeds directly into the income and risk components that underpin RICS-compliant valuations.

💬 "The limitation on possession speed through Section 21 abolition affects valuation methodology — RICS emphasises that valuers must exercise professional judgment regarding the appropriateness of the vacant possession assumption." — RICS Expert Working Group [1]

Pet Rules Under the Act: Landlord Risk and Valuation Exposure

Statutory Pet Consent: What It Means in Practice

Before May 1, 2026, landlords could blanket-refuse pets with no legal consequence. That era is over. Under the Act, tenants now hold a statutory right to request permission to keep a pet, and landlords are prohibited from unreasonably withholding consent [4].

The practical implications for property condition and valuation are significant:

- 🐾 Pet damage risk is now embedded in the tenancy lifecycle for all new agreements from May 2026

- Landlords cannot charge separate pet fees, pet deposits, or pet-related payments under the Tenant Fees Act 2019 [4]

- Landlords who raise rent specifically because a tenant has a pet face penalties of up to £7,000 for treating this as a banned fee or rental bidding offence [4]

- Existing tenancies entered before May 1, 2026 are exempt from the new pet consent rules — but all new tenancies fall within scope immediately [4]

What Landlords Can Still Do

Landlords retain some protections:

✅ Require tenants to obtain pet damage insurance as a condition of consent

✅ Refuse consent on reasonable grounds (e.g., lease restrictions in leasehold properties, property type unsuitable for the animal)

✅ Pursue Section 8 possession if a tenant keeps an unauthorised pet or causes damage

However, the removal of Section 21 means that landlords can no longer use a "no-fault" notice as a backstop enforcement mechanism. Any possession claim must now cite a specific statutory ground, with notice periods ranging from two weeks to four months depending on the ground invoked [3]. This is a material change from the previous two-month Section 21 notice period.

The Fee Restriction Paradox

Here lies a core valuation tension: landlords bear greater pet-related risk but cannot price that risk into the rent or deposit structure. The £7,000 penalty for rent-based pet surcharges effectively prohibits the most direct risk-mitigation tool [4].

This creates a negative externality that valuers must factor into income projections. Properties with higher pet exposure — ground-floor flats, houses with gardens, larger units — may carry a measurable risk premium that suppresses net yield without a corresponding rent uplift.

For a deeper understanding of how property condition assessments feed into valuation reports, see our guide to RICS HomeBuyer Survey methodology and what surveyors examine during inspections.

RICS Adjustment Frameworks: How Valuers Must Respond

Understanding the Valuation Impacts of Renters' Rights Act 2026 Pet Rules and Ombudsman on PRS Properties: RICS Adjustment Frameworks requires examining three core adjustment categories that RICS guidance now demands.

1. Vacant Possession Assumption Review

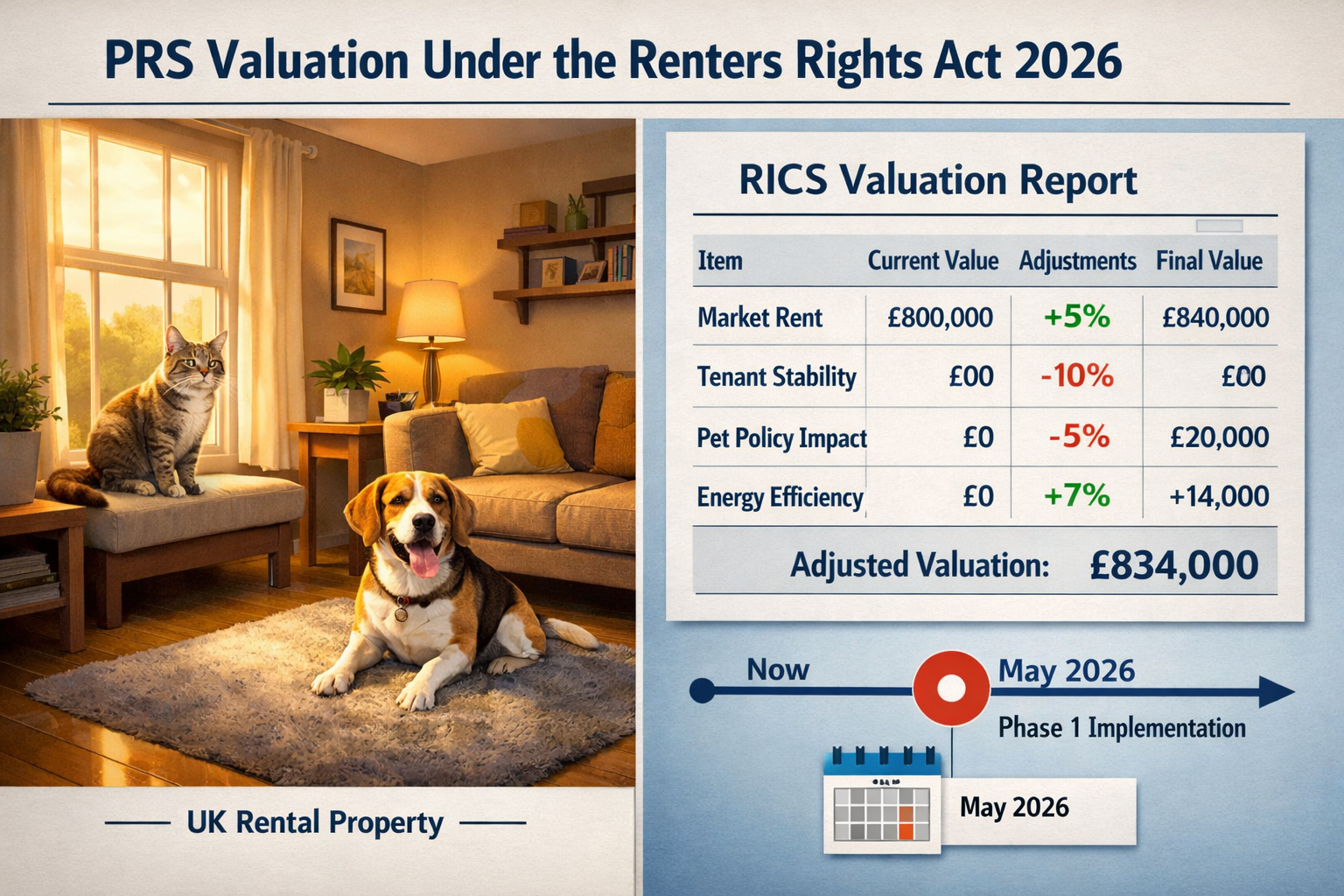

RICS has explicitly flagged that valuers must reassess the vacant possession assumption for all PRS properties [1]. Under the old regime, a landlord could issue a Section 21 notice and recover possession within approximately two months, making the vacant possession assumption relatively reliable for investment analysis.

Post-May 2026, possession requires:

- A valid Section 8 ground

- Notice periods of 2 weeks to 4 months depending on the ground

- Potential court proceedings if the tenant contests

This extended timeline affects:

- Reversionary value calculations

- Break clause assumptions in investment appraisals

- Discount rates applied to income streams with tenants in situ

Valuers conducting expert building evaluations for investment-grade PRS assets should now document their vacant possession reasoning explicitly in valuation reports.

2. Yield Adjustment for Rent Restriction Risk

The rent increase restrictions introduced by Phase 1 directly compress projected income growth [1]:

| Scenario | Pre-Act | Post-Act (May 2026) |

|---|---|---|

| Rent increase timing | Between fixed terms (typically 12–24 months) | No increase in first 12 months; one per year thereafter |

| Increase mechanism | Landlord discretion | Market value constraint applies |

| Investor certainty | Higher | Lower |

For investment valuations, this means discounted cash flow (DCF) models must use more conservative rent growth assumptions. A property previously valued on a 3% annual rent growth trajectory may now require a 1.5–2% assumption, with corresponding yield expansion.

Example adjustment illustration:

- Gross yield on a £350,000 London flat at £1,400/month: 4.8%

- Post-Act yield adjustment for possession risk and rent restriction: +0.3–0.5%

- Adjusted yield requirement: 5.1–5.3%

- Implied capital value reduction: approximately £15,000–£25,000

These figures are illustrative, but they reflect the directional pressure that RICS-compliant valuers are now expected to model.

3. Compliance Cost Capitalisation

The Act imposes enhanced due diligence requirements, including Decent Homes Standard compliance and deposit protection verification [1]. These create recurring compliance costs that reduce net operating income and must be capitalised into valuations.

For property evaluation purposes, surveyors should now assess:

- Cost of pet damage remediation between tenancies (carpets, flooring, paintwork)

- Insurance uplift associated with higher pet exposure

- Legal costs for Section 8 proceedings versus the former Section 21 route

- Ombudsman compliance costs once Phase 2 launches in late 2026

The PRS Ombudsman: Valuation Implications of the Compliance Gap

What the Ombudsman Will Do

The mandatory PRS Landlord Ombudsman is scheduled to launch in late 2026 as part of Phase 2 implementation [4]. Once operational, it will provide:

- A formal channel for tenant complaints about landlord conduct

- Binding dispute resolution on pet consent refusals and related matters

- Potential compensation awards against non-compliant landlords

- A public record of landlord compliance history

The May–December 2026 Gap

Between May 1, 2026 (when pet rights activate) and the Ombudsman's late-2026 launch, there is a structural compliance gap [4]. During this period:

- Pet-related disputes have no formal Ombudsman channel

- Tenants must rely on existing court processes or informal resolution

- Landlords face legal uncertainty about what constitutes "unreasonable" refusal

- Valuation risk during this gap period is arguably higher, not lower

For valuers assessing PRS properties in mid-2026, this gap represents an unquantified contingent liability. RICS guidance suggests that where uncertainty is material, valuers should note it explicitly and consider a special assumptions caveat in their reports [1].

Understanding property rights and how they interact with landlord obligations is essential context for any surveyor advising clients during this transitional period.

Post-Ombudsman Valuation Adjustments

Once the Ombudsman is operational, its existence will introduce a new layer of regulatory risk premium into PRS valuations. Properties with:

- Poor compliance histories — likely to face Ombudsman referrals

- High pet-exposure profiles — ground-floor, garden properties in family areas

- Leasehold restrictions on pets — creating consent conflicts between landlord and freeholder

…will carry measurably higher risk profiles. Investors and lenders will increasingly request evidence of Ombudsman registration and compliance track records as part of due diligence.

For complex leasehold assets, lease extension valuation advice should now incorporate Ombudsman compliance as a factor in the overall risk assessment.

Applying the RICS Framework: A Practical Checklist for Valuers

The Valuation Impacts of Renters' Rights Act 2026 Pet Rules and Ombudsman on PRS Properties: RICS Adjustment Frameworks translate into a concrete set of steps that every RICS-registered valuer should now follow for PRS instructions:

Pre-Inspection Due Diligence ✅

- Confirm tenancy start date — is it pre or post May 1, 2026?

- Identify whether pets are present or consent has been requested/granted

- Check leasehold title for pet restrictions (relevant to consent conflicts)

- Verify deposit protection scheme compliance

- Assess Decent Homes Standard compliance status

Valuation Methodology Adjustments ✅

- Document vacant possession assumption reasoning explicitly

- Apply conservative rent growth assumptions (reflect one-increase-per-year cap)

- Adjust yield to reflect extended possession timeline risk

- Capitalise compliance costs into net income calculations

- Note Ombudsman gap period as a contingent liability where material

Report Disclosure Requirements ✅

- State whether the Act's Phase 1 provisions apply to the subject tenancy

- Disclose any pet consent issues identified

- Reference RICS Expert Working Group guidance [1]

- Flag Phase 2 Ombudsman launch as a forward-looking risk factor

Surveyors conducting building surveys on PRS properties should integrate these checks into their standard inspection protocols alongside structural and condition assessments.

Market-Wide Implications: What the Data Suggests

The scale of potential market impact is substantial. With 4.6 million PRS properties in scope [5], even modest yield adjustments aggregate into significant capital value shifts across the sector.

Key market dynamics to monitor in 2026:

- 📉 Landlord exit acceleration — some smaller landlords may sell rather than navigate the new compliance landscape, increasing supply of ex-rental stock

- 📈 Institutional PRS growth — larger operators with compliance infrastructure are better positioned, potentially increasing their market share

- 🏠 Property type differentiation — houses with gardens (higher pet exposure) may see wider yield spreads versus flats in managed blocks with pet restrictions

- 💼 Lender policy updates — mortgage lenders are likely to update their PRS lending criteria to reflect the new possession timeline risks

For surveyors advising clients on which home survey is right for them, it's worth noting that buy-to-let investors may now require more detailed condition reports to baseline property condition before pet-owning tenants move in.

The financial implications for landlords who fail to adapt their valuation and management approach are considerable — both in terms of asset value erosion and regulatory penalty exposure.

Conclusion: Actionable Next Steps for Surveyors and Investors

The Renters' Rights Act 2026 is not a distant regulatory event — Phase 1 is already live. The valuation impacts of its pet rules, fee restrictions, possession changes, and the incoming Ombudsman are material, measurable, and must be reflected in every RICS-compliant PRS valuation conducted from May 2026 onward.

Immediate Actions for Chartered Surveyors 🎯

- Update valuation templates to include Act-specific disclosure fields and vacant possession assumption documentation

- Recalibrate yield benchmarks for PRS assets to reflect possession timeline risk and rent restriction impact

- Develop pet exposure scoring — a simple risk matrix based on property type, location, and tenancy profile

- Monitor RICS guidance updates as Phase 2 Ombudsman provisions are finalised in late 2026

- Advise investor clients on the compliance cost implications before they acquire new PRS assets

For Landlords and Investors 🎯

- Audit existing tenancies — identify which fall under the new pet consent rules

- Review insurance policies to ensure pet damage cover is adequate without prohibited fee structures

- Prepare Section 8 possession protocols — the Section 21 route is gone

- Register for Ombudsman membership ahead of the late-2026 launch to demonstrate proactive compliance

- Commission updated valuations on investment properties to reflect the new regulatory baseline

The intersection of pet rights, Ombudsman oversight, and RICS valuation methodology is complex — but it is navigable with the right professional guidance. The surveyors and investors who adapt their frameworks now will be best positioned as Phase 2 and Phase 3 of the Act continue to reshape the PRS landscape.

References

[1] Consideration Of Implications Of Renters Rights Act On Valuation – https://www.rics.org/news-insights/consideration-of-implications-of-renters-rights-act-on-valuation

[2] Preparing For 2026 Key Real Estate Law Reforms – https://www.tlt.com/insights-and-events/insight/preparing-for-2026-key-real-estate-law-reforms

[3] Renters Rights Act Implementation Roadmap – https://ww3.rics.org/uk/en/journals/property-journal/renters-rights-act-implementation-roadmap.html

[4] Renting With Pets – https://blog.goodlord.co/renting-with-pets

[5] Renters Rights Bill Impact Assessment – https://assets.publishing.service.gov.uk/media/67405a2353373262c0d825c5/Renters__Rights_Bill_Impact_assessment.pdf