Northern England's property market is quietly defying gravity. While London registered a net balance of -40% on house price sentiment in February 2026 and the South East followed at -24%, the North West of England, Scotland, and Northern Ireland held firm — recording positive or neutral price trends in the same period [1]. For surveyors operating across Yorkshire, Lancashire, Cheshire, and the wider northern regions, this divergence is not a footnote. It is the defining market story of 2026.

The concept of valuation resilience in regional divergence — the central theme of the RICS February 2026 Survey for Northern England surveyors — demands careful interpretation. Understanding why northern markets are outperforming, how long that advantage may last, and what it means for professional valuation practice is essential for any surveyor advising clients in these areas right now.

Key Takeaways 📌

- Northern England, Scotland, and Northern Ireland are outperforming southern markets on price sentiment by a significant margin in early 2026.

- National buyer demand fell sharply to a net balance of -26% in February 2026, driven by geopolitical uncertainty and elevated mortgage rates.

- Short-term price expectations turned negative nationally (-18%), but the 12-month outlook remains positive at +33%.

- Rental stock shortages (landlord instructions at -27%) are adding upward pressure on rents across all regions, including the North.

- Surveyors in Northern England must adapt valuation methodologies to reflect genuine regional conditions rather than applying national sentiment broadly.

Understanding the February 2026 RICS Data: A National Picture First

Before examining what valuation resilience in regional divergence means specifically for Northern England surveyors, it helps to understand the national backdrop that makes the regional story so striking.

Demand Is Weakening Nationally

The RICS UK Residential Survey for February 2026 recorded a net balance of -26% for new buyer enquiries — a notable drop from -15% in January [1]. Agreed sales followed the same trajectory, falling to a net balance of -12% [1]. These are not catastrophic numbers, but they represent a clear cooling of momentum that had briefly appeared to build at the start of the year.

Tarrant Parsons, RICS Head of Market Research & Analytics, noted that while some indicators suggested a tentative improvement at the start of 2026, the deterioration in the geopolitical backdrop has weighed on confidence — with rising oil and energy prices increasing the likelihood that mortgage rates will remain higher for longer [1].

The ongoing Middle East conflict has been specifically cited as a factor contributing to weakened buyer confidence and broader housing market slowdown [3]. Higher energy prices feed directly into inflation expectations, which in turn influence Bank of England rate decisions and, ultimately, mortgage pricing.

Supply Is Broadly Stable — But Not Surging

New vendor instructions registered a net balance of just +2% in February 2026 [1]. This near-flat reading tells an important story: sellers are not flooding the market. The supply pipeline is controlled, which acts as a floor under prices even when demand softens. Tim Green FRICS observed that the increased number of properties coming to the market is an early sign of activity in 2026, with recovery likely to be led from the first-time buyer segment [1].

Short-Term Caution vs. Long-Term Optimism

Perhaps the most nuanced data point from the February survey is the gap between short-term and long-term price expectations:

| Timeframe | Net Balance | Direction |

|---|---|---|

| Near-term price expectations | -18% | ⬇️ Cautious |

| 12-month price outlook | +33% | ⬆️ Positive |

| Current house prices (national) | -12% | ➡️ Broadly flat |

This divergence between short and long-term sentiment is significant for valuation professionals. It suggests that markets are experiencing a temporary confidence dip rather than a structural correction — a distinction that matters enormously when advising buyers, sellers, and lenders [1].

The Regional Divergence Story: Why Northern England Is Different

The headline finding that makes valuation resilience in regional divergence such a pressing topic for Northern England surveyors is the stark contrast between regional performances in the February 2026 data.

The North-South Price Gap in 2026

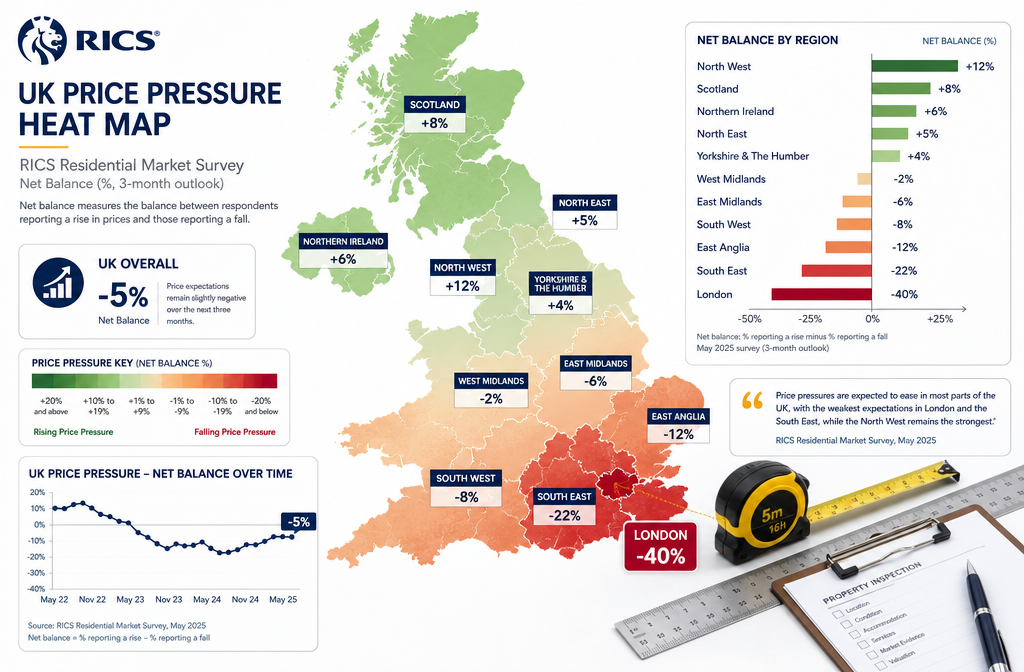

Regional price sentiment readings from the RICS February 2026 survey tell a clear story [1]:

- 🔴 London: Net balance of -40% (strong downward pressure)

- 🔴 South East: Net balance of -24% (notable downward pressure)

- 🔴 East Anglia: Net balance of -26% (notable downward pressure)

- 🟢 North West England: Positive/neutral (outperforming)

- 🟢 Scotland: Positive/neutral (outperforming)

- 🟢 Northern Ireland: Positive/neutral (outperforming)

By April 2026, this regional divide had widened further. Stronger downward pressure on prices was recorded in London, the South East, East Anglia, and the South West, while Northern England, Scotland, and Northern Ireland continued to outperform the rest of the UK [2].

Why Is the North Holding Up?

Several structural factors explain northern resilience:

- Relative affordability — Average house prices in Northern England remain significantly lower than southern equivalents, meaning mortgage rate sensitivity is proportionally lower.

- Regeneration investment — Cities like Manchester, Leeds, and Liverpool have attracted substantial public and private investment, supporting employment and local demand.

- First-time buyer activity — The first-time buyer market, identified by Tim Green FRICS as the likely engine of 2026 recovery [1], is more active in northern markets where entry-level prices are accessible.

- Lower exposure to international buyer retreat — London's price weakness is partly driven by reduced international and investor demand; northern markets are less exposed to this dynamic.

💬 "The increased number of properties coming to the market is an early sign of activity in 2026, though the recovery is likely to be led from the first-time buyer range." — Tim Green FRICS [1]

Practical Implications for Valuation Practice in Northern England

Understanding the lessons from the RICS February 2026 Survey for Northern England surveyors goes beyond reading the data — it requires translating that data into sharper, more defensible professional practice.

1. Resist National Sentiment Contamination

One of the most common valuation errors in a divergent market is allowing national headlines to distort local evidence. When national net balances are negative, there is a natural temptation to apply a cautious discount to northern valuations. The February 2026 data shows this would be methodologically incorrect [1].

Surveyors should anchor valuations firmly to local comparable evidence — recent sales, active listings, and time-on-market data specific to the subject property's postcode and property type. National sentiment is context, not evidence.

For clients seeking a thorough understanding of what a professional assessment involves, reviewing an example homebuyers report and complete property survey guide can clarify the distinction between market commentary and property-specific findings.

2. Calibrate Survey Type Recommendations to Market Conditions

In a market where prices are broadly holding but buyer confidence is fragile, the quality of survey advice becomes a competitive differentiator. Buyers in Northern England who are proceeding despite national uncertainty are often doing so because they have conviction in a specific property or location. They deserve survey advice that matches that conviction.

For most residential purchases in the North, the choice between a RICS HomeBuyer Survey and a RICS Building Survey should be driven by property age, type, and condition — not by market sentiment. Older Victorian and Edwardian terraces common across northern towns and cities often warrant a full Level 3 Building Survey given the potential for structural movement, damp, and aging services.

Understanding whether a HomeBuyer Report or Building Survey is the right choice is a question that comes up frequently in any active market — and getting that guidance right builds long-term client trust.

3. Address the Rental Market Dimension

The rental market data from February 2026 adds another layer of complexity for surveyors advising landlord clients. Tenant demand remained stable at a net balance of +2%, but landlord instructions were deeply negative at -27% [1]. This supply-demand imbalance is pushing rents upward — a trend that has valuation implications for buy-to-let properties and houses in multiple occupation (HMOs).

For surveyors conducting stock condition surveys for housing associations or private landlords in Northern England, the rental market squeeze means that asset condition and compliance are under greater scrutiny than ever. Properties that fail to meet minimum energy efficiency or habitability standards face both regulatory risk and rental income risk simultaneously.

4. Manage Client Expectations with Data-Led Communication

The gap between short-term caution (-18% near-term expectations) and long-term optimism (+33% twelve-month outlook) creates a communication challenge [1]. Clients who read negative headlines may be surprised to hear that their northern property is holding value. Surveyors who can explain this divergence clearly — using the RICS data as a framework — position themselves as trusted advisers rather than just report writers.

A structured approach to client communication might include:

- Contextualise the national data — explain why UK-wide figures do not apply uniformly

- Present local evidence — comparable sales, average days-on-market, local agent feedback

- Acknowledge uncertainty — geopolitical risks and mortgage rate trajectories remain genuine unknowns [3]

- Frame the 12-month outlook — the +33% positive expectation nationally suggests most professionals anticipate recovery, with northern markets likely to lead or match that trend [1]

Broader Survey Strategy in a Divergent Market

The theme of valuation resilience in regional divergence extends beyond residential valuations. Commercial property, development land, and mixed-use assets in Northern England are all subject to the same regional dynamics — and surveyors who understand those dynamics can provide more nuanced advice across all asset classes.

Development Viability

In a market where national demand is soft but northern demand is relatively firm, development viability assessments need to reflect local absorption rates rather than national benchmarks. A residential scheme in a well-connected northern suburb may have stronger sales velocity than equivalent schemes in the commuter belt south of Birmingham — a fact that should be reflected in residual land valuations.

Lender Scrutiny

Mortgage lenders are increasingly using regional data to calibrate their risk appetite. In a divergent market, surveyors providing mortgage valuations in Northern England may find that lenders are more receptive to supporting transactions than their southern-focused risk models might suggest. Equally, surveyors must be precise about which northern sub-markets are performing well and which are not — the regional picture is positive overall, but micro-market variations exist within the North itself.

First-Time Buyer Focus

As Tim Green FRICS highlighted, the 2026 recovery is likely to be led by first-time buyers [1]. Surveyors who position their services clearly for this demographic — offering transparent pricing, clear explanations of survey types, and accessible reporting — are well-placed to capture a growing share of transactions in Northern England.

For first-time buyers navigating the survey process for the first time, resources that demystify the process are genuinely valuable. Understanding common myths about property surveys can help buyers make more confident decisions — and surveyors who proactively address those myths build stronger client relationships.

Looking Ahead: What the April 2026 Data Confirms

The April 2026 RICS survey data reinforces the February findings with even greater clarity. The regional divide widened further, with stronger downward pressure recorded in London, the South East, East Anglia, and the South West, while Northern England, Scotland, and Northern Ireland continued to outperform [2].

This consistency across two consecutive monthly surveys is significant. It suggests that the regional divergence observed in February 2026 is not a statistical anomaly — it reflects genuine structural differences in how different parts of the UK are responding to the same macroeconomic pressures.

For surveyors building a practice in Northern England, this is a sustained competitive advantage. Markets that are outperforming nationally attract more transactions, more lender instructions, and more buyer activity — all of which translate into professional opportunity.

The broader range of RICS survey services available to property professionals provides a framework for meeting this demand across all property types and transaction contexts.

Conclusion: Turning Divergence Into Professional Advantage

The RICS February 2026 survey data presents a clear and actionable message for Northern England surveyors: regional divergence is real, measurable, and consequential. While national headlines focus on falling buyer enquiries and cautious short-term price expectations, the northern market is demonstrating genuine valuation resilience — and that resilience creates both professional responsibility and professional opportunity.

Actionable Next Steps for Northern England Surveyors 🎯

- Update your comparable evidence databases — ensure local sales data is current and granular enough to reflect sub-market variations within northern regions.

- Refine client communication templates — develop clear, data-led explanations of the national vs. regional divergence that clients can understand quickly.

- Review survey type recommendations — in a market where first-time buyers are driving activity, ensure your survey tier guidance is calibrated to property age and condition, not just price point.

- Monitor rental market dynamics — the landlord instruction shortage (-27%) has valuation implications for investment properties; stay current on local rental yields and compliance requirements.

- Track the RICS monthly surveys — the April 2026 data already confirms the February trend; monthly monitoring allows surveyors to spot shifts before they affect transaction volumes.

- Position expertise clearly — surveyors who can articulate the regional divergence story are more valuable to clients, lenders, and developers than those who rely solely on national benchmarks.

The lessons from the RICS February 2026 survey are not merely academic. They are a practical guide to operating with greater precision, greater confidence, and greater value in one of the UK's most resilient property markets.

References

[1] UK Residential Survey February 2026 – https://www.rics.org/news-insights/uk-residential-survey-february-2026?utm_source=openai

[2] UK Residential Survey April 2026 – https://www.rics.org/news-insights/uk-residential-survey-april-2026?utm_source=openai

[3] UK Housing Market Slows As Ongoing Middle East Conflict Raises Borrowing Costs – https://www.rics.org/news-insights/uk-housing-market-slows-as-ongoing-middle-east-conflict-raises-borrowing-costs?utm_source=openai

[4] Valuation Divergences in RICS Q1 2026 Survey: North West Surge Tactics for Surveyors Targeting Resilient Markets – https://wimbledonsurveyors.com/valuation-divergences-in-rics-q1-2026-survey-north-west-surge-tactics-for-surveyors-targeting-resilient-markets/?utm_source=openai