Six point three million properties across England already sit in areas at risk of flooding from rivers, sea, or surface water — and that number is projected to climb to 8 million, or one in four properties, by mid-century [2]. After the spring 2026 flood events accelerated pressure on surveyors, valuers, and buyers alike, the question is no longer whether flood risk affects property value. The question is how precisely surveyors should quantify that risk using the latest Environment Agency data.

Flood Risk Valuations Post-Spring 2026 Events: Building Survey Integration with Environment Agency Data represents a fundamental shift in how property professionals approach assessments. This article sets out clear protocols for surveyors to adjust valuations using real-time flood data, integrate resilience measures into reports, and serve cautious buyers and lenders in a market that has permanently changed.

Key Takeaways 📋

- 6.3 million English properties are currently at flood risk; projections suggest 8 million by mid-century [2].

- The Environment Agency's updated Flood Map for Planning (January 2026) now includes surface water climate change extents and banded depth layers in a single service [4].

- Surveyors must cross-reference multiple EA data layers — not just flood zone classification — to produce defensible valuations.

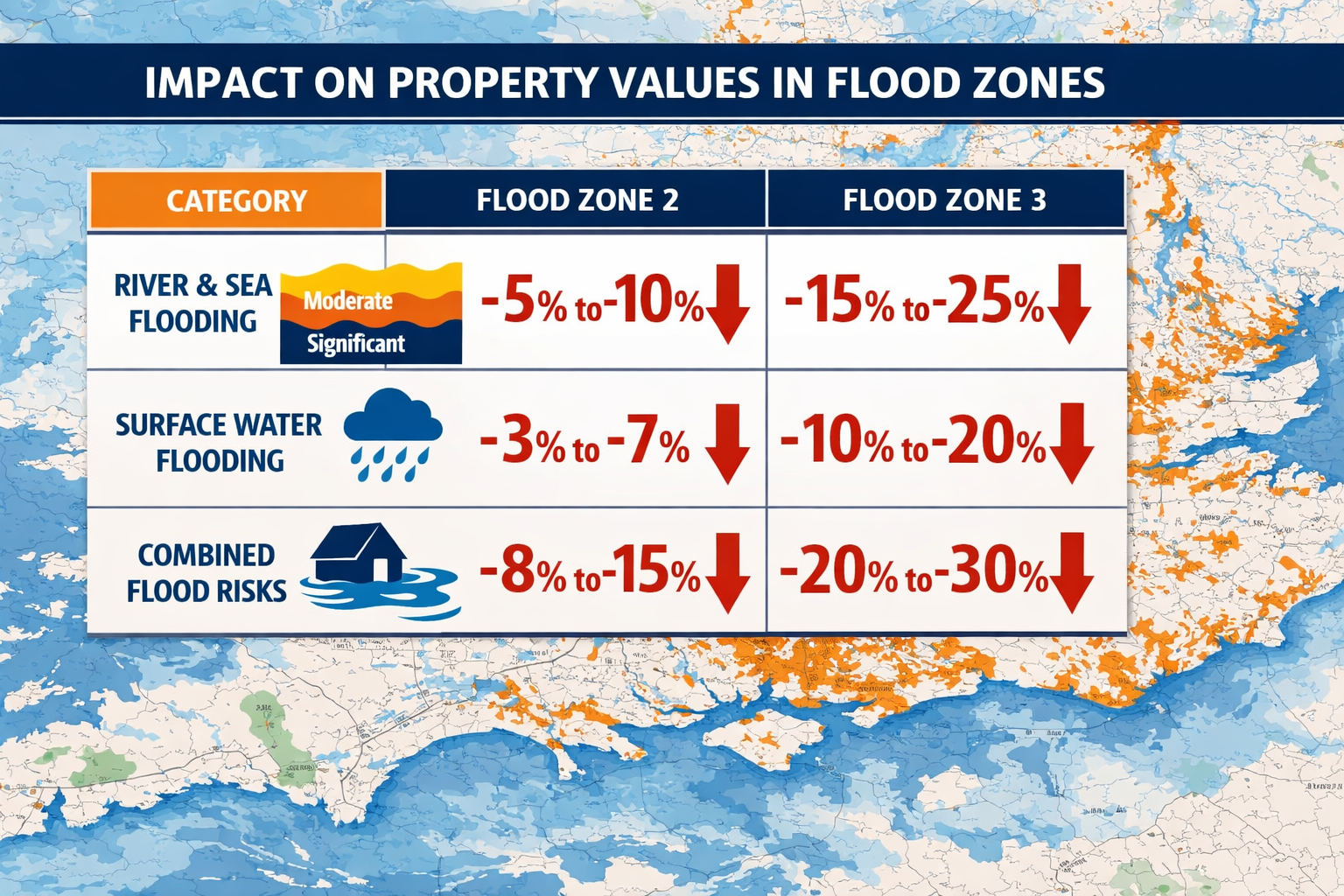

- Flood risk can reduce property values by 5% to 20%+ depending on zone, depth, and resilience measures in place.

- Post-spring 2026, lenders are increasingly requiring flood risk commentary in Level 2 and Level 3 building surveys before issuing mortgage offers.

Why Spring 2026 Changed the Flood Risk Valuation Landscape

The spring 2026 flood events across parts of southern England, the Thames Valley, and low-lying areas of the East Midlands served as a stress test for property markets that many professionals had been quietly anticipating. Insurance premiums spiked. Several lenders tightened their lending criteria for Flood Zone 3 properties. And buyers — better informed than any previous generation — began requesting flood risk commentary as a standard element of building surveys.

This shift did not emerge from nowhere. The Environment Agency had been progressively updating its data infrastructure for precisely this moment. In December 2025, the EA announced significant changes to the Flood Map for Planning (FMfP) service, adding new surface water climate change extents and banded depth layers scheduled for January 2026 [4]. Crucially, this update eliminated the need for planners and surveyors to separately cross-reference the Check Your Long-Term Flood Risk (CYLTFR) service — consolidating risk intelligence into one authoritative platform [3].

💬 "The integration of surface water data into the core planning flood map is the single most important change for property professionals in a decade." — Industry commentary, 2026

For chartered surveyors operating across London and the South East, this consolidation means that the excuse of incomplete data no longer holds. The tools are available. The professional obligation is to use them.

Understanding the Updated Environment Agency Data Framework

The New Flood Map for Planning: What Changed in January 2026

The January 2026 updates to the FMfP represent the most comprehensive overhaul of national flood risk data in years. The key additions include [3] [4]:

| New Data Layer | What It Shows | Why It Matters for Valuations |

|---|---|---|

| Surface water climate change extents | Projected surface water flooding under future climate scenarios | Reveals risk invisible in traditional river/sea flood zones |

| Banded depth layers | Flood depth categories (shallow, medium, deep) | Enables proportionate valuation adjustments |

| Updated fluvial flood zone boundaries | Revised river flood extents based on new modelling | May reclassify properties previously considered low risk |

| Coastal erosion risk updates | Revised shoreline change projections | Critical for coastal property valuations |

Prior to this update, surveyors relying solely on the three-zone classification system (Flood Zone 1, 2, 3) were working with an incomplete picture [1]. A property sitting in Flood Zone 1 — nominally low risk — could still face significant surface water flood risk that only appeared in the separate CYLTFR service. The January 2026 integration closes that gap [5].

Climate Risk Scores: Emerging Scrutiny

A 2026 study highlighted by Rice University researchers raised important questions about the reliability of proprietary climate risk scores used by insurers and lenders, noting that methodological differences between scoring systems can produce materially different risk assessments for the same property [6]. For surveyors, this reinforces the importance of anchoring valuations to publicly verifiable EA data rather than relying exclusively on third-party risk scores.

Flood Risk Valuations Post-Spring 2026 Events: Building Survey Integration with Environment Agency Data — A Practical Protocol

Step 1: Pre-Inspection Data Gathering

Before setting foot on a property, surveyors should complete a structured data review using the following sources:

- ✅ Environment Agency Flood Map for Planning — check flood zone, surface water extents, and depth layers

- ✅ Long-Term Flood Risk service — verify river, sea, surface water, reservoir, and groundwater risk categories

- ✅ Historical flood event records — check EA recorded flood outlines for the specific area

- ✅ Local authority Strategic Flood Risk Assessment (SFRA) — particularly relevant post-spring 2026 events where SFRAs may have been updated

- ✅ Insurance flood data (where accessible) — cross-reference with EA data

For properties in areas affected by the spring 2026 events, surveyors should specifically check whether flood zone boundaries have been updated in the post-event EA data releases [3].

Step 2: On-Site Flood Risk Assessment

During the physical inspection, the surveyor should document:

🔍 Physical evidence of flooding:

- Tide marks on internal or external walls

- Damaged or replaced floor finishes at ground level

- Evidence of previous damp remediation (see our guidance on damp survey costs and assessments)

- Condition of drainage infrastructure and outflows

- Proximity to watercourses, culverts, or drainage channels

🔍 Resilience measures already in place:

- Flood barriers (temporary or permanent)

- Non-return valves on drainage

- Raised electrical sockets and consumer units

- Flood-resistant door and window seals

- Sump pumps and tanking systems

The presence or absence of these measures directly informs the resilience-adjusted valuation figure.

Step 3: Valuation Adjustment Framework

Post-spring 2026, a structured valuation adjustment approach is essential for defensibility. The following framework provides a starting point — surveyors should apply professional judgement and local market evidence alongside these parameters:

| Flood Zone / Risk Category | No Resilience Measures | Basic Resilience in Place | Full Resilience Package |

|---|---|---|---|

| Zone 1 (low risk, surface water only) | -2% to -5% | -1% to -3% | Minimal adjustment |

| Zone 2 (medium risk) | -5% to -10% | -3% to -7% | -2% to -5% |

| Zone 3a (high risk, developable) | -10% to -20% | -7% to -15% | -5% to -10% |

| Zone 3b (functional floodplain) | -20% or greater | -15% to -20% | -10% to -15% |

| Post-spring 2026 event area | Additional -3% to -8% stigma adjustment | Reduced stigma with evidence of remediation | Surveyor discretion |

⚠️ Important: These figures are indicative ranges based on market evidence and professional guidance. Local comparable sales data must always be the primary driver of valuation adjustments.

For buyers considering properties in affected areas, the ability to renegotiate after a poor building survey result is a legitimate and increasingly common outcome where flood risk is identified post-offer.

Step 4: Integrating Resilience Measures into Survey Reports

A high-quality flood risk section in a building survey should include:

- EA flood zone classification with specific reference to the January 2026 updated mapping

- Surface water risk category from the updated FMfP data layers

- Depth band where available from EA banded depth data

- Physical evidence observed during inspection

- Existing resilience measures — described and assessed for adequacy

- Recommended resilience improvements — with indicative costs

- Valuation impact commentary — clearly stated and justified

- Insurance implications — reference to Flood Re eligibility where applicable

Building surveys that omit structured flood risk commentary are increasingly viewed as incomplete by lenders and buyers in 2026's cautious market.

Flood Risk Valuations Post-Spring 2026 Events: Regional Considerations for London and the South East

High-Risk Locations Requiring Enhanced Due Diligence

The spring 2026 events disproportionately affected certain London boroughs and surrounding areas. Surveyors operating in these locations should apply enhanced flood risk protocols:

- Wandsworth and Fulham — Thames tidal risk combined with surface water vulnerability (Wandsworth property surveys | Fulham property surveys)

- Newham and Stratford — historically low-lying, significant surface water risk (Newham property surveys | Stratford property surveys)

- Richmond — River Thames flood plain exposure (Richmond property surveys)

- Havering and Romford — East London river system risks (Havering property surveys | Romford property surveys)

For first-time buyers in particular, the complexity of flood risk data can be overwhelming. A professional building survey for first-time buyers that clearly explains EA data in plain language is an essential service in 2026.

The Lender Perspective

Post-spring 2026, several UK mortgage lenders have updated their internal flood risk policies. Key trends include:

- Mandatory flood risk commentary in survey reports for properties in Flood Zones 2 and 3

- Retention clauses linked to completion of flood resilience works

- Reduced LTV ratios for properties with recent flood history and no resilience measures

- Referral to specialist underwriters for properties in post-event affected areas

Surveyors who produce reports without adequate flood risk commentary face increasing liability exposure as lenders tighten their requirements.

Resilience Measures: What Adds Value and What Does Not

Not all flood resilience investments deliver equal valuation uplift. The following breakdown helps surveyors advise clients accurately:

High-value resilience measures (strong valuation uplift):

- ✅ Professionally installed flood doors and barriers with certification

- ✅ Non-return valves on all drainage entry points

- ✅ Raised electrical installations (consumer units, sockets above 600mm)

- ✅ Flood-resilient ground floor finishes (concrete, tiles rather than timber)

- ✅ Sump pump systems with battery backup

Moderate-value measures:

- 🔶 Temporary flood barriers (demountable systems)

- 🔶 Tanked basement or lower ground floor

- 🔶 Flood-resistant external render

Limited valuation impact (but important for insurance):

- ⚪ Flood alert registration

- ⚪ Emergency flood kit

- ⚪ Flood resilience survey documentation only

The distinction matters because surveyors should not over-credit measures that reduce insurance claims but do not materially reduce flood damage risk to the structure.

Conclusion: Actionable Next Steps for Surveyors and Buyers in 2026

The convergence of spring 2026 flood events and the Environment Agency's most significant data update in years has created both a challenge and an opportunity for property professionals. Flood Risk Valuations Post-Spring 2026 Events: Building Survey Integration with Environment Agency Data is no longer a niche specialism — it is a core competency for any surveyor working in England.

Immediate actions for surveyors:

- Update your pre-inspection checklist to include all January 2026 EA data layers, including surface water climate change extents and depth bands [4]

- Develop a standardised flood risk section for Level 2 and Level 3 survey reports with clear valuation adjustment methodology

- Build local comparable evidence for flood-affected properties in your area — this is the foundation of defensible adjustments

- Engage with local authority SFRAs updated post-spring 2026 for area-specific intelligence

- Communicate clearly with clients about the difference between flood zone classification and actual flood risk — the January 2026 updates make this conversation more important than ever [3]

For buyers and property owners:

- Commission a full building survey that explicitly addresses EA flood data — not just a basic valuation

- Ask your surveyor to confirm they have checked the updated January 2026 FMfP data layers

- Investigate Flood Re eligibility before committing to purchase in affected areas

- Budget for resilience measures as part of purchase negotiations — and use survey findings to support price renegotiation where appropriate

The data is available. The methodology is established. The professional standard in 2026 demands that flood risk is treated with the same rigour as structural condition, damp, or electrical safety. Surveyors who lead on this will build the trust that cautious markets reward.

References

[1] The Updated Environment Agency Flood Risk Mapping Is Here – https://www.fairhurst.co.uk/the-updated-environment-agency-flood-risk-mapping-is-here/

[2] Environment Agency Publishes Major Update To National Flood And Coastal Erosion Risk Assessment – https://www.watermagazine.co.uk/2024/12/17/environment-agency-publishes-major-update-to-national-flood-and-coastal-erosion-risk-assessment/

[3] Updates To National Flood And Coastal Erosion Risk Information – https://www.gov.uk/guidance/updates-to-national-flood-and-coastal-erosion-risk-information

[4] New National Flood And Coastal Erosion Risk Information – https://www.tcpa.org.uk/resources/new-national-flood-and-coastal-erosion-risk-information/

[5] Fmfp Update – https://www.luciongroup.com/news/fmfp-update/

[6] Climate Risk Scores Shape Billion Dollar Decisions And New Study Says Science Behind Them – https://news.rice.edu/news/2026/climate-risk-scores-shape-billion-dollar-decisions-and-new-study-says-science-behind-them