Nearly one in five leasehold flats listed for sale in England currently carries at least one of three critical risk factors — a short lease, an onerous ground rent, or unresolved cladding defects. When all three converge on a single property, the valuation challenge becomes one of the most complex exercises a RICS-registered surveyor can face. Valuing Properties with Short Leases, Escalating Ground Rents, and Cladding Issues: How UK Surveyors Balance Risk in 2026 is not simply a matter of applying a percentage discount and moving on. It demands a structured, evidence-based framework that communicates risk clearly to lenders, buyers, and solicitors alike.

This article builds that framework — covering how to evidence the impact on value, explain risk to all parties, and document assumptions with precision.

Key Takeaways 📋

- Short leases (below 80 years) trigger marriage value calculations and can make a property unmortgageable without extension.

- Escalating ground rents — particularly doubling clauses — remain a significant red flag for lenders even after the Leasehold Reform (Ground Rent) Act 2022.

- Cladding issues without a valid EWS1 form or equivalent assurance continue to suppress values and block mortgage lending in 2026.

- Surveyors must document assumptions explicitly, not just flag issues — vague reports expose professionals to negligence claims.

- A three-layer risk framework (lease, ground rent, cladding) applied consistently gives buyers and lenders the clearest possible picture.

Understanding the Three-Layer Risk Problem

Why These Three Factors Rarely Arrive Alone

The uncomfortable reality of the UK leasehold market is that short leases, problematic ground rents, and cladding defects tend to cluster. Older purpose-built blocks — particularly those built between the 1960s and early 2000s — often carry leases that have naturally eroded over time, ground rent structures written before modern consumer protections existed, and external wall systems that predate post-Grenfell safety standards.

When valuing properties with short leases, escalating ground rents, and cladding issues, surveyors cannot treat each factor in isolation. Each one affects the others. A flat with 72 years remaining on its lease might be marginally mortgageable — but add an escalating ground rent and a pending EWS1 assessment, and the lender pool shrinks to near zero.

💬 "The valuation is not just about what the property is worth today — it is about what a willing buyer can actually pay for it, given the financing constraints each risk factor creates."

The Lender Perspective: Why Financing Constraints Drive Value

Most residential mortgage lenders in the UK apply strict criteria:

| Risk Factor | Typical Lender Threshold | Impact on Value |

|---|---|---|

| Lease length | Minimum 70–85 years (varies by lender) | Severe below 80 years |

| Ground rent | Must not exceed 0.1% of property value annually | Can render unmortgageable |

| Cladding / EWS1 | EWS1 A1/A2 or B1 required for most flats above 18m | Can block lending entirely |

Because value in a market context reflects what a buyer can pay — not just what they might theoretically offer — financing constraints directly suppress market value. A surveyor who ignores this conflates theoretical worth with real-world saleability.

Evidencing the Impact on Value: A Structured Approach

Layer One: Short Lease Adjustments

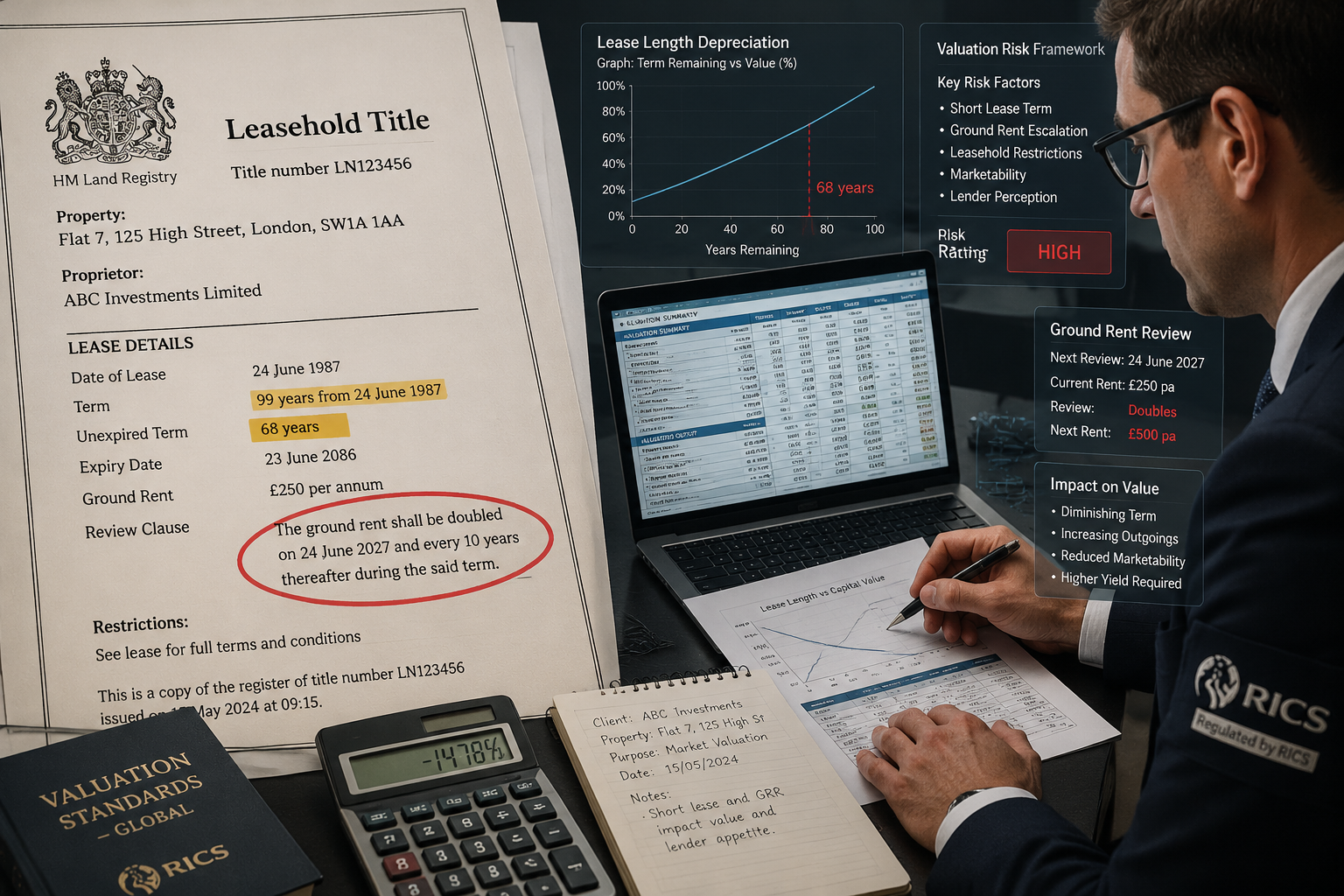

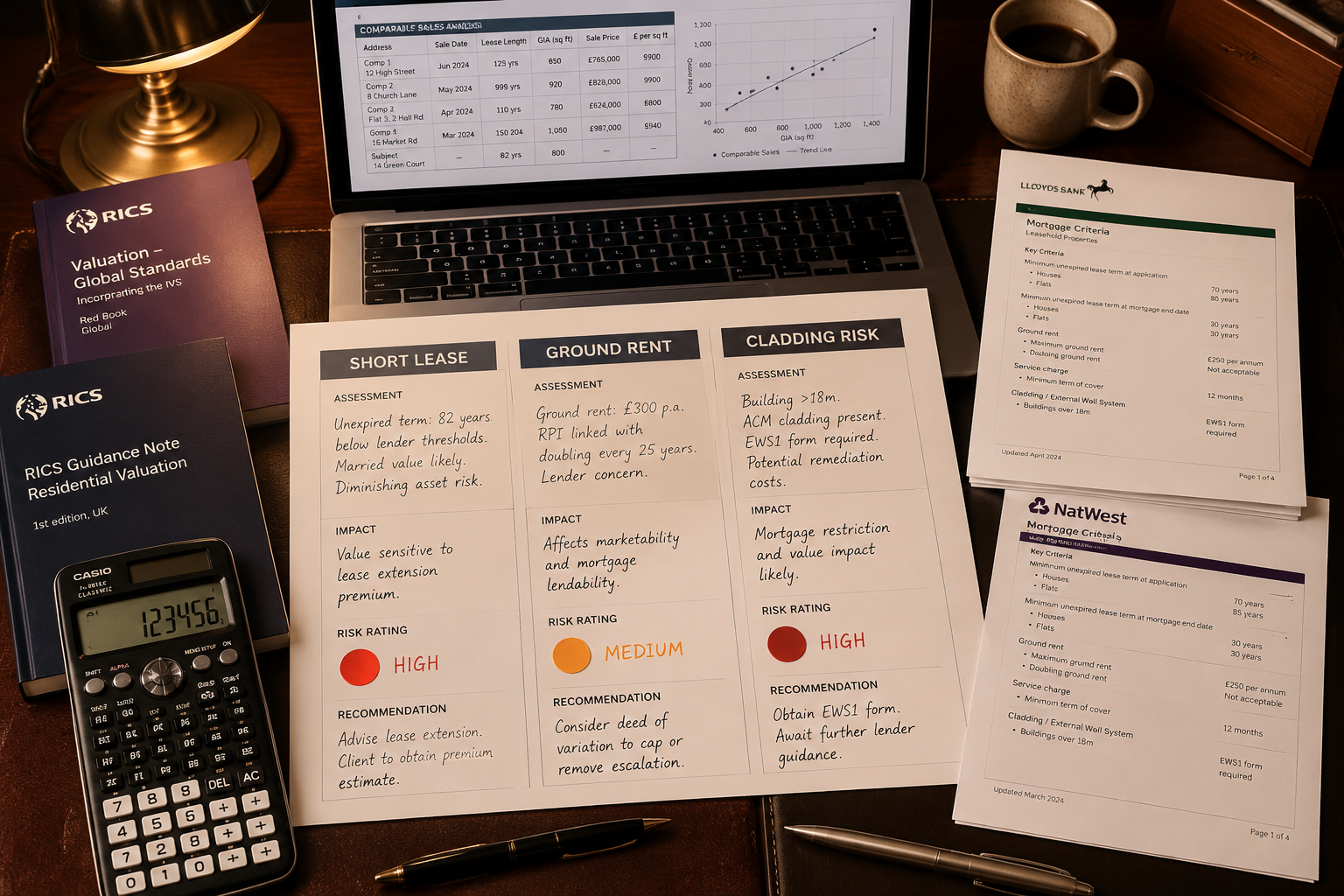

The mathematics of short lease valuation are well-established under the Leasehold Reform, Housing and Urban Development Act 1993. Once a lease falls below 80 years, marriage value becomes payable — typically 50% of the uplift in value that a lease extension would create. This is not a soft discount; it is a calculable figure.

Surveyors should:

- State the unexpired lease term explicitly in the report

- Calculate or reference the estimated cost of lease extension using Deferment Rate and Relativity tables

- Reference comparable sales of similar properties with and without extended leases in the same block or locality

- Note which lenders are likely to decline based on the lease length

For properties with leases below 70 years, the surveyor should consider whether a Special Assumptions section is warranted — for example, valuing "subject to a lease extension being granted" as a separate figure alongside the as-is value. This gives buyers and lenders a realistic picture of the property's potential and its current constraints.

Understanding how to negotiate the purchase price after a survey is especially relevant here — a well-evidenced short lease adjustment gives buyers concrete grounds to renegotiate.

Layer Two: Escalating Ground Rent Analysis

The Leasehold Reform (Ground Rent) Act 2022 capped ground rents at a "peppercorn" for new leases in England and Wales. However, existing leases with doubling clauses, RPI-linked escalators, or fixed-step increases remain in circulation and continue to cause valuation problems in 2026.

The key question is not just the current ground rent figure — it is the trajectory. A ground rent of £250 per annum doubling every 10 years becomes £4,000 per annum within 40 years. At that level, it may be classified as an assured tenancy under the Housing Act 1988 (where annual ground rent exceeds two-thirds of the rateable value), which historically triggered mortgage refusals.

Surveyors should document:

- The current ground rent amount

- The review mechanism (doubling, RPI, fixed step)

- The projected ground rent at key future dates (10, 20, 40 years)

- Whether the ground rent breaches lender thresholds now or will do so within the mortgage term

- Any evidence that the freeholder has agreed to vary the lease

⚠️ Pull Quote: "A ground rent clause that looks manageable today can render a property unsaleable within a single mortgage term. Surveyors must model the trajectory, not just the current figure."

For buyers considering properties in areas with high concentrations of leasehold stock, working with a local property surveyor who understands regional leasehold patterns is particularly valuable.

Layer Three: Cladding and External Wall System Risk

The EWS1 (External Wall System) process, introduced by UK Finance and the Royal Institution of Chartered Surveyors in 2019, remains the primary mechanism for assessing fire safety risk in multi-storey residential buildings in 2026. Despite government remediation schemes and the Building Safety Act 2022, a significant number of buildings still await assessment or remediation.

The valuation impact of cladding issues depends on:

- Building height — Buildings under 11 metres are generally lower risk; those above 18 metres face the strictest scrutiny

- EWS1 status — A1/A2 (no remediation needed) or B1 (works needed but low risk) ratings allow most lenders to proceed; B2 (works needed, higher risk) typically blocks lending

- Remediation funding — Is the developer or government funding remediation, or will leaseholders face service charge demands?

- Timescales — Unresolved remediation with no clear timeline creates the greatest uncertainty and the deepest value discount

When valuing properties with short leases, escalating ground rents, and cladding issues, the cladding layer often interacts most severely with financing. A property might have a manageable lease and an acceptable ground rent, but an outstanding EWS1 assessment can make it entirely unmortgageable regardless.

Surveyors working in areas with significant post-war and early 2000s flat stock — such as those covered by Southwark property surveyors or Brent property surveyors — encounter these combined risk scenarios regularly.

Communicating Risk to Lenders and Buyers: Report Documentation Standards

Why Vague Reports Create Liability

A report that states "the lease is short and may affect value" without quantifying the impact, or "cladding issues are noted" without explaining the EWS1 status, fails both the client and the profession. In 2026, with negligence claims in the surveying sector at elevated levels, explicit documentation of assumptions is not optional — it is a professional and legal necessity.

The RICS Valuation — Global Standards (Red Book) and the RICS Home Survey Standard both require surveyors to state clearly:

- What information was available at the time of inspection

- What assumptions were made in the absence of information

- What Special Assumptions (if any) were applied

- How each risk factor influenced the reported figure

A Practical Documentation Framework

The following structure helps surveyors produce consistent, defensible reports when three risk factors converge:

Section A: Lease Analysis

- State unexpired term

- Confirm whether marriage value applies

- Provide estimated lease extension cost range (or direct to specialist)

- State impact on lender eligibility

Section B: Ground Rent Assessment

- Quote current ground rent

- Describe the review mechanism verbatim from the lease (if available)

- Project future ground rent at 10-year intervals

- State whether current or projected figures breach standard lender criteria

Section C: Cladding and Fire Safety

- Confirm building height and number of storeys

- State EWS1 status if available, or confirm it is outstanding

- Note any government or developer remediation commitments

- Advise whether the property is likely to be mortgageable in its current state

Section D: Composite Value Assessment

- Provide the Market Value figure

- State clearly what assumptions underpin it

- Where appropriate, provide a "subject to resolution" figure showing potential value if all three issues were resolved

- Recommend specialist advice (lease extension solicitor, fire safety engineer) where needed

This structured approach mirrors the rigour described in choosing between a homebuyers survey and a full structural survey — the right level of investigation must match the complexity of the property.

Explaining Risk to Buyers Without Causing Panic

Buyers receiving a report flagging all three risk factors simultaneously can feel overwhelmed. Surveyors have a professional duty to communicate findings clearly and proportionately. Practical language tips:

-

✅ Do: "The lease has 71 years remaining. This means most high-street lenders will require a lease extension before offering a mortgage. The estimated cost of extension is typically £X–£Y for a property of this type."

-

❌ Avoid: "The short lease may cause issues."

-

✅ Do: "The ground rent doubles every 10 years. By 2046 it will reach approximately £1,200 per annum, which may breach lender thresholds."

-

❌ Avoid: "Ground rent escalation is noted."

Buyers who understand the specific financial implications — and the pathways to resolution — are better placed to make informed decisions. Directing them to renegotiate after a poor building survey result is a natural next step when multiple risk factors are identified.

Balancing Risk: The Surveyor's Professional Judgement in 2026

When All Three Factors Converge

The most challenging scenario — and increasingly common in London and other major urban centres — is a flat presenting all three issues simultaneously. In these cases, the surveyor's role extends beyond number-crunching. It requires:

- Prioritising the most immediately material risk (usually the one blocking financing)

- Sequencing advice so buyers understand which issues to address first

- Being explicit about uncertainty — where EWS1 assessments are pending or lease extension negotiations are unresolved, the valuation figure carries inherent uncertainty that must be stated

For example, a flat in a tower block with 68 years on the lease, a doubling ground rent currently at £400 per annum, and an outstanding EWS1 assessment might be valued at a significant discount to comparable properties in the same area with none of these issues. The surveyor should:

- Calculate the discount attributable to the lease (using relativity tables)

- Assess the additional discount for the ground rent trajectory

- Apply a further discount or "subject to" caveat for the unresolved cladding position

- State the composite Market Value with full transparency about what could change it

This level of analysis is what distinguishes a professional valuation from a superficial one. It also protects the surveyor — a clearly reasoned, documented approach is far more defensible than a figure arrived at without explanation.

For buyers and investors in complex leasehold markets across London, working with experienced surveyors — whether through Knightsbridge property surveyors or Hammersmith property surveyors — ensures these nuances are properly captured.

The Role of Comparable Evidence

No risk adjustment is defensible without comparable evidence. Surveyors should:

- 🔍 Search for sales of similar flats with and without the specific risk factors in the same block or postcode

- 🔍 Note where comparable sales were achieved at a discount and document the likely reason

- 🔍 Reference any published research or RICS guidance on value impacts of EWS1 status or ground rent escalation

- 🔍 Acknowledge where the market for such properties is thin and comparable evidence is limited

Thin comparable evidence does not mean the surveyor avoids giving a figure — it means the uncertainty range around that figure must be explicitly stated.

Understanding property valuation principles in the context of distressed or complex leasehold stock is an evolving area, and surveyors are well advised to stay current with RICS guidance updates throughout 2026.

Conclusion: A Framework That Protects Everyone

Valuing Properties with Short Leases, Escalating Ground Rents, and Cladding Issues: How UK Surveyors Balance Risk in 2026 is ultimately about professional rigour in the face of compounding complexity. The three-layer framework — lease analysis, ground rent trajectory, cladding and fire safety assessment — gives surveyors a consistent structure that serves buyers, lenders, and the profession itself.

Actionable Next Steps for Surveyors and Buyers 🎯

- Surveyors: Adopt the four-section report structure (Lease, Ground Rent, Cladding, Composite Value) as standard for any leasehold property with one or more risk flags.

- Buyers: Do not accept a report that identifies these issues without quantifying their financial impact — ask for specific figures and lender eligibility guidance.

- Lenders and solicitors: Engage with the surveyor's assumptions section — if the valuation is conditional on resolution of a risk factor, that condition needs to be tracked through to completion.

- All parties: Recognise that in 2026, the UK leasehold market still contains significant numbers of problem properties. Early identification and clear communication — not avoidance — is the only path to informed transactions.

When all three risk factors converge, the surveyor who documents clearly, evidences rigorously, and communicates proportionately is not just protecting their professional indemnity — they are providing genuine value to everyone in the chain.