"

Nearly one in three UK property transactions that proceed to survey stage result in a price renegotiation, repair request, or mortgage retention — yet most buyers treat the survey as a formality rather than the powerful negotiating instrument it truly is. Understanding the journey from survey to settlement: how building surveys shape negotiations between UK buyers, sellers and lenders can mean the difference between overpaying by tens of thousands of pounds or walking away from a deal that was never worth making.

This guide explores how Level 2 and Level 3 survey findings translate into real-world negotiating leverage, what lenders actually do with survey data, and — critically — how to frame conversations with sellers using language that gets results.

Key Takeaways 📋

- Level 2 and Level 3 surveys produce different depths of evidence, directly affecting how strongly a buyer can negotiate.

- Condition ratings (traffic-light system) are the clearest tool for prioritising which defects warrant price reductions or repair demands.

- Mortgage lenders may impose retention clauses or reduce loan offers based on survey findings — independent of the buyer's own negotiations.

- Sellers respond better to specific, costed repair evidence than to vague requests for discounts.

- Knowing when to walk away is as important as knowing how to negotiate — and a good survey tells you which situation you're in.

Understanding What Level 2 and Level 3 Surveys Actually Reveal

Before exploring how survey findings shape negotiations, it is essential to understand what each survey type delivers — because the depth of evidence determines the strength of any negotiating position.

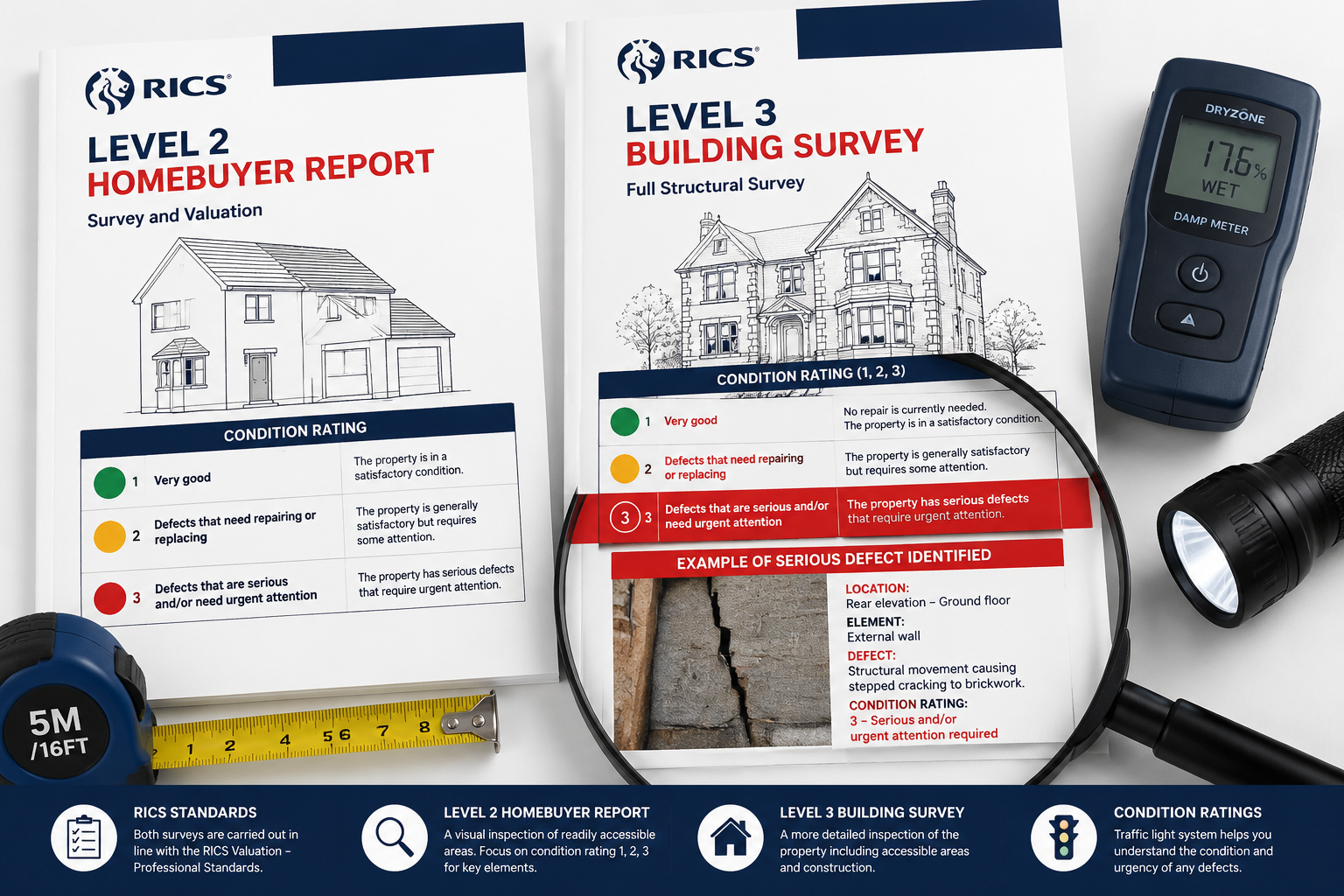

Level 2: The HomeBuyer Report

A Level 2 HomeBuyer Report is a standardised RICS document suited to conventional properties in reasonable condition. It uses a traffic-light condition rating system:

| Condition Rating | Meaning | Negotiating Weight |

|---|---|---|

| 🟢 1 – No action | No significant issues | Minimal |

| 🟡 2 – Attention needed | Defects requiring monitoring or repair | Moderate |

| 🔴 3 – Urgent action | Serious defects requiring immediate attention | Significant |

A Level 2 survey provides a useful snapshot but does not always include opening up of floors, detailed structural investigation, or specialist referrals as standard. For buyers of older or more complex properties, a full building survey is almost always the better choice.

Level 3: The Full Building Survey

A Level 3 Building Survey is the most comprehensive residential survey available. It suits:

- Properties built before 1900

- Non-standard construction (timber frame, thatched roofs, etc.)

- Properties that have been significantly extended or altered

- Any property where the buyer suspects hidden problems

Level 3 reports include detailed descriptions of defects, their likely causes, and — crucially for negotiation — recommendations for specialist investigations. This additional depth transforms the survey from a checklist into a legal and financial document that carries genuine weight at the negotiating table.

💬 Pull Quote: "A Level 3 survey does not just tell you what is wrong — it tells you why it is wrong, how serious it is, and what it will cost to fix. That is the foundation of every successful price negotiation."

For first-time buyers especially, understanding why commissioning a building survey is a non-negotiable step can protect against costly surprises after completion.

From Survey to Settlement: How Building Surveys Shape Negotiations Between UK Buyers, Sellers and Lenders in Practice

This is where theory meets reality. The journey from survey to settlement: how building surveys shape negotiations between UK buyers, sellers and lenders plays out across three distinct relationships — and each requires a different approach.

Negotiating with Sellers: Turning Defects into Discounts

When a survey reveals defects, buyers have three options:

- Request a price reduction equivalent to the estimated repair cost

- Ask the seller to carry out repairs before completion

- Walk away if the defects are too severe or the seller is unwilling to negotiate

The most effective approach is almost always option one, backed by specific evidence. Sellers are far more likely to respond to a costed schedule of works than a vague request for "a reduction."

📌 Sample Scenario: Damp and Timber Decay

A buyer commissions a Level 3 survey on a 1930s semi-detached property in South London. The surveyor identifies rising damp in two ground-floor rooms and evidence of woodworm in the suspended timber floor.

Ineffective approach:

"The survey found some damp issues. We'd like £5,000 off the price."

Effective approach:

"Our Level 3 building survey, conducted by a RICS-chartered surveyor, has identified rising damp in the front reception room and dining room, along with active woodworm infestation in the suspended timber floor. We have obtained two independent contractor quotes totalling £8,400 for damp-proof course installation, timber treatment, and floor reinstatement. We are requesting a price reduction of £8,400 to reflect these remediation costs, supported by the attached survey extract and contractor estimates."

The difference is specificity and documentation. Sellers and their solicitors take costed, evidenced requests far more seriously. For guidance on how to renegotiate after a poor survey result, the approach above forms the template.

📌 Sample Scenario: Structural Movement

A Level 3 survey on a Victorian terrace flags Category 3 cracking to the rear elevation and recommends a structural engineer's report.

Recommended wording:

"Our surveyor has identified significant structural cracking to the rear elevation, rated Condition 3 (urgent action required), and has recommended an independent structural engineer's assessment. We are unable to proceed at the agreed price until this investigation is complete. Subject to the engineer's findings, we reserve the right to renegotiate the purchase price or withdraw from the transaction."

This wording is firm, professional, and protects the buyer's legal position. It also signals to the seller that the buyer is informed and serious — which frequently prompts a more cooperative response.

Research into average price reductions after survey findings suggests that well-evidenced requests regularly achieve reductions of 1–5% of the agreed purchase price, with larger reductions possible where major structural or damp issues are confirmed.

What to Do When Negotiations Stall

Sometimes sellers refuse to negotiate, particularly in competitive markets. In these situations, buyers must weigh:

- The cost of defects versus the value of the property at the agreed price

- The risk of future deterioration if defects are left unaddressed

- Their own financial capacity to fund repairs post-completion

A survey that reveals serious problems is not a failure — it is valuable intelligence. Knowing what to do after a bad building survey report is as important as knowing how to negotiate in the first place.

The Lender's Perspective: Mortgage Retentions and Valuation Adjustments

The journey from survey to settlement: how building surveys shape negotiations between UK buyers, sellers and lenders is not limited to the buyer-seller dynamic. Mortgage lenders are a third, often overlooked party whose decisions can reshape — or derail — a transaction.

How Lenders Use Survey Data

Most buyers commission their own survey separately from the lender's mortgage valuation. However, lenders increasingly request sight of independent survey reports — particularly for older properties or where the mortgage valuation flags concerns.

When a lender's valuer identifies significant defects, they may:

- Reduce the mortgage offer to reflect a lower assessed value

- Impose a retention — withholding a portion of the loan until specified repairs are completed

- Decline to lend on the property entirely

📌 Sample Scenario: Mortgage Retention

A buyer agrees to purchase a 1920s property for £420,000 with a 90% LTV mortgage of £378,000. The lender's valuer identifies roof covering failure and estimates repair costs of £15,000. The lender imposes a retention of £15,000, releasing only £363,000 at completion.

Impact on the buyer:

- Must fund the £15,000 shortfall from savings at completion

- Must arrange and fund roof repairs post-completion

- Must provide evidence of completed repairs before the retention is released

Negotiating implication:

This scenario gives the buyer strong grounds to return to the seller and request a price reduction of at least £15,000 — supported by both the independent survey and the lender's retention letter. The lender's decision, in effect, validates and amplifies the buyer's negotiating position.

Recommended Wording for Lender Retention Situations

"Following our mortgage lender's valuation, a retention of £[amount] has been imposed pending completion of [specified repairs]. We are therefore requesting a corresponding reduction in the purchase price to reflect the immediate financial impact on our mortgage position. We attach the lender's retention notification for your reference."

This approach is transparent, professional, and difficult for sellers to dismiss — because it demonstrates that an independent third party (the lender) has reached the same conclusion as the buyer's surveyor.

Choosing the Right Survey: Matching the Tool to the Property

Not every property requires the same level of investigation. Selecting the appropriate survey type is the first strategic decision in the process.

Quick Decision Guide 🏠

| Property Type | Recommended Survey | Key Reason |

|---|---|---|

| New build | Snagging inspection | Defects are typically minor but numerous |

| Post-2000 conventional property | Level 2 HomeBuyer Report | Standard construction, lower defect risk |

| 1950s–1990s property | Level 2 or Level 3 | Depends on condition and alterations |

| Pre-1919 property | Level 3 Building Survey | High risk of hidden structural and damp issues |

| Non-standard construction | Level 3 Building Survey | Standard assessments insufficient |

| Listed building | Level 3 + specialist advice | Complex legal and conservation obligations |

Even new-build properties are not immune to defects — understanding whether a building survey is needed for a new build can prevent buyers from assuming that "new" means "problem-free."

For buyers seeking a detailed written assessment of a property's visible condition without a full structural investigation, a condition survey report may provide a cost-effective intermediate option.

Common Defects That Drive Negotiations — and How to Cost Them

Understanding which defects carry the most financial weight helps buyers prioritise their negotiating efforts.

High-Impact Defects 🔴

- Subsidence and structural movement — costs range from £5,000 for minor underpinning to £50,000+ for severe cases

- Roof failure — full replacement on an average semi-detached: £8,000–£20,000

- Rising or penetrating damp — treatment and reinstatement: £2,000–£12,000 depending on extent

- Electrical rewiring — full rewire of a 3-bed property: £4,000–£9,000

- Asbestos — survey and removal: £1,500–£10,000+ depending on location and extent

Medium-Impact Defects 🟡

- Failed double glazing units — £500–£3,000

- Chimney stack repointing — £800–£2,500

- Guttering and fascia replacement — £600–£2,000

- Boiler replacement — £2,000–£4,000

💡 Tip: Always obtain two or three independent contractor quotes before presenting a price reduction request. A single quote can be dismissed as unrepresentative; multiple quotes establish a credible market rate.

It is also worth noting that building surveys can generate significant savings that far exceed their upfront cost — particularly on older properties where hidden defects are common.

Protecting the Negotiation: Legal and Practical Considerations

Stay Within the Exchange Window

In England and Wales, buyers are not legally committed until exchange of contracts. This means the entire negotiation process — survey, renegotiation, lender decisions — takes place during a period when either party can withdraw without legal penalty (though not without potential loss of survey fees and legal costs).

This window is the buyer's primary source of leverage. Using it effectively requires:

- Acting quickly once the survey is received

- Communicating through solicitors for formal price reduction requests

- Keeping records of all survey findings, contractor quotes, and correspondence

When to Involve a Chartered Surveyor in Negotiations

For complex defects — particularly structural movement, subsidence, or significant damp — it is worth asking the original surveyor to provide a supplementary letter summarising the key findings in plain language for use in negotiations. Many chartered surveyors will provide this as part of their service or for a modest additional fee.

This letter carries professional authority and can be shared directly with the seller's solicitor, reinforcing the buyer's position without appearing adversarial.

Conclusion: Turning Survey Findings into Settlement Outcomes

The journey from survey to settlement: how building surveys shape negotiations between UK buyers, sellers and lenders is not a passive process — it is an active, strategic exercise that rewards preparation, evidence, and clear communication.

Actionable Next Steps ✅

- Commission the right survey for the property — do not default to the cheapest option on a complex or older building.

- Read the full report carefully — pay particular attention to Condition 3 ratings and any recommendations for specialist investigations.

- Obtain contractor quotes promptly — two to three quotes for all significant defects before approaching the seller.

- Frame requests professionally — use specific, costed, evidence-based language rather than vague discount requests.

- Engage your solicitor — formal price reduction requests should be made in writing through legal channels.

- Understand your lender's position — check whether the mortgage valuation has flagged the same issues and whether a retention is likely.

- Know your exit point — decide in advance at what level of defect cost or seller intransigence you would withdraw from the transaction.

A building survey is not a cost — it is an investment in knowledge. That knowledge, applied strategically, shapes every conversation between buyer, seller, and lender from the moment the report lands until the keys change hands.