New buyer enquiries improved to a net balance of -15% in January 2026 — a meaningful step up from -29% in November 2025 — yet by March 2026, that same metric had collapsed to -39%, the weakest reading since August 2023. [1][3] That whiplash tells a critical story: the early 2026 housing market recovery is real in pockets, fragile in others, and entirely dependent on how prepared buyers, sellers, and their advisors are when conditions shift. For anyone navigating property transactions right now, understanding the Early 2026 Housing Market Recovery: Building Survey Strategies to Capitalise on RICS Survey Momentum is not optional — it is the difference between a deal that completes and one that falls through.

Key Takeaways 📋

- January 2026 showed genuine recovery signals, but March data revealed a sharp reversal driven by mortgage rates climbing back above 5% and geopolitical uncertainty.

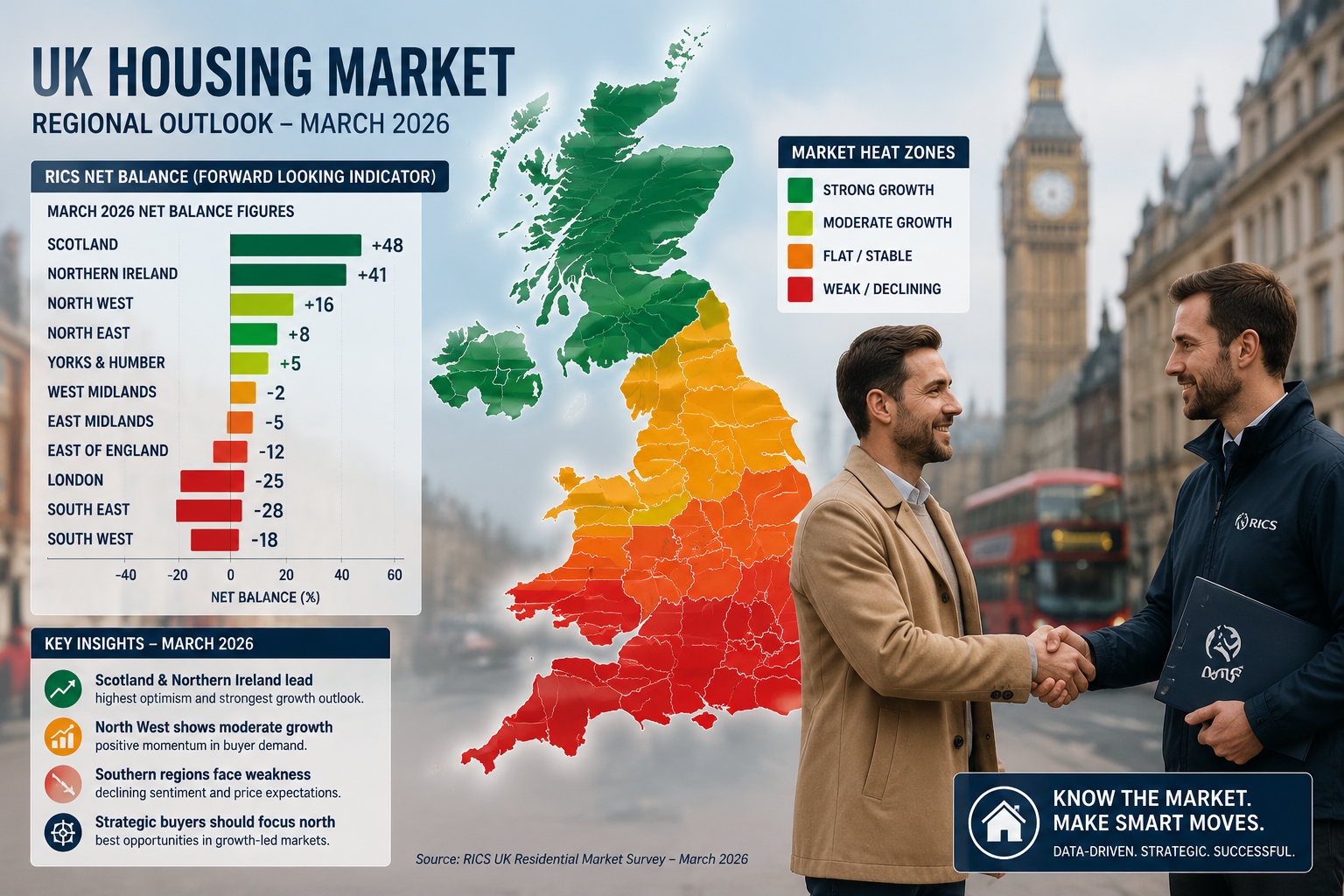

- Regional divergence is significant: Scotland, Northern Ireland, and the North West are outperforming southern England considerably.

- Level 3 Building Surveys are the strategic tool buyers need to overcome caution, negotiate effectively, and protect themselves in a volatile market.

- First-time buyers are identified as the likely recovery catalyst, making entry-level property surveys more commercially important than ever.

- Proactive survey commissioning — especially in regions showing positive RICS momentum — can unlock negotiating leverage and prevent costly post-completion surprises.

Understanding the RICS Data: What Early 2026 Really Looks Like

The RICS UK Residential Market Survey is one of the most closely watched barometers of housing sentiment in the country. Its net balance figures — the percentage of surveyors reporting increases minus those reporting decreases — offer a real-time pulse of market conditions. In early 2026, that pulse has been anything but steady.

January 2026: Cautious Optimism Emerges

January's data offered genuine encouragement. New buyer enquiries improved to -15% net balance, recovering from -21% in December and -29% in November 2025. [1] House price stabilisation was also evident, with the price balance improving to -10% from -19% in October 2025. [1] Perhaps most striking was the twelve-month sales outlook, which hit +35% net balance — the strongest reading since December 2024. [1]

💬 "The best early sign of activity for 2026 is more properties coming to market," noted surveyors commenting on January's data, with new instructions registering a broadly flat but marginally positive +1% net balance. [1][2]

Property supply edging upward, combined with improving buyer sentiment, created conditions where well-prepared buyers had a real window of opportunity. RICS surveys commissioned during this period gave buyers the structural intelligence needed to move decisively.

March 2026: The Reversal That Changes Everything

March 2026 told a starkly different story. New buyer enquiries collapsed to -39% net balance — the worst reading since August 2023. [3] Agreed sales plummeted to -34% net balance, down from -13% in February. [3] The headline price balance fell to -23%, signalling renewed downward pressure on values. [3]

The culprit? Fixed mortgage rates climbing back above 5%, combined with geopolitical uncertainty and energy cost volatility. [3] Christopher Clark FRICS captured the mood bluntly: "It's impossible to know what is happening to the residential market at the moment," pointing to dependency on whether "recent surges in oil and energy costs begin to reverse." [3]

Short-term sales expectations deteriorated to -33% net balance in March, compared to -4% in February — a dramatic reversal that effectively dismantled the recovery narrative built in January. [3]

The Regional Picture: Where Opportunity Still Lives 🗺️

Not all regions are experiencing the same turbulence. RICS data consistently highlights Scotland and Northern Ireland as the strongest performers for price growth in early 2026, with the North West and North of England also showing positive trends. [1] Southern regions and parts of London remain under pressure.

| Region | Early 2026 Price Trend | Survey Strategy Priority |

|---|---|---|

| Scotland | ✅ Strong growth | Level 2 or Level 3 depending on age |

| Northern Ireland | ✅ Strong growth | Level 3 for older stock |

| North West England | 🟡 Positive | Level 3 recommended |

| London & South East | 🔴 Under pressure | Level 3 essential for negotiation |

| East of England | 🔴 Weak | Level 3 for price renegotiation |

For buyers in stronger regions, commissioning a thorough RICS property valuation alongside a structural survey ensures they are not overpaying in a market where values are still being established.

Early 2026 Housing Market Recovery: Building Survey Strategies to Capitalise on RICS Survey Momentum

The volatility in RICS data does not mean buyers should retreat. It means they need better information before committing. This is precisely where Level 3 Building Survey protocols become a strategic asset rather than a procedural formality.

Why Level 3 Surveys Are the Right Tool for This Market

A Level 3 Building Survey — formerly known as a Full Structural Survey — is the most comprehensive inspection available under the RICS framework. It covers the full condition of a property's structure, fabric, and services, with detailed commentary on defects, their causes, and recommended remediation. Understanding the difference between Level 2 and Level 3 surveys is essential before commissioning.

In a market where buyer caution is elevated — as March 2026 data confirms — a Level 3 survey does three things simultaneously:

- Reduces transaction risk by identifying structural defects before exchange

- Creates negotiating leverage by quantifying the cost of remediation

- Builds buyer confidence in a market where hesitation is common

Tim Green FRICS of Green & Co. Oxford identified first-time buyers as the likely recovery catalyst in early 2026, noting the recovery "is likely to be led from the first-time buyer range." [2] First-time buyers, however, are also the most financially exposed group — they cannot absorb post-completion surprises. A Level 3 survey is their primary financial protection.

Key Protocol Elements for a Level 3 Survey in 2026 Market Conditions

Structural integrity assessment remains the foundation. In a market where prices are under downward pressure, any structural compromise — subsidence, roof failure, wall tie corrosion — carries disproportionate financial risk. Understanding subsidence risks and why they matter is particularly important for buyers in areas with clay-heavy soils or older housing stock.

Damp and timber investigations are non-negotiable in 2026's market. With energy costs elevated and many properties having deferred maintenance through the cost-of-living squeeze, rising damp, penetrating damp, and timber decay are more prevalent than in previous cycles. A thorough damp and timber assessment within the Level 3 protocol can reveal hidden costs that reshape a purchase decision entirely.

Services condition reporting — covering heating systems, electrical installations, and drainage — provides buyers with a full picture of immediate capital expenditure requirements.

Roof and chimney inspection is particularly critical for the older housing stock that dominates many of the recovering regions. Period properties in Scotland, Northern Ireland, and the North West frequently present with aging slate roofs, defective flashings, and chimney stack movement.

Using Survey Findings to Negotiate in a Softening Market

One of the most underused applications of a Level 3 survey is price renegotiation. In a market where the RICS headline price balance has fallen to -23% [3], sellers are increasingly motivated to complete transactions. A detailed survey report that quantifies remediation costs gives buyers a factual, professional basis for renegotiating the agreed price.

💡 Pro Tip: A Level 3 survey costing £800–£1,500 can identify defects worth tens of thousands of pounds in remediation — making it one of the highest-return investments in any property transaction.

How an RICS survey can help negotiate property prices is a well-established principle, but it is especially powerful in 2026's conditions where sellers face limited alternatives.

Strategic Survey Commissioning: Timing, Location, and Property Type

The Early 2026 Housing Market Recovery: Building Survey Strategies to Capitalise on RICS Survey Momentum must account for geography, property type, and transaction timing. A one-size-fits-all approach misses the nuances that RICS data consistently highlights.

Timing Your Survey Relative to Market Conditions

The January-to-March 2026 data swing demonstrates that market windows can open and close quickly. Buyers who commissioned surveys in January — when sentiment was improving and competition was lower — were better positioned to complete transactions before March's deterioration set in.

The strategic lesson: commission surveys early in the offer process, not as a final formality. This allows time to:

- Review findings thoroughly

- Obtain remediation quotes if needed

- Renegotiate before the seller finds alternative buyers

- Complete before any further market deterioration

Matching Survey Level to Property Type and Age

Not every property requires a Level 3 survey, though in the current climate, erring toward more comprehensive inspection is advisable. The general framework:

| Property Type | Recommended Survey | Rationale |

|---|---|---|

| Pre-1900 period property | Level 3 (Full Structural) | High defect risk, non-standard construction |

| 1900–1970 property | Level 3 strongly recommended | Asbestos risk, aging services, structural movement |

| 1970–2000 property | Level 2 minimum, Level 3 preferred | Cavity wall insulation issues, flat roof risks |

| Post-2000 new build | Snagging survey or Level 2 | New build surveys address developer defects |

| Converted flat or maisonette | Level 3 | Structural complexity, shared elements |

Geographic Survey Strategy: London and the South

For buyers in London and southern England — where RICS data shows continued weakness — the survey strategy should prioritise defect quantification for negotiation above all else. Markets under price pressure mean sellers are more willing to accept reductions backed by professional survey evidence.

Buyers across London property markets should be particularly attentive to:

- Subsidence in clay-soil areas (common across south London, Croydon, and surrounding boroughs)

- Damp in Victorian and Edwardian terraces

- Structural alterations made without building regulations approval

For those purchasing in specific London boroughs and surrounding areas, local expertise matters. Southwark property surveyors, Croydon property surveyors, and Ealing property surveyors each bring area-specific knowledge of local construction types, planning histories, and common defect patterns.

The Rental Market Dimension

January 2026 RICS data showed tenant demand edging higher, ending two consecutive quarters of flat or negative readings, while rental prices continued rising. [1] For landlords and buy-to-let investors, this signals ongoing rental yield opportunity — but only for properties in lettable condition.

A stock condition survey provides landlords with a baseline assessment of their portfolio's condition, identifying maintenance priorities before regulatory requirements force emergency expenditure. In 2026's environment of rising energy costs and tightening EPC requirements, proactive condition assessment is sound financial management.

Navigating Buyer Caution: Practical Steps for Agents and Advisors

The March 2026 data — with short-term sales expectations at -33% [3] — reflects genuine buyer hesitation. Agents, mortgage brokers, and legal advisors can help clients overcome this caution by positioning the survey as a confidence tool rather than a cost.

Five Actions to Accelerate Transactions in a Cautious Market

- Recommend surveys at offer stage, not post-mortgage offer — this compresses the timeline and reduces fall-through risk

- Brief clients on RICS survey levels before they instruct solicitors — informed buyers make faster decisions

- Use survey findings proactively — share relevant defect information with sellers early to enable price adjustment before exchange

- Target surveys in positive-momentum regions — Scotland, Northern Ireland, and North West buyers face less price resistance

- Integrate survey findings with mortgage applications — lenders increasingly value comprehensive survey data for valuation accuracy

The First-Time Buyer Opportunity

With first-time buyers identified as the likely recovery catalyst [2], the advisory community has a responsibility to ensure this group is properly protected. Many first-time buyers default to the cheapest survey option — often a mortgage valuation alone — which provides no structural protection whatsoever.

A clear explanation of what a homebuyers report versus a structural survey actually covers can be the difference between a buyer who completes with confidence and one who discovers a £20,000 damp problem six months after moving in.

Conclusion: Turning Market Volatility Into Strategic Advantage

The early 2026 housing market recovery is not a straight line — the RICS data makes that abundantly clear. January's optimism, March's reversal, and the persistent regional divergence all point to a market that rewards preparation and punishes complacency.

The Early 2026 Housing Market Recovery: Building Survey Strategies to Capitalise on RICS Survey Momentum comes down to a simple principle: in uncertain markets, information is the most valuable asset a buyer can hold. A Level 3 Building Survey provides that information in a professionally structured, legally defensible format that protects buyers, enables negotiation, and accelerates completions.

Actionable Next Steps ✅

- Commission a Level 3 Building Survey at offer stage — not as an afterthought

- Match survey type to property age and type using the framework above

- Use survey findings to renegotiate in a market where sellers face limited alternatives

- Focus on positive-momentum regions (Scotland, Northern Ireland, North West) for investment decisions

- Ensure first-time buyers understand survey options before they default to a mortgage valuation

- Seek local expertise — surveyors with area-specific knowledge identify defects that generalists miss

The market will continue to fluctuate. The buyers who complete successfully in 2026 will be those who treated due diligence as a strategic investment, not a procedural box to tick.

References

[1] UK Resi Survey Jan 2026 Report Shows Early Signs Market Recovery Despite Caution – https://www.rics.org/news-insights/uk-resi-survey-jan-2026-report-shows-early-signs-market-recovery-despite-caution

[2] Latest RICS Survey Reveals Global Headwinds Are Weighing On Housing Market Confidence – https://www.buyassociationgroup.com/en-gb/news/latest-rics-survey-reveals-global-headwinds-are-weighing-on-housing-market-confidence/

[3] Housing Market Loses Momentum As Borrowing Costs Rise RICS Survey Shows – https://theintermediary.co.uk/2026/04/housing-market-loses-momentum-as-borrowing-costs-rise-rics-survey-shows/

[4] UK Residential Market Survey January 2026 – https://www.rics.org/content/dam/ricsglobal/documents/market-surveys/uk-residential-market-survey/UK-Residential-Market-Survey_January-2026.pdf

[6] RICS Hails Early Signs of Housing Market Improvement in Latest Survey – https://www.housingtoday.co.uk/news/rics-hails-early-signs-of-housing-market-improvement-in-latest-survey/5140683.article