The March 2026 RICS Residential Market Survey recorded a house price net balance of -15% — one of the weakest professional sentiment readings in recent quarters. For investors holding or acquiring high-value residential portfolios, that single data point signals something critical: the gap between what a spreadsheet says a portfolio is worth and what a qualified surveyor will actually sign off on has never been wider. [3]

Understanding Surveyor Valuation Frameworks for £1m+ Residential Portfolios: Yield vs Comparable Evidence in 2026 Markets is no longer optional for serious investors. It is the difference between a deal that gets funded and one that collapses at the lender's desk. This article unpacks both primary methodologies, explains how surveyors weigh them against each other, and provides a practical pre-underwriting checklist to stress-test any acquisition before heads of terms are signed.

Key Takeaways 📌

- Surveyors use two core methodologies: comparable evidence (recent achieved sales) and yield basis (market rent ÷ risk-adjusted yield). Most blend both.

- Evidence beats aspiration: surveyors prioritise actual transaction data over investor projections and asking prices.

- Weak rent evidence, unexplained voids, poor EPC ratings, and location concentration are the top valuation red flags in 2026.

- The March 2026 RICS net balance of -15% means professional sentiment is cautious — conservative pre-underwriting is essential.

- Real-time surveyor judgment now outperforms automated valuation models (AVMs) in volatile market conditions.

How Surveyors Really Value £1m+ Residential Portfolios in 2026

The Two Pillars: Comparable Evidence and Yield Basis

At the heart of Surveyor Valuation Frameworks for £1m+ Residential Portfolios: Yield vs Comparable Evidence in 2026 Markets sit two distinct but complementary approaches. Neither operates in isolation for experienced practitioners. [1]

1. Comparable Evidence (Sales Comparison Approach)

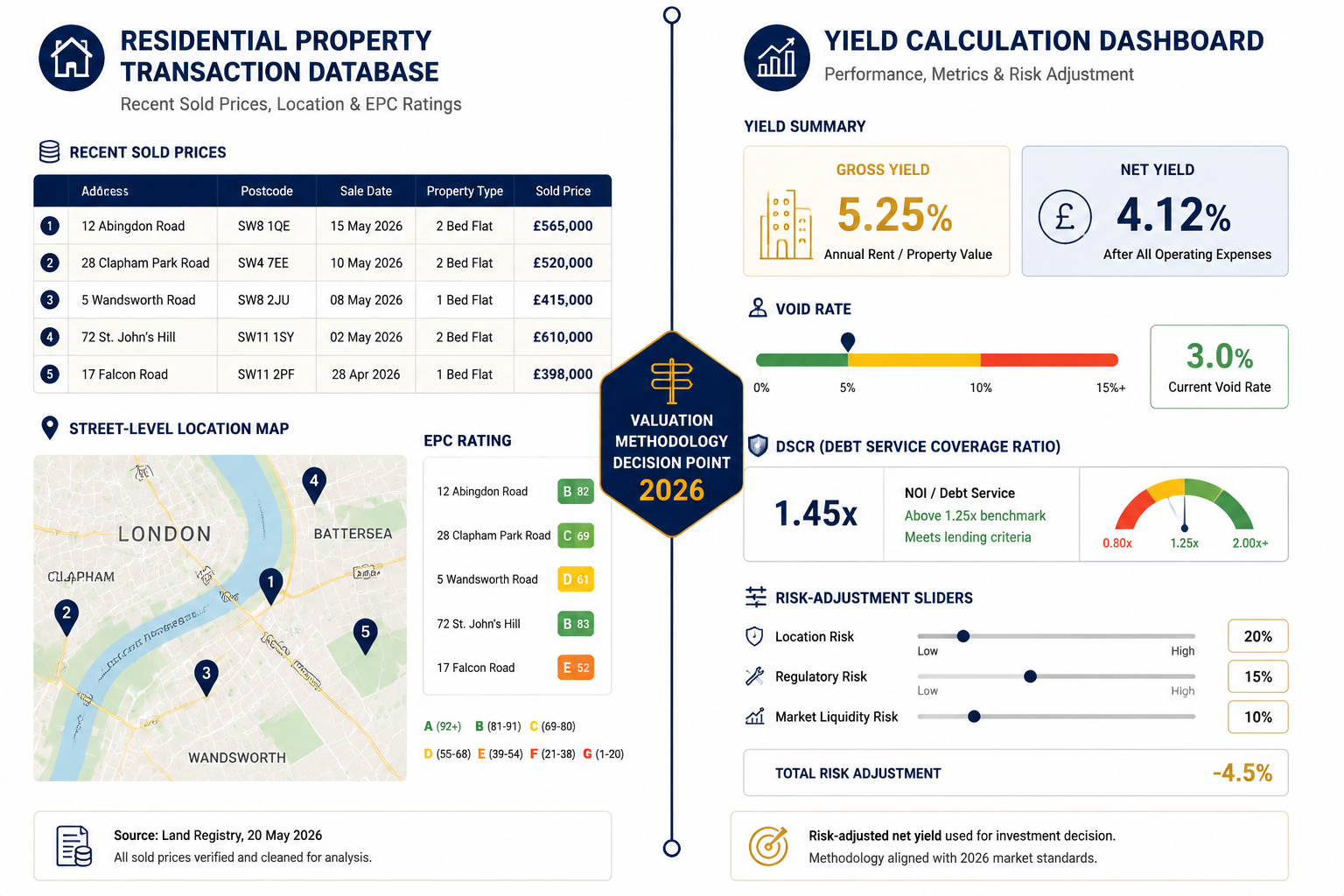

This method anchors value to what similar properties in comparable locations have actually sold for — not what they were listed at, not what the investor's model assumes, and certainly not what an automated algorithm suggests.

Key inputs include:

- ✅ Achieved sale prices from recent transactions (typically within 6–12 months)

- ✅ Location quality — street-by-street, not just postcode-level

- ✅ Property condition relative to local stock

- ✅ Size, configuration, and tenure adjustments

- ✅ EPC ratings and their impact on buyer/lender appetite

💬 "Surveyors value evidence-based transaction data rather than investor spreadsheets and aspirational projections." [1]

The comparable approach is most reliable where transaction volume is healthy and properties are genuinely similar. In thinly traded prime markets or unusual asset types, it becomes harder to apply with confidence.

2. Yield Basis (Income Capitalisation Approach)

The yield method calculates value by dividing the market-achievable annual rent by an appropriate yield rate (expressed as a percentage). The yield rate is risk-adjusted to reflect:

- Local rental market depth

- Void risk and historical occupancy

- Tenant quality and covenant strength

- Maintenance liability and building condition

- Macro market sentiment (critically relevant given the -15% RICS balance) [3]

| Component | What Surveyors Examine |

|---|---|

| Gross Rent | Achieved rents, not asking rents |

| Void Allowance | Historical voids + market norm |

| Management Costs | Realistic, not optimistic |

| Net Rent | Gross minus voids and costs |

| Applied Yield | Risk-adjusted for location and condition |

| Resulting Value | Net Rent ÷ Yield |

Why Most Surveyors Blend Both Methods

For portfolios above £1m, relying on a single methodology introduces unnecessary valuation risk. A property with strong comparable evidence but poor rental fundamentals (high voids, below-market rents) will be overvalued if comparables alone are used. Conversely, a property with excellent rental income in a thin transaction market needs comparable cross-referencing to validate the yield assumption. [1]

The blended approach is particularly important when reviewing an RICS building survey alongside a valuation — structural condition findings directly affect both achievable rent and comparable adjustments.

The 2026 Market Context: Why Valuation Confidence Is Under Pressure

RICS Data vs Automated Valuation Models

The Spring 2026 market has presented a specific challenge: automated valuation models (AVMs) are lagging real conditions. AVMs rely on historical transaction data and algorithmic pattern-matching. In a market where sentiment is shifting rapidly — as evidenced by the -15% RICS net balance — they systematically overestimate values by anchoring to older, more buoyant transaction data. [3]

Real-time RICS surveyor data and professional judgment have demonstrably outperformed AVMs in these conditions. This is not a minor technical distinction. For a lender instructing a valuation on a £2m portfolio, an AVM that reads £2.1m while a qualified surveyor returns £1.75m creates a funding gap that can kill a transaction. [3]

Macro Signals Shaping Surveyor Risk Appetite in 2026

Several structural forces are reshaping how surveyors calibrate risk in 2026 valuations:

- 📉 Muted supply pipelines: Moderating construction activity is helping stabilise values in some sub-markets [5]

- 💰 Selective capital re-entry: Institutional money is returning, but with tighter criteria — prioritising cash-flow growth over cap rate compression [4]

- 🌱 ESG as a valuation variable: Properties with strong energy efficiency credentials and sustainability performance are attracting measurable premiums. Low EPC ratings (particularly below Band C) now represent a direct valuation discount and capital expenditure liability [2]

- 🤖 Data analytics integration: AI-driven market signals are increasingly supporting — not replacing — surveyor judgment on occupancy trends and demographic shifts [2]

For investors considering lease extension valuation as part of portfolio optimisation, these macro signals directly affect the premium calculations surveyors apply.

Primary Valuation Red Flags: What Surveyors Look For in £1m+ Portfolios

The Five Factors That Depress Portfolio Valuations

Surveyors operating within Surveyor Valuation Frameworks for £1m+ Residential Portfolios: Yield vs Comparable Evidence in 2026 Markets consistently identify the same cluster of issues that push valuations below investor expectations. Understanding these is essential preparation before any professional instruction. [1]

🚩 1. Weak or Unverifiable Rent Evidence

If rents cannot be supported by independent market evidence — comparable lettings in the same street or building — surveyors will apply a discount or revert to a lower market rent figure. Aspirational rents in the investor's model carry zero weight.

🚩 2. Unexplained Voids and Arrears

A portfolio showing 15% void rates without clear explanation signals either demand weakness, management failure, or both. Surveyors will stress-test the income stream against realistic void assumptions, often more conservative than the investor's projections.

🚩 3. Poor Condition Relative to Local Comparables

Condition is a direct input into both methodologies. A property in below-average condition compared to recent sales comparables receives a downward adjustment. In yield terms, poor condition increases the risk premium applied, reducing the resulting capital value. Understanding what to check before buying a leasehold property is especially relevant here, as hidden service charge liabilities and major works obligations directly affect net income.

🚩 4. High Concentration in Weaker Streets or Blocks

Portfolio concentration risk is a specific concern at the £1m+ level. A portfolio of ten units in a single block carries different risk characteristics than ten units spread across a borough. Surveyors apply location-specific adjustments that can significantly alter per-unit values.

🚩 5. Low EPC Ratings and Looming CapEx

With regulatory pressure on energy performance intensifying, properties rated below Band C face both reduced tenant demand and potential lender restrictions. Surveyors now explicitly factor in the capital expenditure required to meet future EPC thresholds as a deduction from value. [1]

What Surveyors Will Not Accept as Evidence

| ❌ Not Acceptable | ✅ What Works Instead |

|---|---|

| Investor's own spreadsheet projections | Achieved rents from letting agent statements |

| Asking prices from Rightmove/Zoopla | Completed sale prices (Land Registry data) |

| AVM outputs | RICS-qualified comparable evidence |

| "Comparable" properties in different postcodes | Same street/building transactions within 12 months |

| Optimistic void assumptions | Market-norm void rates for the specific sub-market |

For investors preparing documentation ahead of a professional instruction, reviewing what to do before an RICS home survey provides practical guidance on presenting a property in its best evidential light.

Pre-Underwriting Checklist: Stress-Testing Deals Before Heads of Terms

The Conservative Pre-Underwriting Principle

The most important insight from experienced practitioners is deceptively simple: a deal must work at mid-range surveyor valuations, not just at the optimistic top-end scenario. If positive returns only materialise at maximum valuation assumptions, the investor is banking on perfection — a position that rarely survives first contact with a lender's valuation panel. [1]

This principle directly informs the following pre-underwriting framework.

📋 Pre-Underwriting Checklist for £1m+ Residential Portfolios

Comparable Evidence Checks

- Pull Land Registry achieved prices for the same street/building within the last 12 months

- Identify at least 3 genuine comparables (adjust for size, condition, floor level, tenure)

- Confirm comparables are arm's-length transactions (not distressed sales or related-party deals)

- Apply a 5–10% downward adjustment to test sensitivity — does the deal still work?

- Check whether the subject property's condition matches or lags comparables

Yield and Income Checks

- Obtain independent rental valuations from two local letting agents (not the vendor's agent)

- Calculate gross yield, then stress-test with a realistic void rate (typically 8–12% for residential)

- Deduct management fees, maintenance reserves, and insurance to arrive at net yield

- Apply a yield rate 50–75 basis points above current market consensus to test downside

- Verify DSCR (Debt Service Coverage Ratio) at stress-tested net income — minimum 1.25x is a common lender threshold [6]

Condition and Compliance Checks

- Commission an RICS building survey before finalising acquisition terms

- Obtain EPC ratings for all units — flag anything below Band C and cost remediation

- Check for structural issues: subsidence indicators, damp, or timber problems

- Review service charge history and major works schedule (leasehold portfolios)

- Confirm planning compliance for any HMO or conversion elements

Portfolio-Level Checks

- Map concentration risk — what percentage of units are in a single block or street?

- Review void history for the past 24 months across the portfolio

- Identify any units with arrears and assess recoverability

- Confirm ESG/EPC upgrade costs as a portfolio-wide CapEx line item [2]

- Model returns at three valuation scenarios: optimistic, mid-range, and conservative

💡 Rule of thumb: If the conservative scenario produces an unacceptable return, the deal needs renegotiation — not better assumptions.

For investors active in specific London sub-markets, local expertise matters enormously. Richmond property surveyors and Ealing property surveyors bring granular street-level comparable knowledge that generic valuation tools simply cannot replicate.

Technology, ESG, and the Evolving Surveyor Toolkit in 2026

Data Analytics as a Valuation Support Tool

The integration of AI-driven market signals into professional valuation practice is accelerating. Surveyors are increasingly using data analytics to:

- Predict occupancy and rent trend trajectories at sub-market level

- Analyse demographic and consumer behaviour shifts affecting demand

- Cross-reference comparable databases with greater speed and granularity [2]

Critically, this technology supports rather than replaces professional judgment. The Spring 2026 market has reinforced that human expertise — particularly in reading market sentiment, assessing condition, and applying contextual judgment — remains irreplaceable. [3]

ESG: From Nice-to-Have to Valuation Variable

Morgan Stanley's 2026 real estate strategy explicitly prioritises cash-flow growth over cap rate compression, with selective focus on sectors demonstrating clear demand-supply imbalances. [4] For residential portfolios, this translates directly: properties with strong ESG credentials command higher tenant demand, lower void rates, and — increasingly — explicit investor premiums.

Surveyors now treat ESG performance as predictive of long-term financial resilience. A portfolio with strong EPC ratings, low carbon footprint, and good tenant welfare outcomes is a materially different risk profile from an equivalent portfolio with poor energy performance — and valuations are beginning to reflect this distinction explicitly. [2]

DSCR Refinancing and Portfolio Scaling

For investors looking to scale beyond the initial £1m+ threshold, DSCR cash-out refinancing remains a primary mechanism for extracting equity from appreciated assets and redeploying capital. [6] The surveyor's valuation directly determines the refinanceable equity — making the accuracy of the initial valuation framework critical not just for acquisition but for the entire portfolio growth strategy.

Conclusion: Actionable Next Steps for £1m+ Portfolio Investors

The Surveyor Valuation Frameworks for £1m+ Residential Portfolios: Yield vs Comparable Evidence in 2026 Markets landscape is more nuanced than ever. The -15% RICS net balance, the demonstrated superiority of professional judgment over AVMs, and the growing materiality of ESG factors all point in the same direction: evidence-based, conservative pre-underwriting is the only defensible approach in 2026. [3]

Immediate Action Steps ✅

- Run the pre-underwriting checklist on any live deal before progressing to heads of terms — test at mid-range, not optimistic, valuation assumptions

- Commission independent rental valuations from two local agents before relying on any income figures

- Instruct a qualified RICS surveyor early — not as a box-ticking exercise but as a genuine risk-assessment tool

- Audit EPC ratings across the portfolio and cost remediation as a CapEx line item in all financial models

- Map concentration risk at street and block level — diversification within a portfolio matters as much as diversification across one

- Engage local specialists who carry genuine street-level comparable knowledge for the specific sub-markets in the portfolio

The investors who navigate 2026's challenging conditions successfully will be those who treat surveyor valuation frameworks as a tool for deal discipline — not an obstacle to overcome. Hard evidence, conservative assumptions, and professional expertise are the foundations of durable portfolio performance.

References

[1] Watch – https://www.youtube.com/watch?v=rq408XyXbUI

[2] New Investment Models Reshaping Property Portfolios – https://bfpminc.com/new-investment-models-reshaping-property-portfolios/

[3] Navigating Uncertainty In Spring 2026 Valuations How Rics Real Time Surveyor Data Outperforms Automated Valuation Models – https://nottinghillsurveyors.com/blog/navigating-uncertainty-in-spring-2026-valuations-how-rics-real-time-surveyor-data-outperforms-automated-valuation-models

[4] Real Estate 2026 Outlook – https://www.morganstanley.com/im/en-la/intermediary-investor/insights/outlooks/real-estate-2026-outlook.html

[5] 2026 Valuation Advisory North American Market Survey – https://www.nmrk.com/insights/market-report/2026-valuation-advisory-north-american-market-survey

[6] How To Scale Real Estate Portfolio – https://newfi.com/how-to-scale-real-estate-portfolio/