Buyer enquiries collapsed to a net balance of -26% in February 2026 — the sharpest single-month deterioration recorded since early 2023 — catching many surveyors and property professionals off guard after a tentatively optimistic start to the year. This dramatic reversal sits at the heart of why Valuation Adjustments Post-RICS February 2026 Survey: Strategies for Cautious Buyer Demand and Regional Price Shifts has become the defining challenge for property professionals across England, Scotland, Wales, and Northern Ireland right now. The RICS UK Residential Survey for February 2026 paints a complex picture: short-term sentiment is deteriorating sharply, yet 12-month price expectations remain positive at +33% [1]. Navigating that tension requires precise, regionally calibrated valuation strategies.

Key Takeaways 📌

- Buyer enquiries dropped to -26% net balance in February 2026, a sharp fall from -15% in January, driven partly by geopolitical uncertainty [1].

- Short-term price expectations turned deeply negative at -18%, while 12-month expectations remain positive at +33%, creating a dual-horizon valuation challenge [1].

- London faces the steepest pressure at -40% net balance, with 12-month confidence collapsing from +56% to just +7% [1].

- Northern Ireland, Scotland, and the North West remain resilient, offering surveyors more stable valuation baselines [1].

- Surveyors must apply region-specific adjustment strategies rather than relying on national averages, which mask significant local divergence.

Understanding the RICS February 2026 Data: What the Numbers Actually Mean

The February 2026 RICS UK Residential Survey delivered a sobering set of figures that demand careful interpretation rather than panic. The headline house price net balance registered at -12%, meaning more surveyors reported falling prices than rising ones at the national level [1]. However, this national figure conceals enormous regional variation that directly shapes how valuation adjustments should be applied.

The Buyer Demand Collapse Explained

The drop in buyer enquiries from -15% in January to -26% in February is not simply a seasonal blip [1]. RICS-contributing surveyors specifically cited the Iran conflict and associated geopolitical tensions as a direct driver of declining confidence [1]. Capital Economics noted that Middle East tensions and oil price spikes increased the likelihood of higher mortgage rates persisting for longer, directly dampening the cautious optimism seen at the start of 2026 [4].

This matters enormously for valuations because buyer demand is a leading indicator. When fewer buyers are actively enquiring, agreed sales follow downward — and indeed, agreed sales sat at -12% net balance in February [1]. Near-term sales expectations softened to -2%, though the 12-month forward view remained positive at +17% [1].

💬 "The February data is a reminder that property valuations are not just about bricks and mortar — they are deeply sensitive to macro-economic confidence."

Short-Term vs. Long-Term: The Dual-Horizon Problem

Perhaps the most challenging aspect of Valuation Adjustments Post-RICS February 2026 Survey: Strategies for Cautious Buyer Demand and Regional Price Shifts is the stark divergence between short and long-term signals:

| Metric | January 2026 | February 2026 |

|---|---|---|

| Buyer Enquiries (net balance) | -15% | -26% |

| Agreed Sales (net balance) | — | -12% |

| Short-term Price Expectations | -6% | -18% |

| 12-Month Price Expectations | +43% | +33% |

| Near-term Sales Expectations | — | -2% |

| 12-Month Sales Expectations | — | +17% |

Source: RICS UK Residential Survey February 2026 [1]

This dual-horizon tension — near-term caution versus medium-term optimism — is precisely why surveyors cannot apply a single blanket adjustment. A property valued today for a buyer completing in three months requires different treatment than one being assessed for a long-term investment decision.

For buyers who have recently had an offer accepted, understanding how to negotiate the purchase price after a building survey becomes especially relevant in this environment, where downward pressure creates legitimate grounds for renegotiation.

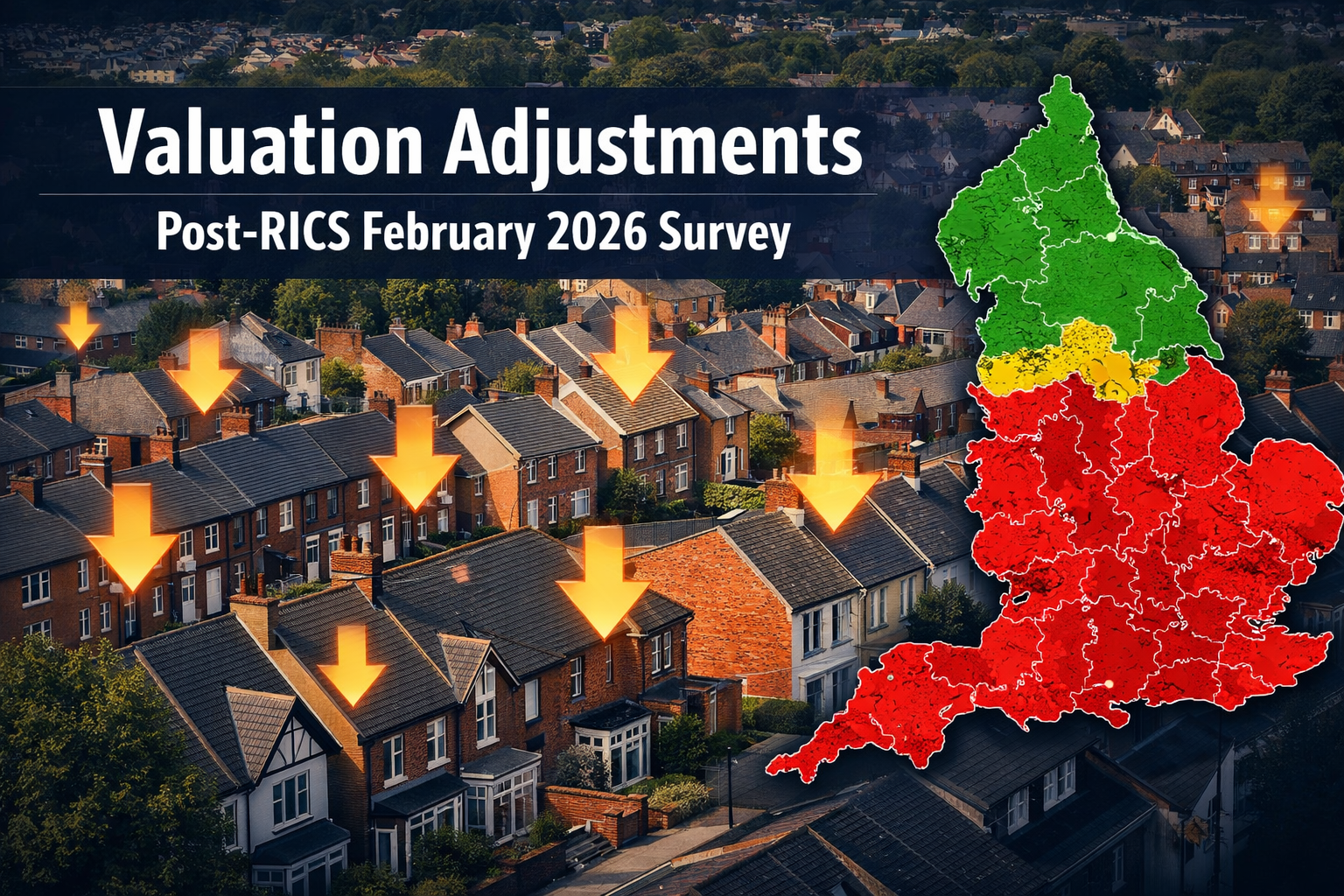

Regional Price Shifts: Where Valuations Face the Greatest Pressure

The national -12% headline figure is, frankly, misleading if used as a valuation benchmark. The February 2026 data reveals a deeply fragmented regional picture that demands location-specific adjustment strategies [1].

Southern England: The Epicentre of Downward Pressure

London recorded a net balance of -40% for current price trends — by far the worst-performing region in the February survey [1]. Even more striking is the collapse in 12-month confidence: London's forward price expectations fell from +56% in January to just +7% in February [1]. This is not a minor correction; it represents a fundamental reassessment of near-term London property values.

The South East and East Anglia are also under significant pressure, registering -24% and -26% net balance respectively [1]. For surveyors working across these regions, this data signals that valuations must be approached conservatively, with explicit acknowledgement of current market conditions in any report.

For property professionals covering specific London areas, local market knowledge is essential. Those working across Croydon, Bromley, Islington, and Fulham will recognise that these borough-level variations can diverge even from the wider London trend.

Northern Resilience: A Different Valuation Baseline

In sharp contrast, Northern Ireland, Scotland, and the North West of England continue to report firmer price trends [1]. These regions offer surveyors a more stable foundation for valuation work, with less need for sharp downward adjustment. This resilience likely reflects a combination of factors: lower absolute price levels, stronger affordability ratios, and less direct exposure to the financial sector confidence that drives London demand.

Supply Side: Limited Relief from New Instructions

New property instructions remained broadly stable at just +2% net balance in February [1], meaning fresh listings are neither surging nor collapsing. This limited supply response provides little relief for buyers navigating valuation decisions in a falling-demand environment. Meanwhile, landlord instructions remain firmly negative at -27% [1], pointing to an ongoing contraction in rental stock that continues to affect the broader property market dynamics.

Regional Valuation Adjustment Framework

When applying Valuation Adjustments Post-RICS February 2026 Survey: Strategies for Cautious Buyer Demand and Regional Price Shifts, surveyors should consider this tiered regional approach:

🔴 High Adjustment Zones (Significant Downward Pressure)

- London (-40% net balance)

- East Anglia (-26%)

- South East (-24%)

🟡 Moderate Adjustment Zones

- East Midlands, West Midlands, South West

- Apply modest downward adjustments aligned with national trend

🟢 Stable Zones (Minimal Adjustment Required)

- Northern Ireland

- Scotland

- North West England

Practical Valuation Strategies for Surveyors in a Cautious Market

Given the complexity of the February 2026 data, surveyors need a structured, evidence-based approach to valuation adjustments. The following strategies are designed to help professionals navigate both the short-term caution and the longer-term optimism embedded in the current data.

Strategy 1: Apply the Dual-Horizon Valuation Method

Rather than producing a single point valuation, surveyors should consider presenting a range with explicit time-horizon commentary. Given that short-term price expectations sit at -18% while 12-month expectations remain at +33% [1], a valuation report that acknowledges this divergence is both more accurate and more useful to clients.

This approach involves:

- A current market value reflecting the -18% short-term sentiment

- A 12-month indicative range reflecting the +33% forward expectation

- Clear caveats linking both figures to prevailing market conditions

Choosing the right survey level is also part of this strategy — a Level 3 Building Survey provides the detailed condition data needed to justify any downward valuation adjustment with concrete evidence.

Strategy 2: Weight Comparable Evidence More Heavily Toward Recent Transactions

In a fast-moving market, comparable sales evidence from six or twelve months ago may significantly overstate current values. Surveyors should:

- Prioritise comparables from the past 8-12 weeks wherever available

- Apply explicit time adjustments to older comparables

- Document the rationale for any time-adjustment in the valuation report

- Note the -26% buyer enquiry decline as a market condition factor [1]

Strategy 3: Distinguish Between Property Types and Buyer Profiles

Not all properties are equally affected by cautious buyer demand. In a market where enquiries are falling, first-time buyer properties and mid-market family homes tend to be more sensitive to mortgage rate concerns than prime or cash-buyer markets.

Surveyors should assess:

- The likely buyer profile for the subject property

- Whether the property is in a zone of high or low regional pressure

- Whether the property has features (energy efficiency, condition, location) that may insulate it from broader market weakness

For buyers considering whether to proceed after a survey reveals issues, understanding whether you can renegotiate after a poor building survey result is a critical piece of the puzzle in this environment.

Strategy 4: Transparent Market Commentary in Reports

The RICS Red Book requires valuers to comment on market conditions where they are unusual or volatile. February 2026 clearly meets that threshold. Surveyors should include explicit commentary noting:

- The -26% buyer enquiry decline and its geopolitical drivers [1]

- The regional context of the subject property

- The divergence between short-term and 12-month expectations

- The caveat that valuations reflect conditions at the date of inspection

This transparency protects both the surveyor and the client, and aligns with why working with RICS-accredited surveyors provides meaningful professional protection in volatile markets.

Strategy 5: Reassess Regularly in High-Pressure Regions

For London, South East, and East Anglia properties, the speed of the February deterioration — London's 12-month expectations fell from +56% to +7% in a single month [1] — means that valuations can become stale quickly. Surveyors should:

- Flag the three-month validity window explicitly in reports

- Recommend clients seek updated valuations if the market shifts materially before exchange

- Monitor RICS monthly data releases as a benchmark for reassessment triggers

Addressing Structural Property Issues in a Falling Market

In a cautious buyer demand environment, structural issues carry greater weight in valuations. Buyers are less willing to accept risk when market conditions are uncertain. Issues such as subsidence or wall cracking — which might have been overlooked in a hot market — now become meaningful valuation factors that require explicit adjustment.

A comprehensive homebuyers report that clearly identifies condition issues gives both buyers and sellers the evidence base needed to negotiate fairly in a market where downward pressure is already significant.

The Bigger Picture: What February 2026 Means for the Rest of the Year

The February 2026 RICS data should not be read as a market collapse. The positive 12-month price expectations of +33% [1] — while moderated from +43% in January — suggest that the property market fundamentals remain intact. The current weakness is sentiment-driven rather than structural, rooted in geopolitical uncertainty and mortgage rate concerns rather than a fundamental oversupply or demand destruction.

For surveyors, this means the current period calls for calibrated caution rather than pessimism. The strategies outlined above are designed to reflect current reality accurately while avoiding the trap of extrapolating short-term sentiment into long-term valuation damage.

The key professional discipline is to separate what the data says today from what it might say in twelve months — and to communicate that distinction clearly to clients who may be making long-term financial decisions based on short-term market noise.

Conclusion: Actionable Next Steps for Property Professionals in 2026

The February 2026 RICS survey data has created a genuinely complex valuation environment. Valuation Adjustments Post-RICS February 2026 Survey: Strategies for Cautious Buyer Demand and Regional Price Shifts requires professionals to move beyond national averages and apply precise, regionally calibrated, time-horizon-aware methodologies.

✅ Immediate Action Steps

- Review all outstanding valuations in London, South East, and East Anglia against the -40%, -24%, and -26% regional net balance data [1] and consider whether adjustments are warranted.

- Update market commentary sections in standard valuation reports to reference February 2026 conditions, geopolitical drivers, and the short-term versus 12-month expectation divergence.

- Prioritise recent comparable evidence (within 8-12 weeks) and apply documented time adjustments to older comparables.

- Communicate clearly with clients about the dual-horizon nature of the current market — near-term caution does not negate medium-term value.

- Monitor the March 2026 RICS release to assess whether the February deterioration represents a sustained trend or a single-month shock.

- In stable northern regions, maintain current valuation baselines while noting the national context as a caveat.

The property market in 2026 rewards professionals who read the data carefully, adjust with precision, and communicate with transparency. The February survey is not a reason to abandon confidence — it is a reason to sharpen it.

References

[1] UK Residential Survey February 2026 – https://www.rics.org/news-insights/uk-residential-survey-february-2026

[2] Valuation Adjustments Post RICS February 2026 Residential Survey Strategies For Flat Prices And Stable Lettings Demand – https://nottinghillsurveyors.com/blog/valuation-adjustments-post-rics-february-2026-residential-survey-strategies-for-flat-prices-and-stable-lettings-demand

[3] Valuation Challenges In Weak Buyer Demand RICS February 2026 Survey Analysis And Surveyor Strategies – https://nottinghillsurveyors.com/blog/valuation-challenges-in-weak-buyer-demand-rics-february-2026-survey-analysis-and-surveyor-strategies

[4] UK RICS Residential Market Survey Feb 2026 – https://www.capitaleconomics.com/publications/uk-housing-market-update/uk-rics-residential-market-survey-feb-2026

[5] UK Residential Market Survey February 2026 (PDF) – https://www.rics.org/content/dam/ricsglobal/documents/market-surveys/uk-residential-market-survey/UK-Residential-Market-Survey_February-2026.pdf