The £2 million threshold has become more than just a number in Britain's property market—it's a fiscal dividing line that fundamentally reshapes how luxury properties are valued, marketed, and transacted. As Valuation Adjustments for Tax-Driven High-Value Property Transactions: Surveyor Tactics for Properties Over £2 Million in 2026 become increasingly sophisticated, chartered surveyors find themselves navigating a complex landscape where tax implications can dramatically influence property valuations and buyer behavior.

In 2026, the convergence of multiple tax burdens—including enhanced Stamp Duty Land Tax (SDLT) rates, Capital Gains Tax considerations, and the Annual Tax on Enveloped Dwellings (ATED)—has created unprecedented valuation challenges for properties exceeding the £2 million mark. Professional surveyors working in prime markets across Westminster, Knightsbridge, and Camden must now incorporate tax-driven adjustments into their methodologies to provide accurate, defensible valuations that reflect real-world market conditions.

Key Takeaways

- Tax thresholds significantly impact valuations: Properties valued just above £2 million face substantially higher tax burdens that directly affect market demand and pricing strategies

- Surveyors must document tax-related adjustments: Professional valuation reports now require explicit consideration of tax implications and their influence on comparable sales data

- Strategic timing matters: Market conditions in 2026 show increased sensitivity to tax-driven pricing, with buyers seeking properties priced strategically relative to key thresholds

- Specialized expertise is essential: High-value property valuations require surveyors with specific knowledge of tax legislation, prime market dynamics, and sophisticated adjustment methodologies

- Communication with clients is critical: High-net-worth individuals need clear explanations of how tax considerations influence property values and transaction strategies

Understanding the Tax Landscape for High-Value Properties in 2026

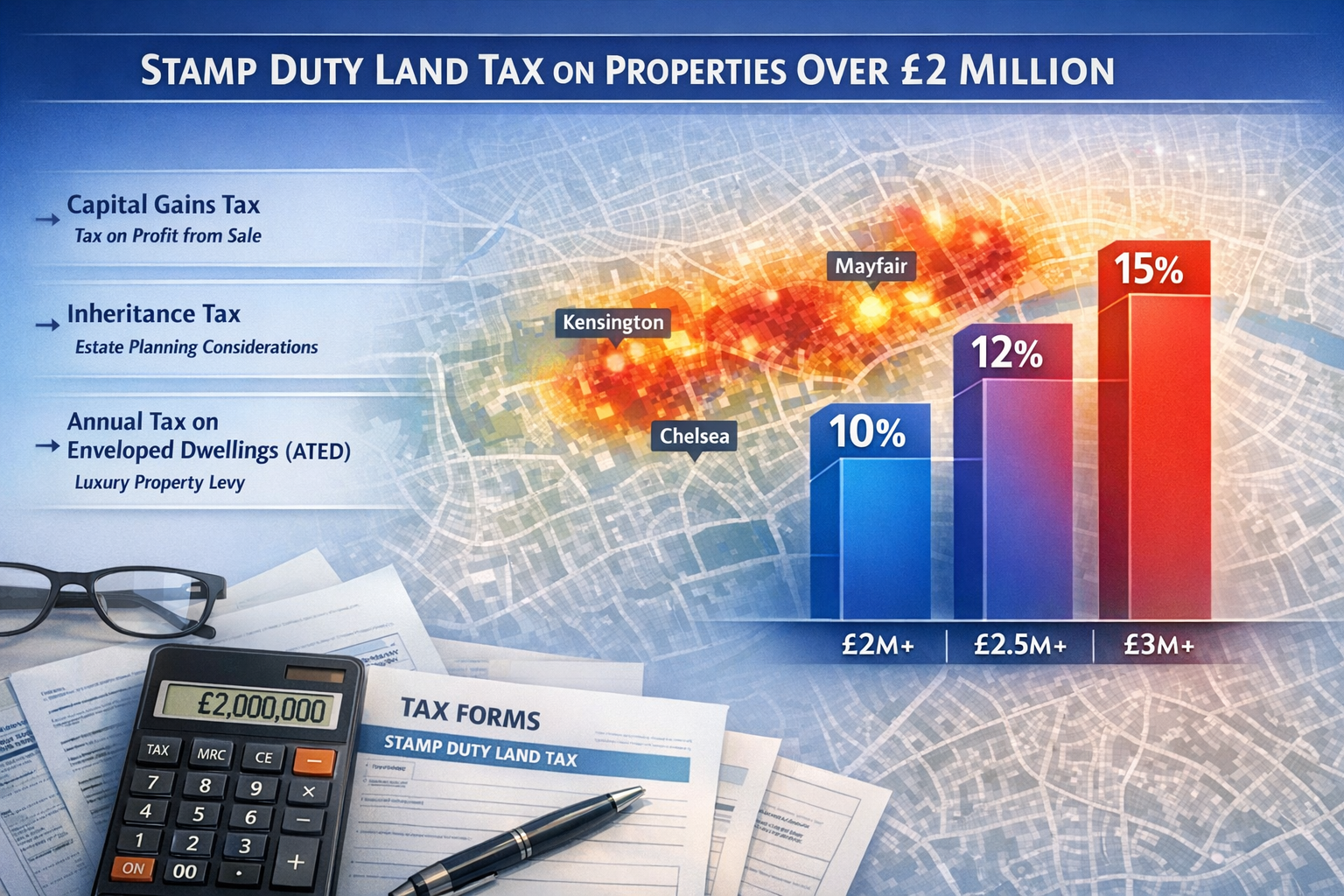

The fiscal environment surrounding properties over £2 million has become increasingly complex, creating what industry professionals describe as a "tax trap" for unwary buyers and sellers. The most significant burden comes from Stamp Duty Land Tax, which escalates dramatically at the £2 million threshold.

Current Tax Structure Affecting £2M+ Properties

For properties exceeding £2 million, buyers face a tiered SDLT structure that includes:

| Property Value Portion | SDLT Rate |

|---|---|

| Up to £250,000 | 0% |

| £250,001 to £925,000 | 5% |

| £925,001 to £1.5 million | 10% |

| £1.5 million to £2 million | 12% |

| Above £2 million | 15% (on portion above) |

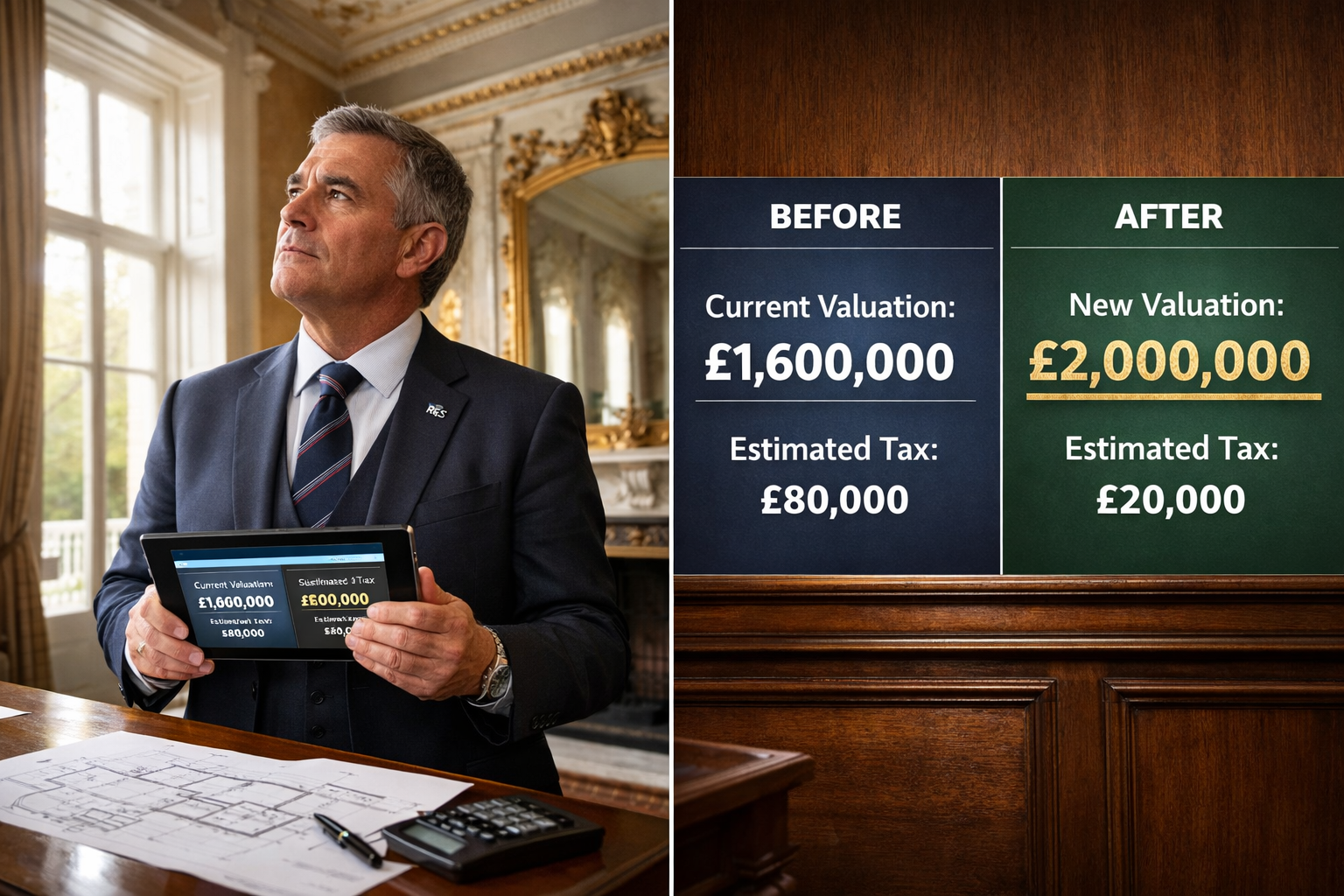

This means a property valued at £2.5 million incurs approximately £313,750 in SDLT alone—a figure that significantly impacts buyer purchasing power and willingness to pay premium prices.

Beyond SDLT, high-value property owners must contend with:

- Annual Tax on Enveloped Dwellings (ATED): Applicable to properties held in corporate structures, with annual charges ranging from £4,150 to £265,900 depending on property value

- Capital Gains Tax: Up to 28% on residential property gains for higher-rate taxpayers

- Inheritance Tax: 40% on estates exceeding nil-rate bands, with property often forming the largest component

According to recent market analysis, these combined tax burdens have created distinct pricing pressure points, with properties clustering just below the £2 million threshold to minimize tax exposure [1].

Market Response to Tax Thresholds

The RICS February 2026 market survey reveals significant buyer sensitivity to tax-driven pricing in the prime property sector [2]. Surveyors report that properties priced between £1.95 million and £2.05 million experience markedly different demand patterns, with strategic pricing just below the threshold generating substantially more buyer interest.

"The £2 million threshold has become a psychological and financial barrier that fundamentally alters valuation approaches. We're seeing sophisticated buyers who understand the tax implications demanding valuations that reflect this reality." — Senior RICS Surveyor, Prime London Market

This market behavior necessitates that professional surveyors incorporate tax-driven adjustments into their valuation methodologies, moving beyond traditional comparable sales analysis to account for fiscal considerations that directly impact property values.

Surveyor Tactics for Valuation Adjustments in Tax-Driven Transactions

Professional surveyors employing Valuation Adjustments for Tax-Driven High-Value Property Transactions: Surveyor Tactics for Properties Over £2 Million in 2026 must adopt sophisticated methodologies that acknowledge the complex interplay between property characteristics, market conditions, and tax implications.

Comparative Market Analysis with Tax Considerations

Traditional comparative market analysis relies on identifying similar properties that have recently sold and adjusting for differences in location, size, condition, and features. For properties over £2 million, this methodology requires additional layers of analysis:

1. Tax-Adjusted Comparable Selection

Surveyors must carefully select comparables that reflect similar tax positions. A property sold at £1.95 million may not be directly comparable to one valued at £2.1 million due to the dramatically different tax burdens faced by buyers. Professional practice now includes:

- Identifying comparables within the same tax bracket

- Adjusting for the differential tax burden between properties at different price points

- Considering whether comparable transactions involved tax-motivated pricing strategies

2. Threshold Proximity Adjustments

Properties positioned near tax thresholds require specific valuation adjustments that account for:

- Buyer pool restrictions: Properties priced above £2 million face a smaller pool of qualified buyers willing to absorb higher tax costs

- Marketing time extensions: Higher-priced properties in 2026 are experiencing extended marketing periods, affecting valuation through time-value considerations

- Negotiation leverage shifts: Sellers of properties just above thresholds face stronger buyer negotiating positions due to tax burden awareness

Documentation and Justification of Tax-Related Adjustments

RICS standards require that all valuation adjustments be clearly documented and defensible. For tax-driven adjustments, this means:

Explicit Statement of Tax Impact

Professional valuation reports for properties over £2 million should include:

- Clear calculation of applicable tax burdens at various price points

- Analysis of how tax considerations have influenced comparable sales data

- Discussion of market evidence showing tax-driven pricing behavior

Quantified Adjustment Factors

Rather than applying subjective adjustments, surveyors should quantify tax-related impacts where possible:

- Threshold discount factor: Market evidence from 2026 suggests properties positioned £50,000-£100,000 above the £2 million threshold may trade at 2-3% discounts compared to tax-neutral valuations

- Liquidity adjustment: Extended marketing times for properties above tax thresholds may warrant 1-2% valuation reductions to reflect reduced marketability

- Buyer pool restriction premium: Properties strategically priced just below thresholds may command 1-2% premiums due to enhanced marketability

Strategic Valuation Approaches for Different Client Objectives

The purpose of the valuation significantly influences how tax considerations are incorporated. Surveyors must tailor their approach based on whether the valuation is for:

Purchase Decisions

Buyers commissioning property surveys need valuations that reflect realistic market value considering tax burdens. This includes:

- Analysis of whether the asking price appropriately reflects tax position

- Identification of negotiation opportunities based on tax-driven market conditions

- Assessment of alternative properties at different price points to optimize tax efficiency

Sale Preparations

Sellers benefit from valuations that identify optimal pricing strategies:

- Evaluation of whether pricing just below the £2 million threshold maximizes net proceeds

- Analysis of target buyer demographics and their tax sensitivity

- Strategic timing recommendations based on market conditions and tax year considerations

Financing and Mortgage Purposes

Lenders require conservative valuations that account for potential market volatility in the high-value segment:

- Incorporation of risk factors related to tax-driven demand fluctuations

- Assessment of property marketability under stressed market conditions

- Consideration of forced sale scenarios where tax burdens may further depress achievable prices

Advanced Tactics for Properties Over £2 Million in 2026

As the surveying profession adapts to the tax-driven landscape of 2026, several advanced tactics have emerged as best practices for handling high-value property valuations.

Segmentation Analysis by Property Type and Location

Not all properties over £2 million respond identically to tax pressures. Surveyors must differentiate between:

Prime Central London vs. Secondary Locations

Properties in Marylebone and Richmond demonstrate different tax sensitivity profiles. Ultra-prime locations with international buyer bases show greater resilience to tax thresholds, while secondary prime locations exhibit more pronounced threshold effects.

Property Type Considerations

- Period properties: Unique heritage properties with limited comparables may justify valuations above tax-efficient thresholds due to scarcity value

- New developments: Modern apartments and houses face stronger tax-driven pricing pressure due to greater substitutability

- Investment properties: Buy-to-let investors demonstrate heightened tax sensitivity, requiring additional yield-based adjustments

Temporal Considerations and Market Timing

The 2026 property market shows distinct seasonal and cyclical patterns that interact with tax considerations [3]:

Tax Year Planning

Sophisticated buyers increasingly time purchases to optimize tax positions:

- Transactions completed before tax year-end to utilize annual allowances

- Strategic delays to align with anticipated tax legislation changes

- Coordination with other asset disposals for overall tax efficiency

Surveyors must consider whether comparable sales reflect optimal or suboptimal timing from a tax perspective, adjusting valuations accordingly.

Market Cycle Positioning

The surveying sector's recovery in 2026 has created variable market conditions across different price segments [3]. Properties over £2 million have experienced:

- Increased price sensitivity: Buyers demanding greater value propositions to justify tax burdens

- Extended negotiation periods: Average time from offer to exchange extending by 15-20% compared to sub-£2 million properties

- Greater due diligence: Enhanced scrutiny of property condition, requiring more detailed building surveys to support valuations

Integration of Tax Advisory Perspectives

Leading surveyors in 2026 increasingly collaborate with tax advisors to provide comprehensive valuation services. This integrated approach includes:

Structure Optimization Analysis

For high-net-worth clients, the ownership structure significantly impacts tax efficiency:

- Personal ownership: Full SDLT and CGT exposure but simpler structure

- Corporate ownership: ATED liability but potential IHT planning benefits

- Trust structures: Complex tax treatment requiring specialist valuation approaches

Surveyors must understand how different structures affect market value and provide structure-specific valuations where appropriate.

Cross-Border Considerations

International buyers face additional tax layers including:

- Non-resident SDLT surcharges (additional 2% for overseas buyers)

- Double taxation considerations

- Currency exchange implications affecting effective property values

Properties in areas with high international buyer concentration, such as Islington and Wandsworth, require valuation adjustments reflecting these factors.

Communication Strategies for High-Net-Worth Clients

Effective communication of tax-driven valuation adjustments represents a critical competency for surveyors working in the £2 million-plus market segment. High-net-worth clients expect sophisticated analysis presented in accessible terms.

Presenting Complex Tax Analysis Clearly

Professional valuation reports should include:

Visual Representations of Tax Impact

- Charts showing cumulative tax burdens at different price points

- Comparison tables illustrating net cost differences between properties priced above and below thresholds

- Scenario analyses demonstrating financial outcomes under different pricing strategies

Plain Language Explanations

While technical accuracy is essential, surveyors must translate complex tax concepts into understandable terms. Effective reports explain:

- Why tax considerations justify specific valuation adjustments

- How comparable properties' tax positions affect their relevance to the subject property

- What strategic options exist for optimizing value realization

Managing Client Expectations

The tax-driven market of 2026 has created situations where professionally supported valuations may differ significantly from client expectations or asking prices. Surveyors must:

Provide Evidence-Based Justifications

When valuations come in below expectations due to tax-driven market adjustments, comprehensive supporting evidence is essential:

- Market data showing actual transaction prices relative to asking prices

- Analysis of days-on-market for comparable properties at different price points

- Documentation of buyer feedback regarding tax burden concerns

Offer Strategic Alternatives

Rather than simply delivering disappointing valuations, professional surveyors provide actionable recommendations:

- Optimal pricing strategies to maximize net proceeds

- Property improvement recommendations that justify premium pricing despite tax burdens

- Timing recommendations based on anticipated market or tax legislation changes

Ethical Considerations and Professional Standards

The pressure to deliver valuations that support client objectives must be balanced against professional obligations to provide accurate, unbiased assessments. RICS standards require that surveyors:

- Maintain independence and objectivity regardless of client preferences

- Clearly distinguish between market value and other value bases

- Disclose any limitations or uncertainties in tax-driven adjustments

- Avoid advocacy positions that compromise professional integrity

When clients request valuations for specific purposes (such as supporting loan applications or tax appeals), surveyors must ensure their methodologies and conclusions remain defensible under professional scrutiny.

Practical Implementation: Case Study Approach

To illustrate how Valuation Adjustments for Tax-Driven High-Value Property Transactions: Surveyor Tactics for Properties Over £2 Million in 2026 function in practice, consider these representative scenarios:

Case Study 1: Period Property in Prime Location

Property: Victorian semi-detached house in Camden

Asking Price: £2,150,000

Client Objective: Purchase valuation to support mortgage application

Surveyor Analysis:

The property's asking price positions it £150,000 above the critical £2 million threshold, creating an additional SDLT burden of approximately £22,500 compared to a property priced at £1,995,000. Market analysis revealed:

- Three comparable properties sold in the previous six months at £1,950,000, £2,050,000, and £2,200,000

- The £2,050,000 comparable took 147 days to sell versus 68 days for the £1,950,000 property

- The £2,200,000 comparable ultimately achieved £2,125,000 after price reduction

Valuation Adjustments Applied:

- Threshold position adjustment: -2% (£43,000) to reflect reduced buyer pool and extended marketing time

- Condition premium: +1.5% (£32,250) for superior presentation relative to comparables

- Location micro-premium: +0.5% (£10,750) for particularly desirable street position

Final Valuation: £2,050,000

This valuation provided the buyer with strong negotiating leverage while remaining defensible to mortgage lenders based on comparable evidence and explicit tax-driven adjustments.

Case Study 2: New Development Apartment

Property: Two-bedroom apartment in luxury development, Southwark

Developer Asking Price: £2,100,000

Client Objective: Investment purchase decision

Surveyor Analysis:

New development properties face particular challenges in the current tax environment due to:

- Limited comparable sales data (development recently completed)

- Higher substitutability compared to unique period properties

- Investment buyers' heightened tax sensitivity due to yield calculations

Market research identified significant buyer resistance to new development pricing above £2 million, with several comparable developments offering incentives or price reductions to stimulate sales.

Valuation Adjustments Applied:

- New build premium reduction: Traditional 5-7% new build premium reduced to 2% due to tax-driven market conditions

- Threshold deterrent factor: -3% adjustment for positioning above £2 million in a market segment with strong price competition

- Liquidity discount: -1.5% for extended anticipated marketing time in current market

Final Valuation: £1,950,000

This valuation identified a significant disconnect between developer pricing and market reality, enabling the client to make an informed decision and negotiate from a position of knowledge.

Technology and Data Analytics in Tax-Driven Valuations

The complexity of Valuation Adjustments for Tax-Driven High-Value Property Transactions: Surveyor Tactics for Properties Over £2 Million in 2026 has driven increased adoption of sophisticated technology tools among professional surveyors.

Automated Valuation Models (AVMs) with Tax Integration

Advanced AVMs now incorporate tax threshold effects into their algorithms, though professional surveyors recognize their limitations:

Strengths:

- Rapid processing of large comparable datasets

- Consistent application of tax-driven adjustment factors

- Identification of pricing anomalies and market trends

Limitations:

- Inability to assess unique property characteristics

- Limited consideration of qualitative factors affecting value

- Potential over-reliance on historical data in rapidly changing markets

Professional practice in 2026 involves using AVMs as starting points while applying expert judgment to refine valuations based on property-specific factors.

Market Intelligence Platforms

Specialized platforms now provide real-time data on:

- Days-on-market trends segmented by price threshold

- Price reduction patterns for properties above £2 million

- Buyer inquiry volumes at different price points

- Transaction completion rates relative to asking prices

This data enables surveyors to quantify tax-driven market effects with greater precision than previously possible.

Client Presentation Technologies

Modern valuation reports increasingly incorporate interactive elements:

- Dynamic charts allowing clients to explore different pricing scenarios

- Tax calculators integrated directly into valuation reports

- Comparative analyses showing net cost implications of different properties

These tools enhance client understanding and support more informed decision-making in complex tax-driven markets.

Future Outlook: Evolving Tax Landscape and Surveyor Adaptation

As 2026 progresses, several trends are shaping the future of high-value property valuation:

Potential Tax Reform Implications

Ongoing discussions about property tax reform could significantly impact valuation approaches:

- Wealth tax proposals: Potential introduction of annual wealth taxes on high-value property holdings

- SDLT threshold adjustments: Speculation about potential changes to tax bands and rates

- Non-dom status reforms: Changes affecting international buyer tax positions

Surveyors must maintain awareness of legislative developments and their potential market impacts, adjusting valuation methodologies as the fiscal landscape evolves.

Market Adaptation Strategies

The property market continues adapting to tax realities through:

- Increased seller flexibility: Greater willingness to negotiate on price to achieve sales

- Creative deal structures: Use of chattels separation, delayed completions, and other mechanisms to optimize tax positions

- Enhanced property presentation: Sellers investing more heavily in presentation to justify premium pricing despite tax burdens

These adaptations require surveyors to continuously refine their understanding of market dynamics and incorporate emerging trends into valuation approaches.

Professional Development Imperatives

The complexity of tax-driven valuations necessitates ongoing professional development. Leading surveyors in 2026 are:

- Pursuing specialized qualifications in tax-related property matters

- Collaborating with tax advisors to deepen understanding of fiscal implications

- Participating in peer review processes to refine adjustment methodologies

- Contributing to industry guidance on best practices for tax-driven valuations

Conclusion

Valuation Adjustments for Tax-Driven High-Value Property Transactions: Surveyor Tactics for Properties Over £2 Million in 2026 represent a sophisticated evolution of traditional valuation methodologies, responding to the complex fiscal landscape that now defines the prime property market. The £2 million threshold has emerged as a critical inflection point that fundamentally influences buyer behavior, market dynamics, and ultimately property values.

Professional surveyors operating in this space must master multiple competencies: technical valuation expertise, deep understanding of tax legislation and its practical implications, sophisticated market analysis capabilities, and effective client communication skills. The integration of these competencies enables delivery of valuations that accurately reflect market realities while providing clients with actionable intelligence for strategic decision-making.

Key Success Factors

Surveyors who excel in high-value property valuation demonstrate:

✅ Rigorous methodology: Systematic approaches to identifying, quantifying, and documenting tax-driven adjustments

✅ Market intelligence: Current knowledge of transaction patterns, buyer behavior, and pricing trends in the £2 million-plus segment

✅ Technical tax knowledge: Understanding of SDLT, CGT, ATED, and other relevant tax considerations

✅ Client-focused communication: Ability to present complex analysis in accessible, actionable terms

✅ Professional integrity: Commitment to objective, evidence-based valuations regardless of client pressure

Actionable Next Steps

For property professionals and high-net-worth clients navigating the tax-driven market of 2026:

-

Engage specialist surveyors early: Properties over £2 million require expertise beyond standard residential valuation capabilities. Seek RICS-qualified surveyors with demonstrated experience in the prime market.

-

Request comprehensive tax analysis: Ensure valuation reports explicitly address tax implications and include scenario analyses showing outcomes at different price points.

-

Consider strategic timing: Work with advisors to identify optimal transaction timing considering tax year planning, market conditions, and personal circumstances.

-

Explore structural alternatives: Investigate whether different ownership structures or transaction mechanisms could optimize tax positions while achieving property objectives.

-

Maintain realistic expectations: Understand that professional valuations may differ from aspirational pricing due to tax-driven market realities, and that accurate valuations ultimately serve client interests better than optimistic assessments.

The tax-driven property market of 2026 presents challenges but also opportunities for those who approach transactions with sophisticated analysis and strategic thinking. Professional surveyors employing advanced valuation tactics provide essential guidance for navigating this complex landscape, enabling clients to make informed decisions that optimize both property value and tax efficiency.

For expert assistance with high-value property valuations incorporating comprehensive tax considerations, consult with experienced chartered surveyors who understand the nuances of the £2 million-plus market and can deliver the sophisticated analysis required for successful transactions in 2026's fiscal environment.

References

[1] Property Valuation Explained Uk Guide 2026 – https://kefihub.co.uk/trending/property-valuation-explained-uk-guide-2026/

[2] Uk Residential Market Survey February 2026 – https://www.rics.org/content/dam/ricsglobal/documents/market-surveys/uk-residential-market-survey/UK-Residential-Market-Survey_February-2026.pdf

[3] Surveying In 2026 Reform Recovery And Renewed Demand – https://www.lrg.co.uk/news-and-insights/surveying-in-2026-reform-recovery-and-renewed-demand/