The UK property market stands at a critical crossroads in 2026. While national house price momentum weakens and southern regions face significant downward pressure, Northern England emerges as a beacon of opportunity for savvy surveyors and property professionals. Understanding how to apply the latest RICS valuation methodologies to these diverging regional markets has never been more important for accurate property appraisals and strategic investment decisions.

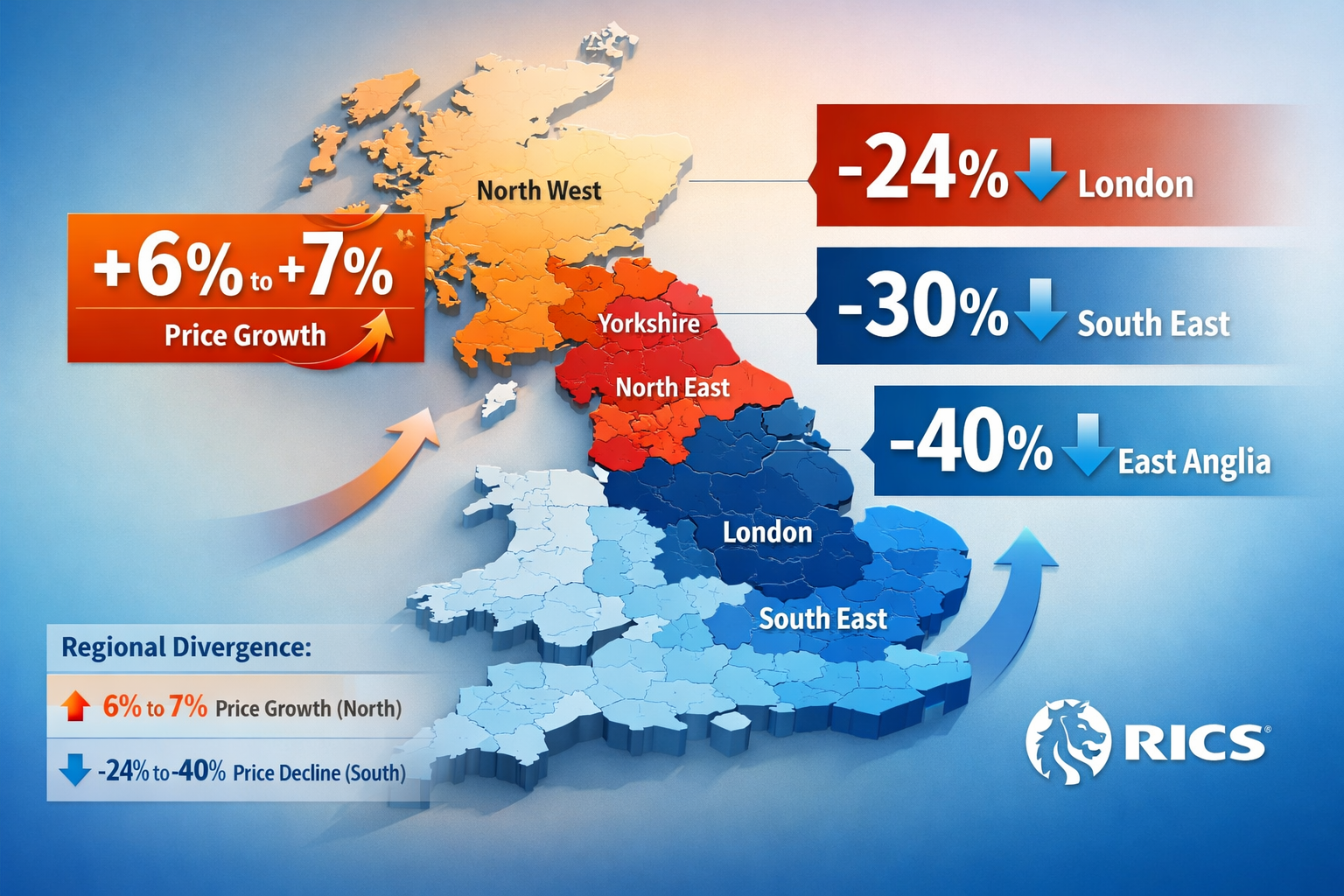

The Valuation Strategies for Stabilising House Prices: Applying March 2026 RICS Insights to Northern England Opportunities represent a fundamental shift in how property professionals must approach regional market analysis. Recent RICS survey data reveals that while the national headline house price balance fell to -12% in February 2026, Northern Ireland, Scotland, and the North West of England continue reporting price gains, with some locations experiencing surges of 6-7%.[1][4]

This stark regional divergence demands refined valuation techniques that account for local market dynamics rather than relying solely on national trends. For surveyors working across different regions, the ability to distinguish between stabilising markets and those experiencing genuine growth has become essential for providing clients with accurate, actionable property valuations.

Key Takeaways

- Regional divergence intensifies: Northern England shows 6-7% price growth while London experiences -40% downward pressure, requiring location-specific valuation approaches[1][4]

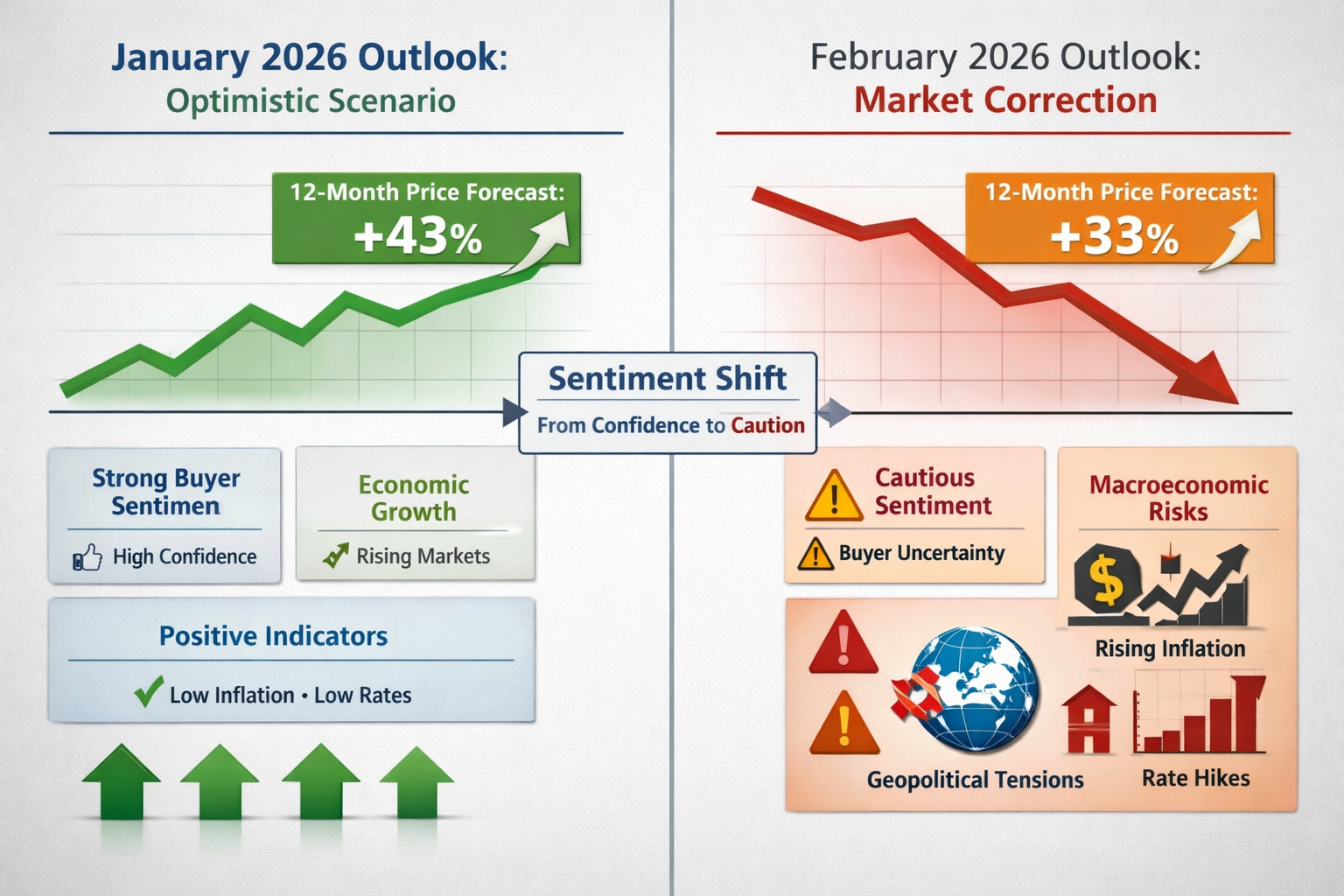

- Short-term sentiment weakened sharply: Near-term price expectations dropped from -6% to -18% in February 2026, but 12-month outlook remains moderately positive at +33%[3]

- RICS Red Book valuation standards provide the framework for navigating volatile markets through comparable analysis and adjustment techniques

- Northern opportunities outweigh southern caution: Scotland, Northern Ireland, and North West England lead price appreciation despite national headwinds[2]

- Macroeconomic factors drive uncertainty: Inflation concerns, interest rate outlook, and geopolitical tensions create volatility requiring robust valuation methodologies[3]

Understanding the March 2026 RICS Market Landscape

National Price Trends and Regional Disparities

The February 2026 RICS Residential Market Survey revealed a concerning reversal in national momentum. The headline house price balance declined to -12% from -10% in January, marking the first deterioration in four months and missing market expectations for improvement to -9%.[1] This represents a net balance where more surveyors reported falling prices than rising ones.

However, this national figure masks dramatic regional variations that create both challenges and opportunities for property professionals:

| Region | Price Balance | Trend Direction |

|---|---|---|

| London | -40% | ⬇️ Significant decline |

| South East | -24% | ⬇️ Moderate decline |

| East Anglia | -26% | ⬇️ Moderate decline |

| North West England | Positive | ⬆️ Price gains |

| Scotland | Positive | ⬆️ Price gains |

| Northern Ireland | Positive | ⬆️ Price gains |

The data clearly demonstrates that Northern England and Celtic nations are experiencing fundamentally different market conditions compared to southern regions.[3] For surveyors conducting valuations, this means that national averages provide limited guidance for local property assessments.

Short-Term Versus Long-Term Market Expectations

One of the most striking findings from the March 2026 RICS insights concerns the divergence between near-term and medium-term price expectations:

Near-term outlook (next 3 months):

- Dropped sharply to -18% in February from -6% in January

- Reflects renewed caution among surveyors

- Influenced by macroeconomic headwinds and interest rate concerns[3]

Medium-term outlook (next 12 months):

- Stands at +33% in February, down from +43% in January

- Remains moderately positive despite cooling

- Suggests underlying confidence in market fundamentals[1]

This divergence is particularly important for RICS surveyors applying valuation strategies. While short-term volatility may affect transaction volumes and negotiation dynamics, the more positive 12-month outlook supports stable underlying property values in well-performing regions.

The London Sentiment Collapse

Perhaps the most dramatic shift in the March 2026 data concerns London's 12-month price expectations, which plummeted from +56% in January to just +7% in February.[3] This represents a collapse in investor confidence and signals that the capital's property market faces unique pressures not present in northern regions.

For surveyors working across multiple regions, this London-specific weakness reinforces the importance of location-specific valuation approaches rather than applying London-centric assumptions to properties elsewhere in the country.

Valuation Strategies for Stabilising House Prices in Northern England Markets

Applying RICS Red Book Standards to Regional Variations

The RICS Valuation – Global Standards (Red Book) provides the professional framework that all chartered surveyors must follow when conducting formal valuations. In the context of the 2026 regional divergence, several Red Book principles become particularly relevant:

Comparable Evidence Analysis 📊

When applying Red Book valuation standards, surveyors must select comparable properties that reflect current market conditions. In Northern England's appreciating markets, this means:

- Prioritizing recent transactions (within the last 3-6 months) over older comparables

- Adjusting for the 6-7% price surge trajectory when analyzing sale prices[4]

- Recognizing that comparables from 12 months ago may significantly undervalue current market levels

- Applying appropriate time adjustments to reflect rapid price appreciation

Market Conditions and Assumptions

The Red Book requires surveyors to clearly state the market conditions and assumptions underlying their valuations. For Northern England properties in 2026, this includes:

- Acknowledging the positive regional price momentum despite national weakness

- Documenting local demand drivers (employment, infrastructure investment, affordability advantages)

- Explaining how regional conditions differ from national trends

- Providing context about buyer demand levels and transaction volumes

Regional Adjustment Techniques for Accurate Appraisals

Effective valuation strategies for stabilising house prices require sophisticated adjustment techniques that account for regional market dynamics:

Location Premium Adjustments 🏘️

Northern England's relative outperformance creates location-specific premiums that must be quantified:

- Affordability advantage: Northern properties typically cost 40-60% less than equivalent southern properties, driving demand from priced-out buyers

- Regional economic growth: Cities like Manchester, Leeds, and Liverpool benefit from business relocation and infrastructure investment

- Quality of life factors: Lower living costs combined with improving amenities enhance regional attractiveness

Time-Based Adjustments

In rapidly appreciating markets, time adjustments become critical:

- Apply monthly appreciation rates based on local RICS survey data

- Use 0.5-0.6% monthly adjustments for properties in the strongest Northern England locations (reflecting 6-7% annual growth)[4]

- Document the methodology and data sources supporting time adjustments

- Consider seasonal variations in local market activity

Physical Condition and Modernisation

Northern England's housing stock includes significant Victorian and Edwardian properties requiring condition-based adjustments:

- Commission detailed building surveys to identify maintenance issues affecting value

- Apply appropriate deductions for properties requiring modernisation

- Recognize that well-maintained period properties command premiums in gentrifying areas

- Account for energy efficiency improvements that enhance marketability

Comparable Sales Selection in Divergent Markets

The quality of comparable evidence directly determines valuation accuracy. In 2026's divergent market conditions, surveyors must refine their comparable selection criteria:

Geographic Proximity Considerations

- Limit search radius to 0.5-1 mile in urban areas with distinct neighborhoods

- Recognize that micromarket conditions vary significantly even within the same city

- Avoid using comparables from declining areas when valuing properties in appreciating neighborhoods

- Document why specific comparables were selected or rejected

Property Type and Condition Matching

- Ensure comparables match the subject property's type, age, and condition

- Apply adjustments for differences in accommodation, plot size, and features

- Consider the impact of structural issues on comparable values

- Account for modernisation differences between subject and comparables

Transaction Circumstances

- Verify whether comparable sales were arm's length transactions

- Exclude forced sales, family transactions, or other non-market circumstances

- Consider whether buyers used Help to Buy or other government schemes

- Assess whether comparable properties sold above or below asking price

Incorporating RICS Survey Data into Valuation Reports

The March 2026 RICS insights provide valuable market intelligence that should inform professional valuation reports:

Market Commentary Sections

Include relevant RICS data in valuation reports to provide context:

"The RICS Residential Market Survey for February 2026 indicates that the North West of England continues to experience positive price momentum, with net balances showing price gains. This contrasts sharply with southern regions where the headline balance stands at -12% nationally."[1][3]

Supporting Professional Judgement

Use RICS data to justify valuation conclusions:

- Reference the +33% twelve-month price expectation to support stable or appreciating valuations[1]

- Cite regional divergence data when explaining why local values differ from national trends

- Acknowledge short-term uncertainty while emphasizing medium-term fundamentals

- Provide clients with balanced market perspectives based on professional survey data

Capitalising on Northern Resilience: Practical Valuation Applications

Residential Purchase Valuations

For buyers seeking mortgage valuations in Northern England, the March 2026 RICS insights suggest several strategic considerations:

Timing and Negotiation Strategy ⏰

The weakening short-term sentiment (-18% near-term expectations) creates negotiation opportunities even in appreciating markets:[3]

- Buyers can reference national uncertainty to negotiate purchase prices

- However, strong local fundamentals limit downward pressure in Northern England

- Average price reductions after surveys may be smaller in high-demand northern locations

- Properties in prime northern areas may receive multiple offers despite national caution

Survey Level Selection

Choosing the right survey type becomes particularly important in Northern England's older housing stock:

- Level 2 (HomeBuyer Report): Suitable for conventional properties built after 1900 in reasonable condition

- Level 3 (Building Survey): Recommended for Victorian/Edwardian properties, unusual construction, or properties requiring renovation

- Specialist surveys: Consider damp surveys for older properties in Northern England's wetter climate

Investment Property Valuations

For property investors targeting Northern England's growth markets, valuation strategies must incorporate rental yield analysis alongside capital appreciation potential:

Yield-Based Valuation Approaches

- Calculate gross and net rental yields based on current market rents

- Compare yields to alternative investments and regional averages

- Apply appropriate capitalisation rates reflecting local market conditions

- Consider the impact of tenant demand on void periods and rental growth

Capital Growth Projections

The 6-7% price surge data provides a foundation for growth projections:[4]

- Use conservative growth assumptions (3-5% annually) for long-term projections

- Recognize that current growth rates may moderate as prices rise

- Factor in infrastructure improvements (HS2, Northern Powerhouse investments) supporting long-term appreciation

- Consider demographic trends and employment growth in target locations

Remortgage and Equity Release Valuations

Existing homeowners in Northern England benefit from recent price appreciation when seeking remortgages or equity release:

Equity Position Assessment

- Recent price gains may have significantly improved loan-to-value ratios

- Homeowners who purchased 2-3 years ago may have substantial equity increases

- This creates opportunities for remortgaging at better rates or releasing equity for improvements

- Accurate current valuations are essential for maximizing borrowing capacity

Valuation Report Requirements

Lenders typically require RICS-compliant valuations for remortgage purposes:

- Desktop valuations may suffice for straightforward properties in stable markets

- Physical inspections recommended for properties with extensions or alterations

- Red Book valuations ensure professional standards and lender acceptance

- Valuation reports should reference recent comparable evidence demonstrating price appreciation

Development Appraisals and Feasibility Studies

For developers and investors considering Northern England projects, the March 2026 RICS insights support positive development feasibility:

Residual Land Valuation

- Strong sales values (reflecting 6-7% growth) improve development viability[4]

- Calculate residual land values using current market sales evidence

- Apply appropriate developer's profit margins (15-20% on GDV)

- Factor in construction cost inflation and planning timescales

Market Absorption Rates

- Assess local demand levels and typical sales periods

- Strong regional fundamentals support steady absorption in well-located schemes

- Consider the impact of national uncertainty on buyer decision-making timelines

- Phase developments appropriately to match market absorption capacity

Navigating Macroeconomic Headwinds and Market Uncertainty

Interest Rate Sensitivity and Affordability

The February 2026 RICS survey specifically noted that renewed concerns over the interest rate outlook contributed to weakening buyer demand.[3] Surveyors must understand how interest rate expectations affect property values:

Affordability Calculations

- Rising interest rates increase monthly mortgage payments, reducing maximum borrowing capacity

- A 1% interest rate increase typically reduces borrowing capacity by approximately 10%

- Northern England's lower absolute prices provide an affordability buffer compared to southern regions

- First-time buyers particularly affected by rate changes

Valuation Adjustments for Rate Sensitivity

- Properties at the upper end of local price ranges face greater interest rate sensitivity

- Smaller, more affordable properties maintain stronger demand during rate uncertainty

- Consider the proportion of cash buyers versus mortgaged buyers in local markets

- Properties requiring large mortgages relative to average incomes face greater downward pressure

Inflation and Construction Cost Impacts

Inflation concerns mentioned in the March 2026 RICS data affect both new-build and existing property valuations:[3]

New-Build Pricing Pressures

- Construction cost inflation may force developers to increase prices

- However, market resistance limits price increases in buyer-sensitive conditions

- This can compress developer margins and affect new scheme viability

- Existing properties may become relatively more attractive if new-build premiums widen

Existing Property Maintenance Costs

- Higher inflation increases the cost of property maintenance and improvements

- This affects investor calculations of net yields and returns

- Properties with deferred maintenance face larger valuation deductions

- Energy efficiency improvements become more economically attractive with higher energy costs

Geopolitical Uncertainty and Market Confidence

The RICS survey referenced geopolitical uncertainty as a factor weighing on market sentiment in early 2026.[3] While surveyors cannot predict geopolitical events, they can incorporate uncertainty into valuation approaches:

Risk-Adjusted Valuation Approaches ⚠️

- Apply more conservative growth assumptions during periods of heightened uncertainty

- Widen valuation ranges to reflect increased market volatility

- Clearly communicate uncertainty and risk factors to clients

- Consider scenario-based valuations showing different outcome possibilities

Flight to Quality Effects

- Uncertainty often drives demand toward prime locations and high-quality properties

- Well-located Northern England properties in strong markets may benefit from flight-to-quality dynamics

- Properties with defects or in marginal locations face disproportionate downward pressure

- This reinforces the importance of thorough building surveys to identify quality issues

Regional Market Intelligence: Northern England Hotspots

North West England: Manchester and Liverpool

The North West stands out as one of the strongest performing regions in the March 2026 RICS data, with positive price balances contrasting sharply with southern decline.[1][2]

Manchester Metropolitan Area 🏙️

- Strong employment growth in technology, professional services, and creative industries

- Major infrastructure investments including HS2 connections and airport expansion

- Significant student population supporting rental demand

- Gentrification of former industrial areas creating value appreciation opportunities

- Typical price appreciation: 6-7% in prime central locations[4]

Liverpool City Region

- UNESCO World Heritage status enhancing cultural appeal

- Regeneration of waterfront and Baltic Triangle areas

- More affordable than Manchester, attracting priced-out buyers and investors

- Strong rental yields (5-7% gross) combined with capital appreciation

- Improving transport links to Manchester and wider North West

Yorkshire and Humber: Leeds and Sheffield

Yorkshire cities benefit from strong economic fundamentals and relative affordability:

Leeds

- Major financial and professional services center

- Excellent rail connections to London (2 hours) and other northern cities

- Diverse economy providing employment stability

- Victorian and Edwardian housing stock in high demand after renovation

- Neighborhoods like Chapel Allerton and Roundhay commanding premiums

Sheffield

- Significant regeneration of city center and former industrial areas

- Lower absolute prices than Leeds or Manchester creating value opportunities

- Strong student population from two universities

- Green space and quality of life advantages

- Emerging technology and advanced manufacturing sectors

North East England: Newcastle and Durham

The North East offers the most affordable entry point into Northern England's property markets:

Newcastle upon Tyne

- Regional capital with diverse economy and cultural amenities

- Quayside and city center regeneration creating prime residential areas

- Strong rental demand from universities and professional employment

- Excellent value compared to other regional cities

- Transport improvements enhancing connectivity

Durham and Surrounding Areas

- Historic city with UNESCO World Heritage Site

- Affluent commuter villages surrounding the city

- Strong demand from professionals working in Newcastle or Teesside

- Period properties in conservation areas commanding premiums

- University providing stable rental demand

Professional Standards and Best Practices for 2026 Valuations

RICS Competency Requirements

Chartered surveyors conducting valuations in 2026's challenging market conditions must demonstrate specific competencies:

Technical Competence 📋

- Thorough understanding of RICS Red Book Global Standards

- Ability to select and analyze appropriate comparable evidence

- Proficiency in applying adjustments for property differences and market conditions

- Knowledge of local market dynamics and regional variations

- Understanding of macroeconomic factors affecting property values

Professional Judgement

- Balancing quantitative analysis with qualitative market intelligence

- Recognizing when standard approaches require modification for unusual circumstances

- Communicating uncertainty and risk factors clearly to clients

- Maintaining objectivity despite client pressure or market sentiment

- Documenting the reasoning behind valuation conclusions

Quality Assurance and Report Standards

High-quality valuation reports demonstrate professional competence and protect both surveyors and clients:

Essential Report Components

- Clear identification of the subject property with photographs

- Comprehensive property description including accommodation, construction, and condition

- Market commentary incorporating relevant RICS survey data

- Comparable evidence analysis with adjustments explained

- Valuation figure with appropriate caveats and assumptions

- Professional indemnity insurance details

Peer Review Processes

- Internal quality checks by senior surveyors before report release

- Regular calibration exercises comparing valuations across team members

- Monitoring of valuation accuracy through post-transaction analysis

- Continuing professional development to maintain market knowledge

- Engagement with RICS guidance updates and technical papers

Managing Client Expectations

The divergence between national trends and Northern England opportunities requires careful client communication:

Educating Clients About Regional Variations 💬

- Explain why national headlines may not reflect local market conditions

- Provide RICS data demonstrating regional divergence[1][3]

- Help clients understand the difference between short-term volatility and medium-term trends

- Clarify the limitations of automated valuation models (AVMs) in divergent markets

Realistic Growth Projections

- Avoid over-optimistic projections based on recent exceptional growth

- Explain that 6-7% growth rates may moderate as prices rise[4]

- Discuss potential downside scenarios and risk factors

- Emphasize that property should be viewed as a long-term investment

- Recommend clients consider their individual circumstances rather than treating property as speculation

Technology and Data in Modern Valuation Practice

Automated Valuation Models (AVMs) and Their Limitations

While technology plays an increasing role in property valuation, the March 2026 market conditions highlight AVM limitations:

AVM Strengths

- Rapid processing of large comparable datasets

- Consistency in applying statistical models

- Cost-effective for portfolio valuations or initial estimates

- Useful for monitoring market trends and price movements

AVM Weaknesses in 2026 Markets ⚠️

- Struggle to capture rapid regional divergence in real-time

- May lag actual market conditions by several months

- Cannot assess property-specific condition factors

- Fail to incorporate qualitative market intelligence

- Unreliable for unusual properties or thin markets

Professional Surveyor Value-Add

- Human judgement essential for interpreting complex market conditions

- Physical inspections identify condition issues affecting value

- Local market knowledge provides context AVMs cannot capture

- Ability to explain and justify valuations to clients and lenders

- Professional indemnity insurance protecting all parties

Data Sources for Enhanced Market Intelligence

Effective valuation strategies for stabilising house prices require access to comprehensive market data:

Primary Data Sources

- RICS Residential Market Survey: Monthly sentiment and price balance data[1][3]

- Land Registry: Actual transaction prices and volumes

- Local estate agents: Current asking prices and time-on-market data

- Rental platforms: Market rent levels and yield calculations

- Economic indicators: Employment, income, and demographic data

Integrating Multiple Data Sources

- Cross-reference RICS survey sentiment with actual transaction data

- Compare asking prices with achieved prices to assess market strength

- Monitor transaction volumes as leading indicator of price changes

- Track days-on-market as measure of demand intensity

- Analyze price-per-square-foot trends for different property types

Future Outlook: Sustaining Valuation Accuracy Through 2026

Monitoring Market Developments

The March 2026 RICS insights represent a snapshot of market conditions that will continue evolving:

Key Indicators to Watch 📊

- Monthly RICS price balances: Track whether the February decline continues or reverses

- Interest rate decisions: Bank of England policy directly affects affordability and demand

- Transaction volumes: Sustained activity levels support price stability

- Regional divergence trends: Monitor whether Northern strength persists or southern regions recover

- Economic growth data: GDP, employment, and wage growth underpin housing demand

Scenario Planning

Prudent surveyors should consider multiple potential scenarios:

- Base case: Continued regional divergence with Northern resilience and southern weakness

- Optimistic case: Interest rate cuts stimulate national recovery, narrowing regional gaps

- Pessimistic case: Macroeconomic headwinds intensify, affecting even strong northern markets

Adapting Valuation Approaches to Market Evolution

Flexibility and responsiveness separate exceptional surveyors from average practitioners:

Continuous Learning

- Regularly review RICS technical papers and market surveys

- Attend professional development courses on valuation methodology

- Engage with local property market networks and intelligence sharing

- Monitor comparable evidence continuously rather than relying on outdated data

- Stay informed about regulatory changes affecting property markets

Methodology Refinement

- Adjust comparable selection criteria as market conditions evolve

- Refine time adjustment factors based on actual price movement data

- Update location premium assessments as regional dynamics shift

- Incorporate new data sources and analytical tools as they become available

- Document methodology changes and rationale for transparency

Conclusion

The Valuation Strategies for Stabilising House Prices: Applying March 2026 RICS Insights to Northern England Opportunities demonstrate that professional surveyors must navigate an increasingly complex and regionally divergent property market. While national headlines show weakening momentum with the house price balance falling to -12% in February 2026, the reality on the ground varies dramatically by location.[1]

Northern England's resilience—with price surges reaching 6-7% in key locations—stands in stark contrast to London's -40% balance and southern England's broad-based weakness.[3][4] This divergence creates both challenges and opportunities for property professionals who can adapt their valuation approaches to local market conditions rather than relying on national averages.

Key strategic takeaways for surveyors and property professionals:

✅ Apply rigorous comparable analysis using recent, location-specific evidence rather than relying on outdated or geographically distant comparables

✅ Incorporate RICS survey data into valuation reports to provide clients with professional market intelligence and context

✅ Distinguish between short-term volatility and medium-term fundamentals, recognizing that the +33% twelve-month outlook supports underlying value stability despite near-term uncertainty[1]

✅ Utilize RICS Red Book standards as the foundation for professional valuations, ensuring consistency and credibility across all assignments

✅ Communicate regional variations clearly to clients, helping them understand why local markets may outperform or underperform national trends

✅ Maintain professional skepticism about automated valuations and headline figures that may not reflect nuanced local conditions

The March 2026 RICS insights reinforce that property valuation remains fundamentally a professional discipline requiring human judgement, local knowledge, and technical expertise. While technology and data provide valuable tools, the ability to interpret complex and contradictory market signals separates chartered surveyors from algorithmic approaches.

Actionable Next Steps

For property professionals seeking to capitalize on Northern England opportunities while navigating national uncertainty:

- Review your comparable evidence databases to ensure they reflect current market conditions and include sufficient Northern England transactions

- Engage with RICS professional standards through continuing professional development focused on regional market analysis

- Establish relationships with local agents and surveyors in Northern England markets to access timely market intelligence

- Commission appropriate surveys (Level 2 or Level 3) when purchasing or valuing properties to identify condition factors affecting value

- Monitor monthly RICS survey releases to track market evolution and adjust valuation approaches accordingly

- Document your methodology thoroughly in valuation reports, explaining how regional factors and current market conditions informed your conclusions

The property market's regional divergence in 2026 underscores that successful valuation practice requires continuous adaptation, professional judgement, and commitment to rigorous methodology. Surveyors who embrace these principles while leveraging RICS insights will deliver accurate valuations that serve their clients' interests and maintain professional standards during challenging market conditions.

For professional valuation services or expert guidance on property assessment in today's complex market, contact qualified RICS surveyors who understand regional dynamics and apply proven methodologies to deliver reliable property valuations.

References

[1] Rics House Price Balance – https://tradingeconomics.com/united-kingdom/rics-house-price-balance

[2] Uk Resi Survey Jan 2026 Report Shows Early Signs Market Recovery Despite Caution – https://www.rics.org/news-insights/uk-resi-survey-jan-2026-report-shows-early-signs-market-recovery-despite-caution

[3] Uk Residential Survey February 2026 – https://www.rics.org/news-insights/uk-residential-survey-february-2026

[4] Valuation Techniques For Northern England Property Boom 2026 Rics Methods Amid 6 7 Price Surges – https://nottinghillsurveyors.com/blog/valuation-techniques-for-northern-england-property-boom-2026-rics-methods-amid-6-7-price-surges