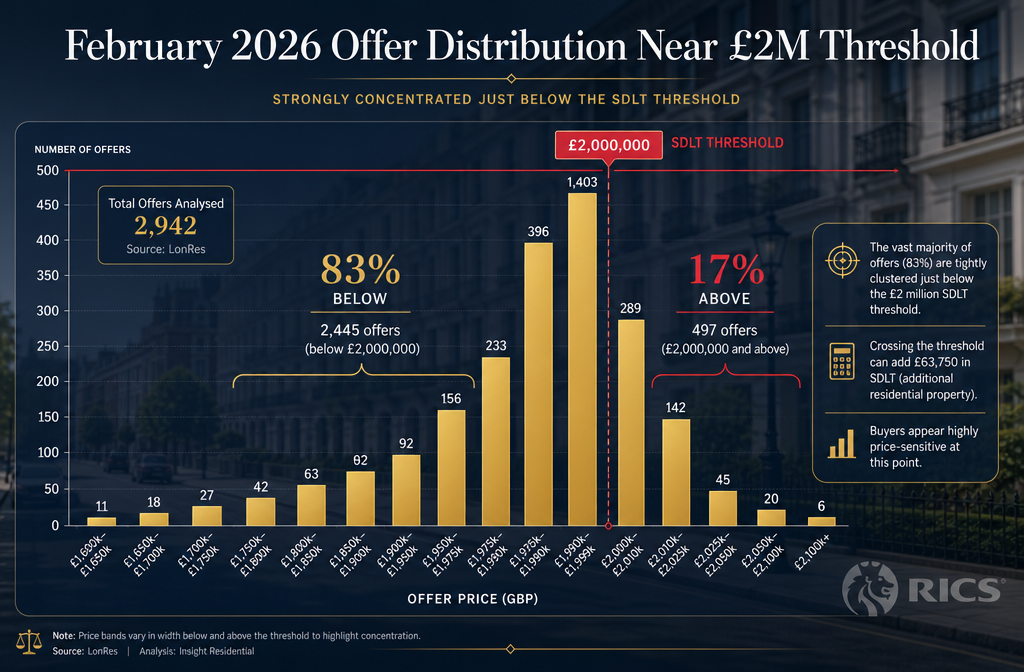

February 2026 transaction data reveals a striking pattern: 83% of accepted offers on properties near the £2 million mark fell just below that threshold — a clustering effect so pronounced it has forced chartered surveyors to fundamentally rethink how they approach luxury valuations. This is not coincidence. It is the direct consequence of stamp duty land tax (SDLT) threshold psychology meeting a cautiously recovering prime London market.

Understanding Valuer Responses to Post-Budget 2026 Threshold Effects: Strategies for High-Value Properties Over £2 Million is now essential for any professional involved in high-value property transactions. Whether acting for buyers, sellers, lenders, or developers, the ability to interpret, justify, and defend valuations in this distorted band of the market has become a core competency.

Key Takeaways 📌

- 83% of near-£2m offers in February 2026 fell below the threshold, confirming strong buyer resistance at fiscal breakpoints.

- Post-budget SDLT changes have created measurable price compression in the £1.8m–£2.2m band.

- RICS-aligned adjustment techniques require valuers to account for threshold distortion as a legitimate market factor.

- Comparable evidence selection must be carefully filtered to avoid importing threshold-suppressed prices into above-threshold valuations.

- Luxury property valuations in a recovering market demand transparent, defensible methodology — especially for mortgage and litigation purposes.

Understanding the Post-Budget Threshold Effect in 2026

The autumn 2025 Budget introduced revised SDLT surcharge thresholds that took full effect in early 2026. For buyers of residential properties above £2 million, the effective tax burden increased materially — creating a hard psychological and financial barrier at that price point.

What the February 2026 Data Tells Us

The 83% sub-threshold clustering figure is not merely anecdotal. It reflects a rational buyer response to a significant tax cliff edge. Consider the numbers:

| Purchase Price | Approximate SDLT Liability | Effective Rate |

|---|---|---|

| £1,999,999 | ~£153,750 | ~7.7% |

| £2,000,001 | ~£163,750+ | ~8.2%+ |

| £2,500,000 | ~£213,750+ | ~8.6%+ |

💡 Pull Quote: "A single pound above £2 million can trigger thousands in additional tax — and buyers know it. Valuers must acknowledge this as a genuine market dynamic, not a distortion to be ignored."

This creates what valuers now commonly refer to as a "shadow band" — a price range between roughly £1.85m and £2.15m where normal comparable evidence becomes unreliable without adjustment. Properties that would ordinarily transact at £2.1m are being negotiated down to £1.99m, while genuinely superior properties above £2m are sitting on the market longer.

For professionals providing RICS property valuations, this creates a direct challenge: how do you value a property whose natural market position sits above the threshold when comparable sales evidence is being systematically suppressed?

Valuer Responses to Post-Budget 2026 Threshold Effects: Core Adjustment Techniques

RICS Red Book guidance (Global Standards) requires valuers to reflect market value — the price a willing buyer and seller would agree in an arm's length transaction. When fiscal thresholds distort that market, the valuer's job is not to ignore the distortion but to understand and account for it correctly.

Technique 1: Threshold-Adjusted Comparable Selection

The most immediate practical challenge is comparable evidence. If 83% of transactions near £2m are clustering below the threshold, a naive selection of recent comparables will systematically undervalue properties that genuinely merit above-threshold pricing.

Best practice steps:

- Separate the evidence pool — distinguish between properties that transacted below threshold due to fiscal pressure versus those that genuinely reflected market value.

- Apply a threshold adjustment factor — where evidence shows a property was negotiated down from an asking price above £2m, the valuer should document the discount applied and consider reversing it for above-threshold subject properties.

- Use time-adjusted comparables — in a recovering market, older comparables (12–18 months prior) may better reflect the underlying value trajectory before threshold distortion took hold.

- Seek pre-negotiation evidence — original asking prices and early-stage offer data can provide useful anchoring evidence, particularly in prime central London markets.

Technique 2: Stratified Market Analysis

Not all high-value markets are equally affected. A stratified approach recognises that:

- Prime central London (Kensington, Chelsea, Knightsbridge) has a deeper pool of cash buyers less sensitive to SDLT thresholds.

- Outer prime markets (Barnet, Brentwood, Woodford Green) have a higher proportion of mortgage-dependent buyers where threshold sensitivity is acute.

Valuers covering Kensington property will encounter a different threshold dynamic compared to colleagues working in Brentwood or Barnet, where the buyer demographic is more cost-sensitive.

Stratified adjustment matrix:

| Market Zone | Cash Buyer % | Threshold Sensitivity | Recommended Adjustment |

|---|---|---|---|

| Prime Central London | 55–65% | Low–Medium | 0–2% upward adjustment |

| Outer Prime London | 25–35% | High | 2–4% upward adjustment |

| Commuter Belt Luxury | 15–25% | Very High | 3–5% upward adjustment |

Technique 3: Explicit Methodology Documentation

In a post-budget market, defensibility is everything. Lenders, courts, and HMRC all scrutinise high-value valuations. Every adjustment must be:

- Clearly stated in the valuation report

- Supported by named comparable evidence

- Cross-referenced to market commentary from recognised indices (Savills, Knight Frank, RICS market surveys)

- Accompanied by a sensitivity analysis showing the valuation range

For building surveyors in Knightsbridge and other prime areas, the expectation of lender scrutiny is particularly high. A valuation that simply adopts sub-threshold comparables without adjustment will not withstand challenge.

Strategies for High-Value Properties Over £2 Million in a Recovering Market

The prime London market in early 2026 is showing signs of recovery — transaction volumes are up approximately 11% year-on-year in Q1, and days-on-market for properties above £2m have shortened. This recovery context matters enormously for valuation strategy.

Strategy 1: Positioning Valuations Within the Recovery Narrative 📈

A recovering market means that current comparables may understate future value, but RICS methodology requires valuers to reflect current market value, not forecast value. The solution is transparent narrative:

- Reference market recovery indices in the valuation report.

- Note the direction of travel without extrapolating it into the valuation figure.

- Flag where threshold distortion may have suppressed recent comparable evidence.

This approach protects the valuer professionally while giving the client a complete picture of the market context.

Strategy 2: Renovation and Condition Adjustments 🔧

Above-threshold luxury properties often differ significantly in condition and specification from sub-threshold comparables. A renovation needs analysis is frequently required to justify the premium being applied.

Key condition factors that support above-threshold valuations include:

- Whole-house refurbishment to contemporary specification (kitchen, bathrooms, mechanical and electrical)

- Heritage features in good repair (original cornicing, fireplaces, period joinery)

- Planning permissions for extension or development

- Energy Performance Certificate (EPC) rating — increasingly important to buyers and lenders

Where a subject property has been recently refurbished to a high standard, the valuer can legitimately apply a condition premium over threshold-suppressed comparables that have not been updated.

Strategy 3: Lease and Tenure Considerations

For leasehold properties above £2m — particularly common in prime central London — lease length and service charge levels can significantly affect value. A property with a short lease (under 80 years) may be depressed below threshold not because of fiscal sensitivity but because of lease liability.

Valuers must disentangle these factors carefully. A statutory lease extension can substantially alter the valuation picture, and this should be noted explicitly where relevant.

Strategy 4: Client Advisory and Price Negotiation Support

Valuer Responses to Post-Budget 2026 Threshold Effects: Strategies for High-Value Properties Over £2 Million extend beyond the written report. Increasingly, valuers are being asked to provide advisory support during price negotiations — particularly where a buyer and seller are separated by the threshold line.

Practical advisory points for clients include:

- Structuring the deal — in some cases, fixtures and fittings can be separated from the headline price to bring the property price below threshold, though HMRC scrutinises this approach carefully.

- Understanding the net position — buyers should model the full cost of acquisition including SDLT, not just the headline price.

- Timing considerations — in a recovering market, waiting for further price growth above threshold may cost more in lost opportunity than the SDLT saving.

Avoiding Common Valuation Errors in the £2 Million Band

Even experienced valuers can fall into traps when working in threshold-distorted markets. The most common errors in 2026 include:

❌ Error 1: Uncritical Use of Sub-Threshold Comparables

Selecting three recent sales all clustered just below £2m and applying them directly to a property whose natural market position is £2.1m–£2.3m will produce a systematically low valuation. This exposes the valuer to challenge from both the client and any reviewing body.

❌ Error 2: Ignoring the Recovery Trend

Using comparables from Q3 2025 — when the market was at its most suppressed — without time adjustment in a Q1 2026 recovery context will undervalue the subject property.

❌ Error 3: Failing to Disclose Threshold Effects

A valuation report that does not acknowledge the existence of threshold distortion in the market commentary section is incomplete. RICS standards require market conditions to be described accurately.

❌ Error 4: Over-Adjusting Without Evidence

The opposite error is equally dangerous. Applying a 10% upward adjustment to "correct" for threshold effects without specific comparable support will not withstand scrutiny. Every adjustment must be evidence-based and proportionate.

For a broader understanding of how to choose the right level of survey and valuation service for different property types, the guide to choosing the right home survey provides useful context on matching survey depth to property complexity.

Regional Considerations Across the London and Home Counties Market

Valuer Responses to Post-Budget 2026 Threshold Effects: Strategies for High-Value Properties Over £2 Million must also account for significant regional variation across the London and Home Counties market.

Properties in Chelsea and Knightsbridge operate in a global prime market where international buyers — less sensitive to UK domestic SDLT thresholds — provide a floor of demand. In contrast, markets like Woodford Green or Romford at the upper end of their price ranges are almost entirely domestic buyer-driven, making threshold sensitivity acute.

Regional threshold sensitivity summary:

- 🏛️ Prime Central London — moderate threshold effect, deep cash buyer pool

- 🌳 Outer London (Barnet, Brentwood) — high threshold sensitivity, mortgage-dependent buyers

- 🚂 Commuter belt luxury — very high sensitivity, limited comparable depth above £2m

- 🌍 International buyer markets — lower sensitivity, but currency and political risk factors apply

Understanding these regional dynamics allows valuers to calibrate their adjustment approach appropriately rather than applying a one-size-fits-all methodology.

Conclusion: Actionable Next Steps for Valuers and Property Professionals

The February 2026 data showing 83% of near-£2m offers falling below the threshold is not just a market curiosity — it is a structural challenge that demands a structured response. The professionals who will serve their clients best in this environment are those who combine rigorous RICS-aligned methodology with a clear-eyed understanding of fiscal threshold psychology.

Actionable next steps:

- ✅ Audit your comparable evidence pools — ensure you are not importing threshold-suppressed prices into above-threshold valuations without adjustment.

- ✅ Document threshold effects explicitly in every valuation report covering the £1.8m–£2.2m band.

- ✅ Apply stratified market analysis based on buyer demographic and cash/mortgage split for each subject property's location.

- ✅ Commission condition and renovation assessments where specification differences between comparables and the subject property are material.

- ✅ Stay current with market recovery data — Q1 2026 recovery trends must be reflected in time adjustments to older comparables.

- ✅ Engage with clients proactively on the advisory dimension of threshold positioning, particularly around deal structuring and timing.

The prime property market above £2 million remains one of the most technically demanding areas of residential valuation practice. Mastering the post-budget threshold landscape is not optional — it is the defining professional challenge of 2026 for every valuer working in this space.