By 2028, an estimated £1 trillion worth of UK commercial property could be classified as stranded assets if owners fail to meet tightening Minimum Energy Efficiency Standards — and lenders are already adjusting their risk models now [4]. The shift is not gradual. Valuation Resilience Metrics for 2026: Incorporating EPC and Net Zero Factors in Upfront Lender Assessments has moved from a niche compliance conversation to a core underwriting priority, reshaping how mortgage lenders, commercial banks, and institutional investors price risk before a single brick is surveyed on-site.

This article breaks down what these changes mean in practice, how GeoConnect-style data tools are reducing costly re-inspections, and what property professionals, buyers, and lenders need to do right now.

Key Takeaways 📌

- 🏠 UK EPCs are moving to a multi-metric system in 2026, replacing the single energy cost score with fabric, emissions, and demand indicators.

- 🏦 Lenders are embedding EPC ratings into upfront risk models, meaning a low EPC score can affect loan-to-value ratios before a physical survey takes place.

- ⚠️ Commercial MEES tightens to EPC C by 2028 and EPC B by 2030, creating measurable stranded asset risk already being priced into valuations.

- 📊 GeoConnect and remote data tools are enabling lenders to build resilience profiles without repeated on-site inspections, cutting costs and delays.

- ✅ Proactive EPC improvement is now a financial strategy, not just a regulatory obligation.

Why 2026 Is a Turning Point for Energy-Based Valuations

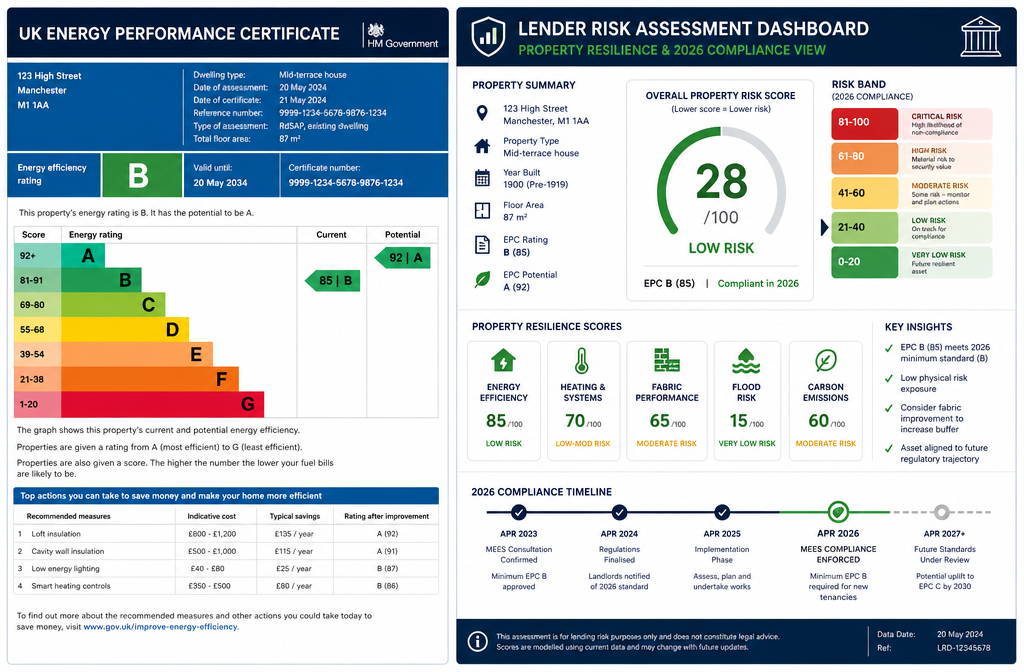

The phrase "turning point" is often overused in property commentary. In 2026, it is accurate. The UK government's reforms to the Energy Performance of Buildings regime are introducing a fundamentally different framework for how buildings are assessed and certified [8]. Rather than a single energy cost metric, the new system will incorporate fabric efficiency, space heating demand, and carbon emissions as separate indicators — each of which carries distinct implications for lenders assessing long-term asset resilience.

💬 "EPC grades and actual energy use remain 'chalk and cheese' — but lenders can no longer afford to treat them as separate conversations." [2]

This matters enormously for upfront lender assessments. Previously, a surveyor's physical inspection was the primary gateway to understanding a property's condition and energy profile. Now, data-led pre-screening is becoming standard practice. Lenders want to know, before commissioning a full survey, whether a property is likely to meet minimum standards — and whether it will hold its value across a 25-year mortgage term.

The Multi-Metric EPC: What Changes for Lenders

The move away from a single A-to-G energy cost score is significant [1]. Under the reformed system, lenders will need to interpret:

| Metric | What It Measures | Why It Matters to Lenders |

|---|---|---|

| Fabric Energy Efficiency | Insulation, windows, thermal mass | Predicts retrofit cost burden |

| Space Heating Demand | Energy needed to heat the building | Flags fuel poverty and default risk |

| Carbon Emissions Score | CO₂ output per square metre | Aligns with net zero lending targets |

| Primary Energy Use | Total energy consumption | Relevant to green finance eligibility |

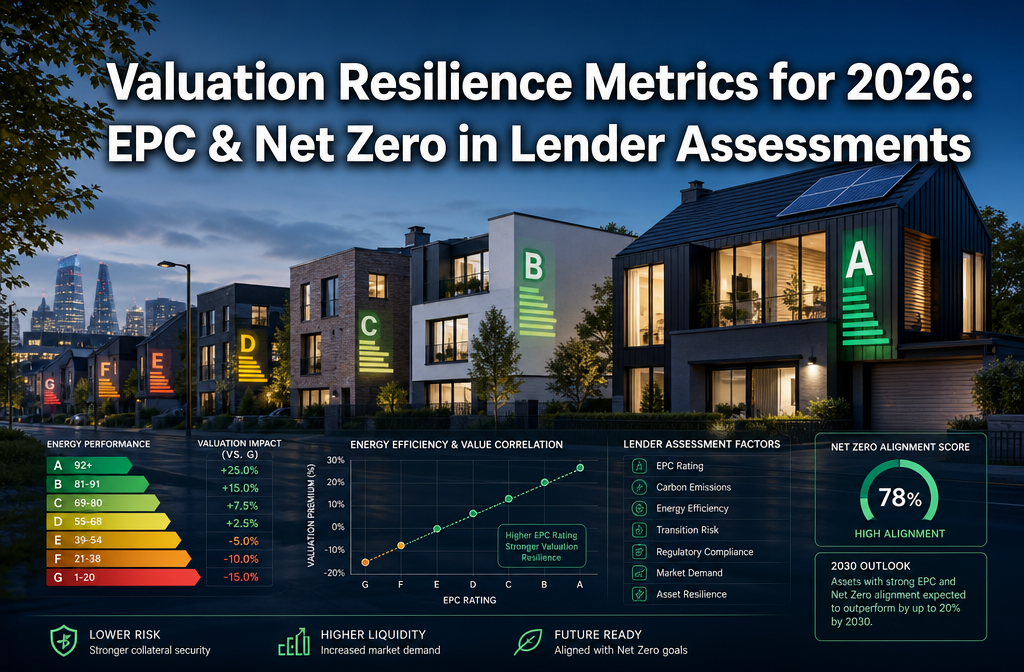

Each of these metrics feeds into what is increasingly called a valuation resilience score — a composite indicator that tells lenders how likely a property is to retain its value as net zero regulations tighten. For building condition assessments carried out by chartered surveyors, this means reports must now speak directly to these data points rather than treating energy performance as a footnote.

MEES Tightening: The Stranded Asset Clock Is Ticking ⏰

The Minimum Energy Efficiency Standards (MEES) trajectory is unambiguous:

- Private Rented Sector (Residential): New tenancies must meet EPC C equivalent standards (exact implementation timeline subject to ongoing consultation).

- Commercial Property: EPC C required by 2028; EPC B required by 2030 [5].

- Non-compliant properties: Cannot be legally let, triggering immediate loss of rental income and a direct hit to lender security valuations.

For lenders, this creates a re-pricing risk that must be factored in at origination, not at renewal. A commercial property currently rated EPC D or E may be fully let and generating income today — but by 2028, it could be unlettable without significant capital expenditure. The OECD has highlighted this dynamic explicitly, noting that climate-related physical and transition risks are increasingly material to real estate investment decisions [4].

How GeoConnect Data Is Reducing Re-Inspections in Upfront Assessments

One of the most practical developments in valuation resilience metrics for 2026 is the integration of geospatial and property data platforms — broadly referred to here as GeoConnect-style tools — into lender workflows. These platforms aggregate:

- Existing EPC register data

- Historic planning permissions and retrofit records

- Flood risk and climate hazard mapping

- Age, construction type, and comparable stock profiles

- Utility consumption data (where available)

The result is a pre-inspection resilience profile that lenders can generate before instructing a surveyor. This has two major benefits: it reduces the number of physical re-inspections required for straightforward cases, and it flags high-risk properties early so that more detailed expert building evaluation resources are directed where they are genuinely needed.

What a GeoConnect-Informed Lender Assessment Looks Like

A typical upfront lender assessment in 2026, informed by geospatial data, would include:

- EPC Register Pull — Current rating, date of last assessment, assessor methodology

- Retrofit Probability Score — Based on construction era, wall type, and local planning constraints

- Climate Hazard Overlay — Flood zone, subsidence risk, overheating potential

- Comparable Energy Performance — How the property performs against similar stock in the same postcode

- Net Zero Pathway Indicator — Estimated cost and timeline to reach EPC C or B

This approach aligns with the IIGCC's 2026 adaptation and resilience engagement priorities, which emphasise the need for asset-level data to support credible transition planning [3]. For lenders, it means that energy and climate risk are no longer assessed in isolation — they are integrated into the same upfront workflow as structural condition and legal title checks.

Reducing Re-Inspections: The Practical Case

Physical re-inspections are expensive. In a high-volume lending environment, requiring a new EPC assessment or structural survey for every remortgage or product transfer creates significant friction. GeoConnect-style data tools address this by:

- Flagging properties where existing EPC data is recent and reliable, avoiding unnecessary reassessment

- Identifying properties where the EPC is likely outdated (e.g., pre-2012 assessments on older stock) and triggering targeted re-inspection

- Providing lenders with a confidence score on the accuracy of existing data, enabling risk-proportionate decision-making

For property professionals working alongside lenders — including those offering RICS surveys — this means the nature of instructions is changing. Surveyors are increasingly being asked to validate or challenge data-led pre-assessments rather than starting from scratch. Understanding what to do before an RICS home survey is therefore more important than ever for buyers and sellers who want to avoid delays.

Incorporating Net Zero Factors into Valuation Resilience Metrics for 2026

Net zero is no longer a distant policy aspiration. It is a present-day valuation variable. Research published in 2026 confirms that properties with strong energy credentials command measurable price premiums, while those facing significant retrofit obligations are beginning to show value discounts — a phenomenon sometimes called the "brown discount" [5].

For lenders incorporating net zero factors into upfront assessments, the key questions are:

- What is the estimated retrofit cost to bring this property to EPC C or above?

- Who bears that cost — owner, tenant, or lender (via distressed sale)?

- What is the timeline risk — when does non-compliance become a legal or financial event?

- Is the property in a location where retrofit is feasible (e.g., listed building constraints, conservation area restrictions)?

The Green Premium and Brown Discount in Practice

Emerging evidence from the UK and European markets suggests:

- 🟢 EPC A/B properties are achieving 3–8% price premiums over equivalent EPC D/E stock in some markets [6]

- 🔴 EPC E/F/G properties in the private rented sector face liquidity discounts as investor demand falls ahead of MEES enforcement

- 🟡 EPC C properties are increasingly seen as the minimum acceptable standard for new lending, particularly in the buy-to-let sector

These dynamics are reshaping how lenders set loan-to-value ratios. A property with a poor EPC rating may still receive a mortgage offer — but at a lower LTV, higher rate, or with a retrofit condition attached. This is a direct translation of valuation resilience metrics into lending terms.

Net Zero Alignment in Commercial Real Estate

The commercial sector faces even sharper transition risk. The Climate Action 100+ Net Zero Company Benchmark highlights the growing expectation that real asset owners align their portfolios with 1.5°C pathways [9]. For commercial lenders, this means:

- Covenant reviews now routinely include EPC trajectory analysis

- Green loan eligibility is increasingly tied to EPC B or above

- Refinancing risk is explicitly modelled for assets likely to breach MEES by 2028 or 2030

Cotality's 2026 climate risk analysis reinforces this, noting that 2026 represents a structural inflection point where climate risk transitions from a disclosure exercise to a pricing mechanism embedded in mainstream finance [7].

For property professionals advising on commercial or mixed-use assets, a condition survey report that incorporates energy performance data is no longer optional — it is a lender expectation.

Practical Steps for Surveyors, Lenders, and Property Owners

The integration of EPC and net zero factors into upfront lender assessments requires coordinated action across the property transaction chain. Here is what each stakeholder should be doing in 2026:

🏦 For Lenders

- Update credit policy to reflect multi-metric EPC data from the reformed assessment framework

- Integrate GeoConnect or equivalent data into pre-application screening workflows

- Set explicit EPC thresholds for different product types (residential, BTL, commercial)

- Model retrofit cost scenarios as part of standard LTV and affordability calculations

🔍 For Surveyors and Valuers

- Upskill on the new multi-metric EPC system to provide accurate commentary in valuation reports

- Reference EPC data explicitly in condition and valuation reports, noting any discrepancies between assessed and likely actual performance [2]

- Flag MEES compliance risk as a material valuation consideration for all rented or investment properties

- Consider how choosing the right property assessment level affects the depth of energy performance commentary available to lenders

🏠 For Property Owners and Buyers

- Commission an up-to-date EPC before approaching lenders, especially for older stock

- Obtain retrofit cost estimates as part of pre-purchase due diligence

- Understand the difference between a property's current EPC rating and its likely rating under the new multi-metric system [1]

- Consider the long-term value impact of energy improvements — these are now directly linked to mortgage availability and pricing

- If purchasing a property that may require significant work, explore what a stock condition survey can reveal about the full scope of improvement needs

The Road Ahead: Resilience as a Core Valuation Principle

The convergence of EPC reform, MEES tightening, and net zero finance commitments means that energy and climate resilience are becoming as fundamental to property valuation as location and condition. The OECD's framework for future-proofing real estate investment makes clear that this is not a UK-specific trend — it is a global repricing of climate risk into asset values [4].

For the UK market specifically, the 2026 EPC reforms represent the moment when data-led resilience metrics move from the margins to the mainstream of lender decision-making. Properties that score well on fabric efficiency, carbon emissions, and net zero alignment will attract better financing terms. Those that do not will face a widening gap in both value and lendability.

The good news is that the tools to navigate this transition exist today. GeoConnect-style platforms, reformed EPC assessments, and a new generation of RICS-qualified surveyors trained in energy performance analysis are all part of an emerging ecosystem designed to make resilience measurable, comparable, and actionable.

Conclusion: Actionable Next Steps for 2026

Valuation Resilience Metrics for 2026: Incorporating EPC and Net Zero Factors in Upfront Lender Assessments is not a future challenge — it is a present-day operational requirement. The regulatory timeline is fixed, the data tools are available, and the market is already beginning to price in the difference between resilient and vulnerable assets.

Here are the most important actions to take right now:

- ✅ Lenders: Audit your current credit policy against the new multi-metric EPC framework and update LTV models to reflect MEES compliance risk.

- ✅ Surveyors: Ensure all valuation and condition reports explicitly address EPC ratings, retrofit costs, and MEES compliance timelines as material valuation factors.

- ✅ Property owners: Commission a current EPC assessment and obtain professional retrofit cost estimates before any sale, remortgage, or lease renewal.

- ✅ Buyers: Treat EPC ratings as a financial due diligence item, not a box-ticking exercise — the difference between EPC C and EPC E could affect your mortgage terms and future resale value.

- ✅ All stakeholders: Engage with GeoConnect and data-led pre-assessment tools to reduce friction, cut re-inspection costs, and build a more accurate picture of long-term asset resilience.

The properties and portfolios that thrive in the next decade will be those whose owners, lenders, and advisers treated energy performance as a core value driver — starting now.

References

[1] 2026 Changes To EPC Energy Efficiency Rules – https://enevo.co.uk/2026-changes-to-epc-energy-efficiency-rules/

[2] EPC Grades Or Actual Energy Use: Grappling With Net Zero Chalk And Cheese – https://www.gresb.com/nl-en/epc-grades-or-actual-energy-use-grappling-with-net-zero-chalk-and-cheese/

[3] Adaptation Resilience Corporate Engagement Priorities 2026 – https://www.iigcc.org/insights/adaptation-resilience-corporate-engagement-priorities-2026

[4] Managing Climate Related Risks For Resilient Real Estate – https://www.oecd.org/en/publications/2025/11/future-proofing-real-estate-investment_f3d78bbb/full-report/managing-climate-related-risks-for-resilient-real-estate_fe6a5ab0.html

[5] The Subtle Influence Of Energy Efficiency – https://www.dentons.com/en/insights/articles/2026/april/30/the-subtle-influence-of-energy-efficiency

[6] S2664328625000063 – https://www.sciencedirect.com/science/article/pii/S2664328625000063

[7] Why 2026 Is A Turning Point For Climate Risk – https://www.cotality.com/uk/insights/articles/why-2026-is-a-turning-point-for-climate-risk

[8] Reforms To The Energy Performance Of Buildings Regime – https://www.gov.uk/government/consultations/reforms-to-the-energy-performance-of-buildings-regime/reforms-to-the-energy-performance-of-buildings-regime

[9] Net Zero Company Benchmark – https://www.climateaction100.org/net-zero-company-benchmark/