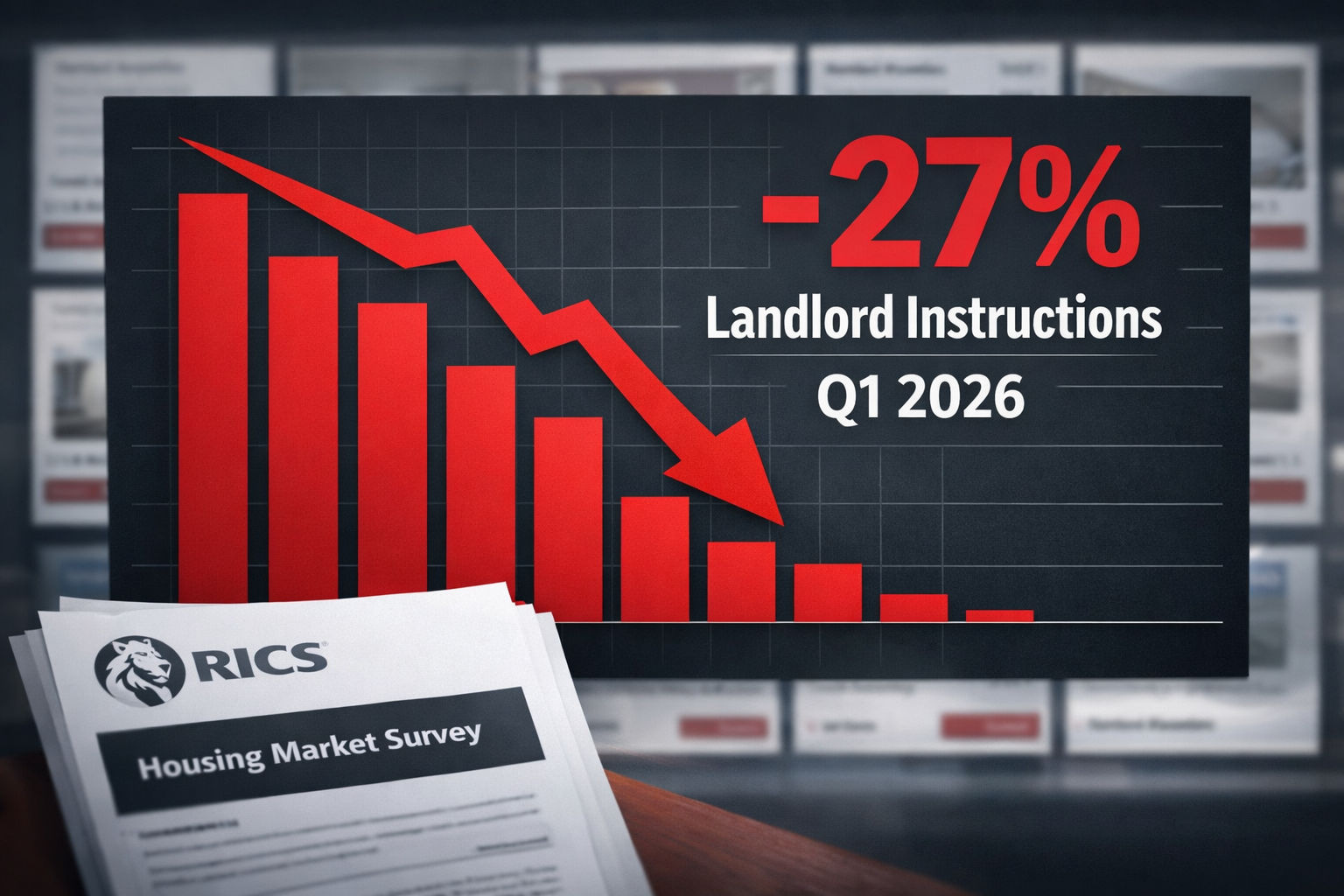

A single RICS survey figure stopped the UK property industry in its tracks in early 2026: landlord instructions had collapsed to -27%, the sharpest recorded net decline in new rental stock coming to market in recent memory. At the same moment, asking rents surged +20% over three months, and tenant demand — paradoxically — hit a six-year low [1]. This collision of shrinking supply, softening demand, and soaring rents is forcing surveyors, investors, and landlords to fundamentally rethink how Private Rented Sector (PRS) properties are valued. The Rental Market Supply Crisis and Valuation Adjustments: How -27% Landlord Instructions Reshape PRS Property Values in Spring 2026 is not an abstract market trend — it is a live recalibration event with direct consequences for every stakeholder in the lettings chain.

Key Takeaways 📌

- Landlord instructions fell to -27% in the February 2026 RICS survey, signalling acute rental stock withdrawal from the PRS.

- Rents rose +20% in three months, yet tenant demand simultaneously reached a six-year low — a paradox driven by affordability stress.

- Surveyors must adjust PRS valuations to account for reduced competition, tenant retention risk, and rising regulatory compliance costs.

- Regulatory pressure (energy efficiency standards, renters' reform legislation) is accelerating landlord exit and compressing net yields.

- Location-specific dynamics mean valuation adjustments vary significantly across London boroughs and regional markets.

Understanding the -27% Landlord Instructions Figure

The -27% net balance recorded in the RICS February 2026 Residential Market Survey represents the percentage of surveying professionals reporting a fall in new landlord instructions minus those reporting a rise. In plain terms: far more surveyors and letting agents across the UK are seeing landlords pull properties from the rental market than are seeing new stock arrive [1].

Why Are Landlords Leaving the PRS?

Several converging pressures are driving this exit:

| Pressure Factor | Impact on Landlord Behaviour |

|---|---|

| Section 24 mortgage interest relief removal | Reduced net yields, especially for leveraged landlords |

| Renters' Reform Act (2026 provisions) | Increased perceived risk of tenant disputes and eviction complexity |

| EPC upgrade requirements | Capital expenditure demands on older stock |

| Capital Gains Tax changes | Incentivising early exit before further rate adjustments |

| Rising insurance and maintenance costs | Eroding cash flow margins |

"The landlord exodus is not a single-cause event — it is the cumulative weight of a decade of regulatory and fiscal change finally tipping the scales."

This structural withdrawal is not temporary volatility. Many landlords are selling into the owner-occupier market or converting properties to short-term lets, permanently removing stock from the PRS. The result is a supply crisis that professional valuers can no longer treat as background noise in their assessments.

For buyers considering acquiring former rental properties, understanding the full condition of a property is critical. A homebuyers report or building survey can reveal deferred maintenance that landlords leaving the sector may have postponed.

The Paradox: Six-Year Low Demand Meets a Supply Crisis

The counterintuitive headline from Q1 2026 data is that tenant demand has fallen to its lowest point in six years — even as supply contracts sharply [1]. How can demand fall while rents rise 20%?

The answer lies in affordability-driven demand destruction:

- 🏠 Renters priced out of the PRS are moving into shared accommodation, returning to family homes, or relocating to lower-cost regions.

- 📉 The pool of active rental applicants shrinks as rents outpace wage growth.

- 🔄 Some former renters have accelerated first-time buyer purchases, further reducing the active tenant pool.

This creates a deceptive market signal. Fewer tenants competing for fewer properties can look like a balanced market on the surface — but the underlying dynamics are far more fragile. Vacancy periods, when they occur, are lengthening in certain sub-markets. Tenant quality (in terms of affordability and creditworthiness) is becoming a more acute concern for remaining landlords.

What This Means for Rental Yield Calculations

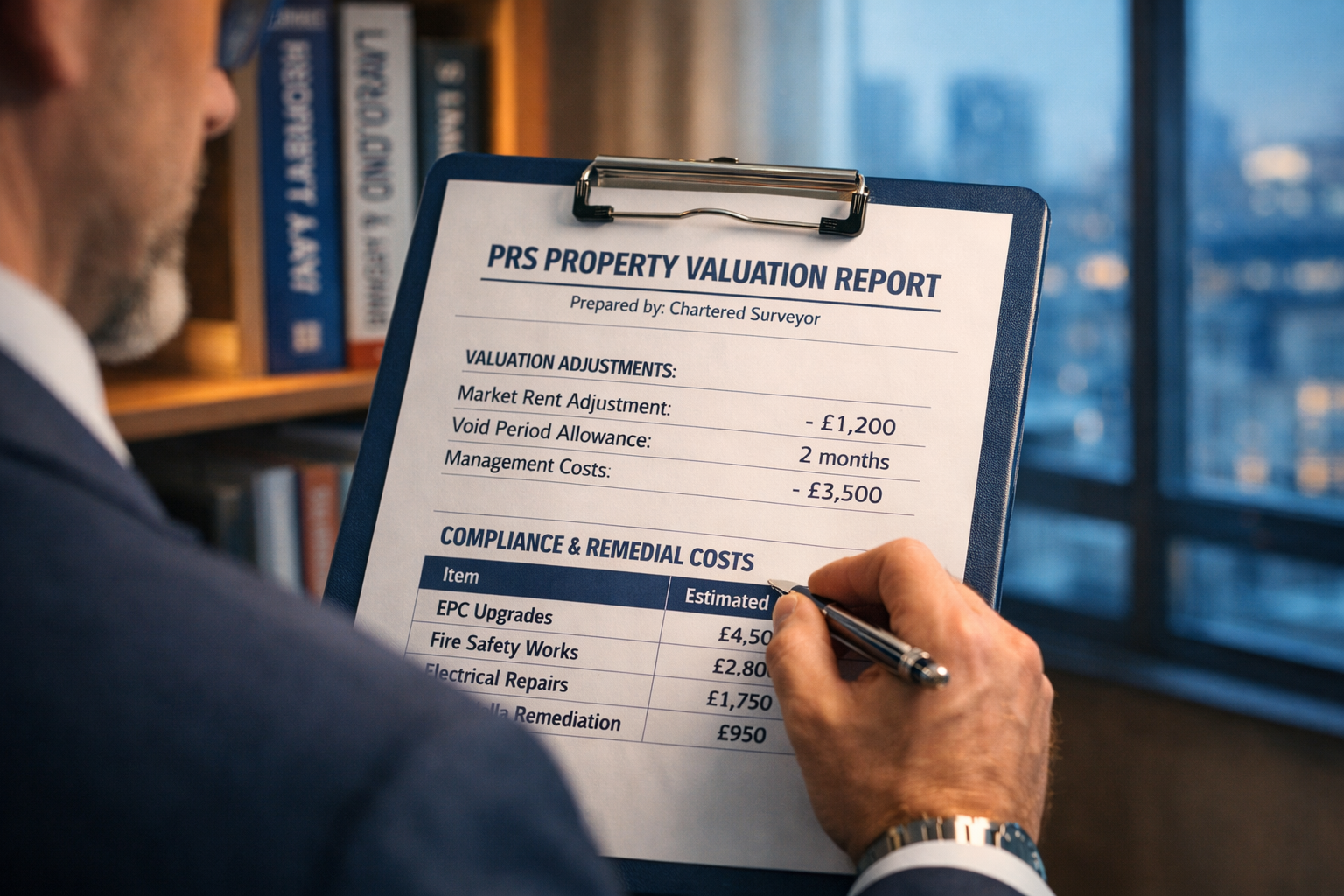

Traditional yield calculations based on gross rental income are increasingly misleading in spring 2026. Surveyors conducting property valuations must now incorporate:

- Void period risk adjustments — even in constrained markets, tenant turnover is more costly when replacement tenants are fewer.

- Rent achievability stress testing — headline asking rents may not reflect achievable rents for specific property types or locations.

- Compliance cost deductions — EPC Band C upgrade costs, licensing fees, and safety certification expenses must be netted against income projections.

- Tenant retention premiums — properties with sitting tenants on reasonable rents may carry a valuation premium over vacant possession in certain contexts.

How the Rental Market Supply Crisis and Valuation Adjustments Affect PRS Property Values in Spring 2026

The Rental Market Supply Crisis and Valuation Adjustments: How -27% Landlord Instructions Reshape PRS Property Values in Spring 2026 plays out differently depending on property type, location, and the intended use of the valuation.

Investment Valuation vs. Mortgage Valuation

There is a growing divergence between how investment buyers and mortgage lenders are approaching PRS property values:

Investment buyers are pricing in the scarcity premium — fewer rental properties means stronger rental income for those who remain in the market. Some are paying above traditional yield thresholds because they anticipate continued rent growth.

Mortgage lenders and their panel surveyors, however, are applying more conservative assumptions. Lenders are stress-testing rental income at lower levels to account for:

- Potential rent control legislation

- Increased regulatory compliance costs

- The possibility of further demand softening

This divergence is creating valuation gaps — situations where a buyer's perceived value exceeds the surveyor's formal assessment. For anyone navigating this environment, understanding what to do when your property offer has been accepted is an important step before proceeding to formal valuation.

Regional Valuation Adjustment Patterns in Spring 2026

The supply crisis is not uniform across the UK. London's inner boroughs are experiencing the most acute stock withdrawal, but the valuation implications differ by location:

Inner London (e.g., Knightsbridge, Marylebone, Chelsea):

- High-value PRS stock is being converted to owner-occupation or short-term lets

- Remaining rental stock commands significant premiums

- Surveyors in Knightsbridge and Marylebone are factoring scarcity uplift into investment valuations

Outer London (e.g., Merton, Wandsworth, Richmond):

- Mid-market rental stock withdrawal is acute

- Demand remains stronger relative to supply than in prime areas

- Surveyors in Merton and Wandsworth are seeing robust rental evidence but applying compliance cost deductions

East London and commuter zones (e.g., Ilford, Redbridge):

- Affordability constraints are most visible here — demand destruction is sharpest

- Surveyors in Ilford and Redbridge are applying more cautious yield assumptions

Regulatory Compliance Costs: The Hidden Valuation Drag

One factor that many informal property assessments overlook is the growing cost of regulatory compliance for PRS landlords. In spring 2026, these costs are material enough to require explicit treatment in formal valuations.

Key Compliance Cost Categories

- EPC Band C upgrades: Older properties requiring insulation, boiler replacement, or double glazing can face costs of £5,000–£25,000+ depending on the starting EPC rating.

- Electrical Installation Condition Reports (EICRs): Mandatory five-yearly inspections with remediation costs.

- Selective and Additional Licensing: Many London boroughs have expanded licensing schemes, adding annual fees and compliance requirements.

- Fire safety upgrades: Post-Grenfell regulations continue to impose costs on leasehold and flatted PRS stock.

"A property that looks attractive on gross yield may deliver a net yield well below the cost of capital once compliance expenditure is properly accounted for."

For leasehold PRS properties specifically, understanding the lease structure is critical to assessing long-term investment viability. Resources on informal lease extension advantages and disadvantages are particularly relevant for landlords holding flats with shorter lease terms.

Surveyors conducting formal valuations of PRS assets in 2026 are increasingly expected to:

✅ Identify compliance deficiencies visible during inspection

✅ Estimate remediation cost ranges

✅ Adjust the income approach valuation to reflect net rather than gross yield

✅ Flag regulatory risk as a material factor in the valuation narrative

Valuation Adjustments: A Framework for Surveyors and Investors

The Rental Market Supply Crisis and Valuation Adjustments: How -27% Landlord Instructions Reshape PRS Property Values in Spring 2026 demands a structured analytical approach. Below is a practical framework for adjusting PRS valuations in the current environment.

Step 1: Establish Gross Rental Income (GRI)

Use current market evidence — not headline asking rents. In many sub-markets, achieved rents are running 5–10% below asking rents as tenant affordability limits are reached. Cross-reference with local letting agent data and RICS rental evidence.

Step 2: Apply Void and Management Deductions

- Standard void allowance: 4–8 weeks per annum (adjust upward in lower-demand sub-markets)

- Management fees: 10–15% of GRI including VAT

- Maintenance and repairs reserve: 1–2% of property value per annum

Step 3: Deduct Compliance Costs

Amortise identified compliance expenditure over a reasonable period (typically 5–10 years) and deduct the annual equivalent from net income.

Step 4: Apply the Appropriate Yield

Current market yields for PRS properties in spring 2026 vary significantly:

| Location Type | Gross Yield Range | Net Yield (Post-Compliance) |

|---|---|---|

| Prime Inner London | 3.0–4.5% | 2.0–3.2% |

| Outer London | 4.5–6.0% | 3.2–4.5% |

| Commuter Zones | 5.5–7.5% | 4.0–5.8% |

| Regional Cities | 6.0–9.0% | 4.5–7.0% |

Step 5: Sense-Check Against Comparable Sales

The income approach must be reconciled with comparable sales evidence. In markets where former PRS properties are selling to owner-occupiers, the vacant possession value may exceed the investment value — a critical distinction for valuation purposes.

What Surveyors, Landlords, and Investors Should Do Now

The spring 2026 PRS market requires active responses from all stakeholders — not a wait-and-see approach.

For Surveyors 🔍

- Update comparable rental evidence databases quarterly — the market is moving faster than annual review cycles.

- Explicitly address compliance costs in valuation reports rather than treating them as footnotes.

- Consider requesting homebuyers report examples as a reference when structuring condition assessments for PRS acquisitions.

- Engage with RICS guidance on PRS-specific valuation methodology as it evolves.

For Landlords 🏠

- Commission a professional condition survey before making exit decisions — deferred maintenance may be suppressing the sale price unnecessarily.

- Assess EPC upgrade costs against the rental income uplift a compliant property can command — the business case for staying may be stronger than anticipated.

- Review lease terms on any leasehold holdings; short leases create compounding valuation risk.

For Investors and Buyers 💼

- Do not rely on gross yield figures alone — insist on net yield analysis inclusive of compliance costs.

- Prioritise properties with strong EPC ratings (Band C or above) to minimise near-term capital expenditure.

- Seek local surveying expertise in target acquisition areas; a surveyor with deep knowledge of Richmond or Bromley will provide materially better-calibrated valuations than a generalist.

- Factor in the possibility that rents plateau or soften in 2026–2027 as affordability constraints deepen — build downside scenarios into investment models.

Conclusion: Navigating the Supply Crisis with Accurate Valuations

The -27% landlord instructions figure is not just a market statistic — it is a structural signal that the PRS is contracting, and that the valuations underpinning investment decisions, mortgage lending, and asset management must adapt accordingly. The Rental Market Supply Crisis and Valuation Adjustments: How -27% Landlord Instructions Reshape PRS Property Values in Spring 2026 represents a genuine inflection point: properties that were straightforward income investments two years ago now require nuanced, compliance-aware, location-specific valuation analysis [1].

Actionable next steps:

- ✅ Commission a professional PRS valuation from a chartered surveyor with current local market knowledge before buying, selling, or refinancing any rental property in 2026.

- ✅ Audit your existing portfolio for EPC compliance gaps and model the cost of upgrades against projected rental income.

- ✅ Stress-test rental income assumptions using net rather than gross yield figures, incorporating realistic void periods and compliance costs.

- ✅ Monitor RICS quarterly survey data — the landlord instructions balance is a leading indicator of supply conditions that will directly affect achievable rents and capital values.

- ✅ Seek specialist advice in your target geography — local surveyors with PRS expertise will provide the most accurate valuation adjustments in this rapidly evolving market.

The landlords and investors who treat the current supply crisis as a temporary disruption risk making valuation errors with long-term financial consequences. Those who engage with the structural reality — and commission rigorous, compliance-aware valuations — will be far better positioned for the PRS landscape of 2026 and beyond.

References

[1] Lettings Tenant Demand Uptick Valuation Surveys For Constrained Rental Supply In Q1 2026 – https://nottinghillsurveyors.com/blog/lettings-tenant-demand-uptick-valuation-surveys-for-constrained-rental-supply-in-q1-2026