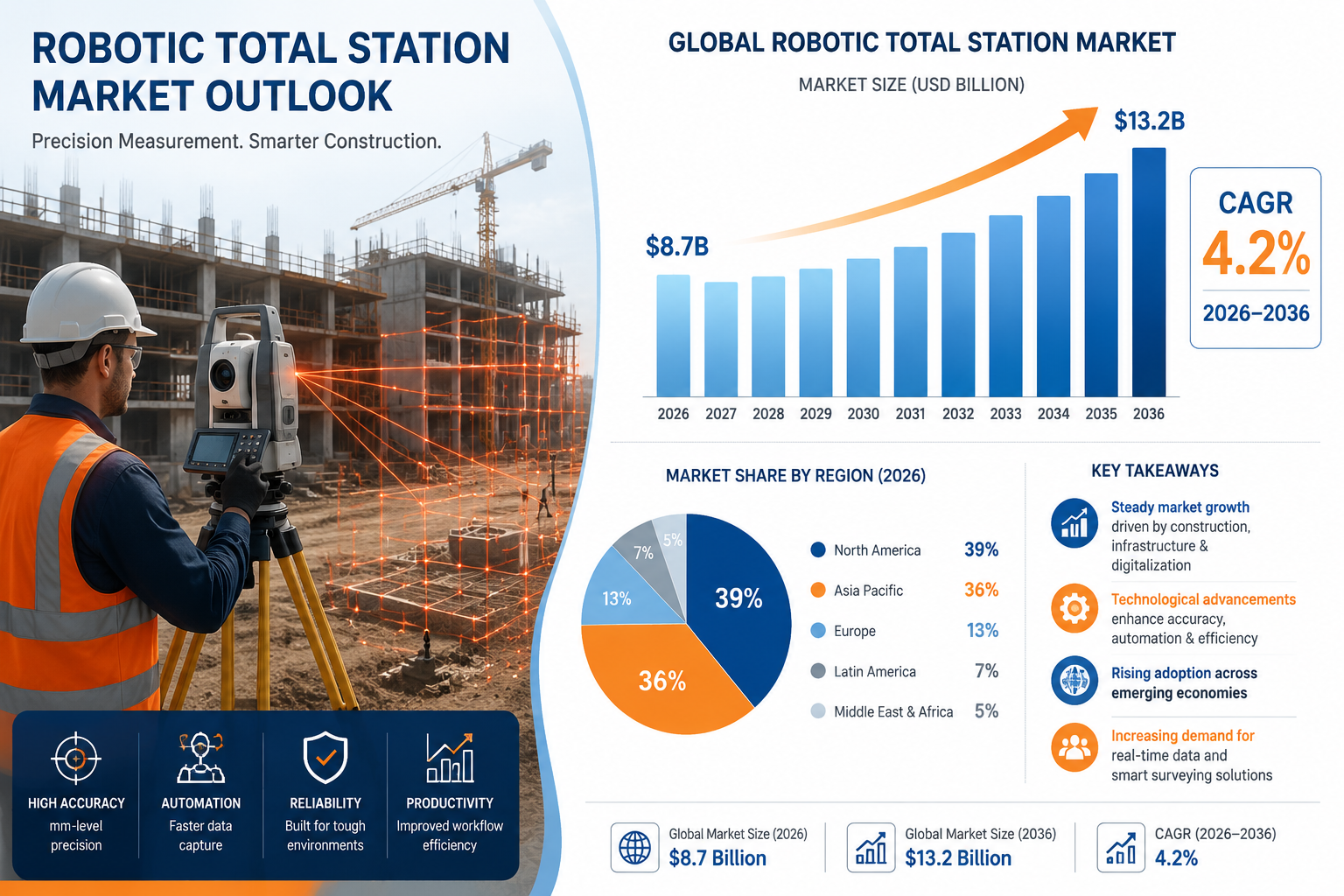

Global spending on land survey equipment crossed the USD 10 billion threshold in 2026 — and analysts project it will not stop climbing until it reaches USD 15.21 billion by 2034, advancing at a compound annual growth rate of 5.01% [1]. That trajectory is not driven by incremental upgrades to traditional theodolites. It is being shaped by a convergence of UAV mapping platforms, 3D laser scanning, GNSS receivers, and geographic information systems (GIS) arriving at precisely the moment when governments worldwide are committing record infrastructure budgets. The Booming Land Survey Equipment Market: Key Technologies Driving Growth to 2036 represents one of the most consequential shifts in geospatial technology in a generation.

Key Takeaways

- The global land survey equipment market is projected to grow from USD 10.29 billion in 2026 to USD 15.21 billion by 2034, driven by infrastructure investment and technological adoption [1].

- UAV-based aerial mapping has cut survey time by more than 50%, accelerating adoption across construction, mining, and utilities [4].

- Total stations remain the single largest product segment, holding a 38.4% market share in 2026 [3].

- North America leads with a 39.26% regional share, while Asia Pacific is the fastest-growing region at 35.9% of the overall market [1].

- The services segment — covering subscription workflows and continuous data analytics — is forecast to grow at a 10.8% CAGR through 2030, outpacing hardware growth [5].

Market Size, Regional Dynamics, and the Forces Behind the Boom

The numbers behind The Booming Land Survey Equipment Market: Key Technologies Driving Growth to 2036 tell a story of sustained structural demand rather than a short-lived cycle. In 2026, North America holds the dominant regional position with a 39.26% market share, underpinned by large-scale highway, rail, and utility corridor projects funded through federal infrastructure legislation [1]. The Asia Pacific region is close behind at 35.9%, with urbanisation in China, India, and Southeast Asia generating continuous demand for cadastral surveys, topographic mapping, and construction layout [2].

What is driving this growth at the macro level?

- Rapid urbanisation requiring precise land assessments for city planning and infrastructure development [2]

- A global surge in commercial construction projects demanding accurate pre-construction surveys [2]

- Expanding renewable energy installations — wind farms and solar parks require detailed terrain analysis

- Government mandates for digital land registries and updated cadastral databases

- Growing adoption of geographic information systems (GIS) across both public and private sector projects

The commercial segment dominated end-use in 2025, reflecting how extensively developers and contractors rely on survey data throughout the project lifecycle — from site selection and feasibility through to handover and asset management [2]. Meanwhile, the inspection application segment held the largest share of activity, confirming that monitoring and condition assessment have become core, ongoing functions rather than one-off exercises [2]. This aligns directly with how monitoring surveys are now embedded into long-term asset management programmes for large structures.

"Rapid urbanisation is fuelling demand for land survey equipment, as expanding cities require continuous and precise land assessments for planning and infrastructure development." — Grand View Research [2]

Hardware Still Dominates, But Services Are Accelerating

In 2024, the hardware segment accounted for 60.4% of total market revenue, confirming that physical instruments — total stations, GNSS receivers, laser scanners, and UAV platforms — remain the core commercial proposition [5]. However, the most significant growth story sits in the services layer. Subscription-based data workflows, cloud-hosted point cloud processing, and continuous analytics platforms are projected to grow at a 10.8% CAGR through 2030 [5]. This mirrors a broader pattern across the technology sector: hardware opens the door, but recurring software and services revenue drives long-term enterprise value.

Key Technologies Reshaping the Survey Equipment Landscape

Understanding The Booming Land Survey Equipment Market: Key Technologies Driving Growth to 2036 requires a clear-eyed look at the specific instruments and platforms that are redefining what is possible in the field. Four technology categories stand out.

1. Total Stations: The Enduring Backbone

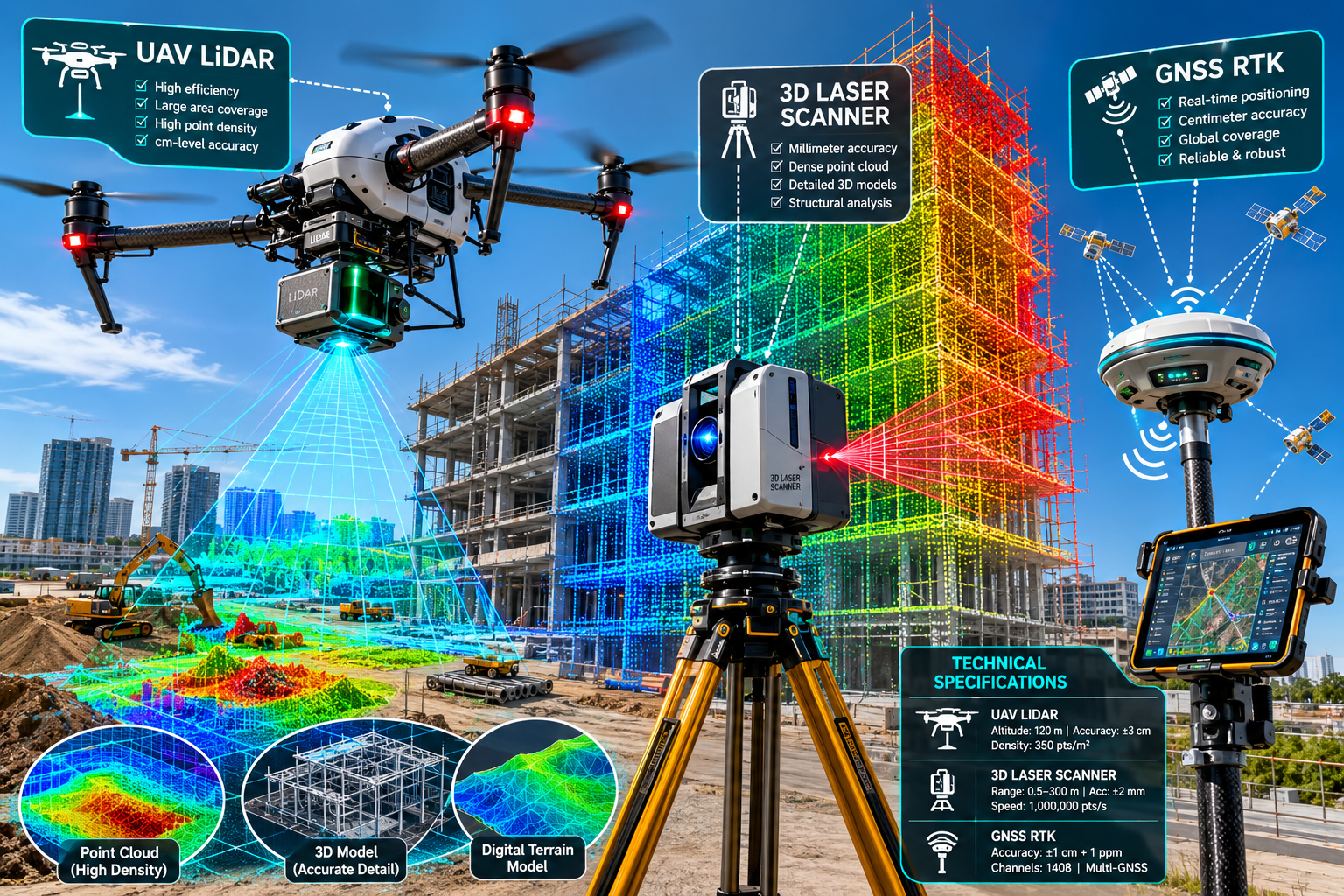

Despite competition from newer platforms, total stations retained the largest single product segment share at 38.4% in 2026 [3]. Modern robotic total stations combine electronic distance measurement, motorised aiming, and onboard data processing into a single instrument capable of sub-millimetre precision. They remain indispensable for high-precision layout, control network establishment, and deformation monitoring on critical infrastructure. Their dominance reflects a market reality: accuracy requirements on construction sites and in legal boundary determinations cannot be compromised, and no other technology yet matches total stations for close-range, high-stakes measurement.

2. GNSS and RTK Systems: Speed Meets Precision

Global Navigation Satellite System (GNSS) receivers — particularly Real-Time Kinematic (RTK) configurations — have transformed fieldwork productivity. Where traditional static GPS surveys required hours of observation, modern RTK systems deliver centimetre-level accuracy in seconds. Network RTK, which uses a web of reference stations to correct atmospheric errors in real time, has extended reliable coverage into challenging urban and semi-urban environments. For professionals working on construction surveying projects, GNSS RTK has become the default tool for topographic data collection and machine control guidance.

3. UAVs and Drone Mapping: The 50% Time Reduction

The adoption of unmanned aerial vehicles (UAVs) for aerial mapping has been one of the most disruptive developments in geospatial practice. Drone-based photogrammetry and LiDAR payloads can now survey hundreds of hectares in a single flight, with the resulting point clouds and orthomosaic images processed into survey-grade deliverables within hours. Critically, this approach has reduced survey time by over 50% compared to conventional ground-based methods, a productivity gain that has driven rapid adoption across construction, mining, agriculture, and utilities [4]. As regulatory frameworks for beyond-visual-line-of-sight (BVLOS) operations mature, UAV coverage will extend further into remote and hazardous environments.

Comparing the three primary field technologies:

| Technology | Primary Strength | Typical Accuracy | Best Application |

|---|---|---|---|

| Total Station | Sub-mm precision | 1-3 mm | Layout, control networks |

| GNSS RTK | Speed and coverage | 10-20 mm | Topographic surveys, machine control |

| UAV / LiDAR | Area coverage | 20-50 mm | Large-area mapping, inspection |

| 3D Laser Scanner | Dense point capture | 2-6 mm | As-built, heritage, structural |

4. 3D Laser Scanning: The Point Cloud Revolution

Terrestrial and mobile 3D laser scanners capture millions of measurement points per second, producing dense point clouds that can be processed into precise 3D models, cross-sections, and as-built drawings. This technology has transformed workflows in heritage documentation, tunnel inspection, and building information modelling (BIM). The integration of laser scanning with topographic mapping workflows has significantly reduced the time required to produce accurate site models for complex brownfield redevelopment projects. For property professionals, the ability to generate precise as-built data feeds directly into stock condition surveys and structural assessments.

5. GIS Integration and Data Analytics

The final piece of the technology puzzle is the analytical layer. GIS platforms aggregate, visualise, and interrogate the spatial data produced by all the hardware categories above. The integration of machine learning into GIS workflows is enabling automated feature extraction from point clouds and drone imagery, reducing post-processing time dramatically. Cloud-based GIS platforms allow survey data to be shared in real time across project teams, clients, and regulatory bodies — a capability that is reshaping how land boundary disagreements and planning disputes are evidenced and resolved.

Competitive Landscape, Challenges, and the Road to 2036

The land survey equipment market exhibits medium concentration, with three companies — Trimble Inc., Hexagon AB, and Topcon Corporation — commanding the largest shares [5]. These firms compete across hardware, software, and services, and have each made significant acquisitions to build integrated platform offerings. Leica Geosystems (part of Hexagon), Topcon, and Trimble have all invested heavily in cloud connectivity and machine control ecosystems, recognising that the future competitive battleground is data management rather than instrument optics alone.

Market Challenges Worth Noting

The growth trajectory is real, but it is not without friction:

- High initial capital costs for advanced instruments remain a barrier for smaller surveying firms and contractors in emerging markets

- Skilled operator shortages — the ability to collect data with a drone is far more common than the ability to process and quality-assure the resulting point cloud

- Regulatory complexity around UAV operations varies significantly across jurisdictions, creating compliance overhead

- Cybersecurity concerns as survey data increasingly flows through cloud infrastructure

- Interoperability gaps between hardware from different manufacturers and GIS platforms

Despite these headwinds, the structural demand drivers — urbanisation, infrastructure investment, and the digitisation of land records — are strong enough to sustain the projected growth through 2036.

What the Services Growth Signals

The projected 10.8% CAGR for the services segment through 2030 [5] is arguably the most strategically significant data point in the market. It signals that clients are moving away from one-off survey commissions toward continuous monitoring and data subscription models. This is already visible in sectors such as rail infrastructure, where track geometry monitoring is shifting from periodic manual surveys to continuous automated measurement. For property professionals, this trend mirrors the growing demand for ongoing property condition assessment services rather than single-point-in-time inspections.

Regional Opportunities to 2036

| Region | 2026 Share | Growth Driver |

|---|---|---|

| North America | 39.26% | Federal infrastructure funding, smart city projects |

| Asia Pacific | 35.9% | Rapid urbanisation, industrial expansion |

| Europe | Significant | Brownfield redevelopment, BIM mandates |

| Middle East & Africa | Emerging | Mega-project construction, land registration |

| Latin America | Emerging | Agricultural land management, mining |

The Asia Pacific region's combination of scale and speed of urbanisation makes it the most dynamic growth market over the forecast period. Countries such as India, Indonesia, and Vietnam are simultaneously expanding their urban footprints and modernising their land administration systems — both of which require substantial survey activity [2].

Implications for Property and Construction Professionals in 2026

The market dynamics described above have direct, practical implications for anyone commissioning or delivering survey services in 2026. As survey technology becomes more capable, client expectations for accuracy, turnaround time, and data richness are rising in parallel. A drone-based topographic survey that would have taken a week using traditional methods can now be completed in a day — and clients are beginning to expect that speed as standard.

For property professionals, the growing sophistication of survey technology also raises the bar for what constitutes an adequate pre-purchase or pre-development investigation. Whether the need is for a homebuyers survey or full structural assessment, the underlying data quality that informs those reports is improving year on year. Similarly, specific defect surveys can now be supported by thermal imaging and 3D scan data that provides far more objective evidence of structural behaviour than visual inspection alone.

The integration of advanced survey data into legal and commercial processes is also accelerating. Point cloud models and georeferenced drone imagery are increasingly accepted as evidence in planning appeals, boundary disputes, and dilapidations claims — making the quality of the underlying survey data a matter of legal as well as technical significance.

Practical steps for professionals engaging with the evolving survey market:

- Specify the required accuracy standard and deliverable format clearly before commissioning any survey

- Ask providers about their data processing workflows and quality assurance procedures

- Consider whether a monitoring or subscription-based survey model is more appropriate than a one-off commission for long-term assets

- Ensure survey data is stored in formats compatible with your GIS or BIM platform

- Verify that drone operators hold appropriate regulatory authorisations for the survey area

Conclusion

The Booming Land Survey Equipment Market: Key Technologies Driving Growth to 2036 is being propelled by a rare alignment of factors: unprecedented infrastructure investment, the maturation of transformative technologies, and the digitisation of land and property records across both developed and emerging economies. The market's growth from USD 10.29 billion in 2026 toward USD 15.21 billion by 2034 is not speculative — it reflects committed government spending programmes, accelerating commercial construction pipelines, and the proven productivity gains delivered by UAVs, 3D laser scanners, and integrated GNSS systems [1].

For property and construction professionals, the actionable response is threefold. First, engage with survey providers who have invested in modern technology platforms and can demonstrate the accuracy and traceability of their data. Second, recognise that survey data is increasingly a long-term asset — not a one-off deliverable — and plan data management accordingly. Third, stay informed about how evolving survey capabilities are changing the standard of care expected in property transactions, planning applications, and asset management. The technology is advancing rapidly; professional practice must keep pace.

References

[1] Land Survey Equipment Market 103329 – https://www.fortunebusinessinsights.com/land-survey-equipment-market-103329/?utm_source=openai

[2] Land Survey Equipment Market Report – https://www.grandviewresearch.com/industry-analysis/land-survey-equipment-market-report?utm_source=openai

[3] 2026 Land Survey Equipment Boom Comparing Total Stations Gps Rtk And Laser Scanners – https://princesurveyors.co.uk/blog/2026-land-survey-equipment-boom-comparing-total-stations-gps-rtk-and-laser-scanners/?utm_source=openai

[4] Land Survey Equipment Market 109381 – https://www.globalgrowthinsights.com/market-reports/land-survey-equipment-market-109381?utm_source=openai

[5] Land Survey Equipment Market – https://www.mordorintelligence.com/industry-reports/land-survey-equipment-market?utm_source=openai