Roughly 1.5 million homes across the UK are classified as non-standard construction — a figure that surprises many buyers, sellers, and even some lenders who assume the majority of the housing stock is built from brick and mortar [1]. For surveyors, understanding how to identify these properties, assess their condition, and communicate their value accurately is one of the most demanding professional challenges in 2026. This guide to Valuing UK Properties with Significant Non-Standard Construction: PRC, Timber Frames, BISF and More in 2026 sets out a structured approach: how to identify each construction type, how construction affects mortgageability and marketability, and how valuation surveyors should evidence and explain their methodology in formal reports.

Key Takeaways

- Non-standard construction covers a wide range of property types including PRC, BISF steel frame, timber frame, and in-situ concrete homes, many built after World War II to address urgent housing shortages.

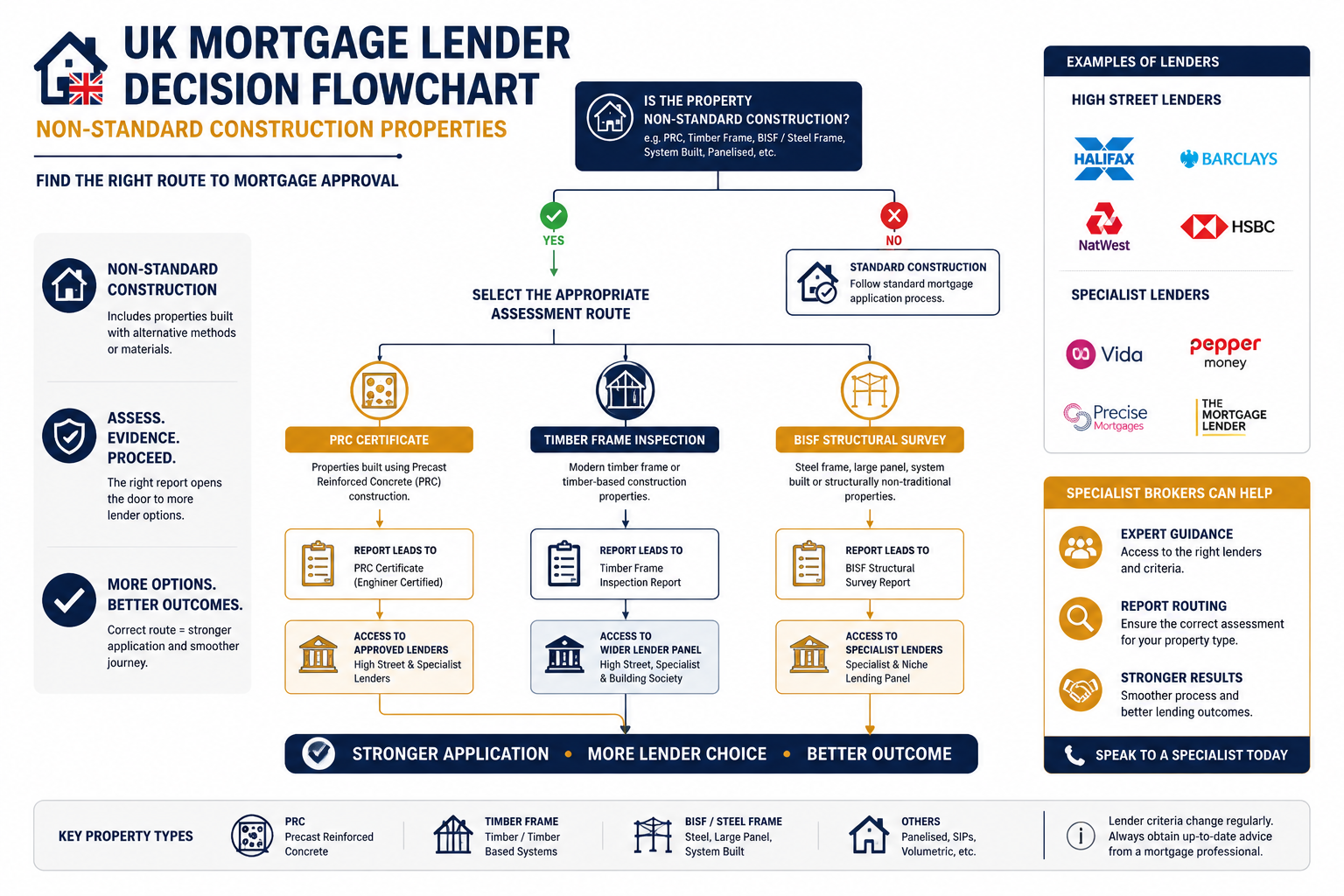

- Mortgage lenders apply significantly stricter criteria to non-standard properties, and some types — particularly unrepaired PRC homes — are effectively unmortgageable without a structural repair certificate.

- A specialist building survey is essential before purchasing any non-standard construction property, as defects such as corrosion, rot, and moisture penetration can be hidden behind cladding or render.

- Insurance premiums are typically higher for non-standard homes, and some insurers will decline cover altogether without specialist underwriting.

- Surveyors must clearly document construction type, condition, comparable evidence, and any adjustments to value in their reports to satisfy both lender requirements and RICS standards.

What Is Non-Standard Construction and Why Does It Matter in 2026

A property is considered non-standard when its walls, roof, or structural frame deviate from the conventional brick-and-block or stone construction with a pitched tile or slate roof that most UK lenders regard as acceptable security. The category is broad and includes:

- Prefabricated Reinforced Concrete (PRC) — including Airey, Cornish Unit, Reema, Wates, and Woolaway types

- British Iron and Steel Federation (BISF) steel-framed houses

- Timber frame construction — both modern engineered systems and older post-war types

- Wimpey No-Fines concrete — in-situ poured concrete without fine aggregate

- System-built and large panel system (LPS) blocks of flats

- Thatched, flat-roofed, and single-skin brick properties

The historical context matters. After World War II, the UK faced a severe housing shortage and constructed approximately 1.5 million homes using non-traditional methods to speed up delivery [7]. Many of those properties remain in use today, concentrated in former council estates across London, the Midlands, and the North. In 2026, they continue to change hands — often at a discount — and continue to present complex valuation challenges.

Identifying the Main Non-Standard Construction Types

Accurate identification is the foundation of any competent valuation. Misidentifying a BISF house as standard brick construction, for example, would invalidate the entire assessment.

PRC Houses

PRC homes were mass-produced using precast concrete panels or frames. Key identification features include:

- Visible vertical or horizontal panel joints on external walls

- Render applied over panels (often concealing the underlying structure)

- Uniform window and door openings reflecting factory production

- Common types: Airey (concrete post and slab), Cornish Unit (concrete panel), Reema Hollow Panel, Wates

PRC homes designated under the Housing Defects Act 1984 are formally listed as defective. Without a structural repair certificate from an approved scheme, they are widely considered unmortgageable [2]. Surveyors must check the NHBC or relevant approved contractor documentation before proceeding.

BISF Houses

BISF properties are identifiable by a distinctive two-storey appearance: a rendered or pebble-dashed ground floor with a steel-framed upper storey clad in profiled metal sheeting [8]. They were built between 1946 and the early 1950s and are common in suburban areas across England and Wales.

Key risks include:

- Corrosion of the steel frame, particularly at ground-floor junctions

- Deterioration of the metal cladding on the upper floor

- Thermal bridging and condensation within the wall construction

Lenders typically require a detailed structural survey before offering a mortgage on a BISF property [3].

Timber Frame Properties

Modern timber frame homes — built since the 1980s using engineered panel systems — are generally accepted by mainstream lenders and present fewer valuation complications. Older timber frame properties, particularly those from the 1960s and 1970s, are more problematic. Issues include:

- Rot and decay in structural members where moisture has penetrated

- Fire risk concerns, especially where cavity barriers are absent or degraded

- Difficulty distinguishing structural from non-structural elements without intrusive investigation

The cost of remedying damp and timber problems in older timber frame homes can be substantial and must be factored into any valuation adjustment.

Wimpey No-Fines and In-Situ Concrete

Wimpey No-Fines homes were built by pouring concrete without fine aggregate directly into shuttering on site. The result is a porous wall that is susceptible to moisture penetration over time [5]. They are often rendered externally, making identification difficult without knowledge of the estate's history or access to local authority records.

How Non-Standard Construction Affects Mortgageability and Marketability

Understanding the mortgage landscape is critical when Valuing UK Properties with Significant Non-Standard Construction: PRC, Timber Frames, BISF and More in 2026, because mortgageability directly drives market value.

Lender Attitudes in 2026

High street banks apply the strictest criteria. Many will decline non-standard properties outright, particularly:

- Unrepaired PRC-designated homes

- Properties with flat roofs covering more than 30% of the floor area

- Single-skin brick or non-cavity wall construction

- BISF homes with evidence of frame corrosion

Building societies and specialist lenders offer more flexibility but typically charge higher interest rates to reflect the perceived risk [6]. The practical effect is that a non-standard property draws from a smaller pool of potential buyers — only those who can access specialist finance or purchase with cash. This reduced demand directly suppresses market value.

| Construction Type | Mainstream Lender Acceptance | Specialist Lender Required | Typically Unmortgageable |

|---|---|---|---|

| Modern timber frame | Yes | No | No |

| BISF (good condition) | Sometimes | Often | Rarely |

| BISF (poor condition) | No | Sometimes | Sometimes |

| PRC (repaired, certified) | Sometimes | Often | No |

| PRC (unrepaired) | No | Rarely | Yes |

| Wimpey No-Fines | Sometimes | Often | Rarely |

| Older timber frame | Sometimes | Often | Rarely |

Insurance Implications

Non-standard construction properties frequently attract higher building insurance premiums. Timber frame and thatched properties in particular may face difficulty obtaining standard cover, with some insurers requiring specialist underwriting [4]. Surveyors should note insurance implications in their reports, as they represent an ongoing cost that affects affordability and therefore value.

The Impact on Market Value

A surveyor cannot simply apply a blanket percentage discount for non-standard construction. The adjustment must be evidenced. Relevant factors include:

- Local market activity: Are there comparable sales of the same construction type in the area?

- Condition: A well-maintained, repaired, and certified PRC home is materially different from an unrepaired one.

- Demand: In some areas with high concentrations of BISF or No-Fines stock, the local market has normalised these types and the discount is modest.

- Remediation costs: Where structural defects are present, the cost of repair must be quantified and deducted.

For a Red Book valuation — required for mortgage lending, probate, or legal proceedings — the surveyor must demonstrate that the figure reflects what a willing buyer would pay in the open market with full knowledge of the construction type and its implications.

The Surveyor's Role: Evidencing and Explaining the Valuation Approach

The most common complaint against surveyors in non-standard construction cases is not that they got the number wrong, but that they failed to explain their reasoning. A robust report must do three things: identify the construction type with precision, assess the condition of the non-standard elements, and justify any value adjustment with comparable evidence.

Identification and Description

The report should name the construction type specifically — not just "non-standard construction" — and describe the identifying features observed during inspection. Where identification is uncertain, the surveyor should state this clearly and recommend further specialist investigation. Access to local authority records, estate agent knowledge, and databases such as the NHBC register can assist identification.

Condition Assessment

A building condition assessment for non-standard properties should address:

- The current condition of structural elements (frame, panels, cladding)

- Evidence of moisture penetration, corrosion, or biological decay

- The presence and condition of any previous repair works

- Compliance with current building regulations where alterations have been made

Where the surveyor cannot access concealed elements — for example, the steel frame within a BISF wall — this limitation must be explicitly stated, and a recommendation for specialist structural investigation should be made.

Comparable Evidence and Value Adjustment

The valuation must be anchored in market evidence. Surveyors should:

- Search for sales of the same construction type in the same locality within the last 12 months

- Where direct comparables are unavailable, use standard construction comparables and apply a reasoned adjustment

- Document the adjustment percentage and the rationale behind it

- Note any conditions that could affect future saleability, such as the absence of a PRC repair certificate

"A valuation of a non-standard construction property that lacks a clear explanation of the construction type, its defects, and the comparable evidence used is not fit for purpose — regardless of whether the final figure is accurate."

For properties in areas such as Croydon, Woolwich, or Newham — where post-war non-standard housing is prevalent — local surveyors will often have a stronger comparable database to draw from than those working in areas where these property types are rare.

Practical Guidance for Buyers, Sellers, and Lenders in 2026

Valuing UK Properties with Significant Non-Standard Construction: PRC, Timber Frames, BISF and More in 2026 requires all parties to understand their responsibilities and the information they need.

For Buyers

- Always commission a full building survey — a HomeBuyer Report is unlikely to provide sufficient detail for non-standard properties.

- Ask the seller directly whether the property is PRC-designated and whether a repair certificate exists.

- Engage a specialist mortgage broker early; do not assume a mainstream lender will lend.

- Budget for higher insurance costs and potential remediation work.

- Request a property condition assessment that specifically addresses the non-standard elements.

For Sellers

- Locate and present any existing structural repair certificates, guarantees, or specialist reports.

- Be transparent about the construction type in marketing materials — concealment will delay or derail the sale.

- Price realistically, taking into account the reduced pool of mortgage-eligible buyers.

- Consider instructing a pre-sale survey to identify issues before they are raised by a buyer's surveyor.

For Lenders and Intermediaries

- Provide clear criteria to brokers regarding which non-standard types are acceptable and under what conditions.

- Require a specialist structural report where frame condition cannot be confirmed by visual inspection alone.

- Ensure the valuer instructed has demonstrable experience with the specific construction type.

Conclusion

Non-standard construction is not a niche concern — it affects a significant portion of the UK housing stock, and in 2026 it remains one of the most technically demanding areas of residential valuation practice. The key to competent valuation lies in three disciplines working together: precise identification of the construction type, thorough condition assessment of the non-standard elements, and rigorous use of comparable market evidence to justify any value adjustment.

Actionable next steps:

- If purchasing a non-standard property, instruct a chartered surveyor with specific experience in that construction type before exchanging contracts.

- If selling, gather all existing documentation — repair certificates, guarantees, specialist reports — and make them available to buyers' solicitors at the outset.

- If instructing a valuation for lending purposes, confirm that the appointed surveyor is familiar with the specific construction type and the local market for comparable evidence.

- Surveyors should ensure their reports name the construction type precisely, describe observed defects, state any limitations on inspection, and provide a clear written rationale for any value adjustment applied.

Getting this right protects buyers from overpaying, lenders from inadequate security, and surveyors from professional liability. For specialist advice or to commission a survey on a non-standard construction property, get a quote from a qualified chartered surveyor with local expertise.

References

[1] Standard Construction House 3905 – https://www.samconveyancing.co.uk/news/house-survey/standard-construction-house-3905?utm_source=openai

[2] Concrete Prefab House Mortgage – https://www.propertypassport.uk/guides/concrete-prefab-house-mortgage?utm_source=openai

[3] What You Should Know About Non Standard Construction Types – https://www.terracottaproperty.com/blog/what-you-should-know-about-non-standard-construction-types?utm_source=openai

[4] Non Standard Construction – https://www.howdeninsurance.co.uk/personal/home/home-insurance/guides/non-standard-construction/?utm_source=openai

[5] Survey Ex Council House Selling – https://getpine.co.uk/guides/survey-ex-council-house-selling?utm_source=openai

[6] Non Standard Construction Mortgage – https://www.propertypassport.uk/guides/non-standard-construction-mortgage?utm_source=openai

[7] Post War Housing Uk Guide – https://www.propertypassport.uk/guides/post-war-housing-uk-guide?utm_source=openai

[8] 163 Non Traditional Housing Bisf Explained – https://www.britmet.co.uk/163-non-traditional-housing-bisf-explained.htm?utm_source=openai