Institutional demand for buy-to-let assets has not retreated despite the UK's cooling price environment — in Q1 2026, RICS data showed twelve-month capital value expectations weakening to a net balance of -18%, yet professional landlords continue to expand portfolios, driven by rental income rather than speculative gain [4]. This divergence between capital caution and income confidence is precisely where disciplined valuation practice becomes the competitive edge. Valuing BTL Properties for Professional Landlords in Stabilising Markets: RICS Checklists Post-Q1 2026 RICS Survey is not merely a compliance exercise; it is the analytical foundation on which risk-adjusted yield decisions are built. For surveyors and landlords operating across London and the wider UK, understanding the post-Q1 2026 RICS landscape — its updated methodology, ESG requirements, and Basel 3.1 prudence criteria — determines whether a portfolio grows profitably or stagnates under mispriced assets.

Key Takeaways

- RICS Q1 2026 data shows weakened capital value expectations, shifting professional landlord focus firmly toward income-driven valuation methods.

- The investment method — converting rental income streams into present value — is the primary RICS-endorsed technique for BTL property assessment.

- Basel 3.1 prudence criteria now require valuers to exclude speculative price growth assumptions from lending-related valuations.

- ESG factors are formally integrated into RICS valuation standards as of April 2026, affecting energy efficiency ratings and long-term asset value.

- Recent, hyper-local comparable evidence is essential in stabilising markets, where national averages mask significant regional divergence.

Understanding the Post-Q1 2026 Market Context for BTL Valuations

The Q1 2026 RICS UK Commercial Property Monitor delivered a sobering set of signals. The credit conditions indicator collapsed from +9% in Q4 2025 to -44% in Q1 2026, a shift attributed largely to geopolitical tensions and tightening lending sentiment [4]. For professional landlords, this matters because lender-instructed valuations now carry heightened scrutiny, and surveyors must navigate a market where sentiment and fundamentals are pulling in different directions.

What stabilising markets actually mean for BTL:

A stabilising market is not a falling market. It is a market in which price growth has plateaued — neither accelerating nor correcting sharply. In this environment:

- Rental yields become the primary driver of investment value

- Capital growth assumptions must be conservative or excluded entirely

- Comparable evidence ages quickly, requiring more frequent re-assessment

- Lender appetite becomes more selective, increasing the importance of precise valuations

RICS guidance consistently emphasises that national statistics can obscure local realities [8]. A landlord with properties in Lewisham faces a different supply-demand dynamic than one operating in Westminster or Enfield. Surveyors working with property surveyors in Lewisham or Westminster property surveyors must apply location-specific comparable evidence rather than relying on headline UK indices.

Why Institutional Landlords Are Still Buying

Despite weakened capital value expectations, professional landlords are not withdrawing. The logic is straightforward: rental demand remains structurally elevated, driven by affordability constraints that prevent many households from purchasing. Gross yields in many London zones and commuter belt towns remain attractive relative to risk-free rates, particularly when operational costs are managed efficiently.

This is the context in which Valuing BTL Properties for Professional Landlords in Stabilising Markets: RICS Checklists Post-Q1 2026 RICS Survey carries its greatest practical weight — not as a theoretical exercise, but as a tool for identifying which assets justify acquisition at current pricing.

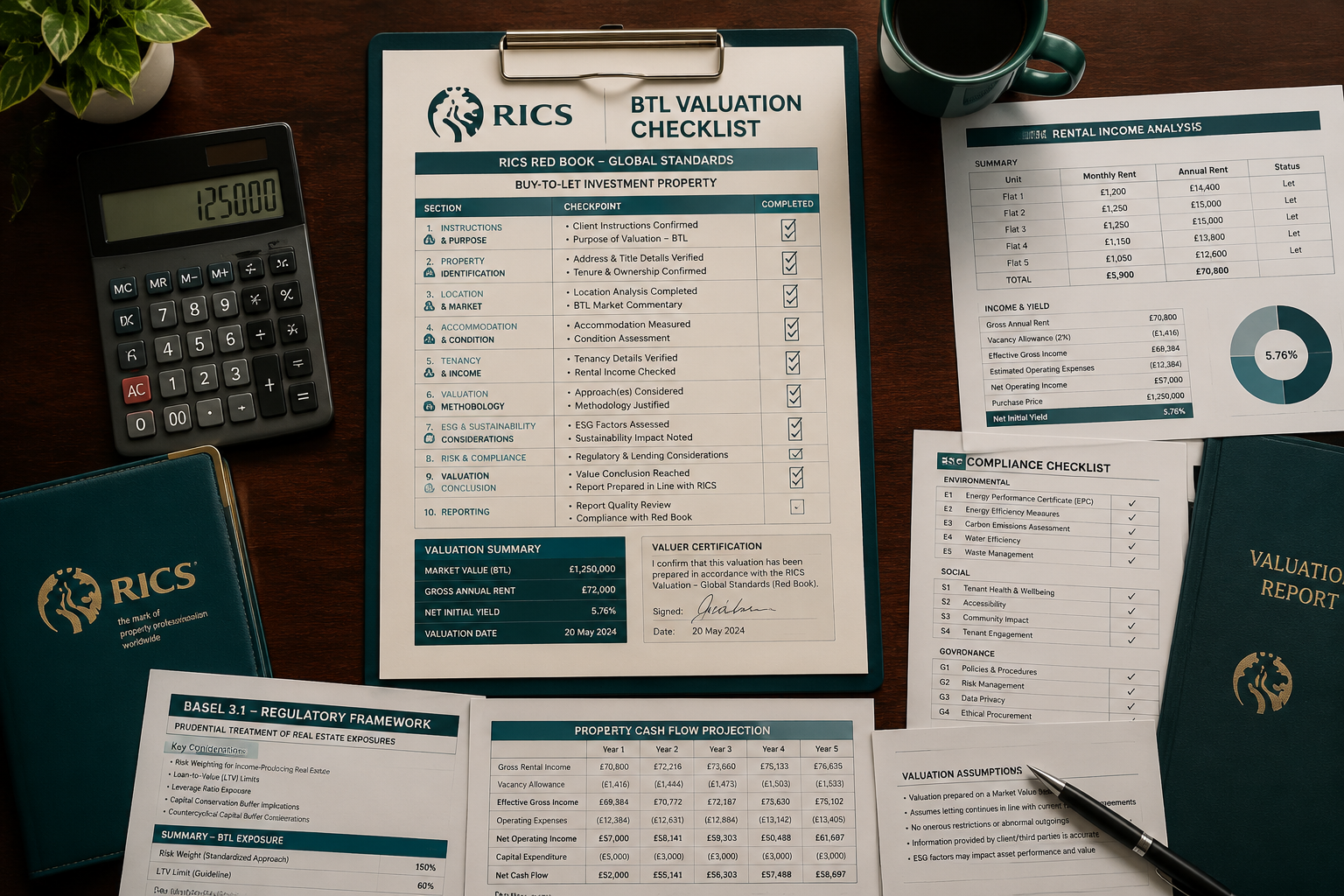

RICS Valuation Methodology: The Three-Approach Framework for BTL Assets

RICS structures property valuation around three overarching approaches: market, income, and cost. Within each approach sit specific methods, and within methods sit quantitative models [1]. This hierarchy — approach, method, model — is not semantic pedantry. It provides a transparent, auditable framework that satisfies lender requirements, Red Book Global Standards, and increasingly, ESG reporting obligations [2].

The Income Approach: Primary Method for BTL

For buy-to-let properties, the income approach is the dominant framework. It converts future rental income into a present capital value, using either:

Traditional Investment Method:

- Estimate gross rental income (market rent or passing rent)

- Deduct operating expenditures (management fees, maintenance, voids, insurance)

- Apply a capitalisation rate (yield) derived from comparable market transactions

- Produce a capital value

Discounted Cash Flow (DCF) Analysis:

- Project income and expenditure over a defined holding period

- Apply a discount rate reflecting risk and opportunity cost

- Calculate net present value of the income stream plus terminal value

RICS guidance on valuing residential property purpose-built for renting specifically endorses the net income capitalisation method, requiring valuers to assess gross income, operating expenditures, and void periods with precision [6]. For older converted BTL stock — the majority of the UK's private rented sector — the same principles apply, though comparable evidence is typically drawn from similar converted properties rather than purpose-built benchmarks.

| Valuation Component | Key Consideration in 2026 |

|---|---|

| Gross Rental Income | Market rent vs. passing rent; rent review clauses |

| Operating Expenditure | EPC compliance costs; management fees |

| Void Allowance | Local vacancy rates; tenant demand indicators |

| Capitalisation Rate | Derived from recent, local comparable yields |

| ESG Adjustment | Energy efficiency rating impact on long-term value |

The Market Approach and Its Limitations in Stabilising Conditions

The market (or comparable) approach — matching a subject property against recent sales of similar assets — remains relevant for BTL valuation, particularly where the subject property might be sold with vacant possession. However, in stabilising markets, the comparable evidence pool shrinks. Transactions slow, and older comparables become less reliable.

RICS advises prioritising recent and relevant comparable evidence, with a preference for transactions completed within the last three to six months in volatile or transitional market conditions [8]. Surveyors should weight more recent evidence more heavily, even if the comparable pool is thin, rather than relying on transactions from a more buoyant period that no longer reflects current pricing.

The cost approach — estimating the cost of replacing or reproducing the asset — is rarely primary for standard BTL residential properties but may be relevant for unusual or specialist assets within a mixed portfolio.

The RICS Checklist for Valuing BTL Properties Post-Q1 2026

A structured checklist approach is essential for professional landlords and their appointed surveyors. The post-Q1 2026 environment introduces several new or elevated requirements that must be embedded into standard valuation practice. The following checklist reflects current RICS standards, Basel 3.1 prudence criteria, and ESG integration requirements.

Pre-Inspection Checklist

Before visiting the property, the valuer should confirm:

- Instruction scope: Is this a Red Book valuation, a desktop assessment, or a monitoring survey? For lending purposes, a full RICS property valuation is typically mandatory.

- Tenure details: Freehold, leasehold (and remaining term), or commonhold

- Current tenancy status: Passing rent, lease expiry, break clauses, and rent review dates

- Planning and permitted use: Confirmed residential use; any Article 4 directions affecting HMO conversion

- EPC rating: Current certificate and any required upgrade works under Minimum Energy Efficiency Standards

- Recent maintenance history: Any major works completed or outstanding

On-Site Inspection Checklist

During the physical inspection, the surveyor should assess:

- Structural condition: Roof, walls, foundations — defects that affect value or insurability. A full RICS building survey may be warranted for older or complex stock.

- Damp and timber: Active damp, rising damp, or timber decay that could trigger remediation costs

- Services condition: Boiler age, electrical installation condition report (EICR) compliance, water pressure

- Layout and lettable area: Net internal area, room sizes against HMO licensing thresholds where applicable

- ESG factors: Insulation quality, heating system type, solar provision, EPC-relevant features

"In stabilising markets, condition-related value adjustments carry disproportionate weight. A property requiring a £15,000 EPC upgrade is not simply worth £15,000 less — it carries additional void risk, financing complications, and tenant retention risk that compound the headline cost."

Rental Income Assessment Checklist

- Confirm passing rent against market evidence: Is the current tenancy above, at, or below market rent?

- Assess rental growth prospects: Local supply pipeline, planning permissions, demographic trends

- Estimate void periods: Based on local letting agent data and historical vacancy for the property type

- Calculate gross-to-net yield: Account for management fees (typically 8-15%), maintenance reserves, insurance, and ground rent/service charge for leasehold assets

- Stress-test the yield: Apply a 1-2% yield expansion scenario to model downside capital value

Basel 3.1 Compliance Checklist

The Basel 3.1 framework, now embedded in UK lending practice, requires that valuations used for mortgage security purposes meet prudently conservative criteria [3]. Specifically:

- Exclude any assumption of future price appreciation beyond current market evidence

- Disregard market prices that appear significantly above sustainable long-term levels

- Apply a Mortgage Lending Value (MLV) concept where instructed by the lender

- Document the basis of valuation clearly, distinguishing between Market Value and any prudently conservative variant

This has direct implications for BTL valuations submitted to lenders. A valuation that assumes 3% annual capital growth to justify a higher figure will not satisfy Basel 3.1 requirements. The income must support the value independently.

ESG Integration Checklist

As of April 2026, RICS formally requires valuers to consider ESG factors in their assessments [8]. For BTL properties, the most material ESG considerations are:

- Energy Performance Certificate (EPC) rating: Properties rated below C face increasing regulatory risk and potential unlettability under future MEES upgrades

- Heating system type: Gas boilers face long-term phase-out risk; heat pump compatibility affects future capital expenditure

- Flood risk: Environment Agency flood zone classification and its impact on insurance costs and mortgage availability

- Social factors: Tenant affordability, local amenity access, and proximity to employment centres

Valuers should note ESG-related adjustments explicitly in their reports, quantifying where possible the impact on net income and capitalisation rate.

Regional Considerations: Applying RICS Checklists Across UK Markets

One of the most consistent findings from post-Q1 2026 RICS analysis is that regional divergence is widening [8]. Professional landlords with geographically diverse portfolios cannot apply a single yield assumption or void rate across all assets.

London: Yield Compression Meets Regulatory Pressure

London BTL assets typically offer lower gross yields (3.5-5% in many zones) but benefit from stronger rental demand and lower void risk. However, regulatory complexity is higher — HMO licensing, selective licensing schemes, and Renters' Rights Act implications all affect net income. Surveyors operating in areas such as Fulham, Hackney, or Ealing must factor local licensing costs and compliance requirements into operating expenditure estimates.

Commuter Belt and Regional Cities: Higher Yields, Greater Sensitivity

Markets in areas such as Brentwood, Southend-on-Sea, and outer London boroughs often offer gross yields of 5-7%, making the income approach more straightforwardly supportive of value. However, these markets are more sensitive to interest rate movements and employment base changes. Brentwood property surveyors and those covering Southend-on-Sea will note that comparable evidence in these markets can be thin, requiring careful weighting of available transactions.

Applying the Checklist Locally

The RICS checklist framework does not change by region, but the inputs do. A void allowance of 3% may be appropriate in a high-demand London zone but inadequate in a market with significant new-build supply. The capitalisation rate must reflect local investor appetite, not a national average. This is where experienced, locally active surveyors add the most value — their knowledge of micro-market conditions cannot be replicated by desktop analysis alone.

Professional Standards and Red Book Compliance in 2026

RICS residential valuation standards require that all Red Book valuations adhere to the current edition of the Red Book Global Standards, with UK-specific supplements applied where relevant [7]. For BTL properties, the key professional standards obligations include:

- Independence and objectivity: The valuer must have no conflict of interest with the instructing party

- Basis of value: Market Value must be clearly defined and distinguished from any alternative basis

- Assumptions and special assumptions: Any departure from standard market conditions — such as assuming a tenancy will be renewed — must be explicitly stated and agreed with the client

- Comparable evidence: The report must reference the comparable transactions used, with commentary on their relevance and any adjustments applied

RICS also emphasises that professional standards in valuations are not optional enhancements — they are the foundation of accuracy and reliability that lenders, investors, and courts rely upon [7]. For professional landlords, instructing a RICS-regulated valuer is not simply about satisfying a lender requirement; it is about obtaining a defensible, auditable assessment of asset value.

Understanding what a surveyor does and their professional responsibilities helps landlords engage more effectively with the valuation process and ask the right questions of their appointed professionals.

Conclusion: Actionable Steps for Professional Landlords in 2026

Valuing BTL Properties for Professional Landlords in Stabilising Markets: RICS Checklists Post-Q1 2026 RICS Survey is a discipline that rewards preparation, local knowledge, and methodological rigour. The post-Q1 2026 environment — characterised by weakened capital value expectations, tightening credit conditions, and expanded ESG obligations — demands that professional landlords and their surveyors operate with greater precision than in a rising market.

Actionable next steps for professional landlords:

- Commission RICS Red Book valuations for all assets under active lending or refinancing review — desktop estimates are insufficient in the current credit environment.

- Audit EPC ratings across the portfolio now — properties below a C rating carry regulatory and income risk that must be priced into acquisition and hold decisions.

- Instruct locally active, RICS-regulated surveyors — regional market knowledge is non-negotiable in a period of widening geographic divergence.

- Stress-test yield assumptions against Basel 3.1 criteria — ensure that valuations submitted to lenders exclude speculative capital growth and stand on income fundamentals alone.

- Review comparable evidence quarterly — in stabilising markets, evidence from 12 months ago may already be misleading.

- Integrate ESG factors into acquisition due diligence — future capital expenditure on energy efficiency is a present-day valuation consideration, not a future problem.

The professional landlords who will outperform in 2026 and beyond are those who treat valuation not as a box-ticking exercise, but as the analytical core of every investment decision.

References

[1] APC 5 Valuation Methods – https://ww3.rics.org/uk/en/journals/property-journal/apc-5-valuation-methods.html?utm_source=openai

[2] Valuation Approaches Methods Models – https://ww3.rics.org/uk/en/journals/property-journal/valuation-approaches-methods-models.html?utm_source=openai

[3] Basel 3.1 Prudently Conservative Valuation Criteria – https://ww3.rics.org/uk/en/journals/property-journal/basel-3-1-prudently-conservative-valuation-criteria.html?utm_source=openai

[4] RICS UK Commercial Property Monitor Q1 2026 – https://www.rics.org/news-insights/rics-uk-commercial-property-monitor-q1-2026?utm_source=openai

[5] Valuation of Licensed Leisure Property 2nd Edition – https://www.rics.org/profession-standards/rics-standards-and-guidance/sector-standards/valuation-standards/valuation-of-licensed-leisure-property-2nd-edition?utm_source=openai

[6] Valuing Residential Property Purpose Built for Renting – https://www.rics.org/profession-standards/rics-standards-and-guidance/sector-standards/valuation-standards/valuing-residential-property-purpose-built-for-renting?utm_source=openai

[7] Residential Valuations – https://www.rics.org/profession-standards/rics-standards-and-guidance/sector-standards/valuation-standards/residential-valuations?utm_source=openai

[8] Valuing Properties Under Stabilising National Prices: RICS Techniques for Q1 2026 – https://manchestersurveyors.com/valuing-properties-under-stabilising-national-prices-rics-techniques-for-q1-2026-house-price-net-balance-of-10/?utm_source=openai