}

The North West of England is now the clearest regional bright spot in the UK property market — and the data proves it. While London, the South East, and East Anglia continue to lag, the RICS January 2026 UK Residential Market Survey explicitly identifies the North West and North of England as regions showing the strongest upward price trajectories nationally [3]. For building surveyors, this is not background noise. This is a strategic signal.

The Building Survey Demand Surge in North West England: Capitalizing on RICS January 2026 Market Recovery Signals is a real, measurable opportunity — and those who understand the underlying data will be positioned to capture it before the wider market catches up.

Key Takeaways 📋

- 🏠 North West leads the UK recovery: RICS January 2026 data identifies North West England as one of the strongest-performing regions for price growth and buyer momentum.

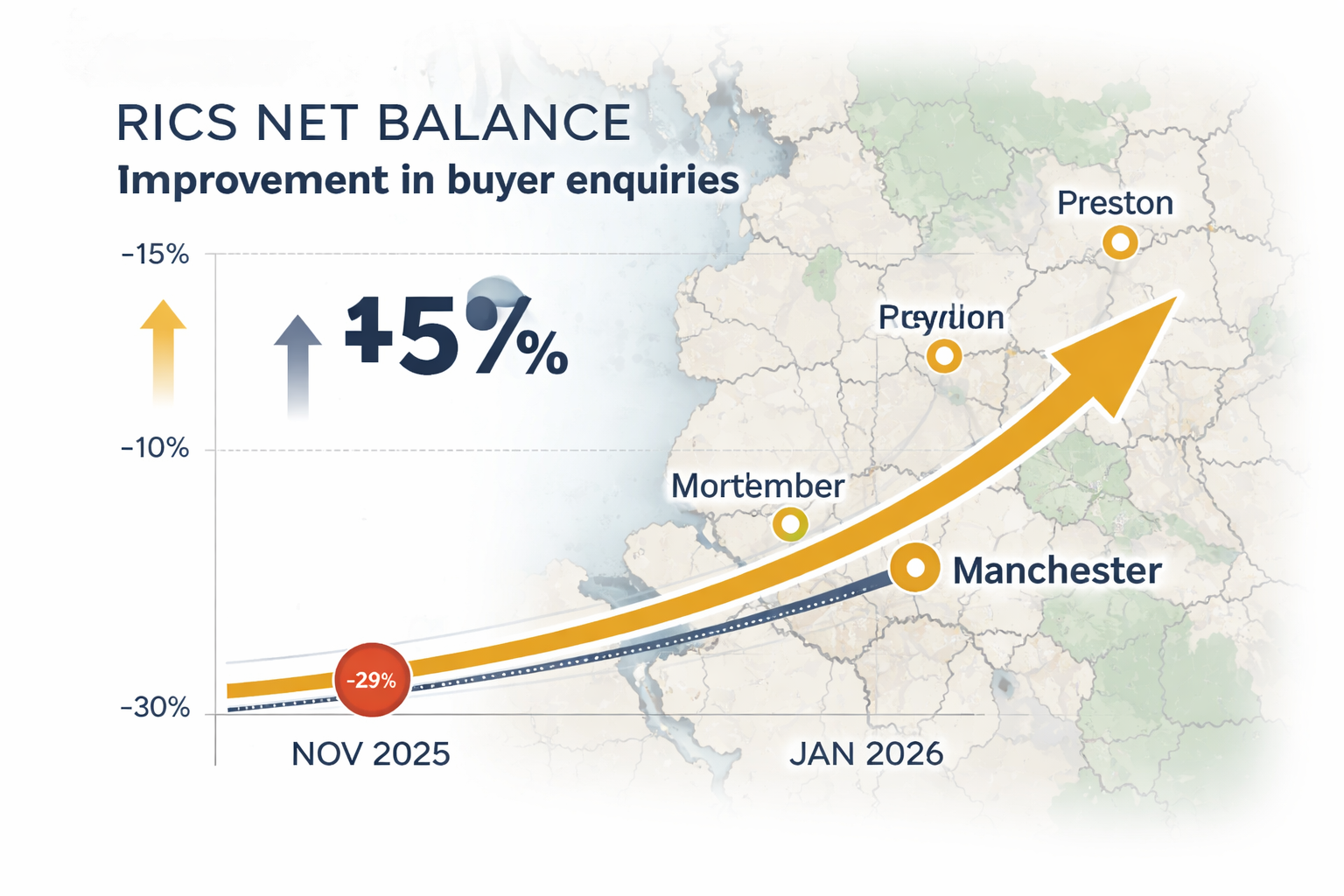

- 📈 Buyer enquiries are rebounding fast: The national net balance for new buyer enquiries improved from -29% (November 2025) to -15% (January 2026), signalling accelerating transaction pipelines.

- 🔨 Construction pipeline is stirring: RIBA's January 2026 Workload Index turned positive (+3) for the first time in five months, supporting new-build survey demand.

- 💷 Northern England expected to outperform on price growth: Forecasts suggest northern regions will see above-average house price growth in 2026, driving more transactions and survey requirements.

- 🎯 Surveyors should position surveys as transaction certainty tools: In recovering markets, buyers need confidence — and a thorough building survey delivers exactly that.

Understanding the RICS January 2026 Recovery Signals for North West England

The Numbers Behind the Narrative

The RICS UK Residential Market Survey for January 2026 paints a picture of cautious but genuine recovery [3]. Three headline metrics stand out for anyone tracking building survey demand:

| Metric | November 2025 | December 2025 | January 2026 |

|---|---|---|---|

| New Buyer Enquiries (net balance) | -29% | -21% | -15% |

| Agreed Sales (net balance) | — | — | -9% (least negative since June 2025) |

| House Prices (3-month net balance) | — | — | -10% (up from -19% in Oct 2025) |

| 12-Month Sales Outlook | — | — | +35% (strongest since Dec 2024) |

Source: RICS UK Residential Market Survey, January 2026 [3]

Every single metric is moving in the right direction. The agreed sales figure reaching -9% — the least negative reading since June 2025 — is particularly significant [3]. Agreed sales are the direct precursor to building survey instructions. When transactions progress, surveys follow.

"The 12-month sales outlook reached +35%, the strongest reading since December 2024 — a clear signal that building survey professionals can expect sustained demand across 2026." [3]

Why the North West Is Different

The RICS data does not treat all regions equally, and that distinction matters enormously for surveyors. The January 2026 report explicitly notes that price growth remains strongest in Scotland and Northern Ireland, with clear upward trends in the North West and North of England, while London, the South East, South West, and East Anglia continue to underperform [3].

This regional divergence has a simple explanation: affordability. North West property prices remain significantly below southern equivalents, attracting first-time buyers, investors, and relocators priced out of southern markets. Cities like Manchester, Liverpool, Preston, and Salford are seeing sustained demand from younger buyers and professionals — exactly the demographic most likely to commission a home survey before completing a purchase.

The HomeOwners Alliance forecast reinforces this view, projecting UK house prices around 2% higher in 2026, with northern England expected to outperform the south [5]. Above-average price growth means above-average transaction volumes — and above-average demand for building surveys.

Construction Signals Add Another Layer

The picture is not purely residential resale. The RIBA Future Trends survey for January 2026 recorded a Workload Index of +3, ending four consecutive months of negative balances [4]. This tentative optimism at the front end of the construction pipeline matters because new-build activity generates its own surveying requirements — from pre-purchase inspections to snagging surveys.

Cost consultant Gardiner & Theobald revised its 2026 average tender price inflation forecast upward to 3.0% from 2.5% as of February 2026, driven by a pipeline that is "starting to stir" [4]. Rising tender prices reflect increased activity — and increased activity means more properties entering the market that need professional assessment.

However, context is important. Residential construction starts remained 32% down compared to 2025 levels as of January 2026, and the North West delivered mixed quarterly results — starts rose quarter-on-quarter but still lagged year-ago figures [1]. This is a recovery in progress, not a boom. Surveyors should plan for sustained, building demand rather than an overnight surge.

What Property Types Are Driving Building Survey Demand Surge in North West England

The Victorian and Edwardian Stock Problem — and Opportunity

The North West's housing stock is dominated by Victorian and Edwardian terraced and semi-detached properties, particularly across Greater Manchester, Merseyside, and Lancashire. These properties are typically 80–140 years old and present a consistent range of structural and condition issues that make professional surveys not just advisable — but essential.

Common defects in this stock include:

- 🧱 Solid wall construction with no cavity insulation — damp penetration risk

- 🪵 Original timber floors and joists susceptible to rot and beetle infestation

- 🏚️ Ageing roof coverings — original slate or early concrete tiles nearing end of life

- ⚡ Outdated electrical installations — pre-consumer unit wiring in older properties

- 💧 Lead or iron pipework in plumbing systems

For buyers purchasing these properties, a Level 2 survey may not be sufficient. Understanding the difference between survey types is critical — and surveyors who can clearly explain home survey levels and which option is right for a Victorian terrace versus a modern apartment will convert more instructions.

A full structural survey — the most comprehensive option — is often the appropriate recommendation for pre-1919 properties, particularly those that have been extended, converted, or left unmaintained.

New-Build and Conversion Activity

Manchester's city centre and inner suburbs have seen significant apartment development and commercial-to-residential conversion activity over the past decade. While overall residential starts remain below prior-year levels [1], the pipeline of completions from earlier starts continues to feed the market.

New-build buyers often underestimate the value of a snagging survey or independent inspection. Surveyors operating in the North West have a clear opportunity to educate this buyer segment — particularly as tenant demand also edged higher in the three months to January 2026 [3], suggesting buy-to-let investors are re-entering the market and will need property condition assessments before committing to purchases.

The Damp and Timber Factor

North West England's climate — characterised by higher rainfall than southern England — means damp-related issues are disproportionately common in the region's housing stock. Rising damp, penetrating damp, and condensation are among the most frequently identified defects in building surveys across Manchester and Liverpool.

Surveyors who can offer specialist damp and timber assessments alongside standard building surveys are well-positioned to serve this market. Buyers who receive a building survey identifying potential damp issues will often require a follow-up specialist report — creating a natural upsell opportunity and a more complete service offering.

Capitalizing on RICS January 2026 Market Recovery Signals: Positioning Surveys as Transaction Certainty Tools

The Confidence Gap in Recovering Markets

In a recovering market, buyer psychology is complex. Buyers are re-entering after a period of hesitation — but they carry residual anxiety about overpaying or inheriting hidden defects. This is precisely the environment where a building survey delivers its highest perceived value.

The RICS data showing agreed sales at their least negative since June 2025 [3] tells a specific story: buyers are progressing transactions, but they are doing so carefully. A building survey is not just a technical document in this context — it is a confidence instrument. It answers the question every cautious buyer is asking: "Am I making a safe decision?"

Surveyors who frame their service around transaction certainty — rather than simply defect identification — will resonate more powerfully with 2026's re-emerging buyer. Key messaging should emphasise:

- ✅ Informed decisions: Know exactly what you are buying before you commit

- ✅ Negotiation leverage: Use survey findings to renegotiate price or request remediation

- ✅ Future cost planning: Understand maintenance liabilities before they become emergencies

- ✅ Mortgage protection: Satisfy lender requirements with a credible professional report

For buyers who want to understand how surveys can actually save money on a property purchase, the financial case is compelling — survey costs are typically a fraction of the defect remediation costs they help buyers avoid or negotiate away.

Why RICS Accreditation Matters More Than Ever

In a market showing early recovery signals, professional credibility becomes a differentiator. The RICS brand carries significant weight with buyers, mortgage lenders, and solicitors. Surveyors who can clearly articulate why choosing a RICS surveyor matters — regulatory oversight, professional indemnity, standardised reporting — will build trust faster with an audience that has been cautious about property decisions for the past 18 months.

The RICS January 2026 data itself becomes a marketing asset. Sharing the recovery signals — improved buyer enquiries, strengthening sales pipeline, North West outperformance — positions a surveying practice as a market-informed professional, not just a technical inspector.

Practical Strategies for Surveyors in 2026

The Building Survey Demand Surge in North West England: Capitalizing on RICS January 2026 Market Recovery Signals requires more than awareness — it requires action. Here are the most effective strategies for surveyors looking to capitalise:

1. Target Estate Agent Referral Networks

Estate agents in Manchester, Liverpool, and surrounding areas are seeing improved enquiry volumes [3]. Building relationships with local agents — and offering fast turnaround times — positions surveyors as the natural referral choice when buyers ask for recommendations.

2. Educate Buyers on Survey Levels

Many buyers default to a basic valuation because they do not understand the difference between survey levels. Providing clear homebuying guidance materials and accessible explainer content converts more undecided buyers into survey clients.

3. Offer Specialist Add-Ons

Given the North West's housing stock profile, offering damp surveys, timber assessments, and roof inspections as add-ons to standard building surveys increases average transaction value and client satisfaction.

4. Leverage Digital Visibility

The recovery in buyer enquiries is happening online first. Surveyors with strong local SEO presence in North West search terms will capture demand at the point of intent — when buyers are actively researching properties and services.

5. Build a Track Record with Investors

The improving lettings market [3] signals that landlords and buy-to-let investors are active again. This segment often requires multiple surveys across a portfolio — making them high-value, repeat clients.

The Broader Context: Caution Alongside Optimism

It would be misleading to present the January 2026 signals as unambiguously positive. The RICS report itself is subtitled "early signs of market recovery despite caution" [3] — and that qualification matters.

Residential construction starts remain 32% below 2025 levels nationally [1]. The North West's construction performance was mixed — quarterly improvement but still below year-ago figures [1]. The house price net balance of -10% is improving but still negative [3]. These are recovery signals, not recovery confirmation.

The most accurate framing is this: the market is moving in the right direction, faster in the North West than elsewhere, but the trajectory is not yet steep enough to be called a boom. For building surveyors, this means:

- Demand is growing, but capacity constraints are not yet a concern

- Pricing power is returning, but not yet sufficient to justify significant fee increases

- The window to build market share is now — before competition intensifies as the recovery matures

Conclusion: Act on the Signals Before the Market Does

The RICS January 2026 data is unambiguous about one thing: the North West of England is leading the UK's residential property recovery. Buyer enquiries are improving month-on-month. Agreed sales are at their strongest since mid-2025. The 12-month outlook is the most optimistic in over a year. Northern regions are forecast to outperform on price growth [5].

For building surveyors, this convergence of signals represents a genuine strategic opportunity. The Building Survey Demand Surge in North West England: Capitalizing on RICS January 2026 Market Recovery Signals is not a future possibility — it is an unfolding reality that rewards those who move with intention.

Actionable next steps for building surveyors in 2026:

- 📍 Review your geographic coverage — ensure North West postcodes are prioritised in your marketing and capacity planning

- 🤝 Activate estate agent relationships in Manchester, Liverpool, Salford, Preston, and Chester now

- 📄 Update your service descriptions to emphasise transaction certainty and buyer confidence, not just defect reporting

- 🔍 Invest in local SEO targeting North West property survey search terms before competition increases

- 📊 Use the RICS data in client communications to demonstrate market awareness and professional authority

- 🏚️ Develop specialist expertise in Victorian and Edwardian stock — the dominant property type driving North West demand

The recovery is early. The opportunity is real. The surveyors who act on the January 2026 signals today will be the ones with full order books when the market reaches its next peak.

References

[1] UK Construction Starts Down 9% in January 2026 – https://www.atkinssearch.co.uk/insights/uk-construction-starts-down-9-in-january-2026/

[2] UK Residential Market Survey January 2026 – https://www.rics.org/content/dam/ricsglobal/documents/market-surveys/uk-residential-market-survey/UK-Residential-Market-Survey_January-2026.pdf

[3] UK Resi Survey Jan 2026 Report Shows Early Signs Market Recovery Despite Caution – https://www.rics.org/news-insights/uk-resi-survey-jan-2026-report-shows-early-signs-market-recovery-despite-caution

[4] Signs of a Building Recovery as Pipeline Begins to Stir – https://www.constructionenquirer.com/2026/02/20/signs-of-a-building-recovery-as-pipeline-begins-to-stir/

[5] House Price Forecast – https://hoa.org.uk/advice/guides-for-homeowners/i-am-buying/house-price-forecast/