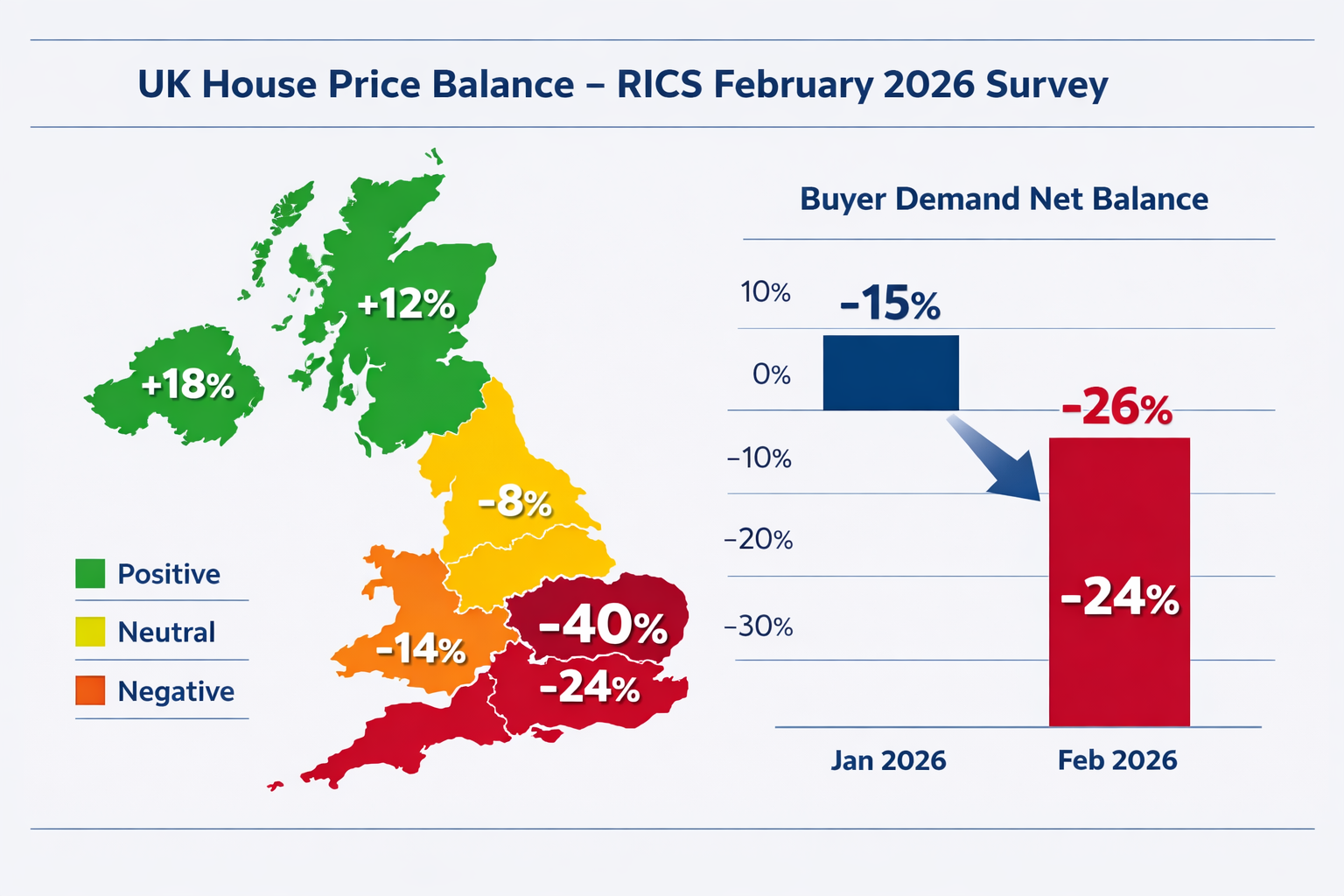

Buyer enquiries across the UK fell to a net balance of -26% in February 2026 — a sharp deterioration from -15% in January — yet surveyors in the North West of England, Scotland, and Northern Ireland are reporting a strikingly different story. The divergence between northern resilience and southern retreat is now one of the defining features shaping valuation challenges in Q2 2026 cautious markets, and the RICS February survey data provides the clearest evidence yet of how geography is splitting the UK property market in two [1].

For valuers, lenders, and property professionals navigating this environment, the February 2026 RICS UK Residential Market Survey is not just a barometer of sentiment — it is a practical toolkit for understanding where adjustments are defensible, where they are necessary, and how to communicate them clearly to clients and lenders under pressure [2].

Key Takeaways

- 📉 Buyer demand fell sharply to -26% nationally in February 2026, driven by interest rate uncertainty and renewed geopolitical tension

- 🏘️ Northern England, Scotland, and Northern Ireland showed firmer price trends, contrasting with London's -40% price balance

- ⚠️ Near-term price expectations turned negative at -18%, but 12-month outlooks remain positive at +33%

- 🔑 Valuers must defend regional adjustments with granular comparable evidence, especially where national indices mask local resilience

- 🏠 The lettings market faces acute supply pressure, with landlord instructions at -27% and rent rise expectations at +20%

Understanding the Regional Split: What RICS February Data Reveals

The headline figures from the RICS February 2026 survey paint a cautious national picture, but the regional breakdown tells a more nuanced story that is essential for any valuation professional working outside London and the South East.

National Headline vs. Regional Reality

At the national level, the headline price net balance sat at -12% in February 2026, only marginally weaker than the previous month [1]. Agreed sales remained subdued at -12%, and near-term sales expectations softened to -2% [1]. On the surface, these figures suggest a market in gentle retreat.

But disaggregate by region, and the picture changes dramatically:

| Region | Price Net Balance (Feb 2026) |

|---|---|

| London | -40% |

| South East | -24% |

| East Anglia | -26% |

| North West England | Positive / Firmer |

| Scotland | Positive / Firmer |

| Northern Ireland | Positive / Firmer |

💬 "The contrast between Southern regions and the North is not a rounding error — it represents a structural divergence in affordability, demand fundamentals, and supply dynamics."

London's -40% price balance is the steepest recorded in the current cycle [1]. For valuers operating in the capital, this creates acute pressure to justify current market values against comparable evidence that may already be dated by the time a report is issued.

Why Northern England Is Holding Firm

Several factors underpin Northern England's relative resilience:

- Relative affordability — average property prices in the North West remain significantly lower than Southern equivalents, keeping more buyers within mortgage reach

- Stronger local employment bases — cities like Manchester and Leeds continue to attract investment and employment, sustaining organic demand

- Lower investor withdrawal rates — fewer speculative buyers means less volatility when sentiment shifts

- Supply constraints — new instructions nationally remained broadly stable at just +2% [1], but in tighter northern markets, even modest supply restriction supports prices

For professionals providing RICS property valuations in any region, understanding these local fundamentals is the foundation of a defensible report.

Valuation Challenges in Q2 2026 Cautious Markets: Defending Adjustments Under Pressure

The valuation challenges in Q2 2026 cautious markets are not simply about falling prices. They are about the growing difficulty of justifying any figure — up or down — when market signals are contradictory, buyer confidence is fragile, and lenders are applying heightened scrutiny to every comparable used.

The Geopolitical and Macroeconomic Overhang

RICS explicitly noted in its February 2026 commentary that renewed geopolitical uncertainty and concerns over inflation and interest rates intensified through the month, directly affecting surveyor sentiment [1]. Rising oil and energy prices are prolonging elevated mortgage rates, creating a compounding headwind for buyer affordability [1].

This matters for valuers in a specific way: when macroeconomic conditions are shifting rapidly, comparable evidence ages faster. A sale agreed three months ago in a different interest rate environment may not be a reliable anchor for today's valuation. Surveyors must:

- Weight recent comparables more heavily — ideally within 8–12 weeks

- Apply explicit market condition adjustments where the evidence base spans a period of material change

- Document the macroeconomic context in the valuation report narrative, not just the figures

- Distinguish between regions — a market condition adjustment appropriate for London is not automatically appropriate for Leeds

Near-Term vs. Long-Term Expectations: A Critical Distinction

One of the most important data points from the February 2026 survey is the gap between short and long-term price expectations:

- Near-term (3-month) price expectations: -18% (down from -6% in January) [2]

- 12-month price expectations: +33% [2]

This divergence is significant for valuers. It suggests that the current caution is cyclical rather than structural — surveyors expect conditions to improve over the medium term, even as they brace for near-term softness. For mortgage valuations in particular, this distinction affects how a valuer frames risk in their report.

Understanding the difference between a Level 2 and Level 3 survey is equally important for buyers trying to determine the right level of professional scrutiny for their purchase in this environment.

Practical Tactics for Defending Valuation Adjustments

When a valuation figure is challenged — by a lender, a vendor, or a buyer — the defence rests on the quality of the evidence and the clarity of the reasoning. In Q2 2026's cautious market, the following tactics are essential:

🔍 Evidence gathering:

- Use at least three recent comparables, with explicit commentary on how each was adjusted

- Cross-reference Land Registry data with local agent intelligence

- Note where comparable evidence is thin and explain why the chosen approach was adopted

📝 Report narrative:

- Reference the RICS February 2026 survey data explicitly when describing market conditions

- Distinguish between national trends and local sub-market conditions

- Flag where geopolitical or macroeconomic factors have influenced the assessment

📊 Adjustment methodology:

- Apply percentage adjustments for condition, size, and location with clear rationale

- Where Northern England resilience is evident, do not apply Southern market discounts without local justification

- Consider the impact of the lettings market on investor-held stock valuations

Surveyors who want to understand their broader roles and responsibilities in this context will find that clear documentation is as important as the valuation figure itself.

Valuation Challenges in Q2 2026 Cautious Markets: The Lettings Market Dimension and Market Stability

The valuation challenges in Q2 2026 cautious markets extend beyond the sales market. The lettings sector is experiencing its own form of stress — one that has direct implications for investment property valuations and the broader market stability picture.

Lettings: A Supply Crisis in Plain Sight

The February 2026 RICS data on the lettings market is stark:

- Landlord instructions (new supply): -27% — firmly negative [1]

- Tenant demand: +2% — broadly stable [1]

- Near-term rent expectations: +20% expect rents to rise [1]

This combination — shrinking supply, stable demand, and rising rent expectations — creates a structural imbalance that is unlikely to resolve quickly. For valuers assessing buy-to-let properties or mixed-use assets, the rental income assumptions embedded in investment valuations need careful scrutiny.

💬 "A -27% landlord instruction balance is not a blip — it reflects a sustained withdrawal of private rental supply that is reshaping the investment case for residential property across multiple regions."

The implications for property professionals include:

- Rental yield assumptions may need upward revision in supply-constrained markets

- Void period assumptions should be reduced where tenant demand remains robust

- Capital value assessments for investment properties must account for the income growth potential that tight supply creates

For buyers considering leasehold properties in this environment, understanding what to check before buying a leasehold property is particularly important, as service charge and ground rent obligations affect net rental returns.

Market Fundamentals: The Stabilising Forces

Despite the cautious sentiment captured in the February 2026 survey, several structural factors are preventing a disorderly market correction:

✅ Responsible lending practices — underwriting standards have remained robust throughout the current cycle, limiting the risk of forced selling [4]

✅ Low repossession activity — mortgage arrears remain historically low, removing a key source of distressed supply that could accelerate price falls [4]

✅ Stable new instructions — the national +2% new instructions balance means supply is not flooding the market, providing a natural floor for prices [1]

✅ Long-term price optimism — the +33% 12-month price expectation balance suggests that market participants view current conditions as temporary [2]

These stabilising forces are particularly relevant for valuers who may face pressure from clients to adopt excessively cautious valuations. The evidence base does not support a systemic market failure — it supports a period of adjustment, particularly in overvalued Southern markets.

For anyone considering whether a survey is necessary before purchase, understanding how to save money with building surveys demonstrates that professional assessment often protects buyers from far greater costs down the line.

Renegotiation in a Softening Market

One practical consequence of the current environment is an increase in buyers seeking to renegotiate after survey findings. In a market where prices are under pressure — particularly in Southern regions — a poor survey result gives buyers additional leverage. Understanding whether renegotiation after a poor building survey result is appropriate is a question more buyers are asking in Q2 2026.

Surveyors should be prepared for their reports to be used as negotiating tools, which reinforces the importance of precise, well-evidenced condition assessments alongside valuation commentary.

The Stock Condition Dimension

For social housing providers and local authorities managing large residential portfolios in Northern England, the current market conditions also affect stock condition survey requirements. Where property values are holding firm, asset management decisions — including major works programmes and disposal strategies — need to be grounded in current market evidence rather than historical benchmarks.

Similarly, damp surveys are increasingly relevant in the current environment, as older Northern England housing stock often presents damp-related issues that directly affect both valuation and mortgage offer outcomes.

Conclusion: Actionable Steps for Valuers in Q2 2026

The RICS February 2026 survey data makes one thing clear: the UK property market in Q2 2026 is not a single market. It is a collection of regional markets with diverging fundamentals, and the valuation challenges in Q2 2026 cautious markets require professionals to respond with precision rather than broad-brush caution.

Actionable Next Steps for Property Professionals

- Segment your comparable evidence by region — do not apply London or South East market condition adjustments to Northern England properties without explicit local justification

- Reference the RICS February 2026 survey in valuation reports — it provides credible, independent evidence of the macroeconomic context affecting sentiment

- Distinguish near-term caution from long-term fundamentals — the -18% near-term expectation and +33% 12-month expectation tell different stories; use both appropriately

- Review rental income assumptions for investment properties in light of the -27% landlord instruction balance and +20% rent rise expectations

- Document geopolitical and macroeconomic factors in report narratives — this protects both the valuer and the client if conditions change rapidly

- Commission the right level of survey — in a market where condition issues can trigger renegotiation, a comprehensive assessment protects all parties

The Northern England resilience story is real, it is evidenced, and it is defensible. Valuers who understand the data — and communicate it clearly — will be best placed to serve their clients and maintain professional standards through the remainder of 2026.

References

[1] UK Residential Survey February 2026 – https://www.rics.org/news-insights/uk-residential-survey-february-2026

[2] UK Residential Market Survey February 2026 – https://www.rics.org/content/dam/ricsglobal/documents/market-surveys/uk-residential-market-survey/UK-Residential-Market-Survey_February-2026.pdf

[3] UK Economy Property Update February 2026 – https://www.rics.org/content/dam/ricsglobal/documents/market-surveys/uk-economy-property-update-february-2026.pdf

[4] Navigating a Cautious UK Housing Market in 2026 and Why Surveying Insight Matters More Than Ever – https://www.mortgagesolutions.co.uk/better-business/business-skills/2026/04/15/navigating-a-cautious-uk-housing-market-in-2026-and-why-surveying-insight-matters-more-than-ever-ison/