{"cover":"Professional landscape format (1536×1024) hero image featuring bold text overlay 'Regional Valuation Strategies Post-RICS February 2026 Survey: North West Growth vs London Price Cooling' in extra large 72pt white sans-serif font with dark shadow and semi-transparent navy overlay box, positioned in upper third. Background shows split-screen composition: left side displays Manchester skyline with modern construction cranes and rising property values visualization, right side shows London cityscape with cooling market indicators and downward trend arrows. Color scheme: deep navy blue, vibrant orange for North West growth, cool gray-blue for London cooling. High contrast, magazine cover quality, editorial style with professional financial aesthetic, subtle UK map overlay in background showing regional heat map of property performance.","content":["Detailed landscape format (1536×1024) infographic showing RICS February 2026 survey data with dual-axis comparison chart. Left panel displays North West England property metrics with upward green arrows, +4% growth indicators, and northern town names (Burnley, Rochdale, Liverpool) highlighted in bold typography. Right panel shows London market with -40% price balance in red, downward trend lines, and 12-month sentiment collapse from +56% to +7% visualized as dramatic cliff chart. Center features UK map with color-coded regions showing performance gradient from warm orange (North) to cool blue (South). Professional financial data visualization style with clean grid lines, percentage annotations, and RICS branding elements.","Detailed landscape format (1536×1024) illustration depicting chartered surveyor conducting property valuation in contrasting regional contexts. Split composition: left shows surveyor with tablet examining modern North West residential development with 'SOLD' signs and buyer queue, warm lighting suggesting market confidence. Right shows same surveyor in prestigious London property with concerned expression, reviewing declining market data on screen, cooler lighting. Foreground features transparent overlay of buyer enquiry graphs (-26% net balance), transaction velocity charts (-15% decline), and regional price balance comparisons. Professional surveying equipment, RICS documentation visible, contemporary business illustration style with subtle data visualization elements integrated into scene.","Detailed landscape format (1536×1024) strategic planning visualization showing property valuation methodology adaptation framework. Central UK map with regional overlays showing divergent market strategies: North West highlighted with growth-focused valuation approaches, comparable sales from expanding markets, optimistic adjustment factors. London area shows conservative valuation methods, risk-adjusted pricing, cooling market comparables. Surrounding the map are floating data cards displaying key metrics: buyer enquiries -26%, new instructions +2%, rental stock -27%, transaction velocity -15%. Professional consulting aesthetic with flowcharts, decision trees, and strategic arrows connecting regional approaches. Modern business intelligence style with clean typography, professional color coding (green for growth strategies, amber for cautious approaches), and RICS professional standards documentation visible in corner."]"}

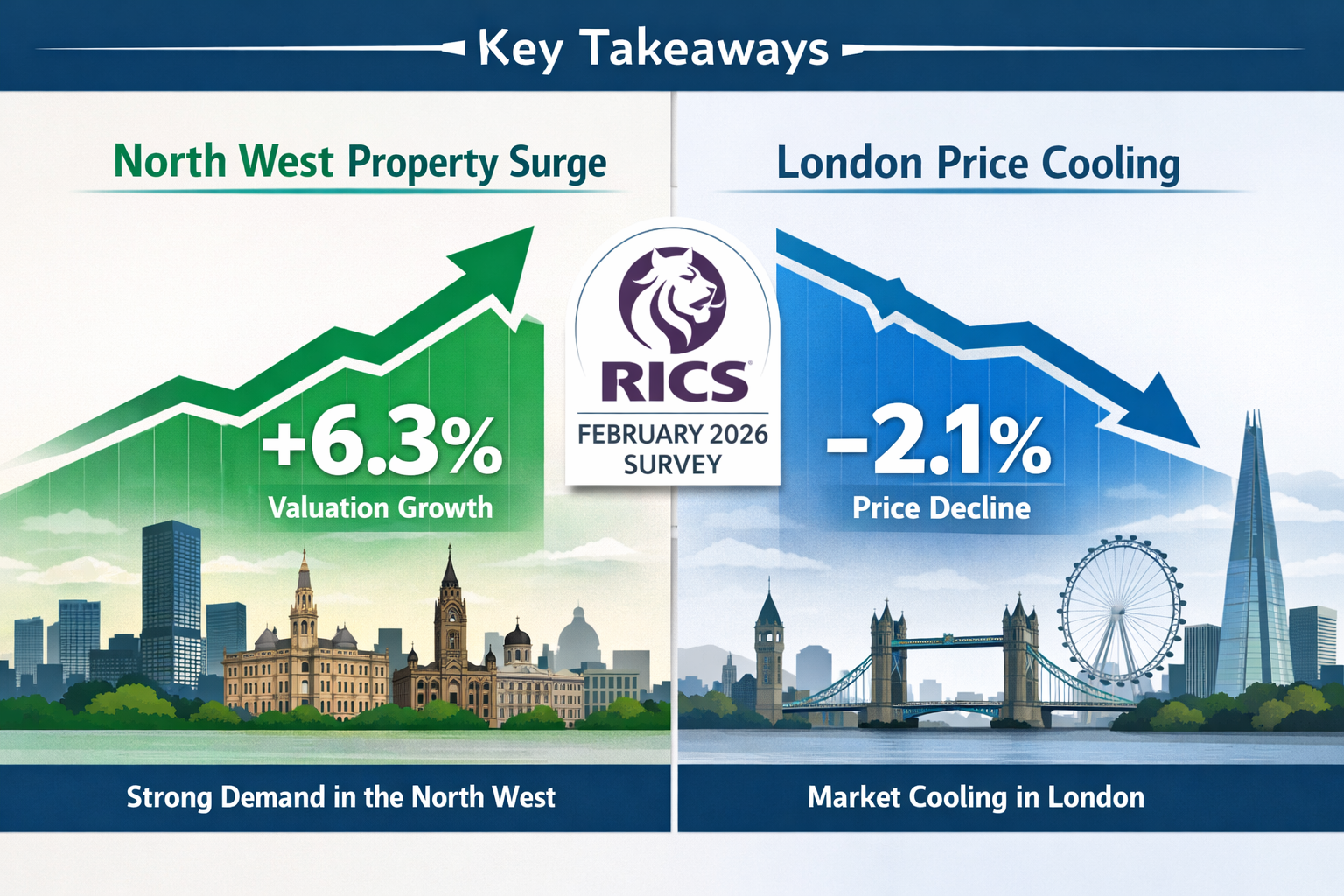

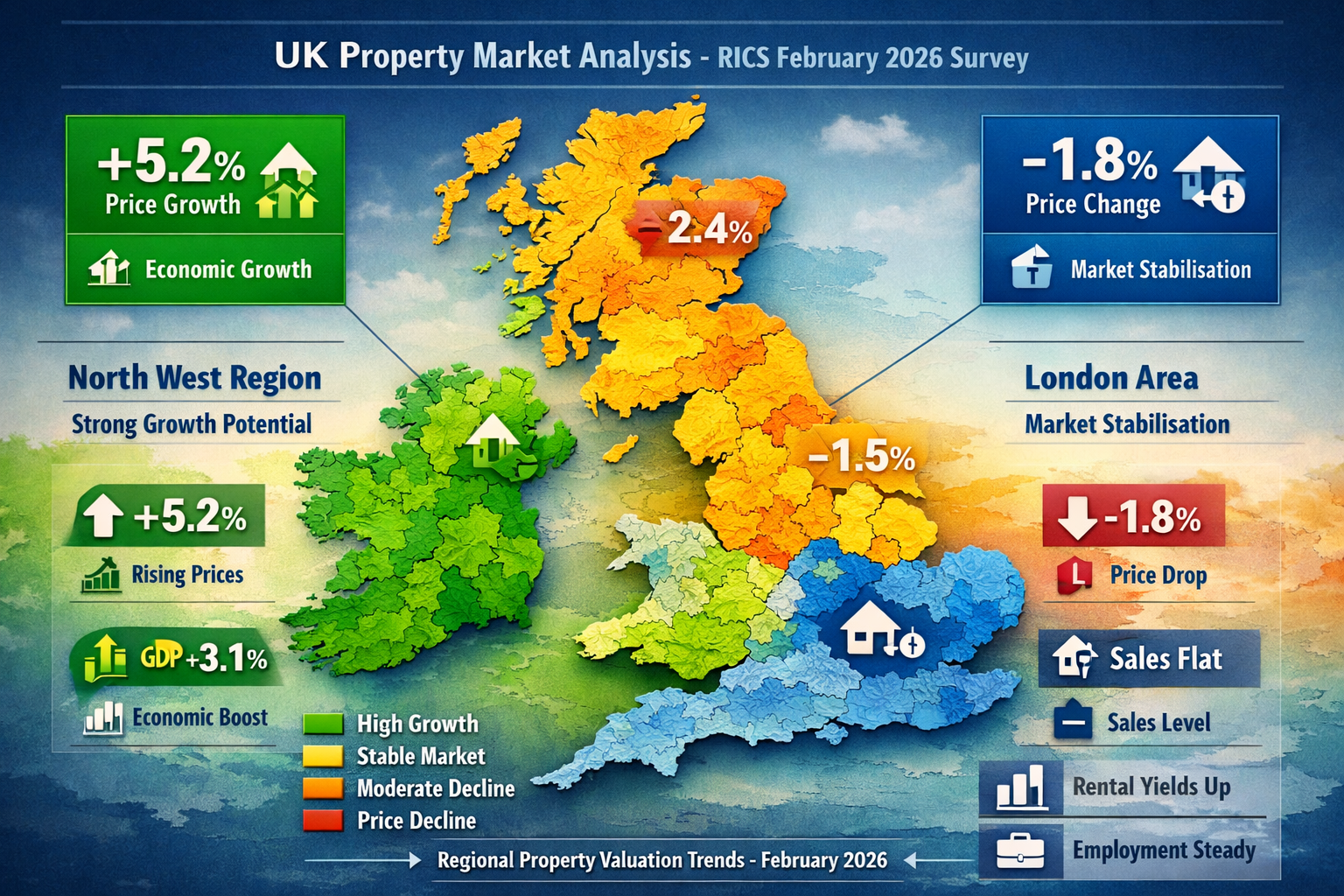

London's property price balance has plummeted to an unprecedented -40% while northern towns like Burnley and Rochdale celebrate gains exceeding 4%—the February 2026 RICS Residential Market Survey reveals a UK housing market split down geographical lines with implications that demand immediate attention from property valuers, surveyors, and investors.[1] This stark divergence between Regional Valuation Strategies Post-RICS February 2026 Survey: North West Growth vs London Price Cooling represents more than statistical variation; it signals a fundamental shift requiring adapted valuation methodologies across different UK markets.

The February 2026 data exposes a property landscape where traditional assumptions about London's perpetual strength no longer hold. Buyer enquiries collapsed to -26%, transaction velocity plunged by approximately 15%, and near-term price expectations deteriorated sharply to -18%.[1][5] Yet beneath these troubling national headlines lies a more nuanced story: the North West of England, Scotland, and Northern Ireland continue demonstrating resilience while southern regions experience acute pressure.

For chartered surveyors and property professionals, this regional divergence demands immediate strategic recalibration. Valuation approaches that worked in a uniformly rising or falling market prove inadequate when Manchester outperforms Mayfair. Understanding these dynamics becomes essential for accurate property assessments, informed client advice, and sound investment decisions in 2026.

Key Takeaways

- London experiences unprecedented weakness with a -40% price balance and 12-month sentiment collapsing from +56% to just +7% in one month

- North West England demonstrates resilience with northern towns recording price gains exceeding 4%, positioning the region among the UK's strongest performers

- Transaction velocity declined sharply by approximately 15% in February, with buyer enquiries dropping to -26% amid geopolitical uncertainty

- Valuation methodologies require regional adaptation based on divergent market conditions, with growth-focused approaches for recovering regions and conservative strategies for cooling markets

- Rental markets remain tight with landlord instructions at -27%, creating ongoing stock shortages that influence regional valuation considerations

Understanding the February 2026 RICS Survey: Key Regional Findings

London's Dramatic Market Deterioration

The capital's property market experienced what can only be described as a confidence crisis in February 2026. The headline price balance dropped to -40%, representing the most severe downward pressure across all UK regions and marking a significant acceleration in the cooling trend that began in late 2025.[1] This figure indicates that 40% more surveyors reported price declines than increases—a level of pessimism not witnessed since the immediate aftermath of previous economic shocks.

Perhaps more concerning for long-term market health, buyer expectations for London prices over the next 12 months plummeted from +56% in January to just +7% in February—a 49-percentage-point collapse in sentiment within a single month.[1] This dramatic shift suggests that market participants have fundamentally reassessed London's near-term prospects, with implications extending well beyond immediate transaction activity.

The South East and East Anglia mirror London's struggles, reporting price balances of -24% and -26% respectively, placing them among the weakest performers nationally.[1] This southern belt of underperformance creates a distinct geographical pattern that property valuers cannot ignore when conducting RICS Homebuyer Surveys or providing market advice to clients.

North West England: The Resilient Outlier

In stark contrast, the North West of England continues to report firmer price trends, positioning itself among the strongest regional performers alongside Scotland and Northern Ireland.[1] Zoopla data reinforces this pattern, showing the highest house price growth over 2025 concentrated in northern towns, with Burnley leading gains, followed by Rochdale, Blackburn, Liverpool, and Wigan—all recording price gains exceeding 4%.[3]

This northern resilience reflects multiple factors:

- Affordability advantages compared to southern regions

- Strong local employment markets in key northern cities

- Continued investment in regional infrastructure and regeneration

- First-time buyer activity concentrated in more accessible price points

- Relative insulation from international investment fluctuations affecting London

The performance gap between regions has widened to levels rarely seen in modern UK property history. RICS and Land Registry data both present Northern Ireland as the strongest performing region across the UK, with the North of England and Scotland also recording solid gains, while London shows negative readings across both datasets.[3]

National Market Indicators Signal Caution

Beyond regional variations, several national indicators from the February 2026 survey warrant attention:

Buyer Enquiries Collapse: New buyer enquiries weakened substantially to a net balance of -26% in February, down from -15% in January, signaling dampened market sentiment across regions.[1] This represents one of the sharpest monthly declines in prospective buyer activity recorded in recent years.

Transaction Velocity Decline: Housing transaction growth plunged from 1.3% (3-month/3-month rate) in January to approximately -15% in February, with Middle East geopolitical events cited as a key factor dampening buyer sentiment.[5] This sudden deceleration suggests external shocks are influencing domestic property decisions more significantly than in previous cycles.

Near-Term Price Expectations Deteriorate: Surveyors' near-term price expectations for all regions fell sharply to -18% in February from -6% in January, reflecting renewed caution driven by geopolitical and macroeconomic uncertainty.[1] This represents the most pessimistic outlook since the market turbulence of 2023.

Supply Dynamics Remain Stable: New instructions (market appraisals) remained in neutral territory at +2%, indicating a broadly stable flow of fresh listings onto the market with little immediate shift in the pipeline of new stock.[2] This stability contrasts with the demand-side weakness, suggesting price adjustments may be necessary to clear inventory in weaker regions.

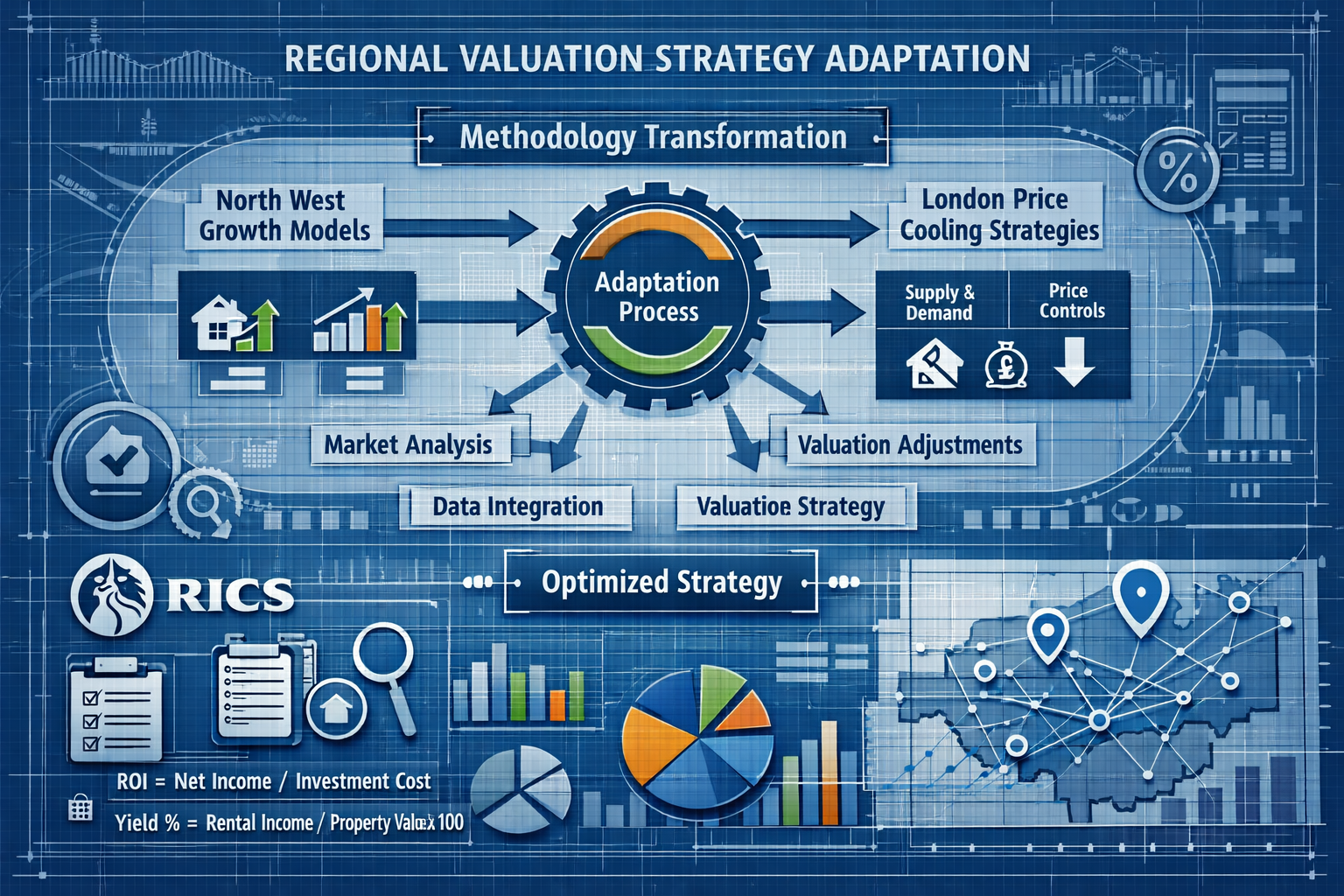

Regional Valuation Strategies Post-RICS February 2026 Survey: Adapting Methodologies

Valuation Principles for Cooling Markets (London and South East)

When conducting property valuations in regions experiencing significant cooling—particularly London, the South East, and East Anglia—chartered surveyors must adopt more conservative approaches that reflect deteriorating sentiment and weakening transaction activity.

Conservative Comparable Selection

The -40% price balance in London demands careful selection of comparable properties. Valuers should:

- Prioritize recent transactions (within the last 3 months) over older sales that may reflect pre-cooling market conditions

- Weight downward adjustments more heavily when comparable properties possess superior characteristics

- Consider withdrawn listings and price reductions as market signals alongside completed transactions

- Apply regional price indices cautiously, recognizing that backward-looking data may overstate current values

For properties in Westminster, Knightsbridge, and Wandsworth, the international buyer withdrawal and sentiment collapse require particular attention to comparable selection from the most recent market period.

Risk-Adjusted Valuation Ranges

Given the 49-percentage-point collapse in 12-month sentiment, providing valuation ranges rather than point estimates offers clients more realistic expectations:

| Market Condition | Recommended Approach | Typical Range Width |

|---|---|---|

| Strong buyer demand | Point estimate or narrow range | ±2-3% |

| Balanced market | Moderate range | ±3-5% |

| Cooling market (London 2026) | Wide range with conservative bias | ±5-8% |

| Distressed/uncertain | Very wide range | ±8-12% |

The lower end of valuation ranges should reflect the possibility of continued deterioration, while the upper end represents values achievable only with optimal marketing and favorable buyer circumstances.

Time-on-Market Adjustments

The -26% buyer enquiry balance suggests extended marketing periods in cooling regions. Valuers should:

- Advise clients on realistic timeframes for achieving asking prices (potentially 6-12 months in current London conditions)

- Factor holding costs into investment valuations, including mortgage interest, maintenance, and opportunity costs

- Consider price reduction strategies in valuation advice, outlining scenarios for achieving quicker sales at lower values

- Document market conditions thoroughly in condition survey reports to manage client expectations

Rental Yield Considerations

With rental prices remaining resilient (20% of participants expect rents to rise over the coming three months) despite capital value cooling, rental yield analysis becomes increasingly important for investment property valuations in London.[1] Properties may justify higher valuations on an income approach basis even as capital values decline, creating opportunities for yield-focused investors.

Valuation Principles for Growth Markets (North West and Northern Regions)

The North West's resilience and northern towns' 4%+ growth rates require different valuation strategies that recognize momentum while avoiding over-exuberance.

Growth-Adjusted Comparable Analysis

In regions like Manchester, Liverpool, and surrounding areas, valuers should:

- Apply positive adjustments for market momentum when comparing to slightly older transactions

- Consider development pipeline and regeneration projects that may enhance future values

- Weight recent upward trends in comparable analysis, recognizing genuine demand fundamentals

- Incorporate regional economic indicators such as employment growth and infrastructure investment

For properties in areas experiencing strong growth, the challenge becomes distinguishing sustainable appreciation from temporary spikes. Surveyors must balance optimism with professional skepticism.

First-Time Buyer Market Dynamics

Northern growth is significantly driven by first-time buyer activity, which influences valuation considerations:

- Entry-level properties (typically under £200,000) may command premium valuations relative to higher-priced stock

- Help to Buy and government scheme eligibility can enhance values for qualifying properties

- Mortgage accessibility at lower price points supports stronger demand fundamentals

- Rental investment potential remains attractive given the -27% landlord instruction balance nationally[1]

First-time buyers seeking properties in growth regions benefit from understanding these dynamics when commissioning surveys and valuations.

New Build Premium Considerations

Northern regions often feature significant new build activity. Valuers must carefully assess:

- Developer incentives and their impact on true market value

- New build premiums versus established property stock

- Quality variations between volume builders and premium developers

- Snagging and defect risks that may affect initial valuations

Understanding whether a building survey is needed for new builds helps buyers in growth markets make informed decisions about property condition alongside valuation considerations.

Momentum Indicators in Valuation Reports

When valuing properties in the North West and other growth regions, incorporating forward-looking momentum indicators provides clients with fuller context:

- Local transaction velocity trends (rising or stable versus declining nationally)

- Days on market comparisons between the subject region and national averages

- Buyer enquiry levels specific to the local market

- Regional economic forecasts from credible sources

- Infrastructure investment timelines that may enhance future values

These indicators help clients understand whether current valuations reflect temporary conditions or sustainable regional advantages.

Adapting Survey Recommendations Based on Regional Conditions

The divergent market conditions revealed in the February 2026 RICS survey should influence not only valuation figures but also the advice and recommendations chartered surveyors provide to clients.

London and Cooling Market Recommendations

For properties in cooling markets, surveyors should:

✅ Emphasize condition over price: With values declining, property condition becomes relatively more important. Buyers gain leverage to negotiate repairs or price reductions based on defects identified in surveys.

✅ Recommend comprehensive surveys: The Level 2 vs Level 3 survey decision tilts toward more comprehensive options when market conditions favor buyers and negotiation opportunities exist.

✅ Highlight negotiation leverage: Survey reports should explicitly note where identified defects provide grounds for price renegotiation, given the -40% price balance and weak buyer demand.[1]

✅ Advise caution on improvements: Major renovation projects may not generate positive returns in cooling markets, suggesting buyers focus on properties requiring minimal work.

✅ Consider timing strategies: For sellers, surveys might recommend addressing major defects before marketing to avoid providing buyers with additional negotiation ammunition in a weak market.

North West and Growth Market Recommendations

For properties in growth regions, surveyor advice shifts:

✅ Focus on structural integrity: With competition for properties potentially stronger, buyers should prioritize identifying serious structural issues that could affect long-term value rather than minor cosmetic concerns.

✅ Emphasize future-proofing: Survey recommendations might focus on improvements that enhance long-term value in appreciating markets, such as energy efficiency upgrades or space optimization.

✅ Realistic about negotiation: While defects should still be reported, surveyors should acknowledge that sellers in strong markets may be less willing to negotiate, requiring buyers to factor repair costs into their overall budget.

✅ Highlight investment potential: For buy-to-let investors, surveys in growth regions should emphasize rental yield potential and tenant appeal factors alongside structural condition.

✅ Speed and decisiveness: Survey reports might note that prolonged decision-making in strong markets risks losing properties to competing buyers, suggesting streamlined survey processes where appropriate.

Practical Implementation: Regional Valuation Strategies in Action

Case Study Approach: Valuing Similar Properties in Different Regions

Consider two comparable properties to illustrate Regional Valuation Strategies Post-RICS February 2026 Survey: North West Growth vs London Price Cooling:

Property A: 3-bedroom Victorian terrace, London (Wandsworth)

- Last sold: June 2025 for £850,000

- Comparable sales (Nov 2025-Jan 2026): £820,000-£860,000

- Regional price balance: -40%

- 12-month sentiment: +7% (collapsed from +56%)

Property B: 3-bedroom Victorian terrace, Manchester (Chorlton)

- Last sold: June 2025 for £425,000

- Comparable sales (Nov 2025-Jan 2026): £430,000-£450,000

- Regional price balance: Positive (firmer trends)

- Northern town growth: 4%+ in surrounding areas

London Property Valuation Approach

For Property A, a conservative February 2026 valuation would:

- Weight recent comparables heavily: The £820,000 sale (January 2026) receives greater weight than the £860,000 sale (November 2025)

- Apply downward adjustment: Given the -40% price balance and sentiment collapse, a 2-3% downward adjustment from recent comparables is justified

- Provide range estimate: £795,000-£825,000, with commentary noting that achieving the upper end requires optimal marketing and buyer circumstances

- Note extended marketing period: 6-9 months to achieve asking price in current conditions

- Highlight rental yield: If rental income is £2,800/month (£33,600 annually), the gross yield of 4.1-4.2% may attract investor interest despite capital value concerns

This approach reflects the market reality documented in the RICS survey while providing clients with actionable information for decision-making.

Manchester Property Valuation Approach

For Property B, a growth-aware February 2026 valuation would:

- Recognize positive momentum: The £450,000 comparable (January 2026) reflects genuine demand strength

- Apply modest upward adjustment: A 1-2% adjustment from recent comparables acknowledges regional growth trends

- Provide tighter range: £448,000-£462,000, reflecting greater market certainty

- Note competitive conditions: Properties at realistic asking prices may receive multiple offers

- Emphasize investment fundamentals: Strong rental demand (landlord instructions -27% nationally) and capital growth potential[1]

The contrast between these approaches demonstrates how the same professional standards produce different valuations when properly adapted to regional conditions.

Integrating RICS Survey Data into Valuation Reports

Professional surveyors should explicitly reference the February 2026 RICS survey findings in valuation reports to provide clients with market context:

Essential Data Points to Include:

📊 Regional price balance: State whether the subject property's region shows positive, neutral, or negative price trends

📊 Buyer enquiry trends: Note the -26% national figure and any regional variations affecting demand[1]

📊 Transaction velocity: Reference the -15% decline and its implications for marketing timelines[5]

📊 Near-term expectations: Include the -18% near-term price expectation figure to set realistic client expectations[1]

📊 Supply dynamics: Note the +2% new instructions balance and what it means for market inventory[2]

📊 Rental market conditions: Reference the -27% landlord instructions and rental price resilience for investment properties[1]

This data integration transforms valuation reports from simple price opinions into comprehensive market analyses that help clients make informed decisions. For those preparing for surveys, understanding what to do before an RICS home survey ensures the process runs smoothly.

Advising Clients on Regional Market Selection

The stark divergence between regional performance creates opportunities for strategic property investment and relocation decisions. Chartered surveyors increasingly find themselves advising clients on regional market selection alongside traditional valuation services.

For Buyers Considering Multiple Regions

Clients with flexibility regarding location should receive advice incorporating:

London/South East Advantages:

- Potential value opportunities as prices cool

- Established infrastructure and amenities

- International connectivity

- Long-term capital growth history (despite current weakness)

- Rental demand remains strong despite capital value cooling

London/South East Disadvantages:

- -40% price balance indicates continued near-term weakness

- 12-month sentiment collapse suggests prolonged recovery period

- Higher absolute prices limit affordability

- Greater exposure to international market volatility

- Extended time-on-market in current conditions

North West/Northern Region Advantages:

- Positive momentum with 4%+ growth in key towns

- Superior affordability enables larger properties or lower mortgage commitments

- Strong first-time buyer and rental investment fundamentals

- Regional economic growth and infrastructure investment

- Shorter time-on-market in competitive local markets

North West/Northern Region Disadvantages:

- Smaller absolute capital gains despite higher percentage growth

- Potentially lower liquidity if resale becomes necessary

- Less established in international buyer consciousness

- Infrastructure gaps compared to London (though improving)

- Economic concentration risks in some local economies

For Investors Seeking Optimal Returns

Property investors benefit from understanding how the February 2026 RICS data influences regional investment strategies:

Capital Growth Focus: The North West and northern towns currently offer superior capital growth prospects, with Burnley, Rochdale, and Liverpool leading gains.[3] Investors prioritizing appreciation should concentrate on these markets.

Yield Focus: London's cooling capital values combined with resilient rental prices (20% of surveyors expect rent increases) create enhanced gross yields.[1] Income-focused investors may find value in London despite capital value concerns.

Balanced Approach: Scotland and Northern Ireland demonstrate both capital growth and rental market strength, potentially offering balanced risk-return profiles.

Risk Considerations: The -26% buyer enquiry balance and -15% transaction velocity decline suggest overall market caution.[1][5] Investors should maintain adequate liquidity reserves and avoid over-leveraging regardless of regional selection.

Rental Market Implications for Valuation Strategies

The February 2026 RICS survey reveals acute rental stock shortages with landlord instructions remaining firmly negative at -27%.[1] This dynamic influences regional valuation strategies significantly.

Rental Valuation Adjustments

Properties suitable for rental investment warrant specific valuation considerations:

Yield Compression in Growth Markets: Strong capital growth in the North West may lead to yield compression as property prices rise faster than rents can adjust. Investors should calculate realistic net yields after:

- Mortgage costs (current interest rate environment)

- Maintenance and management fees

- Void periods

- Regulatory compliance costs

Yield Enhancement in Cooling Markets: London properties may offer counter-cyclical rental investment opportunities where:

- Capital values have cooled but rental demand remains strong

- Gross yields improve as purchase prices decline

- Long-term capital appreciation potential remains (despite near-term weakness)

- Tenant demand supported by continued employment in key sectors

Regional Rental Demand Variations: The -27% landlord instructions figure is national, but regional variations exist. Surveyors should research local rental market conditions through:

- Local letting agent consultations

- Rental listing analysis (days to let, achieved rents vs. asking rents)

- Tenant demographic research

- Local employment and university enrollment trends

Build-to-Rent Development Opportunities

The persistent rental stock shortage creates opportunities for build-to-rent development in both growth and cooling markets:

North West Build-to-Rent: Strong capital growth combined with rental demand suggests development viability in key northern cities. Valuers assessing development sites should consider:

- Planning policy support for residential development

- Construction cost inflation (currently moderating)

- Exit yield assumptions for completed developments

- Tenant demand sustainability beyond current cycle

London Build-to-Rent: Despite capital value cooling, London's rental resilience supports build-to-rent development, particularly in:

- Transport-connected locations

- Areas with employment growth

- Neighborhoods undergoing regeneration

- Locations with limited existing rental stock

Chartered surveyors involved in development valuations must carefully assess how regional market divergence affects residual land values and development viability.

Geopolitical and Macroeconomic Factors Influencing Regional Strategies

The February 2026 RICS survey explicitly cites Middle East geopolitical events as a key factor dampening buyer sentiment and contributing to the -15% transaction velocity decline.[5] Understanding these broader influences helps surveyors provide comprehensive advice.

External Shocks and Regional Resilience

Different UK regions demonstrate varying sensitivity to external economic and geopolitical shocks:

London's International Exposure: The capital's -40% price balance partly reflects its greater exposure to:

- International buyer sentiment and capital flows

- Global financial market volatility

- Currency fluctuations affecting overseas purchasers

- Geopolitical risk perceptions among international investors

Northern Regional Insulation: The North West's resilience may partly stem from:

- Domestic buyer dominance (less international exposure)

- Local economic fundamentals driving demand

- Affordability supporting first-time buyer activity regardless of global conditions

- Regional policy support and infrastructure investment

Interest Rate Sensitivity by Region

While the RICS survey doesn't explicitly detail interest rate impacts, the transaction velocity decline and buyer enquiry weakness occur against a backdrop of elevated mortgage costs. Regional sensitivity varies:

Higher Absolute Price Regions (London, South East): More sensitive to interest rate changes because:

- Larger mortgage amounts mean greater absolute interest cost increases

- Buyers at affordability limits face payment shock

- International buyers may find alternative markets more attractive

- Investor yields compress more significantly

Lower Absolute Price Regions (North West, Northern towns): Demonstrate relative resilience because:

- Smaller mortgage amounts mean lower absolute interest cost increases

- First-time buyers can still achieve affordability at entry levels

- Rental yields remain attractive even with higher mortgage costs

- Local buyer dominance reduces international capital flow sensitivity

Surveyors should incorporate interest rate sensitivity into valuation advice, particularly when advising clients on regional selection and investment strategy.

Future Outlook: Navigating Continued Regional Divergence

The February 2026 RICS survey data suggests regional divergence will persist through at least the first half of 2026, requiring ongoing adaptation of valuation strategies.

Monitoring Key Indicators

Chartered surveyors should track several indicators to refine regional valuation approaches:

📈 Monthly RICS survey updates: Regional price balances, buyer enquiries, and sales expectations

📈 Transaction volume data: Actual completions versus survey sentiment indicators

📈 Mortgage approval figures: Regional breakdowns of lending activity

📈 Rental market metrics: Void periods, achieved rents, tenant demand indicators

📈 Economic indicators: Regional employment, wage growth, and business investment

📈 Policy developments: Planning reforms, taxation changes, regional development initiatives

Scenario Planning for Clients

Given the uncertainty reflected in the -18% near-term price expectations and geopolitical concerns, surveyors should help clients develop scenario-based strategies:[1]

Optimistic Scenario (30% probability): Geopolitical tensions ease, interest rates decline, buyer confidence returns

- London recovery begins Q3 2026

- North West growth moderates but remains positive

- Transaction volumes normalize

- Valuation implication: Current London prices represent value; North West may see modest yield compression

Base Case Scenario (50% probability): Gradual stabilization with continued regional divergence

- London stabilizes at current levels through mid-2026, modest recovery late 2026

- North West continues moderate growth (2-3% annually)

- Transaction volumes remain subdued but stable

- Valuation implication: Current regional patterns persist; strategy differentiation remains essential

Pessimistic Scenario (20% probability): Prolonged economic weakness, further geopolitical deterioration

- London experiences additional 5-10% decline

- North West growth stalls

- Transaction volumes decline further

- Valuation implication: Conservative valuations justified across all regions; cash preservation prioritized

These scenarios help clients understand the range of possible outcomes and make decisions aligned with their risk tolerance and investment horizons.

Conclusion

The February 2026 RICS Residential Market Survey exposes a UK property market experiencing unprecedented regional divergence, with London's -40% price balance and sentiment collapse contrasting sharply with the North West's resilience and northern towns' 4%+ growth rates.[1][3] This geographic split demands immediate adaptation of valuation methodologies, with chartered surveyors applying conservative, risk-adjusted approaches in cooling markets while recognizing genuine growth fundamentals in recovering regions.

Regional Valuation Strategies Post-RICS February 2026 Survey: North West Growth vs London Price Cooling requires professional surveyors to move beyond one-size-fits-all approaches. London valuations must reflect the 49-percentage-point sentiment collapse, -26% buyer enquiry balance, and -15% transaction velocity decline through wider valuation ranges, recent comparable prioritization, and extended marketing period assumptions.[1][5] Conversely, North West and northern region valuations should acknowledge positive momentum, first-time buyer strength, and regional economic fundamentals while maintaining professional skepticism about sustainability.

The rental market's resilience—with 20% of surveyors expecting rent increases despite capital value cooling—creates counter-cyclical opportunities in London for yield-focused investors, while the -27% landlord instructions figure signals ongoing supply constraints that support rental valuations across all regions.[1] Surveyors must integrate these dynamics into comprehensive advice that considers both capital growth and income return potential.

Actionable Next Steps

For property buyers: Commission comprehensive surveys in cooling markets where negotiation leverage exists, and act decisively in growth markets where competition remains strong. Understand homebuyer survey options to select appropriate inspection levels for different market conditions.

For property sellers: In London and the South East, address major defects before marketing to avoid providing buyers additional negotiation ammunition. In growth regions, ensure realistic pricing that reflects genuine market conditions rather than outdated assumptions.

For investors: Consider regional diversification strategies that balance growth potential (North West) with yield opportunities (London). Maintain adequate liquidity reserves given the -18% near-term price expectations and ongoing geopolitical uncertainty.[1]

For chartered surveyors: Continuously monitor monthly RICS survey updates and regional transaction data to refine valuation approaches. Explicitly reference survey findings in valuation reports to provide clients with essential market context. Develop regional expertise that enables nuanced advice reflecting local conditions rather than national averages.

The February 2026 RICS survey confirms that successful navigation of the current property market requires geographic specificity, data-driven analysis, and willingness to adapt traditional methodologies to divergent regional realities. Those who embrace these regional valuation strategies will provide superior client service and achieve better outcomes in an increasingly complex UK property landscape.

References

[1] Uk Residential Survey February 2026 – https://www.rics.org/news-insights/uk-residential-survey-february-2026

[2] Uk Residential Market Survey February 2026 – https://www.rics.org/content/dam/ricsglobal/documents/market-surveys/uk-residential-market-survey/UK-Residential-Market-Survey_February-2026.pdf

[3] Uk Economy Property Update February 2026 – https://www.rics.org/content/dam/ricsglobal/documents/market-surveys/uk-economy-property-update-february-2026.pdf

[4] Valuation Impacts Of February 2026 Rics Survey Strategies For Regional Price Divergence In Uk Markets – https://nottinghillsurveyors.com/blog/valuation-impacts-of-february-2026-rics-survey-strategies-for-regional-price-divergence-in-uk-markets

[5] Uk Rics Residential Market Survey Feb 2026 – https://www.capitaleconomics.com/publications/uk-housing-market-update/uk-rics-residential-market-survey-feb-2026

[6] Regional Valuation Divergences In 2026 Recovery Rics Tactics For North South Price Shifts In Building Surveys – https://nottinghillsurveyors.com/blog/regional-valuation-divergences-in-2026-recovery-rics-tactics-for-north-south-price-shifts-in-building-surveys