Lenders processing mortgage applications for non-standard properties—high-rise condominiums, mixed-use developments, historic conversions—face a persistent challenge: survey delays that can stretch transaction timelines from days into weeks. In 2026, artificial intelligence systems now deliver property valuations in under 60 seconds, compared to the 3-5 days required for traditional appraisals.[2] This dramatic acceleration isn't just about speed; it's fundamentally transforming how lenders approach Early Property Data Tech for Complex Valuations: Lender Strategies to Avoid 2026 Survey Delays, enabling smarter upfront decisions about which properties require full physical surveys versus desktop assessments.

The stakes are considerable. Every delayed survey costs lenders time, money, and potentially the entire transaction. Yet rushing through complex valuations without adequate data creates equally serious risks. Modern property data technology offers a solution: comprehensive preliminary insights that help valuers and lenders make efficient, evidence-based decisions about survey scope before committing resources.

Key Takeaways

- AI-powered valuations achieve 94% accuracy compared to 85-90% for traditional methods, with variance margins under 3% in established markets[1][2]

- Multi-source data integration combining MLS records, tax data, climate assessments, and infrastructure proximity provides comprehensive risk profiles for non-standard properties[3]

- Cost reduction of 95%+: AI valuations cost $5-15 versus $300-500+ for manual appraisals, enabling thorough preliminary assessments[2]

- Hybrid human-AI models deliver optimal results for complex properties, combining algorithmic speed with expert judgment for unique characteristics[2]

- Predictive forecasting with 91% accuracy for 6-month projections helps lenders assess default risk early in the process[2]

Understanding the 2026 Survey Delay Challenge for Non-Standard Properties

Traditional property surveys follow a linear process: application submission, surveyor assignment, physical inspection scheduling, report compilation, and final delivery. For standard residential properties, this system functions adequately. However, non-standard properties present unique complications that exponentially increase processing time.

Why Complex Properties Create Bottlenecks

High-rise buildings, mixed-use developments, and properties with unusual characteristics demand specialized expertise. A surveyor assessing a 30-story condominium must evaluate:

- Structural integrity across multiple levels and shared systems

- Common area valuations and maintenance obligations

- Comparative market analysis with limited directly comparable sales

- Legal complexities involving leasehold arrangements and service charges

- Future development impacts from surrounding infrastructure projects

Each factor requires additional research, consultation, and analysis time. When multiple lenders request surveys simultaneously during peak market periods, qualified surveyors become overwhelmed, creating cascading delays throughout the system.

The Cost of Waiting

Survey delays impose tangible costs on all parties:

💰 Lenders risk losing competitive loan opportunities to faster competitors

🏠 Buyers face extended uncertainty and potential rate lock expirations

📊 Surveyors experience capacity constraints limiting revenue potential

⏰ Transactions become vulnerable to market fluctuations during extended timelines

Traditional approaches lack mechanisms to prioritize which properties genuinely require comprehensive physical surveys versus those that could proceed with desktop valuations supplemented by robust data analysis. This is where Early Property Data Tech for Complex Valuations: Lender Strategies to Avoid 2026 Survey Delays becomes essential.

How Early Property Data Tech Transforms Complex Valuation Workflows

Modern property data technology fundamentally changes the valuation timeline by frontloading comprehensive analysis. Rather than waiting for physical survey results to inform decisions, lenders can now access detailed property intelligence within minutes of receiving an application.

Automated Valuation Models (AVMs) for Initial Assessment

Generative AI-powered AVMs represent the current industry standard for preliminary valuations.[1] These systems simultaneously analyze millions of data points, including:

- Historical sales data across multiple timeframes

- Neighborhood trend analysis and demographic shifts

- Economic indicators affecting local property markets

- Social media sentiment about specific areas or developments

- Proximity to infrastructure projects and amenities

The accuracy metrics are compelling. AI-powered valuations achieve 94% accuracy compared to 85-90% for traditional appraisals, with variance margins reduced to less than 3% in established markets versus 10-15% for conventional methods.[1][2]

For lenders evaluating a complex high-rise property, an AVM can instantly provide:

✅ Estimated market value range with confidence intervals

✅ Comparable sales analysis from similar developments

✅ Market trend trajectory for the specific submarket

✅ Risk factors flagged for further investigation

✅ Recommendation for survey scope (desktop vs. full physical inspection)

Machine Learning Algorithms for Complex Scenarios

Advanced machine learning algorithms, particularly Random Forest and XGBoost models, can achieve up to 93% accuracy (R²) when processing complex property scenarios.[2] These algorithms excel at identifying non-linear relationships between property characteristics and values—critical for non-standard properties where traditional valuation approaches struggle.

For example, a mixed-use development combining retail, office, and residential components presents valuation challenges that simple comparable sales analysis cannot address. Machine learning models can:

- Weight different income streams appropriately

- Account for synergistic value creation between uses

- Identify market-specific premium or discount factors

- Incorporate foot traffic analytics and economic indicators

- Adjust for unique architectural or design features

This capability enables lenders to understand complex properties with unprecedented depth before committing to expensive, time-consuming physical surveys. When working with property surveyors across London, lenders can provide detailed preliminary data that helps surveyors focus their physical inspection on genuinely uncertain elements rather than replicating analysis already completed through data technology.

Essential Data Sources for Early Property Data Tech for Complex Valuations: Lender Strategies to Avoid 2026 Survey Delays

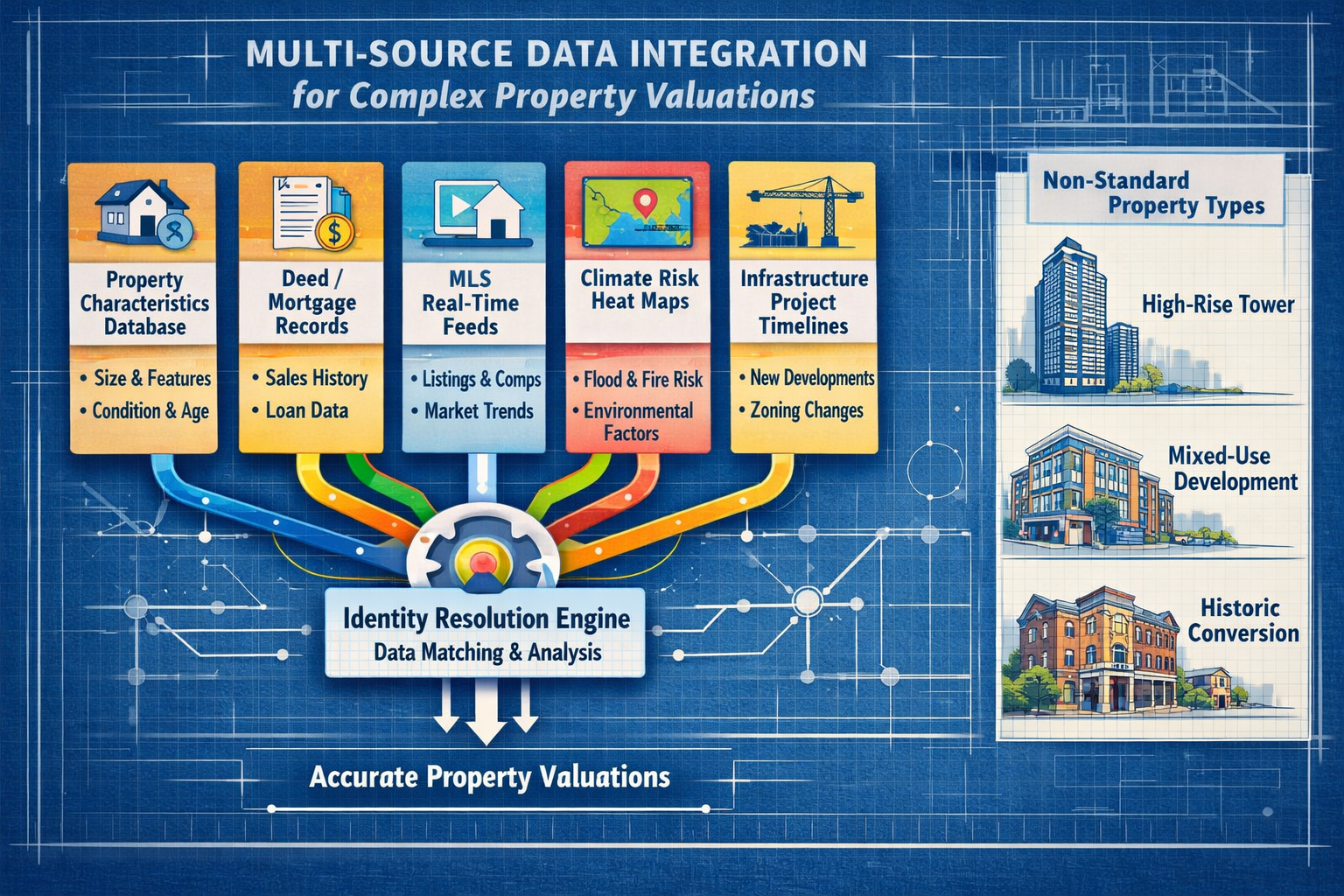

The effectiveness of early property data technology depends entirely on data quality and comprehensiveness. Best-practice lender strategies integrate multiple data sources simultaneously, with internal identity resolution systems preventing double-counting and mismatches.[3]

The Four Critical Data Pillars

According to industry analysis of real estate data providers in 2026, lenders should prioritize four essential dataset categories:[3]

1. Property Characteristics and Parcel Data

This foundational layer includes:

- Detailed property specifications (square footage, room count, construction materials)

- Parcel boundaries and lot dimensions

- Zoning classifications and permitted uses

- Building age, renovation history, and condition indicators

- Energy efficiency ratings and environmental certifications

For complex properties like high-rises, this data must extend beyond individual units to encompass common areas, shared facilities, and building-wide systems. Comprehensive parcel data enables accurate preliminary valuations without physical inspection.

2. Deed and Mortgage Transaction Records

Ownership tracking provides critical context for valuations:

- Complete chain of title information

- Historical sale prices and transaction dates

- Existing mortgage liens and encumbrances

- Ownership structure (freehold, leasehold, shared ownership)

- Legal restrictions or covenants affecting value

For non-standard properties, understanding the legal structure is particularly important. A luxury high-rise condominium might involve complex leasehold arrangements, service charge obligations, or restrictions on subletting—all factors affecting value that data technology can surface before physical survey.

3. MLS Listing and Sale Data

Multiple Listing Service data provides near real-time pricing signals essential for accurate valuations:

- Active listings with asking prices and marketing duration

- Pending sales indicating market velocity

- Completed transactions with final sale prices

- Days on market and price reduction history

- Property descriptions and marketing photographs

For complex valuations, MLS data must be analyzed with sophistication. A building survey specialist in areas like Bromley or Croydon understands that comparable sales for unique properties require careful adjustment—something modern AI systems can perform systematically across thousands of potential comparables.

4. AVM-Ready Data for Bulk Processing

Specialized datasets optimized for algorithmic processing include:

- Standardized property attributes formatted for machine learning

- Geocoded location data with precision coordinates

- Time-series market indicators and economic variables

- Neighborhood characteristic scores (walkability, school quality, crime rates)

- Environmental risk factors (flood zones, earthquake susceptibility)

Unconventional Data Sources for Comprehensive Risk Assessment

Beyond traditional datasets, modern AI systems incorporate unconventional factors that traditional appraisals cannot systematically capture:[1]

🏗️ Infrastructure Project Proximity: Planned transportation improvements, commercial developments, or public facilities that will affect future values

🌍 Climate Risk Assessments: Flood risk projections, heat island effects, wildfire exposure, and other environmental factors increasingly important to property values

📊 Demographic Shift Analysis: Population movement patterns, age distribution changes, and income trajectory forecasts for specific neighborhoods

These factors prove particularly relevant for complex properties where long-term value trajectories matter more than current comparable sales. A high-rise development near a planned transit station might warrant premium valuation despite limited current comparables—insight that data technology can quantify systematically.

Specialized Data for Early Risk Detection

For lenders focused on risk management, additional specialized datasets provide early warning signals:[3]

- Building permit and renovation data: Indicates property improvement activity or potential compliance issues

- Pre-foreclosure indicators: Identifies properties entering financial distress before formal proceedings

- Legal filing events: Flags liens, judgments, or disputes affecting property value

- Code violation records: Reveals maintenance issues or regulatory non-compliance

These datasets enable lenders to identify red flags immediately upon application receipt, determining whether a property requires enhanced due diligence or specialized survey attention. When working with surveyors in areas like Kingston or Wandsworth, providing this preliminary risk intelligence helps focus physical inspection resources efficiently.

Implementing Hybrid Human-AI Strategies for Complex Valuations

While property data technology offers remarkable capabilities, the most successful lender strategies combine algorithmic speed with human judgment.[2] This hybrid approach addresses the limitations of both pure automation and traditional manual processes.

When AI Excels: Standard Characteristics and Pattern Recognition

AI systems demonstrate clear superiority for properties with:

✓ Abundant comparable sales data

✓ Standard construction and design features

✓ Established neighborhoods with stable market patterns

✓ Complete and accurate property records

✓ Typical ownership structures and legal arrangements

For these properties, AI can deliver valuations that are faster, cheaper, and often more accurate than traditional appraisals. The cost differential is substantial: $5-15 for AI valuations versus $300-500+ for manual appraisals.[2] This economic advantage enables lenders to conduct thorough preliminary assessments across entire application portfolios without proportional budget increases.

When Human Expertise Remains Essential: Unique Properties and Judgment Calls

Conversely, human surveyors provide irreplaceable value for properties with:

⚠️ Unique architectural features or historical significance

⚠️ Limited or no comparable sales in the immediate market

⚠️ Complex legal structures or unusual ownership arrangements

⚠️ Visible condition issues requiring physical inspection

⚠️ Recent renovations or modifications not reflected in records

⚠️ Subjective quality factors affecting buyer appeal

A comprehensive building survey conducted by experienced professionals captures nuances that no algorithm can replicate. The surveyor's physical inspection reveals condition issues, quality of construction, and maintenance requirements that fundamentally affect value but don't appear in data records.

The Optimal Workflow: Data-Informed Survey Decisions

The most effective implementation of Early Property Data Tech for Complex Valuations: Lender Strategies to Avoid 2026 Survey Delays follows this workflow:

Step 1: Immediate AI Assessment

Upon application receipt, run comprehensive AVM analysis incorporating all available data sources. Generate preliminary valuation with confidence intervals and risk flags.

Step 2: Risk Stratification

Categorize properties based on AI confidence levels:

- High confidence (>90%): Proceed with desktop valuation supplemented by automated data verification

- Medium confidence (75-90%): Commission targeted survey focusing on specific uncertainty areas

- Low confidence (<75%): Request comprehensive physical survey with full inspection

Step 3: Surveyor Briefing

For properties requiring physical survey, provide surveyors with complete AI analysis results, including:

- Preliminary valuation estimate and methodology

- Comparable sales analysis with adjustments

- Identified risk factors requiring verification

- Specific questions or uncertainties for surveyor attention

Step 4: Human Validation and Adjustment

Surveyors review AI findings, conduct physical inspection, and apply professional judgment to validate or adjust preliminary conclusions. This focused approach reduces survey time by 30-50% while improving accuracy.

Step 5: Continuous Learning

Feed surveyor findings back into AI systems to improve future predictions. This creates a virtuous cycle where human expertise enhances algorithmic performance over time.

Predictive Forecasting for Proactive Risk Management

Advanced AI platforms now provide predictive value forecasting with impressive accuracy: 91% for 6-month projections and 83% for 12-month forecasts.[2] This capability transforms lender risk assessment from reactive to proactive.

For complex properties, predictive forecasting helps lenders:

📈 Assess default risk based on projected value trajectories

📉 Identify overvalued markets before corrections occur

🎯 Optimize loan-to-value ratios based on future value expectations

⚡ Detect refinance opportunities early in market cycles

🛡️ Manage portfolio exposure to specific property types or locations

When evaluating a high-rise development, lenders can model various scenarios: What if planned infrastructure projects are delayed? How would economic downturn affect occupancy rates? What's the probability of value appreciation exceeding inflation? These questions, previously requiring extensive manual analysis, now receive data-driven answers within minutes.

Practical Implementation: Lender Technology Stack for 2026

Implementing effective Early Property Data Tech for Complex Valuations: Lender Strategies to Avoid 2026 Survey Delays requires careful technology selection and integration. Lenders should evaluate potential solutions across several dimensions:

Data Coverage and Refresh Frequency

The value of property data technology depends fundamentally on data comprehensiveness and currency. When evaluating providers, assess:[3][4]

- Geographic coverage: Does the provider cover all markets where you originate loans?

- Update frequency: How often are records refreshed? Daily updates matter for active markets.

- Historical depth: Can you access transaction history spanning multiple market cycles?

- Data completeness: What percentage of properties have full characteristic data?

- Accuracy verification: How does the provider validate data quality?

For lenders operating across diverse markets—from Lewisham to Ealing—consistent data quality across all locations is essential. Gaps in coverage force fallback to traditional processes, undermining efficiency gains.

API Integration and Workflow Automation

Technology solutions should integrate seamlessly with existing loan origination systems:

- RESTful APIs for real-time valuation requests during application processing

- Bulk processing capabilities for portfolio analysis and periodic revaluation

- Webhook notifications for data updates affecting active loan files

- Standardized data formats compatible with underwriting platforms

- Authentication and security meeting regulatory requirements

The goal is zero-friction integration where valuations occur automatically as part of normal workflow, not as separate manual processes requiring data export and import.

Licensing Models and Cost Structure

Property data providers offer various licensing arrangements:[3]

- Per-query pricing: Pay for each valuation request (suitable for lower volumes)

- Subscription access: Unlimited queries within defined parameters (better for high volumes)

- Hybrid models: Base subscription plus overage charges

- Data licensing: Purchase datasets for internal modeling

For lenders implementing Early Property Data Tech for Complex Valuations: Lender Strategies to Avoid 2026 Survey Delays, subscription models typically provide better economics once monthly query volumes exceed 100-200 properties. However, cost analysis must account for the $300-500+ savings per avoided physical survey—even per-query pricing delivers substantial ROI.

Compliance and Regulatory Considerations

Property valuation technology must satisfy regulatory requirements:

✓ Fair lending compliance: Algorithms must not introduce discriminatory bias

✓ Appraisal independence: Maintain appropriate separation between valuation and lending decisions

✓ Documentation standards: Generate reports meeting investor and regulatory requirements

✓ Audit trails: Maintain complete records of valuation inputs and methodology

✓ Model validation: Regular testing and validation of algorithmic accuracy

Lenders should work with technology providers offering compliance-ready solutions with built-in documentation and audit capabilities. The speed advantages of AI valuations disappear if regulatory challenges create downstream delays.

Measuring Success: KPIs for Early Property Data Technology

Effective implementation requires systematic performance measurement. Lenders should track these key performance indicators:

Efficiency Metrics

📊 Average time to preliminary valuation: Target <5 minutes from application receipt

📊 Percentage of loans processed with desktop valuations: Benchmark 40-60% for standard portfolios

📊 Survey turnaround time: Measure reduction in days from application to completed survey

📊 Surveyor productivity: Track surveys completed per surveyor per month

Accuracy Metrics

🎯 Variance between preliminary and final valuations: Target <5% for desktop valuations

🎯 Accuracy of survey scope predictions: Percentage of desktop valuations not requiring subsequent physical survey

🎯 Default rate correlation: Compare predicted risk scores to actual default experience

🎯 Forecast accuracy: Track 6-month and 12-month value predictions against actual market movements

Financial Metrics

💰 Cost per valuation: Compare blended costs to previous all-manual approach

💰 Survey cost savings: Calculate avoided expenses from reduced physical surveys

💰 Pull-through rate improvement: Measure increased application completion from faster processing

💰 Portfolio performance: Track default rates and loss severity for loans originated with data technology

Competitive Metrics

⚡ Application to approval timeline: Compare to market competitors

⚡ Market share trends: Monitor whether faster processing increases origination volume

⚡ Borrower satisfaction scores: Survey applicants about process speed and transparency

⚡ Referral partner feedback: Track broker and real estate agent preferences

Regular review of these metrics enables continuous refinement of Early Property Data Tech for Complex Valuations: Lender Strategies to Avoid 2026 Survey Delays, identifying opportunities for further optimization.

Future Trends: What's Next for Property Data Technology

The 40% growth projection in AI adoption across real estate[1] suggests rapid continued evolution. Several emerging trends will shape the next generation of property data technology:

Expanded Alternative Data Sources

Future systems will incorporate increasingly diverse data:

- Satellite imagery analysis detecting property condition changes, construction activity, and environmental factors

- IoT sensor data from smart buildings providing real-time condition monitoring

- Social media and review data capturing neighborhood sentiment and livability factors

- Traffic and mobility patterns indicating area accessibility and desirability

- Employment and economic microdata forecasting local market trajectories

These unconventional sources will enable even more accurate valuations for complex properties where traditional comparables provide limited insight.

Blockchain for Data Verification

Distributed ledger technology promises to address persistent data quality challenges:

- Immutable transaction records eliminating discrepancies between data sources

- Smart contracts automating data updates when property events occur

- Decentralized verification reducing reliance on single authoritative sources

- Transparent audit trails improving regulatory compliance

While blockchain adoption remains early-stage, pilot programs demonstrate potential for fundamentally improving property data reliability.

Augmented Reality for Remote Surveys

AR technology will enable hybrid survey approaches combining physical and virtual inspection:

- Remote guided tours where surveyors direct property occupants through inspection protocols

- Computer vision analysis of photographs and video identifying condition issues

- 3D modeling from smartphone captures creating detailed property representations

- Measurement automation calculating dimensions and areas from visual data

These capabilities will expand the range of properties suitable for desktop valuations while reducing costs and timelines even for complex properties requiring some physical inspection. When working with local surveyors, AR tools will enable more efficient resource allocation.

Integrated ESG Risk Assessment

Environmental, social, and governance factors are becoming central to property valuations:

- Climate resilience scoring incorporating long-term environmental risk projections

- Energy efficiency modeling predicting operating costs and regulatory compliance

- Social impact metrics measuring community benefit and affordable housing contributions

- Governance quality indicators assessing building management effectiveness

For complex properties like high-rises, comprehensive ESG assessment will become standard practice, with data technology enabling systematic analysis that manual processes cannot match.

Conclusion: Implementing Early Property Data Tech for Complex Valuations in Your Lending Operation

The transformation of property valuation through data technology represents one of the most significant operational improvements available to lenders in 2026. Early Property Data Tech for Complex Valuations: Lender Strategies to Avoid 2026 Survey Delays isn't merely about speed—it's about making smarter decisions with better information, allocating expensive survey resources where they create genuine value, and delivering superior borrower experiences through faster, more transparent processes.

The evidence is compelling: 94% accuracy, under 60-second turnaround times, and cost reductions exceeding 95% demonstrate that AI-powered property data technology has moved from experimental to essential.[1][2] For lenders processing applications involving non-standard properties—high-rises, mixed-use developments, historic conversions—the ability to generate comprehensive preliminary valuations instantly transforms workflow efficiency.

Actionable Next Steps

Lenders ready to implement or enhance property data technology should:

-

Audit current processes: Document time, cost, and accuracy metrics for existing valuation workflows to establish baseline performance

-

Evaluate data providers: Request demonstrations from multiple providers, focusing on coverage in your markets, API integration capabilities, and compliance features—resources like comprehensive provider comparisons can inform selection

-

Pilot with complex properties: Test technology specifically on non-standard properties where traditional processes create the greatest delays, measuring time savings and accuracy

-

Develop hybrid protocols: Create clear guidelines for when AI valuations suffice versus when physical building surveys remain necessary

-

Train underwriting teams: Ensure staff understand how to interpret AI-generated valuations, confidence intervals, and risk flags in lending decisions

-

Establish feedback loops: Systematically compare AI predictions to actual survey results, feeding insights back to improve algorithmic performance

-

Monitor competitive position: Track application processing times against market competitors, adjusting strategies to maintain or gain advantage

The lenders who thrive in 2026's competitive mortgage market will be those who effectively combine technological efficiency with human expertise. Property data technology doesn't replace professional surveyors—it amplifies their effectiveness, enabling them to focus on genuinely complex situations requiring expert judgment while automation handles routine analysis.

For properties requiring comprehensive physical inspection, understanding what happens after a property offer is accepted and how to navigate survey results remains crucial. The goal isn't to eliminate surveys but to ensure they occur strategically, with maximum efficiency and effectiveness.

The 40% growth projection for AI adoption in real estate[1] suggests this transformation is accelerating, not slowing. Lenders who delay implementation risk competitive disadvantage as faster, more efficient competitors capture market share. The technology is proven, the economics are compelling, and the operational benefits are substantial. The question isn't whether to adopt Early Property Data Tech for Complex Valuations: Lender Strategies to Avoid 2026 Survey Delays—it's how quickly you can implement it effectively.

References

[1] How Ai Is Transforming Property Valuations In 2026 – https://european.realestate/how-ai-is-transforming-property-valuations-in-2026/

[2] Ai Property Valuation – https://www.growthfactor.ai/resources/blog/ai-property-valuation

[3] Real Estate Data Providers In 2026 How To Evaluate Coverage Refresh And Licensing Fit – https://www.thewarrengroup.com/blog/real-estate-data-providers-in-2026-how-to-evaluate-coverage-refresh-and-licensing-fit/

[4] The Best Real Estate Data Providers 2026 – https://forage.ai/blog/the-best-real-estate-data-providers-2026/