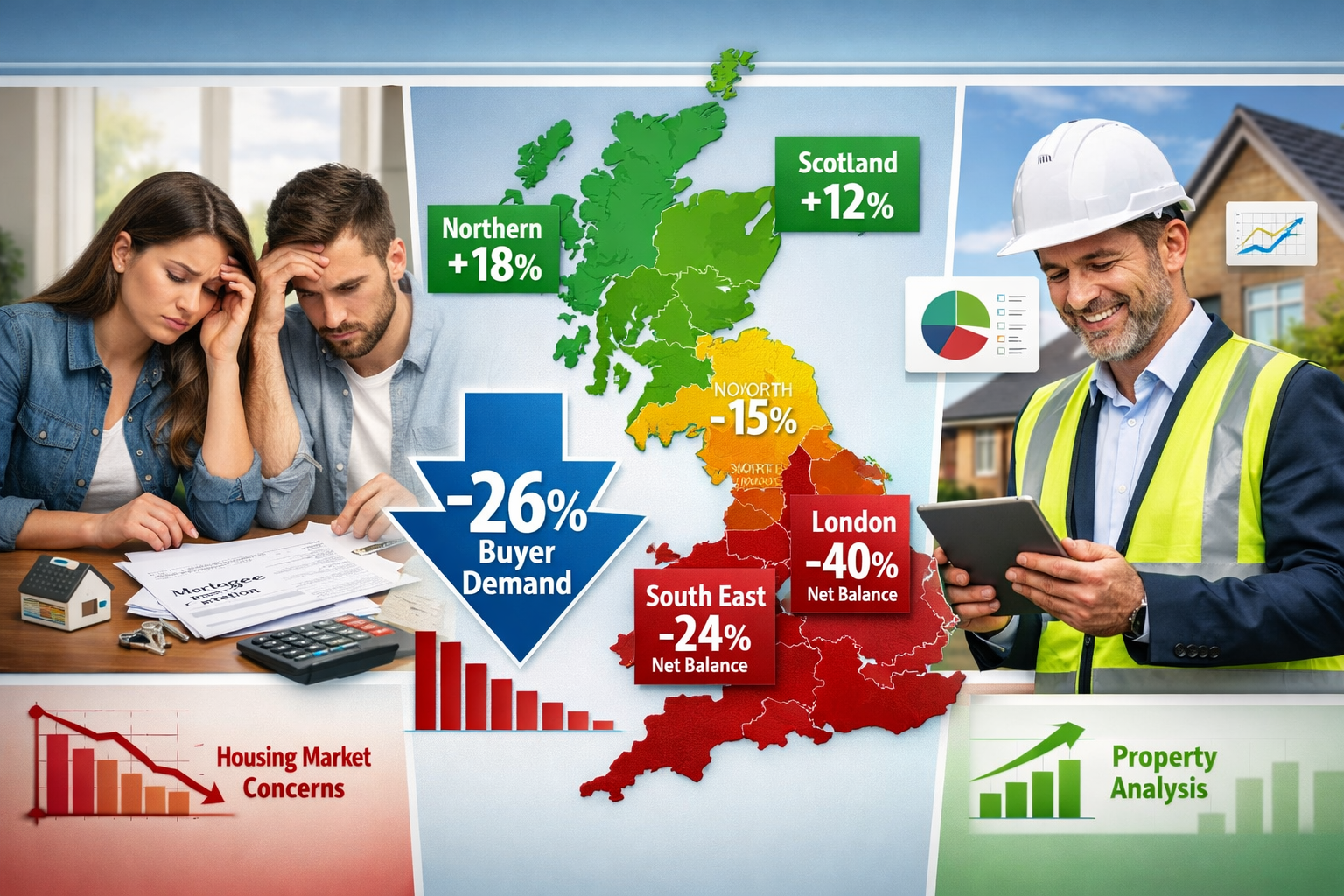

Buyer demand has plummeted to a net balance of -26% in February 2026, marking the sharpest deterioration in market sentiment since the turbulent autumn months of 2023. This dramatic shift, revealed in the latest RICS residential market data, signals a fundamental recalibration in how property professionals must approach surveys, valuations, and client advisory services throughout 2026.

The April 2026 RICS Residential Market Survey: Implications for Building Surveyors and Valuers extends beyond simple market commentary—it represents a critical inflection point demanding strategic adaptation from property professionals. With near-term price expectations collapsing to -18% and London's 12-month outlook crashing from +56% to just +7% in a single month, surveyors and valuers face unprecedented regional divergence and client uncertainty.

This comprehensive analysis examines the survey's key findings and translates surveyor sentiment into actionable intelligence for building survey practices, valuation methodologies, and client communication strategies in this volatile market environment.

Key Takeaways

- Buyer demand weakened dramatically to -26% net balance, requiring surveyors to adjust inspection priorities and valuation assumptions for cautious purchasers

- Regional divergence has intensified sharply, with London (-40%), South East (-24%), and East Anglia (-26%) experiencing severe downward pressure while Northern regions show resilience

- Rental market supply crisis deepens with landlord instructions at -27%, creating urgent demand for specific defect surveys and investment property valuations

- Near-term price expectations deteriorated to -18%, necessitating more conservative valuation approaches and enhanced risk disclosure in survey reports

- 12-month outlook remains cautiously positive at +33%, suggesting surveyors should balance short-term caution with medium-term recovery positioning

Understanding the April 2026 RICS Residential Market Survey: Implications for Building Surveyors and Valuers

Current Market Sentiment and Surveyor Outlook

The February 2026 RICS survey reveals a market gripped by renewed uncertainty. New buyer enquiries fell from -15% to -26% net balance, representing the most significant monthly deterioration in demand since late 2023[1]. This collapse in buyer confidence stems from multiple converging pressures: persistent mortgage rate concerns, geopolitical instability affecting energy prices, and growing affordability constraints particularly in southern England.

For building surveyors and valuers, this sentiment shift carries immediate practical implications. Clients are now approaching property purchases with heightened caution, requesting more detailed defect analysis and conservative valuations to support renegotiation strategies. The survey data indicates that agreed sales remained subdued at -12% net balance, with near-term sales expectations softening to -2%[1].

However, the picture is not uniformly negative. The 12-month sales outlook stands at +17%, suggesting respondents anticipate a gradual recovery as macroeconomic headwinds ease[1]. This temporal divergence—pessimism about the next quarter combined with cautious optimism about the year ahead—creates a complex advisory landscape for property professionals.

Regional Performance Disparities

The most striking feature of the April 2026 survey period is the dramatic regional divergence in market conditions. London experienced a catastrophic sentiment collapse, with 12-month price expectations plummeting from +56% in January to just +7% in February[1]. This 49-percentage-point swing reflects acute affordability pressures in the capital, where average property prices remain severely disconnected from local earnings.

The South East (-24%) and East Anglia (-26%) similarly report strong downward price pressure, creating a distinct "southern weakness" pattern[5]. In contrast, Northern Ireland, Scotland, and the North West continue to demonstrate firmer price trends, benefiting from relatively better affordability ratios and stronger local economic fundamentals.

This geographic split demands that building surveyors and valuers adopt location-specific valuation methodologies. Comparable evidence from six months ago may no longer provide reliable guidance in rapidly shifting markets like London, while northern comparables might show greater stability. Professional valuers must now explicitly acknowledge regional market velocity differences in their reports and adjust confidence intervals accordingly.

Price Trajectory Analysis

National headline house prices remain broadly flat, but this headline figure masks significant underlying volatility[1]. The three-month price outlook deteriorated sharply to -18% from -6%, indicating surveyors expect immediate downward pressure before any recovery materializes[1].

The 12-month price outlook of +33% suggests a more optimistic medium-term view, though this represents a moderation from previous survey periods[1]. This creates what economists term a "J-curve" expectation—short-term decline followed by gradual recovery.

For property valuers, this trajectory pattern necessitates careful consideration of valuation date significance. A valuation conducted today for mortgage purposes carries different risk characteristics than one prepared for investment analysis with a 12-18 month hold period. Professional guidance should explicitly address these temporal dimensions, particularly when advising clients on renegotiation strategies following poor survey results.

Practical Implications for Building Survey Practice

Adapting Survey Scope and Client Communication

The current market environment demands that building surveyors recalibrate their inspection priorities and reporting emphasis. With buyer demand weakening and transaction volumes subdued, clients are increasingly risk-averse and cost-conscious. This creates both challenges and opportunities for survey practices.

Surveyors should anticipate more detailed questioning about defect severity and remediation costs. The survey data showing -26% buyer demand indicates that many clients are on the margin of proceeding with purchases[1]. A building survey that identifies significant defects may be the deciding factor in whether a transaction completes or collapses.

Enhanced pre-survey consultations become critical in this environment. Before conducting inspections, surveyors should discuss with clients:

- Current local market conditions and price trajectory expectations

- The client's negotiating position and purchase timeline flexibility

- Specific concerns about property type, age, or condition

- Budget constraints for potential remedial works

- Whether the client needs valuation guidance alongside the survey

This consultative approach allows surveyors to tailor inspection focus and reporting detail to match client needs in uncertain market conditions. Understanding what to do before an RICS home survey helps clients maximize the value they receive from professional inspection services.

Survey Report Modifications for Market Conditions

Survey reports prepared during periods of market uncertainty should incorporate explicit market context commentary. While building surveyors traditionally focus on physical condition assessment, the current environment justifies brief commentary on how identified defects might affect marketability and price negotiation leverage.

Consider including:

✅ Market context statements: Brief acknowledgment of current local market conditions affecting property values and transaction timelines

✅ Defect severity calibration: Clear categorization of issues as "critical negotiating points" versus "minor maintenance items" given current buyer leverage

✅ Remediation cost ranges: More detailed cost estimates for significant defects, recognizing that clients may use these figures in renegotiation discussions

✅ Timing considerations: Guidance on whether certain repairs should be completed pre-purchase versus post-completion based on current contractor availability and costs

For building surveyor services operating across multiple regions, reports should acknowledge the significant geographic variations revealed in the RICS data. A survey in London requires different market framing than one in Manchester or Edinburgh.

New Build and Development Project Implications

The survey data showing subdued sales activity and weakening buyer demand has particular implications for new build properties. While the RICS survey focuses primarily on existing stock, the market sentiment it reveals directly affects new development viability and completion timelines.

Building surveyors involved in new build inspections should recognize that developers facing slower sales may face pressure to:

- Reduce specification quality to maintain margins

- Accelerate construction timelines to minimize holding costs

- Compromise on snagging resolution to achieve legal completion

These pressures increase the importance of thorough new build surveys, particularly for off-plan purchases where buyers committed during more optimistic market conditions. Surveyors should pay enhanced attention to specification compliance, building regulation adherence, and completion quality standards.

Valuation Practice Adjustments in Response to the April 2026 RICS Residential Market Survey

Comparative Method Challenges

The dramatic monthly shifts in market sentiment revealed by the RICS survey create significant challenges for traditional comparative valuation methods. The fundamental assumption of the comparative approach—that recent comparable transactions reflect current market value—becomes problematic when market conditions shift rapidly.

Valuers must now consider:

1. Comparable Transaction Recency 📊

Transactions from even three months ago may reflect materially different market conditions. The shift from -15% to -26% buyer demand in a single month suggests market velocity has changed substantially[1]. Valuers should weight recent comparables more heavily and potentially disregard older evidence entirely in fast-moving markets like London.

2. Comparable Geographic Relevance

The pronounced regional divergence means that valuers must draw comparables from increasingly narrow geographic areas. Evidence from neighboring boroughs may no longer be relevant if local market conditions differ significantly. RICS property valuations must explicitly acknowledge geographic limitations in comparable evidence.

3. Adjustment Factor Magnitude

Standard adjustment percentages for property characteristics (condition, location, size) may need recalibration during periods of market stress. A property requiring significant remedial work faces greater value impact when buyer demand is weak and financing is constrained.

4. Market Conditions Addendum

Professional valuation reports should include explicit market conditions commentary explaining how current RICS survey data and local market intelligence affect valuation confidence and methodology selection.

Valuation Confidence and Uncertainty Ranges

The April 2026 survey period reveals a market characterized by unusual uncertainty. When surveyor sentiment shifts dramatically month-to-month and regional performance diverges sharply, traditional single-point valuations become less meaningful.

Progressive valuation practices should consider adopting explicit uncertainty ranges in their reports. Rather than stating "Market Value: £650,000," valuers might present:

"Market Value: £650,000

Confidence Range: £630,000 – £670,000

Confidence Level: Moderate (reflecting current market uncertainty)"

This approach provides clients with more realistic expectations about valuation precision during volatile periods. It also offers professional protection for valuers, acknowledging that market conditions may shift between valuation date and transaction completion.

For mortgage lending purposes, where single-point valuations remain standard, valuers should ensure that accompanying commentary clearly explains market conditions and potential value volatility. This is particularly important given the survey's finding that near-term price expectations stand at -18%[1], suggesting values may soften further in coming months.

Investment and Rental Property Valuation

The RICS survey reveals a severe and worsening rental market supply shortage, with landlord instructions at -27% net balance[1]. This persistent shortage, combined with stable tenant demand at +2%, creates a fundamentally different valuation environment for rental properties compared to owner-occupied stock.

Key considerations for investment property valuations:

Rental Growth Assumptions 🏘️

With +20% of survey participants expecting rent rises over the next three months[1], valuers should incorporate robust rental growth assumptions into investment appraisals. However, this must be balanced against potential regulatory changes and landlord taxation that may affect net yields.

Void Period Expectations

The tight rental market suggests shorter void periods and stronger tenant retention. Investment valuations should reflect reduced vacancy risk compared to historical assumptions.

Exit Value Considerations

While rental income streams remain strong, the weak sales market (agreed sales at -12% net balance)[1] suggests that exit liquidity for investment properties may be constrained. This affects discount rates and investment return calculations.

Portfolio Valuations

Landlords holding multiple properties face particular uncertainty given the -27% instruction figure[1]. This suggests many landlords are exiting the market, potentially creating opportunities for remaining investors but also indicating sector headwinds from taxation and regulation.

Strategic Positioning for Surveying and Valuation Businesses

Service Mix Optimization

The market conditions revealed in the April 2026 RICS survey suggest that surveying and valuation businesses should rebalance their service offerings to align with current demand patterns and client needs.

High-demand services in current market:

- Detailed building surveys for risk-averse buyers seeking negotiation leverage

- Investment property valuations for landlords considering portfolio optimization

- Rental property condition assessments for landlords preparing properties for tight rental market

- Pre-purchase defect surveys for buyers concerned about overpaying in weakening market

- Lease extension valuations for property owners seeking to maximize value before potential further market softening

Services facing headwinds:

- High-volume mortgage valuations (due to -12% agreed sales and -26% buyer demand)[1]

- New build snagging (due to slower development completions)

- Auction valuations (due to reduced transaction volumes)

Businesses should consider developing specialized expertise in rental market services, given the persistent supply shortage and strong tenant demand. This might include schedule of condition reports for landlords, tenant-commissioned condition surveys, and rental value assessments.

Geographic Market Selection

The pronounced regional divergence in the RICS survey data suggests that surveying businesses with geographic flexibility should strategically prioritize markets showing resilience over those experiencing severe headwinds.

Markets showing relative strength:

- Northern Ireland (positive price sentiment)

- Scotland (firm price trends)

- North West England (resilient demand)

- Wales (stable conditions)

Markets facing significant challenges:

- London (12-month outlook collapsed to +7%)[1]

- South East (-24% price pressure)[5]

- East Anglia (-26% price pressure)[5]

However, challenging markets also create opportunities. Weak buyer demand in London and the South East means buyers are more likely to commission detailed surveys and valuations to support negotiation. While transaction volumes may be lower, fee potential per instruction may be higher as clients seek comprehensive professional guidance.

Practices operating across multiple regions should ensure their marketing and client communication reflects understanding of local market conditions. Generic national messaging will resonate poorly with clients experiencing very different conditions in London versus Manchester.

Client Advisory and Value-Added Services

In markets characterized by uncertainty and weak transaction volumes, surveying and valuation businesses can differentiate through enhanced advisory services that extend beyond basic inspection and valuation reports.

Consider offering:

Market condition briefings: Regular email updates to past clients explaining current RICS survey findings and implications for their local market

Pre-purchase strategy consultations: Paid advisory sessions helping potential buyers understand current market positioning and negotiation leverage before making offers

Portfolio review services: For landlords and investors, comprehensive reviews of property portfolios considering current market conditions and optimization opportunities

Post-survey negotiation support: Guidance on how to use survey findings effectively in price renegotiations, particularly valuable given current weak buyer demand

Valuation update services: For clients who obtained valuations 3-6 months ago, discounted update valuations reflecting current market conditions

These value-added services build deeper client relationships, create additional revenue streams during periods of lower transaction volumes, and position the business as a trusted advisor rather than a transactional service provider.

Technology and Efficiency Investments

With transaction volumes subdued (agreed sales at -12%)[1] and near-term outlook uncertain, surveying businesses face pressure on revenue and utilization. This environment paradoxically creates an ideal opportunity for technology and process investments that improve efficiency and service quality.

Priority investment areas:

Digital survey tools: Tablet-based inspection software, digital floor plan creation, and photo annotation tools that reduce report preparation time

Automated comparable analysis: Systems that automatically identify and analyze comparable transactions for valuation purposes, particularly valuable given the need for recent, geographically-specific evidence

Client portal systems: Online platforms where clients can track survey progress, access reports, and communicate with surveyors, improving service experience and reducing administrative burden

Marketing automation: Email marketing and CRM systems to maintain contact with past clients and generate repeat business during slow transaction periods

Remote valuation capabilities: Desktop valuation tools and processes for appropriate instruction types, allowing businesses to serve clients efficiently when physical inspections aren't required

The current market slowdown provides time to implement these systems before the anticipated 12-month recovery (+17% sales outlook)[1] materializes. Businesses that emerge from this period with improved efficiency and service delivery will be well-positioned to capture market share during the recovery phase.

Conclusion: Navigating Market Uncertainty with Professional Expertise

The April 2026 RICS Residential Market Survey: Implications for Building Surveyors and Valuers reveals a property market at a critical juncture. Dramatic demand weakness, sharp regional divergence, and pronounced short-term pessimism combined with cautious medium-term optimism create a complex environment demanding strategic adaptation from property professionals.

Building surveyors must recognize that clients now approach property purchases with heightened caution and risk aversion. Survey reports should provide enhanced context, detailed defect analysis, and clear guidance on negotiation implications. The current market rewards surveyors who combine technical excellence with commercial awareness and client-focused communication.

Valuers face particular challenges from rapid market condition changes and regional performance divergence. Traditional comparative methods require careful application, with enhanced attention to comparable recency, geographic relevance, and explicit acknowledgment of valuation uncertainty. The rental market supply crisis creates significant opportunities for investment property valuation specialists.

Actionable Next Steps for Property Professionals 🎯

Immediate actions (next 30 days):

- Review and update standard report templates to incorporate market condition commentary and enhanced defect severity guidance

- Analyze your geographic service area using RICS regional data to understand local market positioning

- Develop client communication materials explaining current market conditions and how your services provide value in uncertain times

- Assess your service mix and consider developing rental market specializations given persistent supply shortage

Medium-term strategic priorities (3-6 months):

- Invest in technology and efficiency improvements to maintain profitability during lower transaction volumes

- Build value-added advisory capabilities that differentiate your business beyond basic survey and valuation services

- Develop regional market expertise and specialized knowledge for markets you serve

- Strengthen client relationships through regular market updates and proactive communication

Long-term positioning (6-12 months):

- Prepare for market recovery anticipated in 12-month outlook (+17% sales expectations)[1]

- Build capacity and systems to scale efficiently when transaction volumes recover

- Establish thought leadership through market commentary and professional insights

- Develop strategic partnerships with estate agents, mortgage brokers, and legal professionals in your target markets

The current market environment challenges property professionals to demonstrate their value through expertise, insight, and client-focused service delivery. Those who successfully navigate this period of uncertainty will emerge stronger and better positioned for the anticipated recovery ahead.

For professional surveying services adapted to current market conditions across London and surrounding areas, explore comprehensive RICS surveys and building survey options designed to provide clients with the detailed analysis and strategic guidance they need in today's challenging property market.

References

[1] Uk Residential Survey February 2026 – https://www.rics.org/news-insights/uk-residential-survey-february-2026

[2] Uk Resi Survey Jan 2026 Report Shows Early Signs Market Recovery Despite Caution – https://www.rics.org/news-insights/uk-resi-survey-jan-2026-report-shows-early-signs-market-recovery-despite-caution

[3] Uk Residential Market Survey February 2026 – https://www.rics.org/content/dam/ricsglobal/documents/market-surveys/uk-residential-market-survey/UK-Residential-Market-Survey_February-2026.pdf

[4] Property Market Turning Corner Rics Survey Suggests – https://todaysconveyancer.co.uk/property-market-turning-corner-rics-survey-suggests/

[5] Latest Rics Survey Reveals Global Headwinds Are Weighing On Housing Market Confidence – https://www.buyassociationgroup.com/en-gb/news/latest-rics-survey-reveals-global-headwinds-are-weighing-on-housing-market-confidence/

[6] Rics House Price Balance – https://tradingeconomics.com/united-kingdom/rics-house-price-balance

[7] Residential Market Shows Signs Of Early Recovery In January 2026 Rics – https://theintermediary.co.uk/2026/02/residential-market-shows-signs-of-early-recovery-in-january-2026-rics/

[8] Uk Residential Market Survey – https://www.rics.org/news-insights/market-surveys/uk-residential-market-survey

[9] housingtoday.co.uk – https://www.housingtoday.co.uk/news/rics-hails-early-signs-of-housing-market-improvement-in-latest-survey/5140683.article