The 2026 Budget has fundamentally altered the landscape for high-value property transactions in the United Kingdom. With new tax measures targeting properties valued at £2 million and above, property owners, investors, and surveyors face unprecedented challenges in accurately assessing market values while accounting for fiscal burdens. Understanding Valuation Techniques for Budget Tax Impacts on High-Value Properties: RICS Adjustments Post-2026 Reforms has become essential for anyone involved in the luxury property market. These reforms demand that chartered surveyors adapt their methodologies to reflect not just market conditions, but also the significant tax implications that now influence buyer behavior and property pricing strategies.

The Royal Institution of Chartered Surveyors (RICS) has responded to these changes by updating its guidance and valuation standards, ensuring professionals can navigate this complex new environment. For high-net-worth individuals purchasing or selling premium properties, the difference between a standard valuation and one that properly accounts for tax impacts can mean hundreds of thousands of pounds in negotiation leverage.

Key Takeaways

- Tax-adjusted valuations are now mandatory for properties exceeding £2 million, requiring surveyors to factor fiscal burdens into market value assessments

- RICS has updated Red Book standards to address post-2026 Budget reforms, providing clear guidance on tax impact adjustments and valuation methodology

- Regional variations significantly affect valuation approaches, with Manchester properties showing 8.2% year-on-year growth while London's prime sector faces different dynamics [2]

- Leasehold reform complications add another layer of complexity, particularly for high-value properties transitioning toward commonhold tenure [3]

- Professional surveyors must balance traditional comparative market analysis with new tax-driven pricing models to deliver accurate, defensible valuations

Understanding the 2026 Budget Tax Reforms Affecting High-Value Properties 💷

The 2026 Budget introduced several targeted measures that directly impact properties valued above £2 million. These changes represent the most significant shift in high-value property taxation in over a decade, creating ripple effects throughout the luxury real estate market.

Key Tax Changes Implemented

The primary reforms include:

- Enhanced Stamp Duty Land Tax (SDLT) surcharges for properties over £2 million

- Annual Tax on Enveloped Dwellings (ATED) rate increases for corporate-owned residential properties

- Capital Gains Tax (CGT) adjustments affecting disposal of high-value investment properties

- Inheritance Tax (IHT) valuation requirements with stricter reporting standards

These measures were designed to generate additional revenue from the luxury property segment while discouraging speculative investment in high-end residential real estate. However, they've created significant challenges for property professionals who must now incorporate these fiscal considerations into their valuation work.

Market Response and Pricing Adjustments

The immediate market response has been notable. Buyers of properties in the £2 million-plus bracket now factor tax burdens into their maximum purchase price calculations, effectively reducing what they're willing to pay for properties that previously commanded premium prices. This phenomenon has forced sellers to adjust expectations and surveyors to develop new methodologies that reflect these market realities.

According to RICS data from January 2026, regional variations have become more pronounced, with some areas experiencing significant value growth while others face pressure [2]. This divergence makes standardized valuation approaches increasingly problematic, requiring surveyors to adopt more nuanced, location-specific techniques.

RICS Red Book Standards: Post-2026 Valuation Methodology Adjustments

The RICS Red Book—formally known as the RICS Valuation – Global Standards—serves as the definitive guide for valuation professionals worldwide. Following the 2026 Budget reforms, RICS has issued updated guidance specifically addressing how surveyors should incorporate tax impacts into their valuations of high-value properties.

Core Principles of Tax-Adjusted Valuations

When conducting RICS property valuations for high-value properties in 2026, surveyors must now consider:

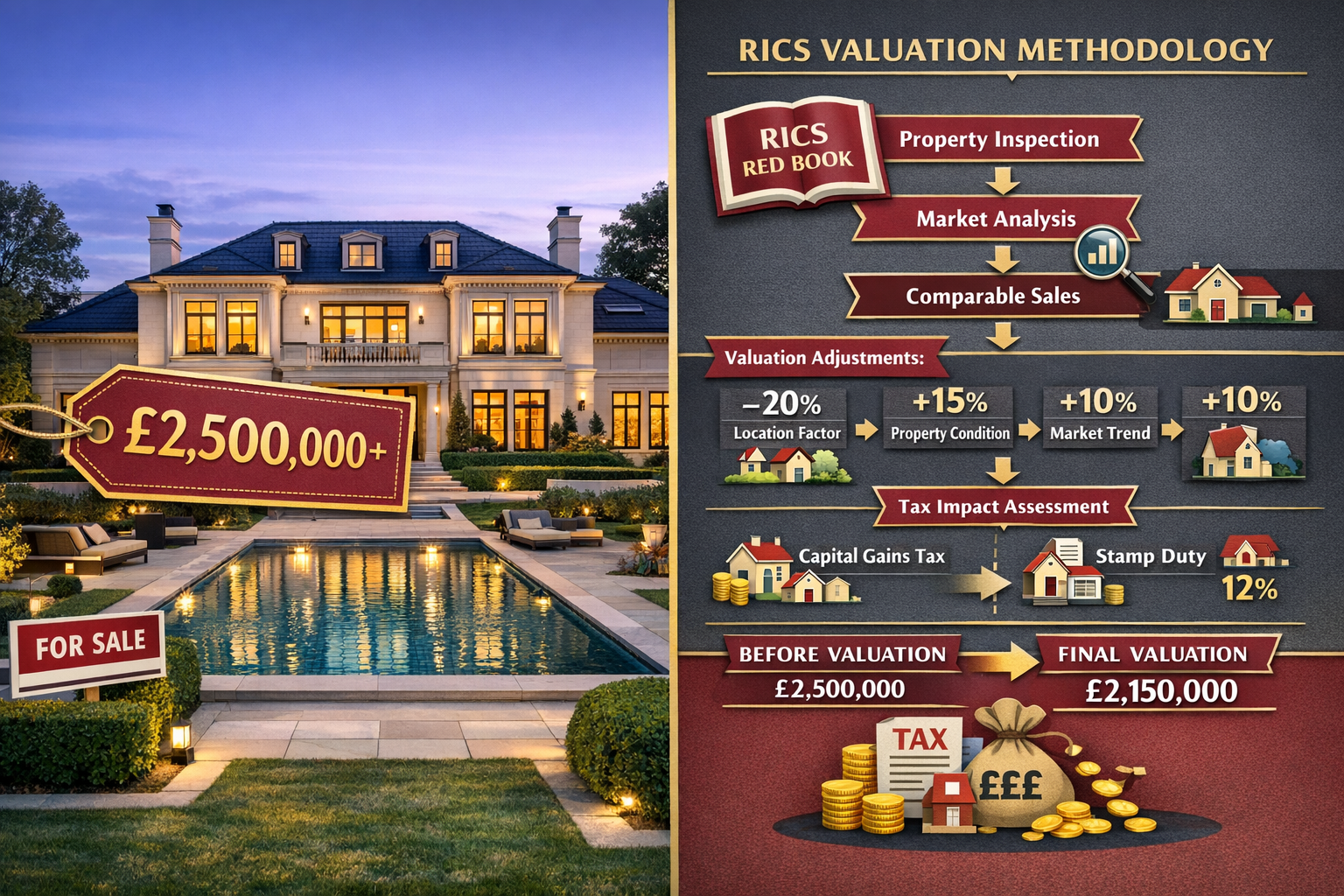

Market Value vs. Tax-Adjusted Value: Traditional market value represents the estimated amount for which a property should exchange between a willing buyer and seller in an arm's-length transaction. Tax-adjusted value incorporates the fiscal burden that buyers will bear, effectively reducing the net value to the purchaser.

Comparable Evidence Adjustments: When selecting comparable properties for analysis, surveyors must ensure they're comparing transactions that occurred under similar tax regimes. Pre-2026 sales data requires adjustment to reflect current fiscal conditions.

Buyer Profile Considerations: Different buyer categories face varying tax exposures. Domestic buyers, overseas investors, corporate entities, and individual purchasers each encounter distinct tax treatments that influence their willingness to pay.

The Red Book Valuation Process for High-Value Properties

A comprehensive Red Book valuation in Wimbledon, London or other premium locations now follows an enhanced framework:

- Initial Property Assessment: Physical inspection and condition analysis

- Market Research: Gathering comparable sales data with tax regime classification

- Tax Impact Calculation: Determining applicable SDLT, ATED, and other fiscal burdens

- Adjustment Application: Modifying comparable values to reflect tax differentials

- Final Value Opinion: Providing both standard market value and tax-adjusted value

- Sensitivity Analysis: Demonstrating how different buyer profiles might value the property

This methodology ensures that clients receive comprehensive information for decision-making, whether they're purchasing, selling, refinancing, or planning estate strategies.

Leasehold Reform Complications

Adding complexity to the valuation landscape, ongoing leasehold reforms have introduced additional uncertainty. RICS submitted evidence to UK Parliament in March 2026 highlighting challenges with valuation methodology during the transition to commonhold tenure, including concerns about lender readiness and professional standards [3]. For high-value leasehold properties, this creates a dual-layer challenge: surveyors must account for both tax reforms and tenure transition uncertainties.

Practical Valuation Techniques for Budget Tax Impacts on High-Value Properties: RICS Adjustments Post-2026 Reforms

Implementing effective Valuation Techniques for Budget Tax Impacts on High-Value Properties: RICS Adjustments Post-2026 Reforms requires a systematic approach that combines traditional surveying expertise with financial analysis capabilities.

Comparative Market Analysis with Tax Normalization

The cornerstone of property valuation remains comparative market analysis (CMA), but the 2026 reforms necessitate a refined approach:

Step 1: Comparable Selection

Identify recent sales of similar properties within the same value bracket (£2M-£3M, £3M-£5M, £5M+) and geographic area. Ensure comparables are recent enough to reflect current tax conditions.

Step 2: Tax Burden Calculation

For each comparable, calculate the total tax burden the buyer faced:

| Property Value | SDLT Standard | SDLT Additional Property | ATED (if applicable) | Total First-Year Tax |

|---|---|---|---|---|

| £2,000,000 | £153,750 | £213,750 | £0 | £153,750-£213,750 |

| £3,000,000 | £263,750 | £363,750 | £0 | £263,750-£363,750 |

| £5,000,000 | £513,750 | £713,750 | £119,550 | £513,750-£833,300 |

Step 3: Value Adjustment

Apply tax normalization adjustments to ensure all comparables reflect equivalent fiscal conditions. This might involve adjusting pre-2026 sales upward to reflect the additional tax burden buyers now face.

Step 4: Location-Specific Factors

Regional market dynamics significantly influence valuation outcomes. As noted in recent RICS survey data, Manchester property values surged 8.2% year-on-year while London's prime sector experienced different trends [2]. Surveyors must understand these regional variations when applying tax adjustments.

Residual Value Method for Development Properties

For high-value properties with development potential, the residual value method requires modification to account for tax impacts at both acquisition and disposal stages:

Gross Development Value (GDV) – Development Costs – Developer's Profit – Tax Burden = Residual Land Value

The tax burden component now includes enhanced SDLT on acquisition, potential ATED during the development period, and CGT implications on disposal—all of which reduce the residual value a developer can justify paying.

Income Capitalization for Investment Properties

High-value investment properties require careful analysis of how tax changes affect net yields:

- Rental Income (gross annual rent)

- Less: Operating Expenses (management, maintenance, insurance)

- Less: Tax Costs (ATED, income tax implications)

- Net Operating Income

- Divided by: Capitalization Rate (adjusted for tax environment)

- Equals: Property Value

The capitalization rate must reflect the increased holding costs associated with post-2026 tax measures, effectively reducing property values relative to pre-reform levels.

Negotiation Leverage Through Tax-Informed Valuations

Understanding tax impacts provides significant negotiation advantages. When buyers can demonstrate through professional valuation that tax burdens justify a lower purchase price, sellers often have limited counterarguments. This is where RICS surveys can help negotiate property prices effectively.

Regional Variations in Valuation Approaches Across the UK 🗺️

The application of Valuation Techniques for Budget Tax Impacts on High-Value Properties: RICS Adjustments Post-2026 Reforms varies considerably across different UK regions, reflecting local market conditions, buyer demographics, and property characteristics.

London and the South East

London's prime property market has historically been dominated by international buyers, many of whom face additional tax surcharges. The combination of existing non-resident taxes and the 2026 reforms has created a compound effect that requires careful analysis.

Key considerations for London valuations:

- International buyer premium: Properties attractive to overseas purchasers may command higher base values but face steeper tax adjustments

- Leasehold prevalence: Many high-value London properties are leasehold, adding reform-related uncertainty [3]

- Micro-market variations: Values in Kensington differ significantly from those in emerging areas

- Corporate ownership patterns: ATED implications are particularly relevant in central London

Surveyors working in areas like Wimbledon, Kensington, and Notting Hill must be particularly attuned to these factors.

Northern Powerhouse Cities

Manchester, Leeds, and other northern cities present a different valuation landscape. With stronger growth trajectories and lower absolute property values, fewer properties exceed the £2 million threshold where the most significant tax impacts apply.

However, the premium segment in these markets requires careful attention:

- Growth momentum: Manchester's 8.2% year-on-year value increase [2] suggests strong underlying demand that may offset tax concerns

- Buyer profile differences: More domestic buyers relative to London, affecting tax exposure patterns

- Development activity: Significant new construction in the luxury segment creates valuation benchmarking challenges

Scotland and Wales

Devolved tax systems in Scotland and Wales create additional complexity. Scotland's Land and Buildings Transaction Tax (LBTT) and Wales's Land Transaction Tax (LTT) have different rate structures than England's SDLT, requiring region-specific valuation adjustments.

Practical Implementation: Case Studies and Examples 📊

To illustrate how Valuation Techniques for Budget Tax Impacts on High-Value Properties: RICS Adjustments Post-2026 Reforms work in practice, consider these scenarios:

Case Study 1: £2.5M Period Property in Richmond

Property: Five-bedroom Victorian house requiring home renovation

Pre-2026 Valuation: £2,500,000

Tax Analysis:

- SDLT (primary residence): £213,750

- SDLT (additional property): £313,750

- Renovation costs: £200,000

- Total buyer outlay: £2,713,750-£2,813,750 (plus renovation)

Post-2026 Adjusted Valuation: £2,350,000-£2,400,000

Rationale: Buyers now factor the £213,750-£313,750 tax burden into their maximum purchase price, effectively reducing what they'll pay for the property itself. The surveyor's tax-adjusted valuation reflects this market reality, providing the seller with realistic pricing expectations.

Case Study 2: £4M Leasehold Apartment in Marylebone

Property: Three-bedroom luxury apartment, 85-year lease

Complications:

- Leasehold reform uncertainty [3]

- Potential lease extension costs

- SDLT implications

- Service charge considerations

Valuation Approach:

The surveyor conducted a comprehensive property valuation that included:

- Freehold equivalent value: £4,200,000

- Leasehold discount (85 years): -£300,000

- Reform uncertainty discount: -£150,000

- Tax-adjusted value: £3,750,000

- Lease extension cost provision: -£200,000

- Final valuation: £3,550,000

This multi-layered analysis provided the buyer with clear justification for a significantly reduced offer, which the seller ultimately accepted after receiving independent verification.

Case Study 3: £6M Portfolio of Investment Properties

Portfolio: Three high-value rental properties held in corporate structure

Tax Considerations:

- ATED annual charges: £358,650 total

- CGT on disposal implications

- Corporate structure maintenance costs

- Rental income tax treatment

Valuation Methodology:

The surveyor used an income capitalization approach with tax-adjusted cap rates:

- Gross annual rental income: £360,000

- Operating expenses: -£72,000

- ATED charges: -£358,650

- Net operating income: -£70,650 (negative)

This analysis revealed that the portfolio's holding costs exceeded its income generation, leading to a recommendation for restructuring or disposal—a conclusion that wouldn't have been apparent without tax-informed valuation techniques.

Technology and Tools Supporting Modern Valuation Practices 💻

The complexity of Valuation Techniques for Budget Tax Impacts on High-Value Properties: RICS Adjustments Post-2026 Reforms has driven adoption of specialized technology:

Valuation Software Enhancements

Leading valuation platforms now include:

- Automated tax calculators that compute SDLT, ATED, and CGT based on property characteristics and buyer profiles

- Comparable database filters that allow tax-regime-specific searches

- Scenario modeling tools that demonstrate value sensitivity to different tax assumptions

- Regional adjustment algorithms that account for location-specific market dynamics

Data Analytics and Market Intelligence

RICS-accredited surveyors increasingly rely on sophisticated data analytics to inform their valuations:

- Transaction databases with detailed tax treatment information

- Predictive modeling for future tax policy scenarios

- Regional performance tracking to identify emerging trends like Manchester's 8.2% growth [2]

- Buyer behavior analysis showing how different demographics respond to tax changes

Quality Assurance and Compliance

Technology also supports compliance with enhanced RICS standards [4]:

- Audit trail documentation ensuring all valuation decisions are defensible

- Peer review systems allowing quality control checks

- Continuing professional development (CPD) tracking to ensure surveyors remain current with evolving standards

Professional Standards and Continuing Education Requirements

The introduction of Valuation Techniques for Budget Tax Impacts on High-Value Properties: RICS Adjustments Post-2026 Reforms has necessitated enhanced professional development for chartered surveyors.

RICS Training and Certification

RICS has introduced specialized training modules covering:

- Tax impact assessment methodologies

- Regional market analysis techniques

- Leasehold reform implications for valuation [3]

- Technology tools for tax-adjusted valuations

- Ethical considerations in tax-informed advice

Surveyors must complete these modules to maintain their accreditation and ensure they're providing clients with current, accurate guidance.

Ethical Considerations

Tax-adjusted valuations raise important ethical questions:

Independence: Surveyors must maintain objectivity even when clients pressure them to produce valuations that support predetermined conclusions about tax impacts.

Transparency: Valuation reports must clearly distinguish between traditional market value and tax-adjusted value, explaining the methodology and assumptions used for each.

Competence: Surveyors should only undertake tax-adjusted valuations if they possess adequate knowledge of current tax law and its implications—referring clients to specialists when necessary.

Collaboration with Tax Advisers

Optimal outcomes often require collaboration between chartered surveyors and tax advisers. While surveyors provide property valuation expertise, tax specialists offer detailed analysis of individual client circumstances, creating comprehensive advice packages that address both valuation and tax planning considerations.

Future Outlook: Anticipated Reforms and Market Evolution 🔮

The valuation landscape continues to evolve, with several developments likely to affect Valuation Techniques for Budget Tax Impacts on High-Value Properties: RICS Adjustments Post-2026 Reforms in coming years.

Potential Policy Adjustments

Government reviews of the 2026 reforms are expected in 2027-2028, potentially leading to:

- Threshold adjustments to account for property price inflation

- Regional variations in tax rates reflecting different market conditions

- Simplified tax structures to reduce compliance burdens

- Enhanced reliefs for certain property types or buyer categories

Surveyors must stay informed about these potential changes and understand how they might affect valuation methodologies.

Market Adaptation

As the market adjusts to the 2026 reforms, several trends are emerging:

- Price compression in the £2M-£2.5M bracket as sellers reduce prices to stay below key thresholds

- Product innovation with developers creating properties specifically designed to minimize tax impacts

- Buyer education improving as purchasers become more sophisticated about tax implications

- Regional rebalancing as some buyers relocate to areas with more favorable tax-to-value ratios

Technology Integration

Continued technological advancement will further transform valuation practices:

- AI-powered valuation models incorporating real-time tax policy changes

- Blockchain-based transaction records providing more transparent comparable data

- Virtual inspection technologies enabling more efficient valuation processes

- Integrated advisory platforms connecting surveyors, tax advisers, and legal professionals

Conclusion: Navigating the New Valuation Landscape

The 2026 Budget reforms have fundamentally transformed how high-value properties must be valued in the United Kingdom. Valuation Techniques for Budget Tax Impacts on High-Value Properties: RICS Adjustments Post-2026 Reforms represent not just technical adjustments to existing methodologies, but a wholesale rethinking of how surveyors approach their work in the premium property segment.

For property owners, investors, and professionals working in the high-value market, several key principles should guide decision-making:

✅ Engage qualified professionals early: Don't wait until you're ready to transact—understand the tax implications and valuation considerations well in advance.

✅ Demand comprehensive analysis: Ensure your surveyor provides both traditional market value and tax-adjusted value opinions, with clear explanations of the methodology and assumptions used.

✅ Consider regional variations: Market conditions vary significantly across the UK, and valuation approaches must reflect these differences [2].

✅ Account for ongoing reforms: Leasehold changes and other policy developments add additional complexity that must be factored into valuations [3].

✅ Use valuations strategically: Tax-informed valuations provide powerful negotiation tools when properly deployed in transaction discussions.

The surveyors who thrive in this new environment will be those who combine traditional valuation expertise with sophisticated understanding of tax policy, regional market dynamics, and emerging technologies. For clients, working with RICS-accredited professionals who have invested in developing these enhanced capabilities is essential for achieving optimal outcomes.

Whether you're purchasing a luxury property in Richmond, selling a high-value asset in Fulham, or managing a portfolio of premium properties across London, understanding and applying current valuation techniques is critical to protecting your financial interests in the post-2026 reform environment.

Next Steps

If you're involved in a high-value property transaction or portfolio management:

- Schedule a consultation with a qualified RICS surveyor who specializes in tax-adjusted valuations

- Request a comprehensive valuation that addresses both market value and tax implications specific to your circumstances

- Review your portfolio strategy to ensure it remains optimal under current tax conditions

- Stay informed about ongoing reforms and their potential impact on your property interests

- Contact professional surveyors to discuss your specific valuation needs

The complexity of modern property valuation in the high-value segment demands expert guidance. By working with professionals who understand Valuation Techniques for Budget Tax Impacts on High-Value Properties: RICS Adjustments Post-2026 Reforms, you'll be well-positioned to make informed decisions that protect and enhance your property investments.

References

[1] Rics Comments On Us Governments Promoting Access To Mortgage Credit Executive Order – https://www.rics.org/news-insights/rics-comments-on-us-governments-promoting-access-to-mortgage-credit-executive-order

[2] Navigating Widening North South Valuation Divides In 2026 Rics Techniques For Accurate Property Appraisals – https://nottinghillsurveyors.com/blog/navigating-widening-north-south-valuation-divides-in-2026-rics-techniques-for-accurate-property-appraisals

[3] Rics Responds To Latest Government Reforms On Leasehold And Commonhold – https://www.rics.org/news-insights/rics-responds-to-latest-government-reforms-on-leasehold-and-commonhold

[4] Update From Justin Young Rics Ceo March 2026 – https://www.rics.org/news-insights/update-from-justin-young-rics-ceo-march-2026

[5] Surveying In 2026 Reform Recovery And Renewed Demand – https://www.lrg.co.uk/news-and-insights/surveying-in-2026-reform-recovery-and-renewed-demand/