Across England and Wales, RICS data from early 2026 shows tenant demand registering positive readings in every region while new landlord instructions have fallen to their lowest level in over a decade. That divergence — rising demand meeting shrinking supply — is not a temporary blip. It is the direct consequence of years of stacking tax reform, and it is reshaping how surveyors, investors, and landlords must approach property valuation today.

Valuation surveys for constrained rental supply: assessing yields amid 2026 landlord tax pressures has become one of the most pressing challenges in the UK property sector. Surveyors are being asked to do more than confirm bricks-and-mortar value. They are now expected to model net yields after tax, flag compliance costs, and help clients decide whether holding, selling, or restructuring a portfolio still makes financial sense.

This article explains how professional valuation surveys must adapt to a market where supply is structurally constrained, tax burdens are rising, and the gap between gross and net yield has never been wider.

Key Takeaways

- RICS data in 2026 shows tenant demand outpacing landlord supply, compressing available stock and distorting traditional yield benchmarks.

- Section 24 mortgage interest restrictions and the April 2026 Making Tax Digital deadline are the two most immediate tax pressures affecting landlord profitability.

- Gross yield figures on a standard valuation report are increasingly misleading; net yield after tax and compliance costs is the only meaningful metric for buy-to-let decisions in 2026.

- A professional RICS survey provides the condition data needed to model realistic maintenance deductions, which directly affect net yield calculations.

- Landlords exiting the market are creating acquisition opportunities, but buyers must commission thorough surveys before relying on distressed-sale pricing.

Why Rental Supply Is Structurally Constrained in 2026

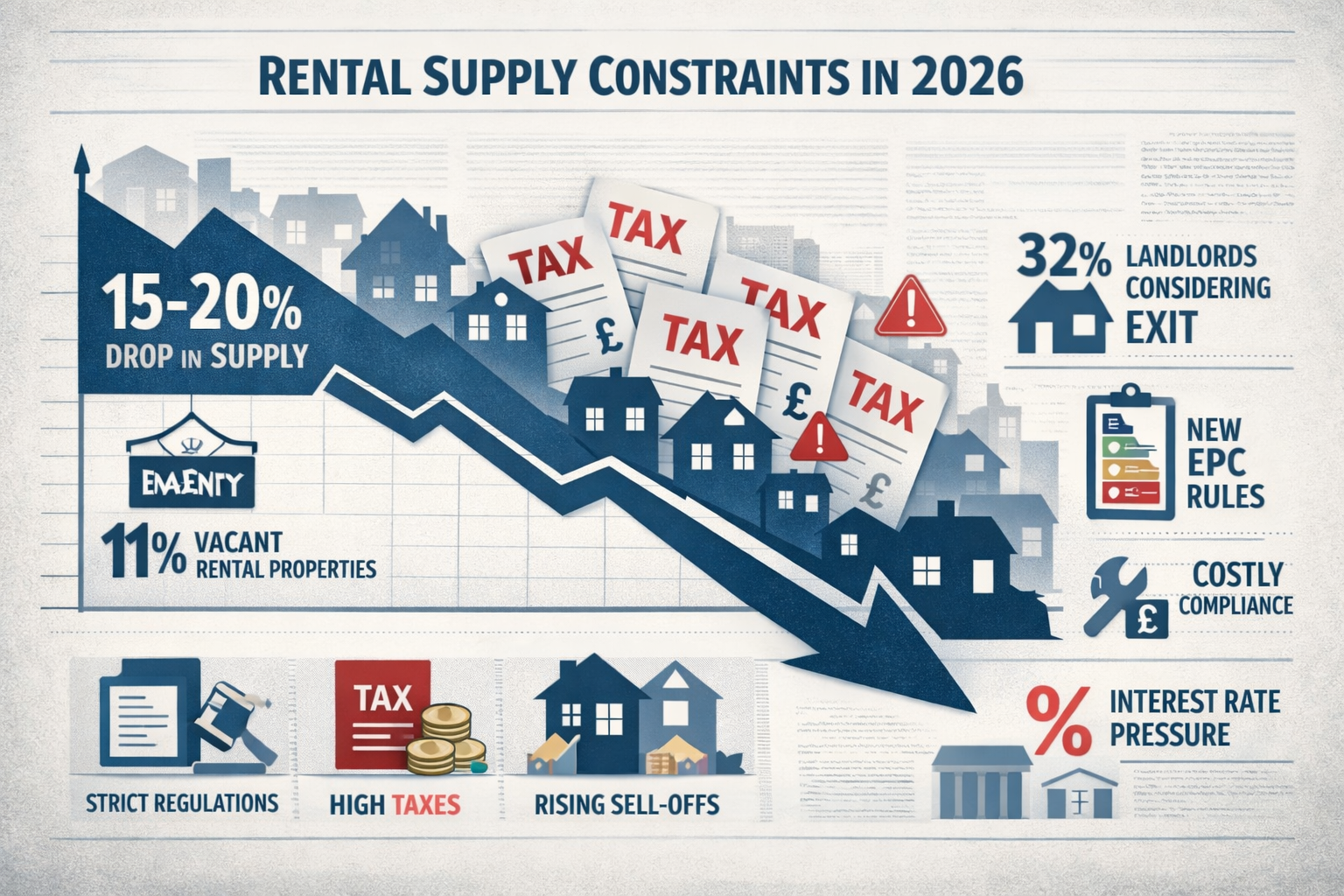

The phrase "landlords are leaving the market" has been repeated so often it risks losing its weight. The numbers behind it, however, are significant. RICS lettings surveys throughout 2025 and into 2026 consistently recorded negative landlord instructions — meaning more landlords are listing properties for sale than are adding new rental stock. At the same time, tenant demand readings remain firmly positive, particularly in London, the South East, and major university cities.

Several forces are driving this contraction simultaneously:

- Section 24 (Finance Act 2015): Mortgage interest can no longer be deducted as a business expense. Instead, landlords receive only a 20% tax credit, meaning higher-rate taxpayers are effectively taxed on turnover rather than profit.

- Stamp Duty Land Tax surcharge: The 3% additional SDLT on second properties (now 5% following the Autumn Budget) has raised the entry cost for new buy-to-let purchases significantly.

- EPC upgrade requirements: Proposed minimum EPC Band C requirements for new tenancies are forcing capital expenditure that many landlords cannot justify against current net yields.

- Making Tax Digital compliance: From April 6, 2026, landlords earning gross property income above £50,000 must file quarterly digital updates under MTD for Income Tax [4]. This administrative burden is accelerating exit decisions among smaller portfolio landlords.

- Income tax rates: UK landlords continue to pay income tax at 20%, 40%, or 45% depending on total income, with the personal allowance tapering above £100,000 [3]. Separate property income tax rates of 22%, 42%, and 47% are scheduled to take effect from April 2027, adding further pressure to forward yield projections [3].

The result is a lettings market where rising rents reflect scarcity rather than underlying property value growth. This creates a specific valuation challenge: headline rental income looks attractive, but the after-tax, after-cost reality for a landlord is often far less so.

How Valuation Surveys Must Adapt to Tax-Squeezed Yields

Standard mortgage valuations were never designed to answer the question "should I keep this property in my portfolio?" They confirm that a lender's security is adequate. For landlords navigating 2026 landlord tax pressures, that is simply not enough information.

Gross yield versus net yield: the critical distinction

Gross yield is calculated as annual rental income divided by property value. A property worth £350,000 generating £18,000 per year in rent shows a gross yield of 5.1%. That figure appears on most basic valuation reports and is widely quoted in the market.

Net yield strips out:

- Mortgage interest costs (no longer fully deductible under Section 24)

- Letting agent fees (typically 10-15% of rental income)

- Insurance, maintenance, and void periods

- Income tax payable on rental profit

- MTD compliance costs from April 2026 onwards

For a higher-rate taxpayer with a mortgage, that 5.1% gross yield can fall to 1.5-2.5% net — or even turn negative in high-value, high-mortgage scenarios.

What a professional RICS survey adds to yield analysis

A RICS survey does not replace a financial model, but it provides the condition data that makes a financial model accurate. Specifically:

- Defect identification: Roofing issues, damp, structural movement, and failing services all carry repair costs that must be deducted from projected income. A condition survey report will flag these before a landlord commits to a purchase or a refinance.

- EPC-linked upgrade costs: Surveyors can assess the likely cost of insulation, heating upgrades, and window replacements needed to achieve Band C, allowing this capital expenditure to be factored into yield projections.

- Dilapidations assessment: For landlords reviewing existing tenancies, a dilapidations survey establishes the condition baseline and potential end-of-tenancy costs.

Choosing the right level of survey matters. For most rental acquisitions, a homebuyers report provides a balanced overview of condition and value. For older properties or those with visible defects, a full Level 3 building survey is the appropriate choice — and understanding which home survey is right for you before instructing a surveyor can save significant time and cost.

| Yield Type | What It Includes | Typical Range (London, 2026) |

|---|---|---|

| Gross Yield | Rent / Property Value | 4.0% – 6.5% |

| Net Yield (pre-tax) | After agent fees, maintenance, voids | 2.8% – 4.5% |

| Net Yield (post-tax, basic rate) | After 20% income tax credit adjustment | 2.2% – 3.8% |

| Net Yield (post-tax, higher rate) | After Section 24 restriction | 0.8% – 2.5% |

"In a tax-constrained market, the gap between what a property appears to yield and what it actually returns after all costs and obligations is wider than at any point in the modern buy-to-let era."

Valuation Surveys for Constrained Rental Supply: Practical Steps for Landlords and Investors

The combination of shrinking supply, rising rents, and increasing tax pressure creates a paradox: the rental market looks profitable on the surface, but the net returns for many individual landlords are deteriorating. Navigating this requires a structured approach to valuation surveys for constrained rental supply: assessing yields amid 2026 landlord tax pressures.

Step 1: Commission a Survey Before Any Buy-to-Let Acquisition

In a constrained market, properties are selling quickly. The temptation to skip or rush a survey is real. Resist it. A survey that identifies £20,000 of required works on a property generating £1,200 per month in rent changes the investment case entirely. Understanding what to do before an RICS home survey — including gathering existing documentation and identifying access requirements — speeds up the process without cutting corners.

If a survey returns significant defects, the valuation implications can be substantial. Knowing how to negotiate the purchase price after a building survey is a practical skill that can recover the cost of the survey many times over.

Step 2: Model Net Yield Using Survey-Informed Cost Data

Once survey findings are available, build a net yield model that includes:

- Gross annual rent (based on current comparable lettings in the area)

- Deduct: Letting agent fees, insurance, service charges, ground rent (if leasehold)

- Deduct: Annualised maintenance reserve (informed by survey condition ratings)

- Deduct: Void period allowance (typically 4-6 weeks per year)

- Apply: Income tax calculation using current 2026/27 rates, accounting for Section 24 restriction [3]

- Deduct: MTD compliance costs if gross income exceeds £50,000 [4]

The result is a realistic net yield figure that can be compared against alternative investments and used to justify (or challenge) the asking price.

Step 3: Assess Damp and Structural Issues as Priority Cost Items

Damp is consistently one of the most common and most underestimated defects in rental properties. It affects tenant health, triggers legal obligations under the Homes (Fitness for Human Habitation) Act 2018, and can escalate rapidly if untreated. A damp survey in London provides a detailed assessment of moisture sources, penetration routes, and remediation costs — all of which feed directly into a net yield model.

Similarly, subsidence and structural movement are issues that can make a property unmortgageable or uninsurable if not addressed. Any sign of cracking, settlement, or movement identified during a survey warrants specialist investigation before purchase.

Step 4: Factor in the Regulatory Compliance Pipeline

Beyond tax, landlords in 2026 face a regulatory compliance pipeline that adds to holding costs:

- Renters' Rights Act: Abolition of Section 21 no-fault evictions changes the risk profile of tenancies and may extend void periods during possession proceedings.

- EPC Band C requirements: Capital expenditure for energy efficiency upgrades must be modelled as a near-term cost, not deferred indefinitely.

- Selective and additional licensing schemes: Many London boroughs and other councils operate licensing schemes that carry annual fees and inspection requirements.

Each of these costs reduces net yield and must be reflected in any serious valuation exercise.

Step 5: Review Portfolio Properties with a Schedule of Condition

For landlords who already own rental properties and are deciding whether to hold or sell, a schedule of condition provides a documented baseline of property state. This is particularly valuable when:

- Reviewing a tenancy ahead of renewal

- Assessing whether to invest in upgrades or sell

- Preparing for end-of-tenancy dilapidations claims

A professional schedule of condition, produced by a chartered surveyor, carries weight in any subsequent dispute and provides the data needed to make informed hold/sell decisions.

The Global Context: Tax Pressure on Landlords Is Not Uniquely British

While the focus here is on UK landlords, it is worth noting that tax pressure on property investors is a global trend in 2026. New York introduced an annual surcharge on secondary residences valued over $5 million in 2026, targeting properties that sit empty while the city faces a housing shortage. The measure is projected to generate approximately $500 million annually through 2031 [1]. Critics argue it risks depressing the high-end real estate market and reducing associated employment, but the political direction is clear: governments are using tax policy to address housing supply constraints.

In the US more broadly, the IRS has confirmed 2026 tax inflation adjustments including a top marginal rate of 37% for incomes over $640,600 (single filers) [2]. For non-resident landlords with US rental income, the tax treatment of rental profits adds another layer of complexity to yield calculations [6].

The pattern is consistent across jurisdictions: tax authorities are targeting property income more aggressively, and the gap between gross and net yield is widening in every major market.

Working With Surveyors in a Tight Lettings Market

The contraction of rental supply has an indirect effect on surveying demand. As landlords exit, properties are being listed for sale — often in condition that reflects years of deferred maintenance under cost-squeezed ownership. This creates a wave of properties entering the sales market that require thorough survey assessment before purchase.

For buyers considering these properties as buy-to-let investments, the survey is not a formality. It is the foundation of the entire investment case. A property sold by an exiting landlord may carry:

- Accumulated maintenance arrears (heating systems, roofing, windows)

- Damp or mould issues that were managed rather than resolved

- Outdated electrical installations that require upgrading to meet current standards

- EPC ratings below Band D that require significant capital expenditure to improve

Understanding what to do after a bad building survey report is essential for buyers who receive a survey with significant findings. In many cases, the right response is not to walk away but to renegotiate — and understanding whether you can renegotiate after a poor building survey result gives buyers the confidence to use survey findings as a legitimate negotiating tool.

Key questions to ask a surveyor when assessing a buy-to-let acquisition:

- What is the estimated cost of all Category 2 and Category 3 defects identified?

- Are there any issues that would affect mortgage valuation or insurability?

- What is the likely EPC rating, and what works would be needed to reach Band C?

- Are there any signs of damp, timber decay, or structural movement that require specialist investigation?

- What is the estimated annual maintenance reserve appropriate for this property type and age?

The answers to these questions, combined with a tax-adjusted yield model, provide the information needed to make a sound investment decision in the current market.

Conclusion

The rental market in 2026 presents a genuine paradox. Supply is contracting, rents are rising, and on the surface the sector looks attractive. But for individual landlords and investors, the after-tax, after-cost reality is far more challenging. Section 24, Making Tax Digital, rising SDLT, and the incoming regulatory compliance pipeline have collectively eroded net yields to levels that no longer justify the risk for many participants.

Valuation surveys for constrained rental supply: assessing yields amid 2026 landlord tax pressures is not simply a technical exercise. It is a strategic discipline that separates informed investors from those relying on headline numbers that no longer reflect reality.

Actionable next steps for landlords and investors in 2026:

- Commission a RICS Level 2 or Level 3 survey on any property under consideration for buy-to-let acquisition — do not rely on a basic mortgage valuation.

- Build a net yield model that incorporates survey-identified maintenance costs, current tax rates under Section 24, and MTD compliance costs where applicable.

- Use survey findings as a negotiating tool — defects identified in a professional report are a legitimate basis for price reduction.

- Review existing portfolio properties with a schedule of condition to inform hold/sell decisions before the April 2027 property income tax rate changes take effect.

- Engage a chartered surveyor with experience in the local lettings market, who can provide comparable rental evidence alongside condition assessment.

The properties that generate sustainable returns in this environment will be those where the investor understood the full cost picture before committing — and a professional valuation survey is the most reliable way to build that picture.

References

[1] New York Power Utility Rebates – https://www.kiplinger.com/taxes/new-york-power-utility-rebates?utm_source=openai

[2] Irs Releases Tax Inflation Adjustments For Tax Year 2026 Including Amendments From The One Big Beautiful Bill – https://www.irs.gov/newsroom/irs-releases-tax-inflation-adjustments-for-tax-year-2026-including-amendments-from-the-one-big-beautiful-bill?utm_source=openai

[3] Income Tax Rates Landlords 2026 27 Complete Guide – https://www.propertytaxpartners.co.uk/blog/landlord-tax-essentials/income-tax-rates-landlords-2026-27-complete-guide?utm_source=openai

[4] Making Tax Digital Landlords April 2026 Deadline – https://www.propertytaxpartners.co.uk/blog/making-tax-digital-mtd/making-tax-digital-landlords-april-2026-deadline?utm_source=openai

[6] Non Resident Landlord Tax Rates On Us Rental Income – https://legalclarity.org/non-resident-landlord-tax-rates-on-us-rental-income/?utm_source=openai