{"cover":"Professional landscape format (1536x1024) hero image featuring bold text overlay 'Valuation Impacts of 2026 Budget's £2 Million+ Property Taxes' in extra large 72pt white sans-serif font with dark shadow and semi-transparent navy overlay box, positioned in upper third. Background shows stunning aerial view of luxury London properties including Georgian townhouses and modern penthouses in Kensington and Knightsbridge, golden hour lighting. Foreground includes subtle overlay of property valuation documents and RICS surveyor's measuring tools. Color palette: deep navy, gold accents, white text. High contrast, editorial magazine cover quality, professional real estate aesthetic with architectural detail visible.","content":["Detailed landscape format (1536x1024) image showing split-screen comparison: left side displays elegant Georgian mansion valued above £2 million with 'Before Tax Changes' label, right side shows same property with red downward arrow overlay and '50% Relief Cap' annotation. Center features professional RICS surveyor in business attire holding tablet displaying valuation software with percentage calculations. Background includes subtle tax document overlays and inheritance tax forms. Color scheme: burgundy, cream, professional blue. Infographic style with clear labels, percentage figures, and visual hierarchy showing tax threshold impacts.","Detailed landscape format (1536x1024) image depicting professional surveyor's desk workspace from overhead angle, featuring large architectural blueprints of luxury property, RICS valuation methodology checklist with checkmarks, calculator displaying figures above £2.5 million, property comparable sales data spreadsheets, and tablet showing digital valuation software interface. Scattered elements include professional measuring tools, property photographs of high-end London homes, and tax adjustment calculation worksheets. Warm natural lighting from window, organized professional aesthetic, rich wood desk surface, burgundy leather desk accessories visible.","Detailed landscape format (1536x1024) image showing interactive map of South England and Greater London with color-coded zones indicating property market stagnation levels: deep red for severely affected areas (Westminster, Kensington, Camden), amber for moderately affected zones, green for stable markets. Overlay includes property value trend graphs with downward trajectories, percentage markers showing valuation adjustments (-8%, -12%, -15%), and location pins marking luxury property hotspots. Professional cartographic style with clean legends, data visualization elements, and modern geographic information system aesthetic. Background features subtle property silhouettes and RICS surveyor certification badge."]}

The luxury property market faces unprecedented challenges in 2026. New council tax surcharges and inheritance tax reforms are reshaping how high-value properties are valued, marketed, and sold across southern England. For property owners, investors, and surveyors working with estates exceeding £2 million, understanding the Valuation Impacts of 2026 Budget's £2 Million+ Property Taxes: Surveyor Strategies for High-End Market Adjustments has become essential for accurate property assessments and successful transactions.

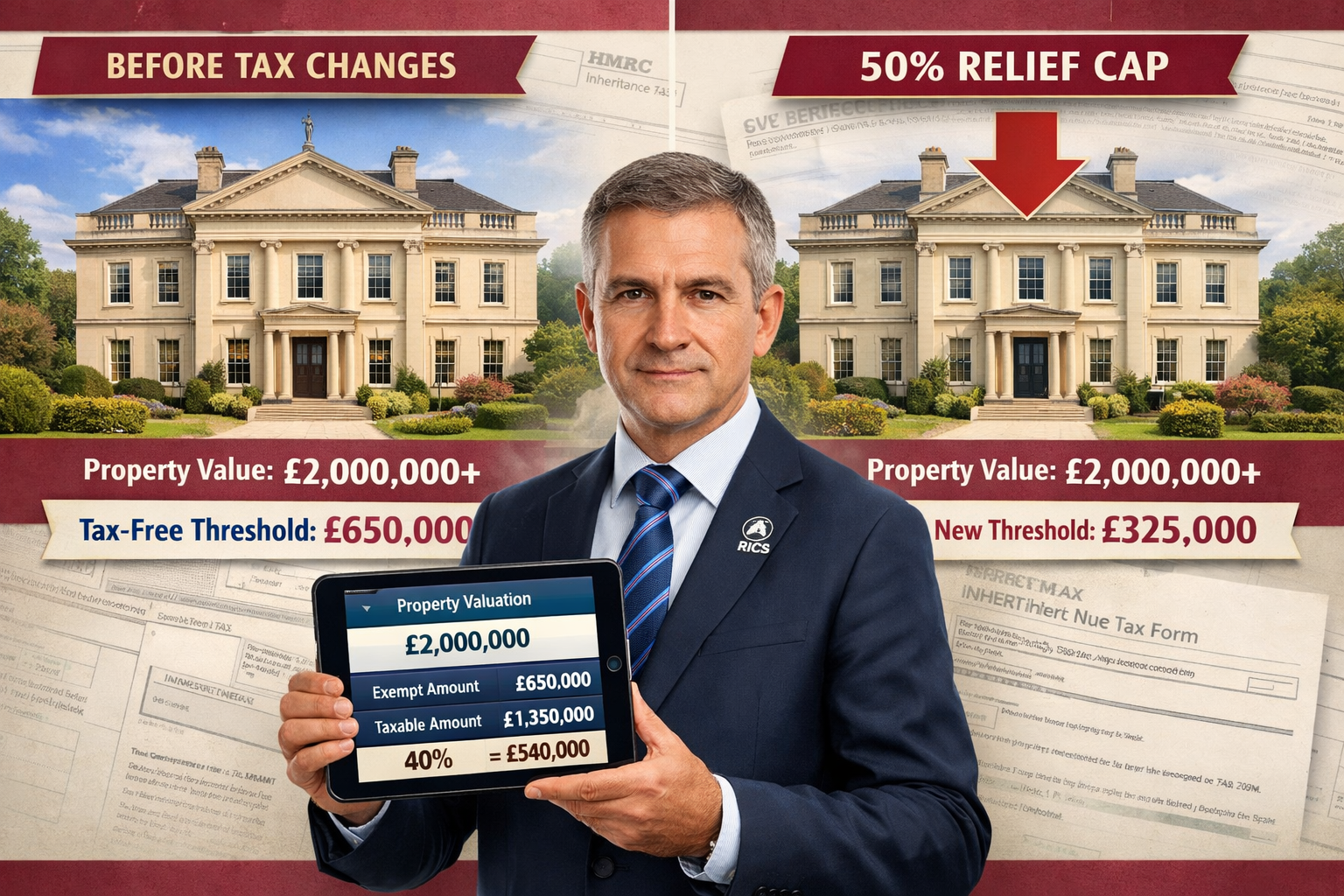

The 2026 Budget introduced sweeping changes that directly affect properties valued above £2 million. Agricultural Property Relief (APR) and Business Property Relief (BPR) now face a combined £2.5 million cap for 100% relief, with assets exceeding this threshold receiving only 50% relief[1][2]. These changes, effective from 6 April 2026, create significant valuation challenges for surveyors assessing high-end residential properties, particularly in areas like Westminster, Kensington, and Knightsbridge.

Key Takeaways

- £2.5 million relief cap now limits 100% inheritance tax relief, with only 50% relief available for assets exceeding this threshold from April 2026[1][2]

- Transferable allowances between spouses enable up to £5 million combined relief, creating strategic planning opportunities for married couples[1]

- New rateable values taking effect 1 April 2026 will substantially change business rates bills for non-domestic properties[1][2]

- Southern market stagnation requires surveyors to adopt specialized valuation methodologies that account for tax-driven price adjustments

- RICS-compliant strategies must now incorporate inheritance tax exposure calculations into standard valuation reports for properties above £2 million

Understanding the 2026 Tax Changes Affecting High-Value Properties

The 2026 Budget represents a fundamental shift in how luxury properties are taxed and valued. These changes extend beyond simple tax rate adjustments—they alter the underlying economics of property ownership for high-net-worth individuals.

The £2.5 Million Relief Cap Explained

From 6 April 2026, the combined Agricultural Property Relief and Business Property Relief face a £2.5 million allowance per individual for 100% relief[1]. Any assets exceeding this threshold receive only 50% relief from inheritance tax. This creates a clear valuation threshold that surveyors must consider when assessing properties.

For married couples, the £2.5 million allowance is transferable between spouses, effectively allowing 100% relief up to £5 million combined[1]. This transferability creates strategic opportunities but also complicates valuation scenarios where ownership structures matter significantly.

Business Rates Revaluation Impact

New rateable values for non-domestic properties in England and Wales take effect from 1 April 2026, which could substantially change rates bills[1][2]. The government has introduced tiered multipliers:

| Property Rateable Value | Multiplier Rate | Property Type |

|---|---|---|

| Below £51,000 | 38.2p | Retail, hospitality, leisure |

| £51,000 – £499,999 | 43p | Retail, hospitality, leisure |

| Over £500,000 | Increased rates | All property types |

These increased multipliers for properties with rateable values over £500,000 directly affect high-end commercial properties and mixed-use developments[1][2]. Surveyors must now factor these ongoing cost increases into their valuation calculations.

AIM Shares and Non-UK Entity Changes

Shares listed on the Alternative Investment Market (AIM) are now restricted to 50% relief under the new rules[2]. Additionally, interests in non-UK entities that own UK agricultural property are brought within the scope of inheritance tax[2]. These changes affect property portfolios held through corporate structures, requiring surveyors to understand ownership arrangements when conducting valuations.

Valuation Impacts of 2026 Budget's £2 Million+ Property Taxes on Market Dynamics

The tax changes create ripple effects throughout the luxury property market, particularly in southern England where property values already face stagnation pressures. Understanding these impacts is crucial for accurate property valuations.

Price Adjustment Mechanisms in the High-End Market

Properties valued above £2 million now carry an implicit tax liability that buyers factor into their purchase decisions. When a property exceeds the relief threshold, potential buyers must consider:

- Inheritance tax exposure of 20% (50% relief on 40% standard rate) on values exceeding £2.5 million

- Holding costs associated with increased business rates for commercial elements

- Liquidity constraints as fewer buyers can absorb the combined purchase price and future tax liability

Surveyors working in areas like Camden and Richmond report that buyers are increasingly requesting detailed tax impact analyses as part of standard valuation reports.

Southern England Market Stagnation Zones

The luxury property market in southern England faces unique pressures. Several factors combine to create "stagnation zones" where property values struggle to appreciate:

📊 Key stagnation factors:

- High existing property values pushing more estates over relief thresholds

- Limited buyer pool willing to absorb increased tax exposure

- Competition from international markets with more favorable tax regimes

- Economic uncertainty affecting high-net-worth purchasing decisions

These stagnation zones require surveyors to adjust their comparable sales analyses. Properties sold before April 2026 may not provide accurate comparables for post-tax-change valuations, particularly for estates valued between £2 million and £5 million where the relief cap has maximum impact.

The Discount Factor for Tax Exposure

Professional valuers now apply a tax exposure discount when assessing properties above the relief threshold. This discount reflects the present value of future inheritance tax liabilities that buyers must consider.

The discount calculation typically involves:

- Determining excess value above the £2.5 million (or £5 million for couples) threshold

- Calculating 20% tax liability on the excess (50% relief on 40% rate)

- Applying time-value adjustments based on expected holding period

- Factoring market liquidity constraints for high-value properties

For a property valued at £3.5 million owned by an individual, the excess £1 million faces a potential £200,000 inheritance tax liability. Buyers typically demand a 3-8% purchase price discount to compensate for this future tax exposure, depending on market conditions and property characteristics.

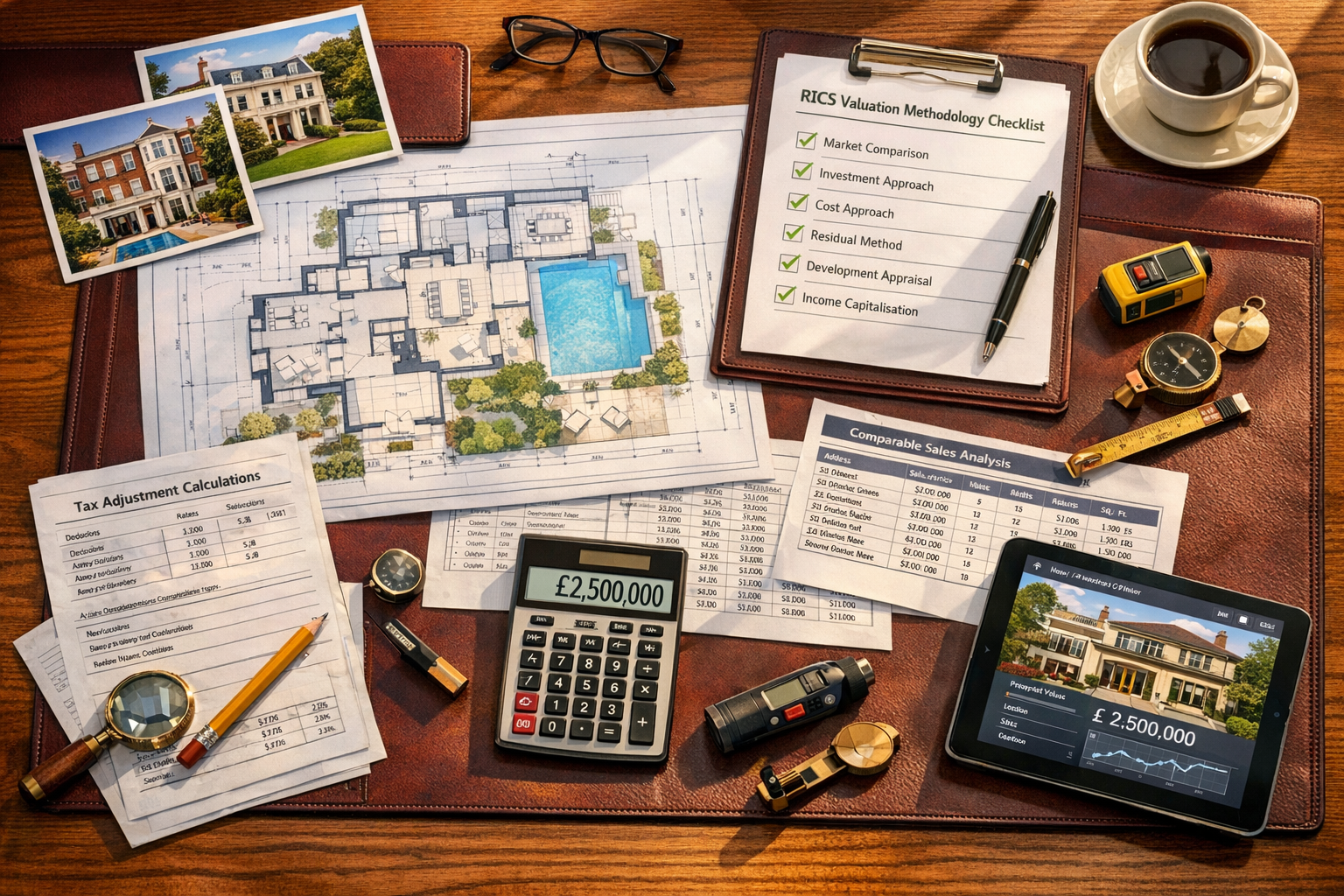

Surveyor Strategies for High-End Market Adjustments

Professional surveyors must adapt their methodologies to accurately reflect the Valuation Impacts of 2026 Budget's £2 Million+ Property Taxes: Surveyor Strategies for High-End Market Adjustments. RICS-compliant approaches now incorporate tax considerations into standard valuation frameworks.

RICS Red Book Compliance in the New Tax Environment

The RICS Valuation – Global Standards (Red Book) provides the framework for professional valuations. In 2026, surveyors must ensure their reports address tax implications while maintaining compliance with established standards.

Essential reporting elements include:

✅ Clear identification of the valuation basis (Market Value, Investment Value, etc.)

✅ Explicit statement of tax assumptions and their impact on valuation

✅ Separate disclosure of pre-tax and post-tax-adjustment values where relevant

✅ Detailed explanation of comparables selection in the post-April 2026 market

✅ Risk factors associated with future tax policy changes

Surveyors providing services in Fulham and Paddington increasingly include dedicated tax impact sections in their reports, helping clients understand the full financial picture.

Comparative Method Adjustments

The comparative method—traditionally the primary approach for residential valuations—requires significant adjustments in 2026. Surveyors must now:

Segregate comparables by transaction date:

- Pre-April 2026 sales require upward or downward adjustment for tax regime differences

- Post-April 2026 sales reflect the new tax environment but may show market volatility

- Cross-regime comparisons need explicit adjustment factors (typically 3-8% for properties £2-4 million)

Analyze ownership structure impacts:

- Properties sold to married couples may command premium prices (£5 million combined relief)

- Single-owner purchases may reflect steeper discounts (£2.5 million individual relief)

- Corporate purchases through non-UK entities now face different tax treatment[2]

Account for regional variation:

- Southern stagnation zones show different price adjustments than northern markets

- Prime central London locations maintain different dynamics than suburban areas

- Areas with high concentrations of properties above £2 million face greater market pressure

Investment Method for Mixed-Use Properties

For mixed-use and commercial properties, the investment method requires recalibration to reflect increased business rates. Properties with rateable values over £500,000 face increased multipliers[1][2], directly affecting net operating income calculations.

Adjusted investment method approach:

- Calculate gross rental income using current market rents

- Deduct increased business rates based on new multipliers (effective 1 April 2026)

- Apply management and maintenance costs including any tax-related administrative burdens

- Determine net operating income reflecting the new cost structure

- Apply appropriate yield adjusted for increased holding costs and market conditions

This methodology ensures valuations reflect the true income-generating potential under the 2026 tax regime.

Residual Method for Development Properties

Development sites and properties with significant renovation potential require careful analysis of the tax implications on development viability. The residual method must now incorporate:

- Exit value adjustments for completed properties above £2 million

- Holding period tax costs during development

- Developer profit margins adjusted for increased market risk

- Purchaser pool limitations due to tax exposure concerns

Surveyors conducting building surveys for development properties must clearly communicate how tax changes affect development feasibility and ultimate property values.

Regional Considerations: Southern England Focus

The Valuation Impacts of 2026 Budget's £2 Million+ Property Taxes: Surveyor Strategies for High-End Market Adjustments vary significantly across regions. Southern England presents unique challenges due to high property concentrations above the relief thresholds.

Prime Central London Dynamics

Prime central London boroughs—Westminster, Kensington and Chelsea, Camden—contain the highest concentration of properties affected by the £2.5 million relief cap. Surveyors working in these areas report:

Market characteristics:

- 60-70% of transactions involve properties exceeding the relief threshold

- International buyers increasingly compare UK tax treatment with alternative jurisdictions

- Downsizing trends as owners seek to reduce inheritance tax exposure

- Structural changes in ownership patterns favoring married couples and trusts

Professional surveyors in Knightsbridge and Westminster must maintain detailed databases of post-April 2026 transactions to ensure accurate comparable analysis.

Suburban Luxury Markets

Suburban areas with significant luxury property stock—Richmond, parts of Camden, select areas of Fulham—face different dynamics:

- Mixed market composition with properties both above and below thresholds

- Greater price sensitivity as buyers have more alternative locations

- Commuter considerations affecting value propositions

- School catchment premiums interacting with tax considerations

Surveyors must carefully analyze which factors drive value in these mixed markets, as tax impacts may be overshadowed by other location-specific considerations.

Agricultural and Estate Properties

Large agricultural estates and country properties face particularly complex valuation challenges. The changes to Agricultural Property Relief and the inclusion of non-UK entity interests[2] create multiple layers of tax exposure.

Valuation considerations for estates:

🏛️ Historic properties with heritage value may qualify for alternative reliefs

🌾 Working agricultural land requires separate analysis under APR rules

🏡 Residential elements must be valued considering the £2.5 million cap

🏢 Commercial elements face business rates revaluation impacts

Surveyors must work closely with tax advisors to ensure comprehensive valuation reports that address all applicable relief mechanisms and tax exposures.

Scottish Market Differences

Scotland operates under different business rates rules, with poundage reductions of 1.7p, 1.9p, and 2p applying to basic, intermediate, and higher property rates respectively[1]. The capped support of £110,000 per business for retail, hospitality, and leisure creates different economic dynamics than in England.

Surveyors working across the England-Scotland border must clearly distinguish which tax regime applies and adjust their methodologies accordingly.

Practical Implementation: Case Studies and Examples

Understanding theoretical frameworks is essential, but practical application demonstrates how surveyors navigate the Valuation Impacts of 2026 Budget's £2 Million+ Property Taxes: Surveyor Strategies for High-End Market Adjustments in real transactions.

Case Study 1: Georgian Townhouse in Camden

Property details:

- 5-bedroom Georgian townhouse in prime Camden location

- Pre-April 2026 valuation: £3.2 million

- Single owner, age 68

- Excellent condition following recent renovation

Valuation approach:

The surveyor identified three comparable sales: one from March 2026 (£3.15 million), and two from May 2026 (£2.95 million and £2.98 million). The post-April sales showed clear price adjustments reflecting tax considerations.

Tax impact calculation:

- Excess over relief threshold: £3.2m – £2.5m = £700,000

- Potential inheritance tax liability: £700,000 × 20% = £140,000

- Market discount factor: 5% (£160,000)

Final valuation: £3.04 million (reflecting market-adjusted value post-tax changes)

The surveyor's report clearly explained that the £160,000 discount exceeded the actual tax liability due to market psychology and liquidity concerns affecting properties in this value range.

Case Study 2: Mixed-Use Property in Fulham

Property details:

- Ground floor commercial (restaurant)

- Three residential flats above

- Rateable value: £580,000

- Pre-April 2026 investment value: £4.1 million

Valuation approach:

The surveyor applied the investment method, carefully calculating the impact of increased business rates multipliers on the commercial unit. The residential elements were valued separately using the comparative method.

Business rates impact:

- Previous annual rates: £245,000

- New rates (increased multiplier): £267,000

- Annual cost increase: £22,000

- Capitalized impact (8% yield): £275,000

Residential tax considerations:

- Combined residential value: £2.8 million

- Within relief threshold for married couple purchasers

- Premium positioning for this buyer type

Final valuation: £3.78 million (reflecting increased holding costs and targeted marketing to couples)

Surveyors providing professional surveyor services must demonstrate this level of detailed analysis in their reports to meet client expectations in 2026.

Case Study 3: Development Site in Richmond

Property details:

- Former commercial building with planning permission for conversion

- Approved scheme: 8 luxury apartments

- Site acquisition price (pre-development): £2.4 million

- Estimated gross development value: £12 million

Valuation approach:

The surveyor used the residual method but adjusted the gross development value to reflect tax impacts on individual unit sales. With units priced £1.3-1.8 million each, most fell below the relief threshold, but the development timeline and market conditions required careful analysis.

Key adjustments:

- GDV reduction: 3% across portfolio (£360,000) due to market uncertainty

- Extended sales period: 18 months vs. 12 months (increased holding costs)

- Developer profit margin: increased from 18% to 20% (risk premium)

Final site valuation: £2.15 million (reflecting reduced development viability)

This case demonstrates how tax changes affect not just end values but entire development economics, requiring surveyors to understand the full property lifecycle.

Future-Proofing Valuation Strategies

The 2026 tax changes represent a significant shift, but surveyors must also anticipate future developments. Property income tax rates will rise by 2% from April 2027 (not 2026), to 22%, 42%, and 47% across basic, higher, and additional rates[2][3]. This creates additional planning considerations for investment properties.

Building Flexible Valuation Models

Professional surveyors should develop valuation models that can accommodate:

Variable tax scenarios:

- Sensitivity analysis showing value ranges under different tax assumptions

- Scenario planning for potential further policy changes

- Stress testing for market condition variations

Ownership structure optimization:

- Comparative analysis of single vs. joint ownership impacts

- Trust structure considerations (requiring specialist tax advice)

- Corporate ownership implications following non-UK entity changes[2]

Market cycle positioning:

- Recognition of current position in property cycle

- Adjustment factors for market recovery or further stagnation

- Long-term value projections incorporating tax trajectory

Technology Integration

Modern surveying practices increasingly rely on technology to manage complex tax-adjusted valuations:

💻 Automated valuation models (AVMs) incorporating tax adjustment algorithms

📊 Comparable sales databases with tax regime filtering capabilities

📱 Client reporting platforms providing interactive tax scenario modeling

🔐 Secure data management for sensitive ownership and tax information

Surveyors who invest in these technologies can provide more sophisticated analysis and better serve clients navigating the complex 2026 tax environment.

Continuing Professional Development

The rapidly evolving tax landscape requires surveyors to maintain current knowledge through:

- RICS technical updates on valuation standards and tax considerations

- Tax law seminars covering inheritance tax, business rates, and property taxation

- Market intelligence from transaction data and industry research

- Peer collaboration sharing practical approaches and case studies

Professional surveyors should view understanding surveyor roles as an evolving responsibility that extends beyond traditional property assessment into financial planning support.

Client Communication and Report Writing

Effective communication of the Valuation Impacts of 2026 Budget's £2 Million+ Property Taxes: Surveyor Strategies for High-End Market Adjustments is as important as the technical analysis itself. Clients need clear, actionable information to make informed decisions.

Structuring Tax-Aware Valuation Reports

Modern valuation reports for properties above £2 million should include:

Executive summary section:

- Clear statement of valuation figure

- One-paragraph explanation of key tax considerations

- Highlight of any significant risks or opportunities

Detailed tax impact analysis:

- Calculation of relief threshold position

- Quantification of potential inheritance tax exposure

- Explanation of market discount factors applied

- Comparison with pre-April 2026 valuation approaches

Recommendations section:

- Suggestions for ownership structure optimization (with tax advisor caveat)

- Marketing strategy recommendations reflecting tax considerations

- Timing considerations for potential transactions

Supporting documentation:

- Detailed comparable analysis with tax regime annotations

- Market data showing price trends in relevant segments

- Regulatory and policy background information

Clients purchasing properties in areas like Battersea or Marylebone particularly value this comprehensive approach.

Managing Client Expectations

The tax changes create uncertainty that can concern clients. Surveyors should:

✓ Be transparent about limitations in predicting market responses to tax changes

✓ Provide ranges rather than single-point valuations where appropriate

✓ Explain assumptions clearly, allowing clients to understand the analysis basis

✓ Recommend specialist advice for complex tax planning beyond surveying scope

✓ Document methodology thoroughly to support decision-making and future reference

Coordinating with Other Professionals

High-value property transactions increasingly require multi-disciplinary teams:

- Tax advisors for inheritance tax and estate planning strategies

- Legal professionals for ownership structure and transaction documentation

- Financial planners for overall wealth management integration

- Specialist surveyors for particular property types or technical issues

Professional surveyors should position themselves as coordinators who ensure all parties work from consistent property valuation information. When clients require specialized surveys, clear communication between all professionals ensures comprehensive service delivery.

Regulatory Compliance and Professional Standards

Navigating the Valuation Impacts of 2026 Budget's £2 Million+ Property Taxes: Surveyor Strategies for High-End Market Adjustments requires strict adherence to professional standards and regulatory requirements.

RICS Standards and Guidance

The Royal Institution of Chartered Surveyors maintains rigorous standards that govern valuation practice. In the context of 2026 tax changes, particular attention should be paid to:

RICS Valuation – Global Standards (Red Book):

- Compliance with VPS 1 (Terms of Engagement)

- Adherence to VPS 2 (Inspections, Investigations and Records)

- Application of VPS 3 (Valuation Reports)

- Following VPS 4 (Bases of Value, Assumptions and Special Assumptions)

- Implementation of VPS 5 (Valuation Approaches and Methods)

UK National Supplement requirements:

- Specific guidance for UK property valuations

- Compliance with UK regulatory frameworks

- Integration with UK tax legislation considerations

Surveyors must ensure their reports explicitly state which standards they follow and how tax considerations are incorporated within the RICS framework. Those seeking to understand why to choose RICS surveyors should recognize this commitment to professional standards.

Professional Indemnity Insurance

The complexity of tax-adjusted valuations increases professional liability exposure. Surveyors should:

- Review insurance coverage to ensure adequate protection for tax-related valuation work

- Clearly define scope of valuation services vs. tax advice in engagement letters

- Document limitations of tax analysis provided within valuation reports

- Maintain detailed records of assumptions, methodologies, and client communications

Ethical Considerations

The high-value nature of affected properties creates potential ethical challenges:

⚖️ Independence: Maintaining objectivity despite client pressure for particular valuations

🔍 Transparency: Clear disclosure of limitations and assumptions

📋 Competence: Only accepting instructions within areas of expertise

🤝 Integrity: Resisting pressure to manipulate valuations for tax avoidance purposes

Professional surveyors must prioritize ethical practice over client preferences, even when this creates difficult conversations about property values.

Conclusion

The Valuation Impacts of 2026 Budget's £2 Million+ Property Taxes: Surveyor Strategies for High-End Market Adjustments represent a fundamental shift in how luxury properties are valued and transacted across southern England. The £2.5 million relief cap, transferable to £5 million for married couples, creates clear valuation thresholds that professional surveyors must navigate with precision and expertise[1][2].

Successful valuation practice in 2026 requires surveyors to integrate tax considerations into traditional methodologies while maintaining RICS compliance and professional standards. The comparative method needs adjustment for pre- and post-April 2026 transactions, the investment method must incorporate increased business rates for properties over £500,000 rateable value, and the residual method requires recalibration for development viability under the new tax regime.

Regional variations matter significantly, with prime central London areas like Westminster, Kensington, and Knightsbridge showing different market dynamics than suburban luxury markets or agricultural estates. Surveyors must develop location-specific expertise and maintain detailed comparable databases reflecting post-tax-change transactions.

Actionable Next Steps for Property Professionals

For surveyors:

- Update valuation templates to incorporate tax impact analysis sections

- Build post-April 2026 comparable databases for relevant market segments

- Invest in continuing professional development covering tax and valuation integration

- Review professional indemnity insurance to ensure adequate coverage

- Develop relationships with tax advisors for complex client situations

For property owners:

- Obtain updated valuations reflecting 2026 tax changes for estate planning

- Consider ownership structure optimization with professional tax advice

- Review timing of potential property transactions in light of tax implications

- Engage RICS-qualified surveyors experienced in high-value property assessment

- Plan proactively for the April 2027 property income tax increases[2][3]

For property buyers:

- Request tax-adjusted valuations as part of purchase due diligence

- Factor inheritance tax exposure into purchase price negotiations

- Consider joint ownership structures to maximize relief allowances

- Engage professional advisors early in the transaction process

- Understand regional market dynamics affecting value and liquidity

The luxury property market continues to evolve in response to the 2026 tax changes. Surveyors who develop sophisticated tax-aware valuation methodologies, maintain rigorous professional standards, and communicate effectively with clients will provide the greatest value in this transformed landscape. As the market adjusts to the new tax regime, the role of professional property surveyors becomes increasingly critical in ensuring accurate valuations that reflect both property characteristics and tax implications.

For property owners and buyers navigating these complex changes, engaging experienced surveyors who understand the Valuation Impacts of 2026 Budget's £2 Million+ Property Taxes: Surveyor Strategies for High-End Market Adjustments is no longer optional—it's essential for informed decision-making and successful transactions in the high-end property market.

References

[1] 10 Key Tax Changes April 2026 – https://www.armstrongwatson.co.uk/news/2026/03/10-key-tax-changes-april-2026

[2] Uk Tax Landscape Key Changes For 2026 – https://taxscape.deloitte.com/article/uk-tax-landscape–key-changes-for-2026.aspx

[3] New Property Tax – https://hoa.org.uk/news/new-property-tax/