{"cover":"Professional landscape format (1536x1024) hero image featuring bold text overlay 'Valuation Challenges in 2026's Affordability-Driven Market' in extra large 72pt white sans-serif font with dark semi-transparent overlay box, centered in upper third. Background shows split composition: left side displays modern chartered surveyor reviewing property documents with digital tablet showing declining mortgage rate graphs, right side shows residential UK property exterior with 'For Sale' sign. Foreground includes subtle overlay of descending percentage symbols (6% to 5.98%) and upward-trending affordability arrows. Color scheme: deep navy blue, white, gold accents. High contrast, editorial magazine cover quality, professional financial-property aesthetic with clean modern typography and balanced composition.","content":["Landscape format (1536x1024) detailed infographic showing mortgage rate decline timeline from 2022 to 2026, featuring prominent line graph with rates dropping from 6.76% (2025) to 5.98% (February 2026), annotated with key milestones and Bank of England policy decisions. Visual includes three-column comparison chart showing 30-year fixed, 15-year fixed, and jumbo mortgage rates with percentage changes. Background features faded UK housing market imagery with calculator and financial documents. Color palette: professional blues, greens for positive trends, clean white background with subtle grid lines, data visualization style with clear labels and annotations.","Landscape format (1536x1024) conceptual illustration showing chartered surveyor conducting property valuation assessment, split-screen composition comparing traditional valuation methodology (left) versus recalibrated 2026 approach (right). Left side shows clipboard with standard comparable sales data, right side displays digital tablet with dynamic market indicators, affordability metrics, and rate-adjusted valuations. Central element features balance scale weighing 'Rate-Driven Price Movements' versus 'Market Fundamentals'. Background includes UK residential properties, RICS building survey documents, and subtle overlay of financial charts. Professional color scheme: burgundy, navy, white, with modern clean aesthetic and clear visual hierarchy.","Landscape format (1536x1024) professional photograph of modern surveyor's desk workspace showing detailed property valuation report being reviewed, with multiple data sources visible: mortgage rate forecast charts showing 6% projection through 2027, property market analysis spreadsheets, RICS survey documentation, and digital tools displaying comparative market analysis. Foreground includes calculator, measuring tools, and property photographs. Background shows dual monitors displaying geographic property data and valuation software interfaces. Warm professional lighting, shallow depth of field focusing on valuation documents, color scheme of warm woods, professional blues, and document whites, editorial business photography style with authentic workspace details."]}

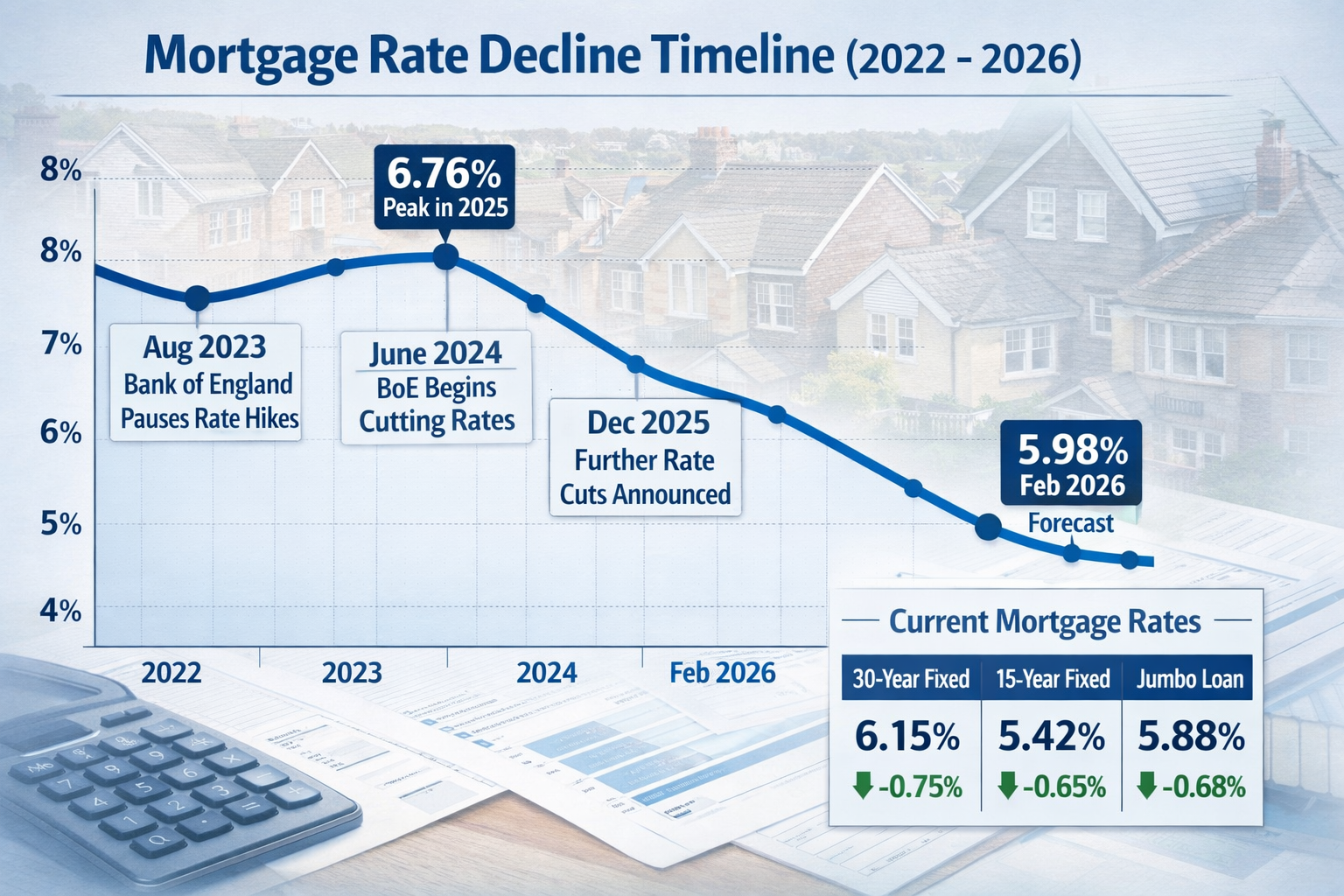

As mortgage rates dip below 6% for the first time in over three years, the UK property market stands at a critical inflection point. 📊 The Valuation Challenges in 2026's Affordability-Driven Market: Recalibrating Survey Assessments as Mortgage Rates Fall represent a fundamental shift that chartered surveyors must navigate with precision and expertise. With the 30-year fixed rate reaching 5.98% as of February 26, 2026[3][5], and Bank of England interest rate cuts improving borrowing capacity, property valuations can no longer rely solely on historical comparable sales data. The question facing surveyors today is whether recent price movements reflect genuine market fundamentals or merely rate-driven speculation.

This transformation demands a complete recalibration of valuation methodologies. As affordability pressures ease and mortgage applications increase by 0.4%[1], surveyors must distinguish between sustainable value appreciation and temporary rate-induced price inflation. The stakes have never been higher for accurate property assessments.

Key Takeaways

- Mortgage rates fell below 6% for the first time since 2022, with 30-year fixed rates at 5.98%, creating new affordability dynamics that impact property valuations[3][5]

- Surveyors must recalibrate methodologies to distinguish between rate-driven price movements and genuine market fundamentals as borrowing costs decline

- Refinancing activity surged 4%, with applications reaching 58.6% of total mortgage applications, indicating significant market movement[1]

- Year-over-year improvement of 78 basis points from 6.76% to 5.98% requires reassessment of comparable sales data and valuation assumptions[5]

- Forecasts predict rates around 6% through 2027, necessitating long-term valuation strategies that account for sustained affordability improvements[2]

Understanding the 2026 Mortgage Rate Environment and Its Valuation Impact

The Historic Rate Decline: Context and Magnitude

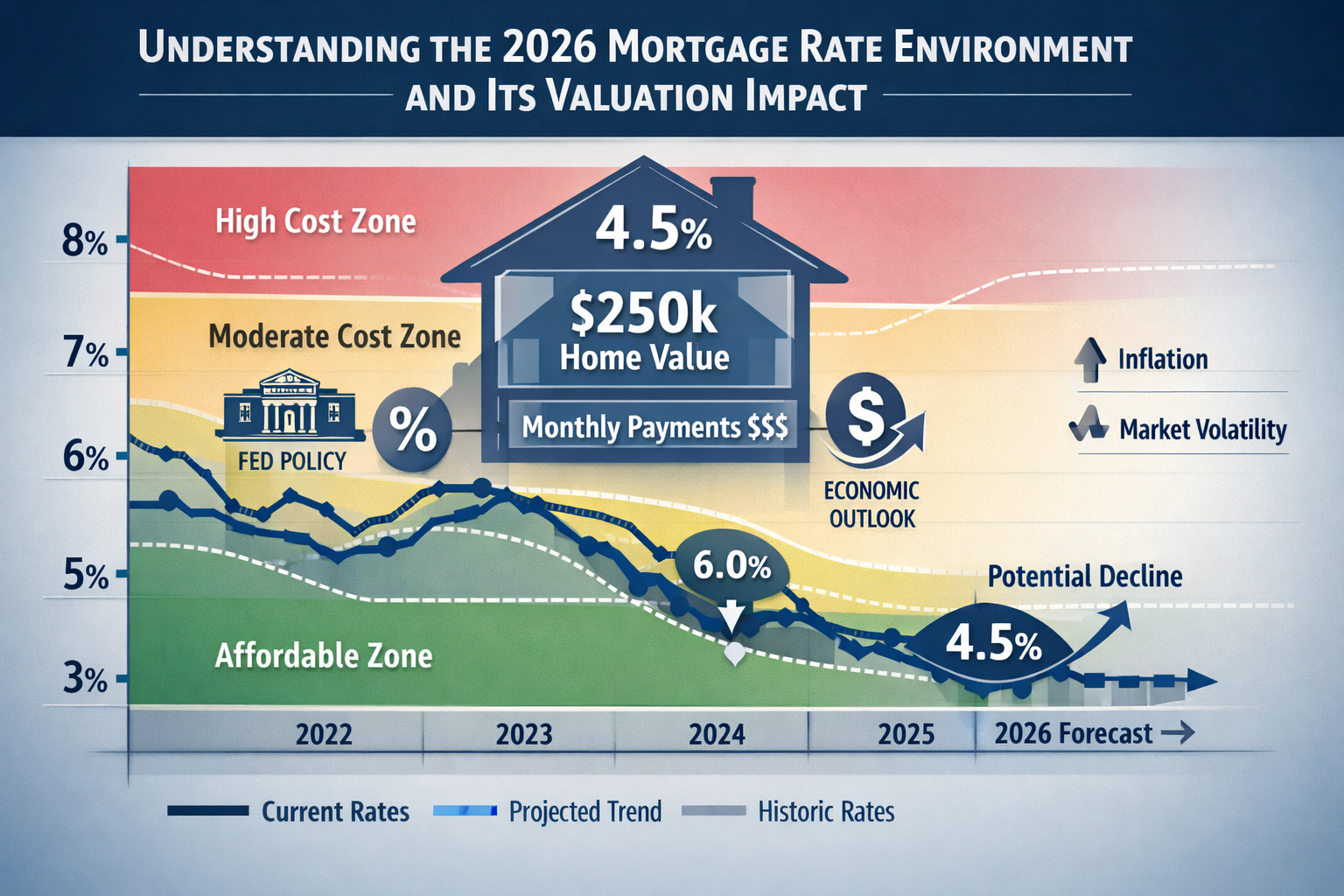

The mortgage rate landscape in 2026 represents a dramatic reversal from the peak rates experienced in recent years. According to Freddie Mac's benchmark data, the 30-year fixed mortgage rate decreased to 5.98% from 6.01% the previous week[3][5], marking the first time rates have fallen below the psychologically significant 6% threshold since mid-2022. This 78 basis point improvement from the 6.76% rate recorded one year ago[5] fundamentally alters the affordability equation for property buyers.

Optimal Blue data reveals even more granular movement, with 30-year conventional rates at 5.942%, representing minimal daily fluctuation but significant weekly trends[1]. Meanwhile, 15-year fixed rates increased slightly to 5.44-5.45%[3][4][5], and jumbo mortgage rates averaged between 6.141-6.23%, down 10-17 basis points week-over-week[1][4].

For chartered surveyors conducting RICS building surveys, these rate movements create valuation complexity. Properties that appeared overpriced at 6.5% rates may now represent fair value at sub-6% rates, yet this affordability improvement doesn't necessarily indicate fundamental property value changes.

Market Response: Applications and Refinancing Activity

The market's response to falling rates has been immediate and measurable. Mortgage applications increased 0.4% for the week ending February 20, 2026[1], signaling renewed buyer confidence. More significantly, refinancing activity increased 4%, with refi applications reaching 58.6% of total applications[1]. This refinancing surge indicates existing homeowners are capitalizing on improved rates, potentially freeing up equity for property improvements or creating competitive pressure on available housing stock.

When surveyors prepare RICS Homebuyer surveys, understanding this refinancing dynamic becomes crucial. Properties may command premium valuations not solely based on physical condition or location, but on the improved affordability calculations that buyers can now justify at lower rates.

Forward-Looking Rate Projections

Fannie Mae's forecasts provide essential context for long-term valuation strategies, predicting rates will remain around 6% through 2026 and 2027, with expectations that rates will drift slightly lower[2]. This sustained affordability environment differs markedly from temporary rate dips that characterized previous market cycles.

For surveyors, this forecast stability suggests that current valuations should reflect a "new normal" rather than temporary market conditions. Properties assessed in 2026 must be valued with the understanding that sub-6% rates may persist, fundamentally resetting price-to-income ratios and affordability thresholds across the market.

Valuation Challenges in 2026's Affordability-Driven Market: Core Methodological Concerns

The Comparable Sales Dilemma

Traditional valuation methodology relies heavily on comparable sales analysis, examining recent transactions of similar properties in similar locations. However, the Valuation Challenges in 2026's Affordability-Driven Market: Recalibrating Survey Assessments as Mortgage Rates Fall create a fundamental problem: which comparables are truly relevant?

Properties sold six months ago at 6.5% mortgage rates operated under completely different affordability constraints than properties transacting today at 5.98% rates. A buyer's monthly payment capacity has improved by approximately 8-10% solely due to rate changes, without any change in property fundamentals. This means:

- Historical comparables may undervalue current market potential

- Recent sales may reflect rate-driven premiums rather than sustainable values

- Geographic variations in rate sensitivity create inconsistent comparable pools

When conducting property surveys across different London locations, surveyors must weight comparables based on the prevailing rate environment at the time of each transaction, applying appropriate adjustments for affordability changes.

Rate-Driven Price Inflation vs. Fundamental Value

Perhaps the most critical challenge facing surveyors in 2026 is distinguishing between rate-driven price inflation and genuine fundamental value appreciation. Consider two scenarios:

Scenario A: Rate-Driven Inflation

- Property prices increase 5-7% following rate declines

- No improvements to property condition, location amenities, or infrastructure

- Price increase reflects expanded buyer purchasing power only

- Value vulnerable to rate reversals

Scenario B: Fundamental Value Appreciation

- Property prices increase due to area regeneration, transport improvements, or school quality enhancements

- Rate changes amplify but don't create the value increase

- Value supported by tangible improvements regardless of rate environment

Surveyors must develop analytical frameworks that isolate these factors. A specific defect survey might reveal that a property's structural integrity hasn't changed, yet its market price has increased 6% in three months—a clear signal of rate-driven inflation rather than fundamental value change.

Adjusting Valuation Models for Affordability Metrics

The 2026 market demands that surveyors incorporate affordability metrics directly into valuation models. Traditional approaches focused primarily on:

- Square footage comparisons

- Location quality assessments

- Property condition evaluations

- Historical price trends

Modern valuations must additionally consider:

- Monthly payment affordability at current rates

- Debt-to-income ratio implications for typical buyers

- Rate sensitivity analysis showing value ranges across rate scenarios

- Buyer demographic shifts enabled by improved affordability

This expanded framework requires surveyors to understand not just property characteristics but also financial market dynamics and buyer behavior patterns. When preparing comprehensive homebuyers reports, including affordability context helps clients understand whether a property represents sustainable value or rate-dependent pricing.

Geographic and Segment-Specific Variations

The Valuation Challenges in 2026's Affordability-Driven Market: Recalibrating Survey Assessments as Mortgage Rates Fall manifest differently across property segments:

| Property Segment | Rate Sensitivity | Valuation Challenge |

|---|---|---|

| First-time buyer properties (£200k-£350k) | High | Extreme affordability impact; small rate changes create large demand shifts |

| Mid-market family homes (£350k-£600k) | Moderate-High | Significant refinancing activity; comparable sales highly variable |

| Luxury properties (£1M+) | Low-Moderate | Jumbo rate changes (6.141-6.23%)[1][4] less impactful; cash buyers prevalent |

| Investment properties | Moderate | Rental yield calculations shift with financing costs |

Surveyors working across diverse London locations must calibrate their approaches based on these segment-specific dynamics, recognizing that a one-size-fits-all methodology fails to capture market nuances.

Recalibrating Survey Assessments: Practical Methodologies for 2026

Implementing Rate-Adjusted Comparable Analysis

To address the comparable sales dilemma, surveyors should implement rate-adjusted comparable analysis that normalizes historical sales data to current rate environments. This methodology involves:

Step 1: Identify Comparable Properties

Select properties matching key physical characteristics (size, condition, location) within the past 12-18 months.

Step 2: Determine Rate Environment for Each Comparable

Record the prevailing mortgage rate at the time of each comparable sale.

Step 3: Calculate Affordability Adjustment Factor

Use the formula:

Adjustment Factor = (Monthly Payment at Historic Rate) / (Monthly Payment at Current Rate)

Step 4: Apply Adjustment to Sale Price

Adjust historical sale prices upward or downward based on affordability changes.

Step 5: Weight Recent Comparables More Heavily

Assign greater weight to sales occurring in similar rate environments.

This approach provides rate-normalized valuations that better reflect current market conditions while maintaining the integrity of comparable sales methodology. Surveyors conducting building evaluations can integrate these financial adjustments with traditional physical assessment criteria.

Developing Dual-Scenario Valuation Frameworks

Given the uncertainty inherent in rate-driven markets, prudent surveyors should provide dual-scenario valuations that present:

Conservative Scenario:

- Assumes rates return to 6.5-7% within 18-24 months

- Values property based on reduced affordability

- Identifies price support levels if rate environment deteriorates

- Highlights properties vulnerable to rate-driven corrections

Optimistic Scenario:

- Assumes rates remain at or below 6% through 2027 (aligned with Fannie Mae forecasts)[2]

- Values property based on sustained affordability improvements

- Identifies upside potential if rate environment stabilizes

- Highlights properties positioned to benefit from continued rate declines

This dual-scenario approach provides clients with comprehensive risk assessment, enabling informed decision-making regardless of future rate movements. When preparing survey assessments that inform negotiations, this framework empowers buyers and sellers with realistic value ranges.

Incorporating Forward-Looking Market Indicators

Beyond backward-looking comparable sales, 2026 valuations should integrate forward-looking market indicators:

- Mortgage application trends: The 0.4% increase in applications[1] suggests strengthening demand

- Refinancing ratios: The 58.6% refinancing share[1] indicates market liquidity and owner confidence

- Rate forecasts: Fannie Mae's 6% projection through 2027[2] provides stability assumptions

- Economic indicators: Employment rates, wage growth, and inflation trends affecting buyer capacity

Surveyors should explicitly reference these indicators in valuation reports, providing context that helps clients understand the macroeconomic forces influencing property values. This approach transforms a standard property survey into a comprehensive market intelligence document.

Enhancing Client Communication and Transparency

The complexity of Valuation Challenges in 2026's Affordability-Driven Market: Recalibrating Survey Assessments as Mortgage Rates Fall demands enhanced client communication. Surveyors should:

✅ Explicitly state rate assumptions used in valuations

✅ Explain affordability calculations showing monthly payment implications

✅ Provide rate sensitivity analysis demonstrating value changes across rate scenarios

✅ Distinguish fundamental vs. rate-driven value components

✅ Include market context explaining current rate environment and forecasts

This transparency builds client trust and ensures that property buyers, sellers, and lenders understand the assumptions underlying valuation conclusions. When clients prepare for RICS home surveys, providing this educational context enhances the value of professional surveying services.

Leveraging Technology and Data Analytics

Modern valuation challenges require modern tools. Surveyors should leverage:

Automated Valuation Models (AVMs) that incorporate real-time rate data and affordability calculations

Geographic Information Systems (GIS) that map rate sensitivity across different neighborhoods and property types

Machine Learning Algorithms that identify patterns in rate-driven price movements versus fundamental value changes

Financial Calculators integrated into survey reports that allow clients to model different rate scenarios

Market Data Platforms providing real-time comparable sales with rate environment context

By combining traditional surveying expertise with advanced data analysis capabilities, professionals can deliver valuations that reflect both property-specific characteristics and broader market dynamics.

Strategic Implications for Different Market Participants

For Property Buyers

Buyers navigating the 2026 market should recognize that affordability improvements create opportunity but also risk. When commissioning surveys, buyers should:

- Request rate-adjusted valuations that show value across different rate scenarios

- Understand whether asking prices reflect fundamental value or rate-driven inflation

- Consider properties that may be undervalued if sellers haven't adjusted to improved affordability

- Avoid overpaying for rate-driven premiums that may evaporate if rates rise

Working with qualified local surveyors who understand these dynamics provides crucial protection against overpaying in an affordability-driven market.

For Property Sellers

Sellers face the opposite challenge: capturing the value created by improved affordability without overpricing properties relative to fundamental value. Sellers should:

- Obtain professional valuations that account for current rate environments

- Understand that buyers can afford higher prices at 5.98% rates than at 6.5% rates

- Price properties to reflect improved buyer capacity while maintaining justifiable value

- Be prepared to adjust if rates change during the selling process

For Mortgage Lenders

Lenders bear significant risk in rate-driven markets, as property values securing loans may fluctuate with rate changes. Lenders should:

- Require valuations that explicitly address rate sensitivity and affordability factors

- Implement loan-to-value ratios that account for potential rate reversals

- Distinguish between properties with fundamental value support versus rate-dependent pricing

- Consider dual-scenario valuations when assessing lending risk

For Property Investors

Investors must evaluate whether rate-driven price increases justify acquisition or whether fundamental rental yields and capital appreciation potential support investment decisions. Investors should:

- Focus on rental yield calculations that remain viable across rate scenarios

- Avoid properties where purchase prices reflect rate-driven premiums without rental income support

- Consider refinancing existing holdings to capitalize on improved rates

- Evaluate markets where affordability improvements may drive sustained demand growth

Conclusion

The Valuation Challenges in 2026's Affordability-Driven Market: Recalibrating Survey Assessments as Mortgage Rates Fall represent more than a technical adjustment—they demand a fundamental rethinking of how chartered surveyors approach property valuation. With 30-year fixed rates at 5.98%[3][5], the lowest level in over three years, and forecasts suggesting sustained rates around 6% through 2027[2], the market has entered a new affordability paradigm that cannot be ignored.

Surveyors must move beyond traditional comparable sales analysis to implement rate-adjusted methodologies that distinguish genuine fundamental value from rate-driven price inflation. This requires incorporating affordability metrics, developing dual-scenario frameworks, leveraging forward-looking market indicators, and enhancing client communication with transparent rate assumptions.

The 78 basis point year-over-year improvement[5] and 4% increase in refinancing activity[1] demonstrate that market participants are responding rapidly to improved affordability. Surveyors who fail to recalibrate their assessments risk providing outdated valuations that either undervalue properties in the new affordability environment or overvalue properties vulnerable to rate reversals.

Actionable Next Steps

For surveyors seeking to master these challenges:

- Develop rate-adjustment protocols for comparable sales analysis that normalize historical data to current affordability conditions

- Create dual-scenario valuation templates that present conservative and optimistic value ranges based on different rate assumptions

- Invest in technology platforms that integrate real-time rate data with traditional property assessment tools

- Enhance client reporting to explicitly state rate assumptions and affordability calculations

- Pursue continuing education on financial market dynamics and their intersection with property valuation

- Establish relationships with mortgage brokers and financial advisors to better understand buyer capacity in current market conditions

The surveyors who successfully navigate the Valuation Challenges in 2026's Affordability-Driven Market: Recalibrating Survey Assessments as Mortgage Rates Fall will provide superior value to clients while maintaining the professional integrity and accuracy that define chartered surveying excellence. 🏡

As the market continues evolving, the fundamental principle remains unchanged: accurate property valuation requires understanding not just bricks and mortar, but the financial context in which properties are bought, sold, and valued. The 2026 affordability-driven market simply makes this principle more explicit—and more critical—than ever before.

References

[1] Current Mortgage Rates 02 26 2026 – https://fortune.com/article/current-mortgage-rates-02-26-2026/

[2] Mortgage Rates February 25 2026 – https://www.bankrate.com/mortgages/analysis/mortgage-rates-february-25-2026/

[3] Mortgage Rates February 26 2026 – https://www.foxbusiness.com/economy/mortgage-rates-february-26-2026

[4] Mortgage Rates For Thursday February 26 2026 – https://www.bankrate.com/mortgages/todays-rates/mortgage-rates-for-thursday-february-26-2026/

[5] Pmms – https://www.freddiemac.com/pmms

[6] Mortgage30us – https://fred.stlouisfed.org/series/MORTGAGE30US