The UK property market stands at a pivotal crossroads in early 2026. While national headlines suggest stabilisation, a deeper examination of the RICS January 2026 Survey Insights: Building Survey Strategies for Stabilising House Prices and Regional Divides reveals a more nuanced picture—one where tentative recovery signals clash with persistent regional disparities. For property professionals, buyers, and investors, understanding these dynamics is no longer optional; it's essential for making informed decisions in an increasingly fragmented market.

The latest Royal Institution of Chartered Surveyors (RICS) data paints a picture of cautious optimism tempered by geographical reality. As buyer enquiries improve and long-term sales expectations strengthen, the widening North-South divide demands tailored approaches to property assessment and valuation. This comprehensive analysis explores how building survey strategies must evolve to address these diverging market conditions.

Key Takeaways

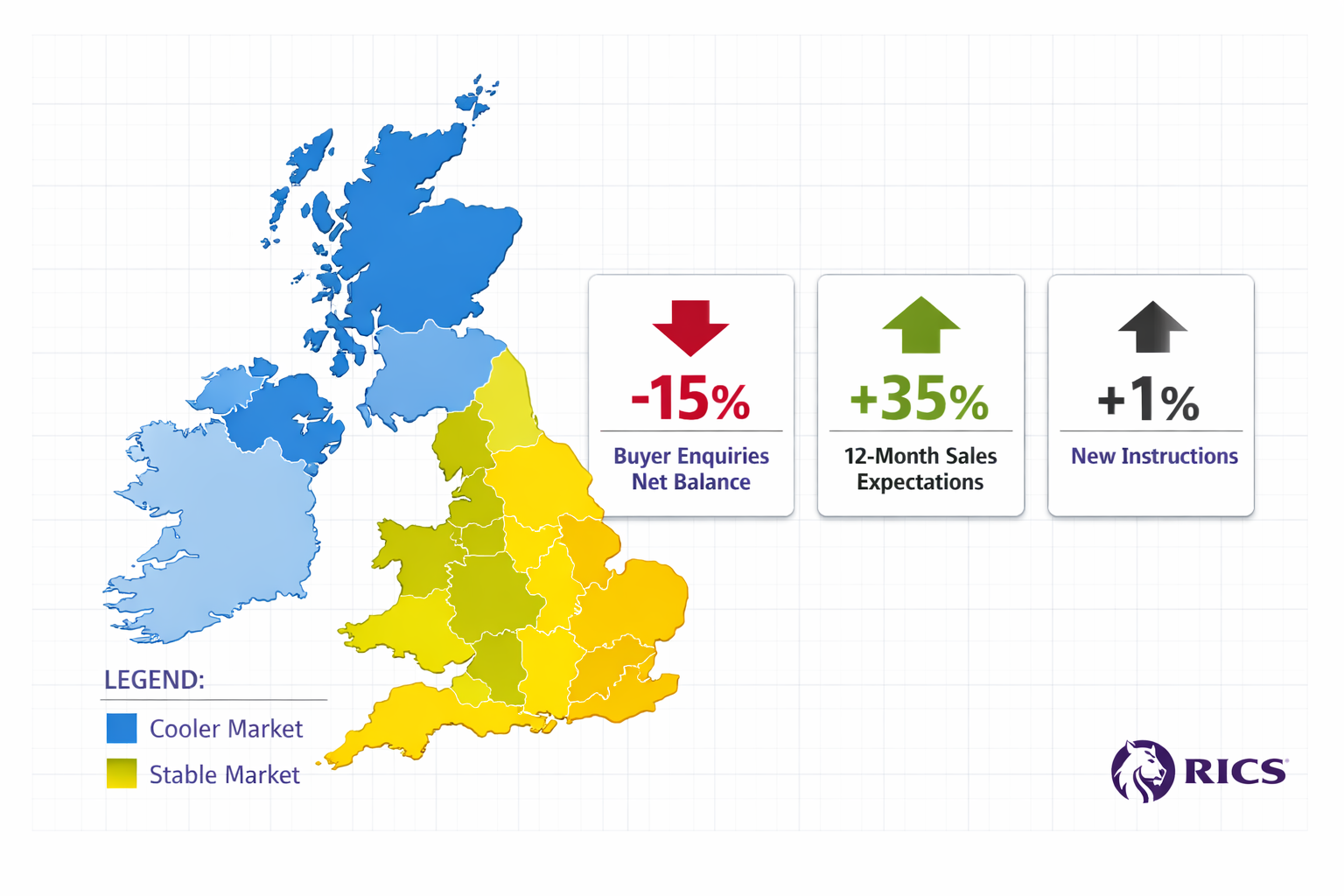

- 🏠 Buyer enquiries improved to -15% in January 2026 from -21% in December 2025, signaling tentative market recovery but still reflecting overall caution

- 📊 Strong 12-month outlook with +35% net balance expecting increased sales activity, the most optimistic reading since December 2024

- 🗺️ Regional divergence widening significantly, with Northern Ireland and Scotland experiencing different market conditions than Southern regions

- 🔍 Building surveys (Level 2 and Level 3) increasingly critical for risk identification and price negotiations in selective markets

- 💷 Accurate pricing remains essential, with over-ambitious valuations leading to extended marketing periods and necessary price reductions

Understanding the RICS January 2026 Survey Insights: Building Survey Strategies for Stabilising House Prices and Regional Divides

Market Stabilisation Signals and Persistent Challenges

The January 2026 RICS Residential Market Survey, covering 456 branches from 232 responses, reveals market conditions showing tentative signs of improvement[1]. Several activity-related indicators recorded their least negative readings in several months, suggesting the market may be turning a corner after an extended period of subdued activity.

New buyer enquiries recorded a net balance of -15% in January, a marked improvement from -21% in December 2025[1]. While still negative, this upward trajectory indicates growing consumer confidence and willingness to engage with the property market. However, the negative reading reminds us that demand remains below historical norms.

Perhaps most striking is the 12-month sales expectations figure: a net balance of +35% of survey participants anticipate increased sales activity over the next year[1]. This represents the strongest reading since December 2024 and reflects growing conviction among property professionals that a recovery trajectory is underway.

Yet caution persists in the near term. Three-month sales expectations recorded a net balance of just +4% in January, a significant drop from December's +22%[1]. This indicates that while professionals are optimistic about the medium-term outlook, they expect the immediate months to remain relatively flat.

The Supply-Demand Imbalance Continues

One of the most persistent challenges facing the UK property market is the ongoing supply constraint. New instructions showed minimal month-on-month movement with a net balance of +1% in January, broadly in line with December's -1%[1]. This stagnation in new listings continues to limit buyer choice and supports price stability, even in softer market conditions.

The constrained supply environment has several implications:

- Limited inventory keeps prices from falling significantly despite subdued demand

- Selective buyers can afford to be more discerning about property condition

- Competition for quality stock remains intense in desirable locations

- Properties with defects face longer marketing periods and price resistance

For property professionals, this supply-demand dynamic underscores the importance of thorough RICS building surveys that accurately assess property condition and value in a market where both buyers and sellers need reliable information.

Regional Divergence: The Widening North-South Gap

Perhaps the most significant finding in the RICS January 2026 Survey Insights: Building Survey Strategies for Stabilising House Prices and Regional Divides is the emerging geographical fragmentation. A widening divergence is becoming evident across different parts of the UK, particularly affecting Northern Ireland and Scotland differently than other regions[1].

This regional variation reflects several underlying factors:

| Region | Market Characteristics | Survey Strategy Implications |

|---|---|---|

| London & South East | Price stabilisation, selective buyers, affordability constraints | Emphasis on detailed condition assessment, negotiation leverage |

| Northern England | Relatively stronger demand, better affordability | Standard surveys sufficient for most properties |

| Scotland | Market softening, cautious buyer sentiment | Enhanced due diligence, conservative valuations |

| Northern Ireland | Distinct market dynamics, different regulatory environment | Specialist local knowledge essential |

For surveyors and property professionals operating across multiple regions, a one-size-fits-all approach no longer suffices. Survey strategies must be tailored to local market conditions, with particular attention to regional pricing dynamics and buyer expectations.

Building Survey Strategies for the RICS January 2026 Survey Insights: Building Survey Strategies for Stabilising House Prices and Regional Divides

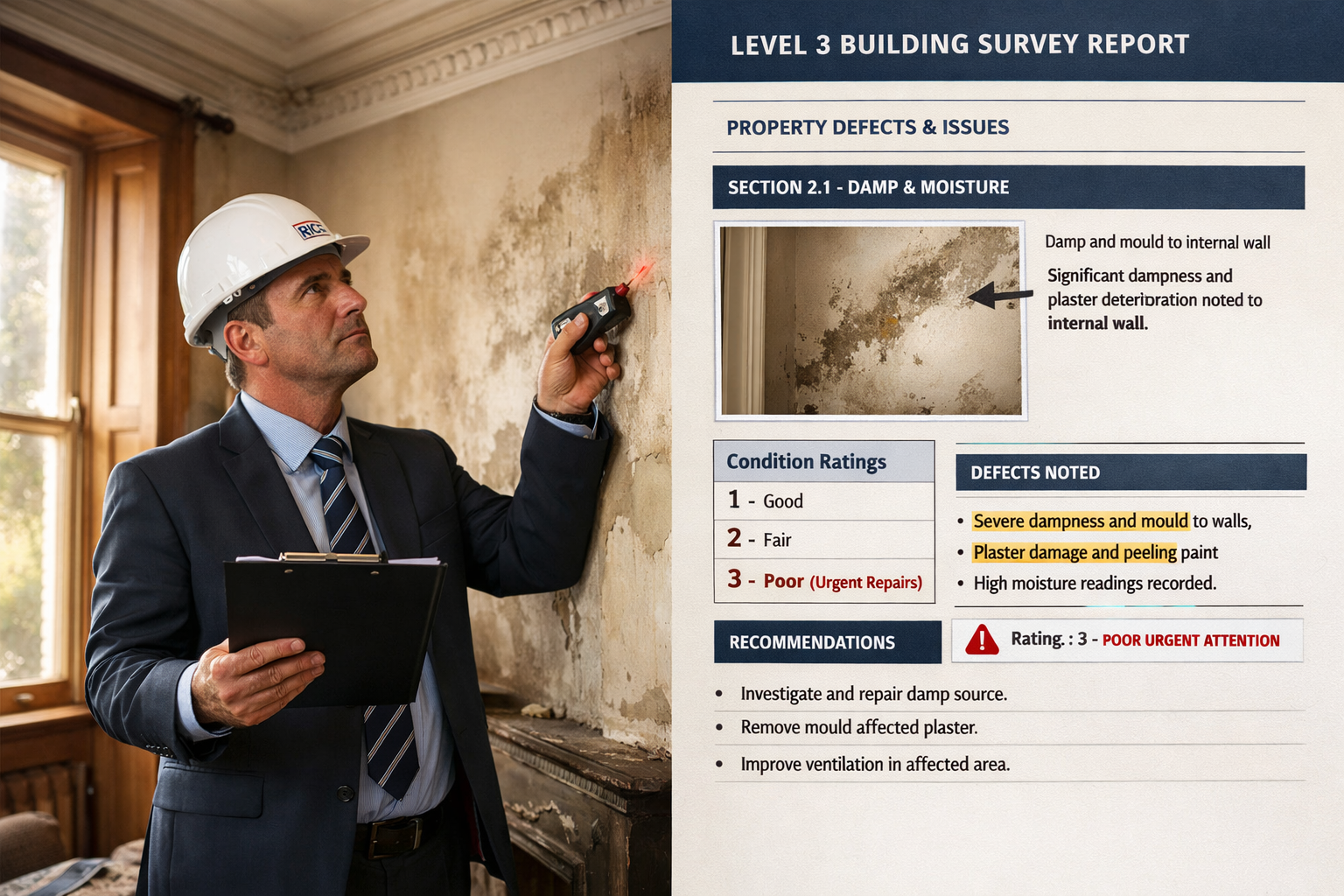

The Growing Importance of Level 2 and Level 3 Surveys

In the current market environment characterized by buyer caution and regional variation, there is continuing strong demand for RICS Home Surveys (Level 2 and Level 3), particularly for older or altered properties[2]. Purchasers increasingly seek clarity around condition and potential liabilities before committing to what remains, for most, the largest financial decision of their lives.

The distinction between survey levels becomes crucial in different market contexts:

Level 2 (RICS Home Survey):

- ✅ Suitable for conventional properties in reasonable condition

- ✅ Provides condition ratings for key elements

- ✅ Identifies urgent defects and potential legal issues

- ✅ More affordable option for budget-conscious buyers

- ✅ Appropriate in stronger regional markets with newer stock

Level 3 (RICS Building Survey):

- ✅ Comprehensive inspection for older, altered, or unusual properties

- ✅ Detailed analysis of construction and condition

- ✅ Essential for properties with visible defects or complex histories

- ✅ Provides detailed repair cost guidance

- ✅ Critical in softer markets where negotiation leverage is important

For buyers navigating the RICS January 2026 Survey Insights: Building Survey Strategies for Stabilising House Prices and Regional Divides, understanding which survey level is appropriate can mean the difference between a sound investment and a costly mistake.

Accurate Pricing and Market Positioning

Properties that are well-presented and sensibly priced continue to perform best, while over-ambitious pricing is being challenged, often leading to extended marketing periods or price adjustments across Hertfordshire, Essex, and Cambridgeshire[2]. This observation has profound implications for survey strategy and valuation practice.

Early identification of risk through detailed surveys remains a key factor in supporting negotiations and protecting value in the current selective market[2]. When buyers commission comprehensive building surveys, they gain several strategic advantages:

- Negotiating Power: Documented defects provide objective evidence for price reductions

- Risk Mitigation: Understanding repair obligations prevents post-purchase surprises

- Budget Planning: Accurate repair cost estimates inform financial planning

- Insurance Clarity: Identified issues can be addressed before coverage becomes problematic

The average price reduction after survey varies by property condition and market strength, but in the current environment, buyers with detailed survey evidence are achieving meaningful adjustments—particularly in regions experiencing softer demand.

Evidence-Based Valuations in a Fragmented Market

Independent RICS Red Book Valuations remain important in a stabilising but regionally varied market, where lenders, legal advisers, and private clients require defensible and well-supported figures[2]. The regional divergence highlighted in the January 2026 survey makes standardised valuation approaches increasingly problematic.

Professional valuers must now consider:

- Regional market momentum and directional trends

- Local supply-demand dynamics specific to postcode areas

- Property-specific condition and maintenance requirements

- Comparable evidence from genuinely similar properties in similar market conditions

- Forward-looking indicators rather than purely historical data

For property professionals, choosing RICS surveyors ensures valuations meet professional standards and provide the defensible evidence required by lenders and legal advisers in an uncertain market.

Survey Strategies for Different Property Types

The RICS January 2026 Survey Insights: Building Survey Strategies for Stabilising House Prices and Regional Divides necessitate differentiated approaches based on property characteristics:

Period Properties (Pre-1919):

- 🏛️ Comprehensive Level 3 surveys essential

- 🏛️ Particular attention to structural movement, damp, and obsolete materials

- 🏛️ Specialist investigations often required (timber, damp, structural)

- 🏛️ Higher negotiation potential due to typical maintenance backlogs

Inter-War Properties (1919-1945):

- 🏡 Level 2 surveys typically sufficient unless significant alterations evident

- 🏡 Focus on cavity wall condition, original windows, and roof coverings

- 🏡 Moderate defect expectations with predictable repair profiles

Post-War Properties (1945-1980):

- 🏘️ Level 2 surveys appropriate for standard construction

- 🏘️ Attention to non-traditional construction methods where applicable

- 🏘️ Electrical and heating system age considerations

Modern Properties (Post-1980):

- 🏢 Level 2 surveys generally adequate

- 🏢 Focus on building regulations compliance and warranty coverage

- 🏢 New-build snagging surveys for properties under 2 years old

Understanding what to do after a bad building survey report is equally important—particularly in the current market where buyers have increased negotiating leverage due to selective demand.

Practical Applications of RICS January 2026 Survey Insights: Building Survey Strategies for Stabilising House Prices and Regional Divides

Leveraging Survey Intelligence for Price Negotiations

In a market characterized by cautious buyers and constrained supply, survey findings become powerful negotiation tools. The key is translating technical survey observations into commercially relevant price adjustments.

Effective Negotiation Strategies:

1. Quantify Repair Costs Accurately

- Obtain contractor quotations for identified defects

- Include professional fees and VAT in cost estimates

- Consider disruption costs and temporary accommodation if required

- Present evidence in clear, professional format

2. Prioritise Material Issues

- Focus negotiations on structural, damp, and safety-critical defects

- Distinguish between urgent repairs and routine maintenance

- Highlight issues affecting mortgage ability or insurance coverage

3. Consider Market Context

- In softer markets (Scotland, Northern Ireland), buyers have stronger negotiating positions

- In constrained supply areas, sellers may resist adjustments more firmly

- Time on market indicates seller motivation and flexibility

4. Propose Reasonable Solutions

- Price reduction reflecting genuine repair costs

- Retention of funds held by solicitors pending repairs

- Seller completion of urgent works before exchange

- Warranty or insurance arrangements for specific defects

For first-time buyers, understanding how to leverage survey findings can mean the difference between overpaying and securing a fair price that reflects true property condition.

Regional Survey Strategy Adjustments

The widening regional divergence identified in the RICS January 2026 Survey Insights: Building Survey Strategies for Stabilising House Prices and Regional Divides requires location-specific approaches:

Southern Markets (London, South East, South West):

- Buyers remain cautious despite stabilisation signals

- Detailed surveys provide negotiation leverage in price-sensitive environment

- Focus on long-term maintenance costs given higher property values

- Emphasis on energy efficiency and modernisation requirements

Northern Markets (North East, North West, Yorkshire):

- Relatively stronger demand supports firmer pricing

- Standard surveys appropriate for most transactions

- Value-focused buyers prioritise move-in condition

- Renovation potential less attractive given lower capital appreciation

Scottish Market:

- Distinct legal framework (Home Report system)

- Additional private surveys increasingly common for buyer protection

- Market softening increases importance of condition assessment

- Conservative valuations reflecting cautious outlook

Northern Ireland:

- Separate regulatory environment and market dynamics

- Local surveyor knowledge essential for accurate assessment

- Different defect priorities (e.g., cavity wall insulation issues)

- Valuation approaches reflect distinct comparable evidence

The Role of Specialist Surveys and Investigations

Beyond standard building surveys, the current market environment often necessitates specialist investigations to address specific concerns:

Damp and Timber Surveys:

Properties with visible moisture issues or timber decay require specialist assessment. Understanding the causes, extent, and remediation costs is essential for accurate valuation and negotiation.

Structural Engineering Reports:

Where structural movement or significant defects are identified, specialist structural engineer input provides the detailed analysis required for repair specification and cost estimation.

Drainage Surveys:

CCTV drainage investigations identify hidden defects in underground drainage systems—a common source of expensive repair obligations that standard surveys cannot fully assess.

Energy Performance Assessments:

With increasing focus on energy efficiency and future regulatory requirements, detailed energy assessments inform buyers about potential improvement costs and running expenses.

Rental Market Considerations

The January 2026 RICS survey also reported that tenant demand in the lettings market edged higher, with a net balance of +13% reported[1]. This secondary indicator provides additional market confidence and has implications for survey strategy:

For Buy-to-Let Investors:

- Survey focus on maintenance costs affecting rental yield

- Assessment of compliance with rental property standards

- Evaluation of tenant appeal and rental positioning

- Long-term capital expenditure forecasting

For Landlords:

- Periodic condition surveys identify maintenance requirements

- Compliance surveys ensure regulatory adherence

- Energy efficiency assessments inform improvement priorities

The strengthening rental market provides an alternative exit strategy for properties that prove difficult to sell, making accurate condition assessment valuable for both purchase and investment decisions.

Future Outlook and Strategic Recommendations

Interpreting the 12-Month Positive Outlook

The +35% net balance of surveyors expecting increased sales activity over the next twelve months represents significant optimism[1]. However, this must be interpreted carefully within the context of regional variation and near-term caution.

What This Means for Property Decisions:

For Buyers:

- 📌 Current market provides good negotiating conditions

- 📌 Detailed surveys maximize value protection and negotiation leverage

- 📌 Regional variation means location selection increasingly critical

- 📌 Long-term outlook supports purchase decisions for quality properties

For Sellers:

- 📌 Realistic pricing essential to capitalize on improving sentiment

- 📌 Pre-sale surveys identify issues allowing proactive remediation

- 📌 Property presentation and condition increasingly important differentiators

- 📌 Regional market strength varies significantly—local advice essential

For Investors:

- 📌 Regional divergence creates both opportunities and risks

- 📌 Detailed due diligence through comprehensive surveys non-negotiable

- 📌 Rental market strength provides income security

- 📌 Long-term capital appreciation prospects vary significantly by location

Building a Robust Survey Strategy

Based on the RICS January 2026 Survey Insights: Building Survey Strategies for Stabilising House Prices and Regional Divides, property professionals and buyers should adopt the following strategic framework:

Step 1: Assess Regional Market Context

- Research local market conditions and trends

- Understand supply-demand dynamics in target area

- Consider regional economic fundamentals and outlook

- Evaluate comparable evidence and pricing trends

Step 2: Match Survey Level to Property and Market

- Select appropriate survey level based on property age, type, and condition

- Consider market strength when determining survey investment

- In softer markets, comprehensive surveys provide greater negotiation value

- For unusual or complex properties, always commission Level 3 surveys

Step 3: Engage Qualified RICS Professionals

- Ensure surveyor has relevant local market knowledge

- Verify RICS membership and professional indemnity insurance

- Discuss specific concerns and requirements before instruction

- Request examples of previous reports for similar properties

Step 4: Act Decisively on Survey Findings

- Review reports thoroughly and seek clarification where needed

- Obtain repair cost estimates for identified defects

- Develop negotiation strategy based on evidence

- Consider specialist investigations where recommended

Step 5: Integrate Survey Intelligence into Decision-Making

- Use survey findings to inform purchase price negotiations

- Factor repair costs into financial planning and budgeting

- Consider long-term maintenance implications

- Make informed decisions about proceeding, renegotiating, or withdrawing

Preparing for Continued Market Evolution

The UK property market in 2026 remains in transition. While the January RICS survey provides encouraging signals about medium-term recovery, the near-term outlook remains cautious and regionally varied. Property professionals and buyers must remain adaptable and evidence-focused.

Key Preparedness Strategies:

Monitor Market Indicators:

- Track monthly RICS survey releases for trend evolution

- Follow regional price indices and transaction volumes

- Monitor mortgage availability and interest rate movements

- Stay informed about regulatory and tax policy developments

Maintain Flexible Strategies:

- Avoid over-commitment to specific locations or property types

- Remain open to alternative approaches based on market feedback

- Build contingency into budgets for repair and improvement costs

- Consider multiple scenarios in investment planning

Prioritize Professional Advice:

- Engage qualified professionals early in property decisions

- Invest in comprehensive surveys and valuations

- Seek specialist input for complex or unusual situations

- Build relationships with trusted advisers for ongoing support

Conclusion

The RICS January 2026 Survey Insights: Building Survey Strategies for Stabilising House Prices and Regional Divides reveal a UK property market at a critical juncture. While national indicators suggest tentative stabilisation and growing medium-term optimism, the widening regional divergence demands nuanced, location-specific approaches to property assessment and valuation.

For buyers navigating this complex landscape, comprehensive building surveys represent not merely prudent due diligence but strategic tools for value protection and negotiation leverage. The improvement in buyer enquiries from -21% to -15%, combined with strong 12-month sales expectations of +35%, indicates growing market confidence—yet the near-term caution reflected in the +4% three-month outlook reminds us that recovery remains fragile and uneven.

The persistent supply constraint, with new instructions effectively flat at +1%, continues to support price stability even in softer demand environments. However, this same dynamic increases the importance of accurate condition assessment, as limited choice means buyers must thoroughly evaluate available properties rather than simply moving to alternatives.

Regional variation—particularly the distinct experiences of Northern Ireland, Scotland, and Southern England—underscores that national statistics mask significant local differences. Property professionals must tailor survey strategies, valuation approaches, and advice to reflect these geographical realities rather than applying standardised methods across diverse markets.

Actionable Next Steps

For Property Buyers:

- Commission appropriate survey levels based on property characteristics and market conditions

- Engage RICS-qualified surveyors with relevant local expertise

- Use survey findings to negotiate fair prices reflecting true property condition

- Factor repair costs and long-term maintenance into purchase decisions

- Consider regional market dynamics when selecting locations

For Property Sellers:

6. Price realistically based on current market conditions and comparable evidence

7. Consider pre-sale surveys to identify and address issues proactively

8. Present properties in optimal condition to maximize appeal

9. Be prepared for buyer survey findings and negotiate constructively

For Property Professionals:

10. Stay informed about evolving market conditions through regular RICS survey monitoring

11. Tailor advice and valuation approaches to regional market characteristics

12. Provide clients with evidence-based, defensible recommendations

13. Maintain professional standards and comprehensive professional indemnity coverage

The UK property market of 2026 rewards those who combine professional expertise with market intelligence and evidence-based decision-making. As stabilisation takes hold unevenly across regions, the role of thorough building surveys and accurate valuations becomes not just important but essential for protecting value and facilitating successful property transactions in an increasingly complex and fragmented market landscape.

References

[1] UK Residential Market Survey January 2026 – https://www.rics.org/content/dam/ricsglobal/documents/market-surveys/uk-residential-market-surveys/UK-Residential-Market-Survey_January-2026.pdf

[2] UK Residential Market Survey January 2026 – https://www.navah-consulting.co.uk/news/uk-residential-market-survey-january-2026

[3] UK RICS Residential Market Survey Jan 2026 – https://www.capitaleconomics.com/publications/uk-housing-market-update/uk-rics-residential-market-survey-jan-2026