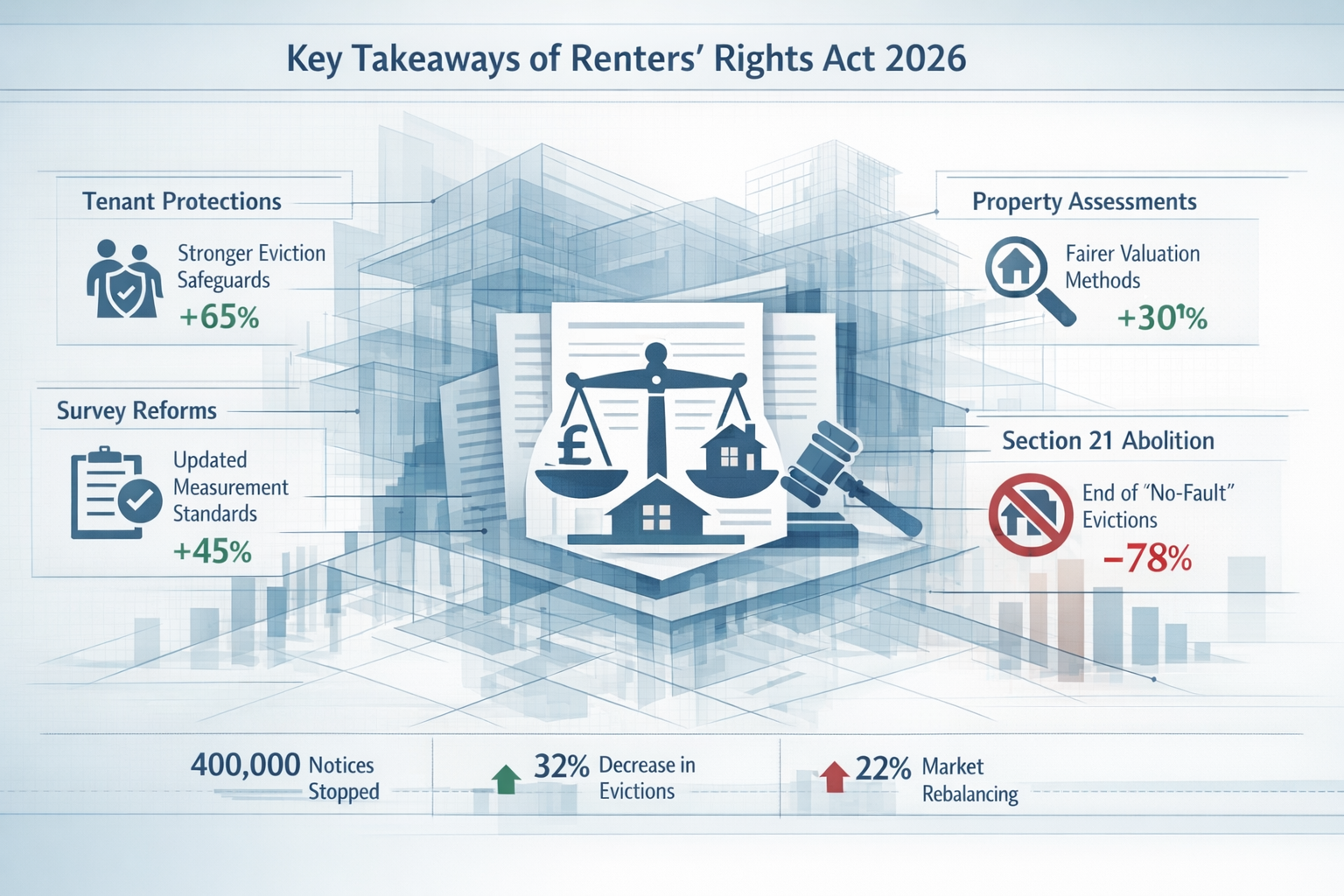

The Renters' Rights Act received Royal Assent on October 27, 2025, and fundamentally reshapes how 11 million private renters and 2.3 million landlords interact across England [1]. With all provisions taking effect from May 1, 2026, property valuers face their most significant challenge in decades: recalibrating rental property assessments in a landscape where Section 21 'no-fault' evictions no longer exist. The Renters' Rights Act 2026 Impact on Valuation Surveys: Adapting Rental Property Assessments Post-Section 21 Abolition represents a seismic shift from predictable fixed-term income streams to open-ended periodic tenancies with constrained rent growth mechanisms.

This legislative transformation demands immediate attention from chartered surveyors, property investors, and mortgage lenders who must now navigate valuation methodologies that account for increased income volatility, enhanced compliance costs, and fundamentally altered landlord-tenant power dynamics. The days of straightforward comparable evidence analysis are giving way to sophisticated income modeling that mirrors commercial property valuation complexity.

Key Takeaways

- Section 21 abolition replaces fixed-term ASTs with periodic (monthly rolling) tenancies, introducing income unpredictability that requires conservative valuation assumptions and potentially higher yields

- Rent increase restrictions limit growth to one annual adjustment after the first 12 months, with tribunal oversight creating cash-flow variability that traditional comparable methods may not capture

- Enhanced compliance requirements including Decent Homes Standards and deposit protection obligations add measurable costs that must be factored into property valuation assessments

- Vacant possession assumptions remain reasonable given Section 8 grounds still exist, though case-by-case assessment is now essential for accurate market value determination

- Mixed-use properties face amplified valuation risk due to reduced tenant tolerance for disturbances combined with periodic tenancy structures that increase void period likelihood

Understanding the Renters' Rights Act 2026 Legislative Framework

The Renters' Rights Act 2026 represents the most comprehensive overhaul of England's private rental sector since the Housing Act 1988 introduced Assured Shorthold Tenancies. Understanding its core provisions is essential for property professionals conducting property condition assessments and valuations in the current market.

Core Legislative Changes Affecting Valuations

The Act's primary transformation centers on abolishing Section 21 'no-fault' evictions entirely [2]. This mechanism previously allowed landlords to regain possession of their property without providing a reason, typically with two months' notice after a fixed-term tenancy expired. While Section 8 grounds for repossession remain available—covering scenarios like rent arrears, property damage, or landlord's intention to sell—these require specific justification and tribunal approval, potentially extending possession timelines significantly [2].

Fixed-term Assured Shorthold Tenancies are replaced with open-ended periodic tenancies that operate on monthly rolling terms with no minimum commitment period [3]. This structural change eliminates the predictable income horizon that valuers previously relied upon when assessing rental investment properties. Where landlords once secured six or twelve-month income certainty, they now face theoretical monthly termination risk from tenants, though in practice, notice periods still apply.

Rent Review Constraints and Market Value Determination

The Act introduces strict rent increase limitations that fundamentally alter income growth projections [2]:

- No rent increases permitted during the first 12 months of any tenancy

- Only one annual increase allowed thereafter

- Market value determination required, with increases subject to challenge at tribunal

- Tribunal oversight of disputed rent adjustments, introducing third-party decision-making into what was previously a bilateral landlord-tenant negotiation

These constraints force valuers to adopt more conservative assumptions about future income growth [1]. Investors are already reflecting higher perceived income risk through the yields they demand, with early market evidence suggesting yield expansion in certain rental property segments as capital values adjust to reduced income certainty.

Enhanced Tenant Rights and Dispute Mechanisms

The legislation strengthens tenant protections through less adversarial dispute resolution mechanisms via property tribunals [1]. This shift means rent-setting may not be purely market-determined in practice, with tribunal precedents potentially establishing rental value benchmarks that differ from open market transactions. For valuers, this introduces an additional layer of complexity: understanding not just market comparables but also tribunal decision patterns that could influence achievable rents.

The Act also mandates enhanced landlord obligations including:

✅ Decent Homes Standard compliance across all rental properties

✅ Deposit Protection scheme adherence with stricter enforcement

✅ Awaab's Law provisions requiring prompt resolution of health hazards

✅ Electrical safety certification and regular inspection requirements

These compliance costs must now be explicitly factored into valuation assessments, as they represent ongoing operational expenses that affect net rental yields and investment viability.

Renters' Rights Act 2026 Impact on Valuation Surveys: Methodological Adjustments Required

The Renters' Rights Act 2026 Impact on Valuation Surveys: Adapting Rental Property Assessments Post-Section 21 Abolition necessitates fundamental changes to how chartered surveyors approach rental property valuations. Traditional methodologies developed under the AST framework require significant adaptation to reflect the new legislative reality.

Income Approach Modifications and Conservative Projections

The shift from fixed-term to periodic tenancies introduces volatility similar to commercial property valuation [3], where income streams are less predictable and require more sophisticated modeling. Valuers must now:

Adopt conservative income growth assumptions that reflect the one-annual-increase limitation and potential tribunal intervention. Where previous valuations might have assumed 2-3% annual rental growth aligned with inflation indices, current assessments should consider scenarios where rent increases are successfully challenged or delayed through tribunal processes [1].

Model cash-flow variability explicitly rather than assuming stable income streams. This includes quantifying the financial impact of:

- Extended void periods due to tenant-friendly termination provisions

- Potential rent reductions ordered by tribunals

- Increased management costs associated with compliance verification

- Legal expenses related to Section 8 possession proceedings

Adjust capitalization rates (yields) to reflect increased risk perception. Early market evidence suggests investors are demanding higher yields to compensate for reduced income certainty [1], with some segments experiencing 25-50 basis point yield expansion compared to pre-Act comparable transactions.

Comparable Evidence Challenges and Alternative Approaches

Historic sales and yield benchmarks collected under the old AST system may no longer provide direct comparisons [3]. Properties sold in 2024-2025 with fixed-term tenancies in place cannot be directly compared to 2026 sales subject to periodic tenancy structures without appropriate adjustments.

This reliability gap in comparable evidence forces valuers to:

Place greater emphasis on income modeling rather than traditional direct comparison methods [3]. The valuation process increasingly resembles commercial property assessment, where discounted cash flow analysis and explicit yield risk adjustments take precedence over simple comparable analysis.

Develop adjustment factors for pre-Act comparable transactions. When using sales evidence from before May 2026, valuers must apply explicit adjustments accounting for:

| Adjustment Factor | Typical Range | Rationale |

|---|---|---|

| Income stability premium | -3% to -7% | Reflects loss of fixed-term income certainty |

| Possession risk discount | -2% to -5% | Accounts for extended Section 8 timelines vs. former Section 21 |

| Compliance cost allowance | -1% to -3% | Represents enhanced regulatory obligations |

| Rent review constraint | -2% to -4% | Reflects limited growth potential vs. previous flexibility |

These adjustments are market-dependent and require careful calibration based on property type, location, and tenant demographics. Properties in high-demand areas with strong rental markets may experience minimal adjustment, while marginal rental investments could see significant value impacts.

Seek post-Act comparable evidence wherever possible, recognizing that the most reliable valuation benchmarks will come from transactions completed after May 1, 2026, where both parties understood and priced in the new legislative framework.

Vacant Possession Assumption: Still Valid but Context-Dependent

RICS guidance currently maintains that vacant possession assumption remains reasonable given Section 8 possession grounds still exist [2]. However, this assumption requires more careful case-by-case assessment than previously necessary.

Valuers should consider:

Property-specific factors that might affect possession likelihood under Section 8 grounds. Properties with well-maintained condition, clear documentation, and professional management are more likely to successfully navigate Section 8 proceedings if required, supporting vacant possession assumptions.

Tenant profile considerations where known. Long-term tenants with excellent payment history represent lower possession risk than properties with frequent turnover or arrears history, though this information may not always be available for vacant possession valuations.

Alternative valuation scenarios for investment valuations where tenanted status is relevant. Providing both vacant possession and investment value assessments offers clients comprehensive understanding of the property's value in different contexts, particularly important given the changed tenancy landscape.

For stock condition surveys and portfolio valuations, this nuanced approach to vacant possession assumptions becomes especially critical, as bulk assessments must account for varying possession risk across different property types and conditions.

Adapting Rental Property Assessments: Practical Implementation Strategies

Property professionals conducting valuations in 2026 must implement concrete strategies that address the Renters' Rights Act 2026 Impact on Valuation Surveys: Adapting Rental Property Assessments Post-Section 21 Abolition while maintaining RICS compliance and providing clients with reliable market value opinions.

Enhanced Due Diligence and Compliance Verification

Valuation surveys now require expanded due diligence beyond traditional structural and condition assessment [2]. Chartered surveyors must verify and account for:

Decent Homes Standard compliance status, which affects both immediate value and future capital expenditure requirements. Properties failing to meet these standards face mandatory upgrade costs that must be reflected in valuation adjustments. This is particularly relevant when conducting property maintenance requirements assessments as part of comprehensive surveys.

Deposit Protection scheme compliance verification for tenanted properties. Non-compliance creates legal liability that affects investment value and may indicate broader management deficiencies requiring further investigation.

Electrical and gas safety certification currency and compliance history. Properties with lapsed certifications or recurring safety issues present both immediate rectification costs and potential income disruption risk if tenants exercise enhanced rights to withhold rent for unresolved hazards.

Historical tribunal interactions where discoverable. Properties with previous rent dispute tribunal cases or possession proceedings may indicate higher ongoing management risk that warrants yield adjustment or specific value qualification.

This enhanced due diligence extends survey timelines and costs but provides essential information for accurate valuation in the post-Act environment. Clients commissioning property surveys should anticipate these expanded scope requirements when budgeting for rental property assessments.

Mixed-Use and HMO Properties: Amplified Valuation Complexity

Properties with mixed-use characteristics face amplified risk under the new framework [3]. Flats above commercial units, for example, experience combined challenges of:

- Periodic tenancies allowing easier tenant exit if commercial disturbances occur

- Reduced tenant tolerance for noise, access disruptions, or operational inconvenience

- Potentially higher void periods as tenant pool narrows to those accepting mixed-use trade-offs

- Yield expansion reflecting these compounded risks

Valuers assessing mixed-use properties should:

Apply additional risk premiums beyond single-use residential adjustments, typically 50-100 basis points higher yields than comparable single-use properties in the same location.

Model extended void assumptions reflecting reduced tenant pool and easier exit mechanisms. Where single-use properties might assume 4-6 week void periods, mixed-use assessments should consider 8-12 week assumptions or longer depending on specific commercial use compatibility.

Consider use-specific factors carefully. A flat above a quiet professional office presents different risk than one above a late-night restaurant or early-morning bakery, with valuations adjusted accordingly.

Houses in Multiple Occupation (HMOs) face similar amplified complexity, as periodic tenancies for individual rooms create compounded income volatility across multiple tenant relationships simultaneously. HMO valuations require particularly sophisticated income modeling that accounts for rolling turnover patterns and the statistical likelihood of concurrent vacancies affecting overall property yield.

Landlord Adaptation Strategies Affecting Market Value

Landlords are already implementing adaptation strategies that valuers must recognize and incorporate [1]:

Higher initial rents at tenancy commencement to offset constrained future growth. This front-loading strategy affects comparable rent analysis, as current market rents may be inflated relative to historic patterns, requiring adjustment when projecting sustainable income streams.

Negotiated stepped increases or fixed escalation clauses agreed at tenancy start. Where landlords successfully negotiate predetermined annual increases (subject to market value limits), these properties present lower income uncertainty and may warrant yield compression relative to properties relying on annual negotiation.

Selective tenant screening intensification to minimize possession risk. Properties with enhanced tenant verification processes may experience lower turnover and arrears risk, supporting more optimistic income projections, though this factor is difficult to quantify objectively in valuation.

Professional management adoption by previously self-managing landlords. The increased complexity of compliance and dispute management is driving professionalization of the sector, with associated management costs (typically 10-15% of gross rent) that must be reflected in net income calculations for investment valuations.

Understanding these market adaptations helps valuers distinguish between temporary market disruption and permanent structural changes that warrant lasting valuation methodology adjustments.

Reporting and Disclosure Requirements

Valuation reports prepared under the new legislative framework should include explicit disclosure of:

✍️ Assumptions regarding tenancy structure and income stability

✍️ Adjustments applied to pre-Act comparable evidence

✍️ Compliance status of subject property and its impact on value

✍️ Yield selection rationale with explicit risk factor consideration

✍️ Limitations of available comparable evidence in transitional market

This enhanced disclosure protects both valuer and client by ensuring transparent communication about the uncertainties inherent in valuing rental property during this significant legislative transition. For property rights considerations and legal framework understanding, clear documentation of assumptions becomes essential risk management.

Technology and Data Analytics Integration

Forward-thinking valuation practices are leveraging technology solutions to address the increased complexity:

Tribunal decision databases tracking rent determination outcomes to inform market rent assessments and identify patterns that might affect specific property types or locations.

Enhanced income modeling software capable of scenario analysis, Monte Carlo simulation, and sensitivity testing to quantify the range of potential value outcomes under different income assumptions.

Compliance tracking systems integrated with valuation workflows to ensure systematic verification of regulatory requirements across portfolio assessments.

Market intelligence platforms providing real-time rental market data segmented by post-Act transaction status, enabling more reliable comparable identification and analysis.

These technological tools don't replace professional judgment but provide data-driven support for the more complex analytical requirements the Act imposes on valuation practice.

Sector-Specific Considerations and Portfolio Implications

Different property sectors and portfolio types experience varying degrees of impact from the Renters' Rights Act 2026 Impact on Valuation Surveys: Adapting Rental Property Assessments Post-Section 21 Abolition, requiring tailored assessment approaches.

Build-to-Rent Developments and Institutional Investment

Institutional build-to-rent portfolios with professional management infrastructure may experience relatively modest valuation impact compared to smaller private landlords. These assets typically already operated with:

- Sophisticated tenant management systems

- Comprehensive compliance frameworks

- Professional dispute resolution processes

- Diversified income streams across large unit counts

However, even institutional portfolios face yield pressure from the fundamental shift to periodic tenancies and constrained rent growth. Valuers assessing BTR assets should focus on:

📊 Portfolio-level income volatility modeling rather than individual unit analysis

📊 Management cost efficiency as competitive advantage affecting net yields

📊 Tenant retention metrics as key value driver in periodic tenancy environment

📊 Compliance infrastructure as value-protective asset requiring capital allocation

Student Accommodation and Specialist Housing

Student housing presents unique considerations, as the academic calendar creates natural fixed-term occupancy patterns that partially mitigate periodic tenancy risks. However, the Act's provisions still apply, requiring:

- Careful structuring of tenancy agreements to align with academic terms while respecting periodic tenancy requirements

- Enhanced compliance given vulnerable tenant population

- Tribunal risk management given student tenants' increased awareness of rights

Specialist housing including senior living, co-living, and serviced accommodation may fall under different regulatory frameworks depending on specific service provision, requiring careful legal analysis to determine Act applicability and appropriate valuation methodology.

Geographic Variation and Local Market Dynamics

The Act's impact varies significantly by location and local market conditions:

High-demand urban markets with strong rental fundamentals (London, Manchester, Birmingham) may experience minimal value impact as tenant demand supports landlord negotiating position despite legislative changes.

Marginal rental markets with weaker fundamentals face greater risk, as periodic tenancies combined with constrained rent growth may push yields to levels where investment becomes economically unviable, potentially triggering portfolio disposals and market contraction.

Regional yield spreads are likely to widen as investors differentiate between locations based on perceived income security and growth potential under the new framework. Valuers must maintain granular local market intelligence to accurately assess these geographic variations.

Portfolio Valuation and Risk Assessment

For portfolio valuations encompassing multiple properties, the Act introduces both challenges and opportunities:

Diversification benefits become more valuable as periodic tenancy income volatility at individual property level is partially offset through portfolio aggregation, potentially supporting yield compression for large portfolios relative to single-asset investments.

Risk stratification within portfolios becomes essential, with properties categorized by:

- Compliance status and upgrade requirements

- Tenant profile and retention likelihood

- Location and local market strength

- Physical condition and maintenance obligations

This stratification enables risk-adjusted valuation where high-quality, compliant properties in strong markets receive favorable yield treatment while problematic assets face appropriate discounting.

Portfolio optimization strategies may emerge from valuation analysis, identifying properties where disposal is economically rational given the changed risk-return profile under the Act, while other assets warrant retention or additional investment to enhance compliance and value protection.

Future Outlook and Market Evolution

The rental property valuation landscape will continue evolving as the market adapts to the Renters' Rights Act 2026 Impact on Valuation Surveys: Adapting Rental Property Assessments Post-Section 21 Abolition and participants gain experience with the new framework.

Market Adjustment Timeline and Valuation Convergence

2026-2027 represents a transitional period where valuation uncertainty remains elevated due to:

- Limited post-Act comparable transaction evidence

- Uncertainty about tribunal decision patterns and precedents

- Landlord and tenant behavior adaptation still in progress

- Potential secondary legislation or guidance clarifications

2028 onwards should see greater valuation stability as:

- Sufficient post-Act transaction evidence accumulates

- Tribunal precedents establish clearer rent determination patterns

- Market participants fully internalize new risk-return dynamics

- Valuation methodologies standardize around best practices

Valuers operating during the transitional period must maintain flexibility and transparency, clearly communicating the elevated uncertainty inherent in current assessments while providing best professional judgment based on available evidence.

Regulatory Evolution and RICS Guidance Updates

RICS continues monitoring market developments and will likely issue updated guidance as practical experience accumulates [2]. Valuers should anticipate:

- Refined position on vacant possession assumptions based on Section 8 possession timeline data

- Standardized adjustment factors for pre-Act comparable evidence

- Clarification on income modeling best practices for periodic tenancies

- Portfolio valuation guidance addressing diversification and risk aggregation

Staying current with evolving professional guidance is essential for maintaining RICS compliance and providing clients with valuations that reflect current best practice standards.

Technology and Data Infrastructure Development

The increased complexity of rental property valuation creates opportunities for enhanced data infrastructure:

Tribunal decision databases becoming standard reference tools for valuers, similar to how property price indices and yield databases currently inform valuation practice.

Predictive analytics leveraging machine learning to model income volatility and possession risk based on property characteristics, tenant demographics, and local market conditions.

Integrated compliance platforms linking property condition data with regulatory requirements to automatically flag value-affecting compliance gaps during survey processes.

These technological developments will gradually reduce the analytical burden the Act currently imposes while improving valuation accuracy and consistency across the profession.

Investment Market Implications

The Act is likely to accelerate existing trends toward institutional investment and portfolio consolidation in the rental sector, as professional operators with sophisticated compliance and management infrastructure gain competitive advantage over smaller private landlords.

This market evolution affects valuation practice through:

- Increasing prevalence of portfolio valuations over single-asset assessments

- Growing importance of operational efficiency and management quality as value drivers

- Potential emergence of rental property securitization requiring specialized valuation approaches

- Greater integration between property valuation and operational due diligence

Valuers developing expertise in these evolving areas will be well-positioned to serve the changing market structure the Act is helping to catalyze.

Conclusion

The Renters' Rights Act 2026 Impact on Valuation Surveys: Adapting Rental Property Assessments Post-Section 21 Abolition represents a fundamental transformation in rental property valuation methodology. The abolition of Section 21 no-fault evictions, replacement of fixed-term ASTs with periodic tenancies, and introduction of strict rent review constraints have eliminated the income predictability that underpinned traditional valuation approaches.

Chartered surveyors must now adopt more sophisticated income modeling techniques that explicitly account for cash-flow variability, apply conservative growth assumptions reflecting regulatory constraints, and adjust yields to reflect increased investor risk perception. Enhanced due diligence covering compliance status, maintenance obligations, and regulatory adherence has become essential to accurate valuation, while comparable evidence from the pre-Act period requires careful adjustment before application to current assessments.

The transitional period through 2027 will present ongoing challenges as limited post-Act transaction evidence and evolving tribunal precedents create valuation uncertainty. However, professionals who embrace these methodological adaptations, maintain transparent communication about assumptions and limitations, and leverage emerging data and technology tools will successfully navigate this new landscape.

Actionable Next Steps

For property valuers conducting rental property assessments:

✅ Review and update valuation templates to include enhanced due diligence requirements and compliance verification

✅ Develop adjustment frameworks for pre-Act comparable evidence with documented rationale

✅ Invest in income modeling capabilities that can handle scenario analysis and volatility quantification

✅ Establish tribunal decision tracking to inform rent determination assumptions

✅ Enhance client communication protocols to ensure transparent disclosure of Act-related uncertainties

For property investors and landlords commissioning valuations:

✅ Request explicit disclosure of how the Act's provisions affect valuation assumptions and conclusions

✅ Consider scenario analysis showing value sensitivity to different income and yield assumptions

✅ Evaluate compliance status of existing portfolios and budget for necessary upgrades

✅ Review management infrastructure to ensure capability for enhanced regulatory environment

✅ Seek specialist advice for complex assets including mixed-use properties and HMOs

For mortgage lenders relying on valuation reports:

✅ Update lending criteria to reflect changed risk profile of rental property security

✅ Review valuer panel qualifications to ensure Act-related expertise and methodology adaptation

✅ Consider enhanced reporting requirements for rental property valuations

✅ Monitor portfolio exposure to properties with elevated compliance or possession risk

The rental property market will adapt to this new legislative framework, and valuation practice will evolve accordingly. By proactively implementing these methodological adjustments and maintaining professional standards throughout the transitional period, the surveying profession will continue providing the reliable market value opinions that clients, lenders, and the broader property market depend upon.

For comprehensive property assessments that account for these legislative changes, consider professional property valuation services from qualified chartered surveyors experienced in post-Act rental property analysis.

References

[1] New Rules New Risks The Renters Rights Act Effect – https://www.shw.co.uk/articles/2025/new-rules-new-risks-the-renters-rights-act-effect.html

[2] Consideration Of Implications Of Renters Rights Act On Valuation – https://www.rics.org/news-insights/consideration-of-implications-of-renters-rights-act-on-valuation

[3] Renters Rights Bill Future Of Valuations – https://www.terracottaproperty.com/blog/renters-rights-bill-future-of-valuations