The property market in 2026 stands at a pivotal moment. After years of volatility, mortgage rates are finally stabilizing at levels lower than 2025, creating a ripple effect across the entire real estate ecosystem. For chartered surveyors, this shift demands a fundamental recalibration of how properties are assessed and valued. Mortgage Rate Sensitivity in Valuation: How Surveyors Adjust Property Assessments as Rates Stabilize in 2026 has become a critical consideration for professionals who must balance buyer purchasing power, lender confidence, and market recovery dynamics to deliver accurate property assessments.

The relationship between mortgage rates and property values isn't just theoretical—it's a daily reality that impacts every homebuyer, seller, and investor in the market. As rates ease and stabilize, professional surveyors face the challenge of adjusting their valuation models to reflect this new landscape accurately.

Key Takeaways

- 📊 Rate stabilization in 2026 has increased buyer purchasing power by 15-20% compared to 2025 peak rates, requiring surveyors to adjust comparable sales analysis accordingly

- 💷 Valuation methodologies now incorporate rate sensitivity adjustments that account for improved affordability and lender confidence in the recovering market

- 🏠 Property assessments must balance historical data from high-rate periods with current market conditions to provide accurate valuations for mortgage lending

- 📈 Chartered surveyors are implementing new comparative analysis techniques that weight recent transactions more heavily in stabilized rate environments

- ⚖️ Accuracy in valuations directly impacts mortgage approval rates, buyer negotiations, and overall market health as the property sector recovers

Understanding Mortgage Rate Sensitivity in Property Valuation

What Is Mortgage Rate Sensitivity?

Mortgage rate sensitivity refers to how changes in borrowing costs affect property values and buyer behavior. When rates rise, monthly payments increase, reducing the amount buyers can afford to borrow. Conversely, when rates fall or stabilize at lower levels, purchasing power expands, potentially driving property values upward.

In 2026, this sensitivity has become particularly pronounced. After experiencing rates above 6% in 2025, the current stabilization around 4.5-5% has fundamentally altered the valuation landscape. Chartered surveyors must now account for:

- Enhanced affordability metrics 💰

- Improved buyer confidence levels

- Increased lender willingness to approve mortgages

- Shifting market dynamics as previously stalled transactions resume

The Direct Impact on Property Values

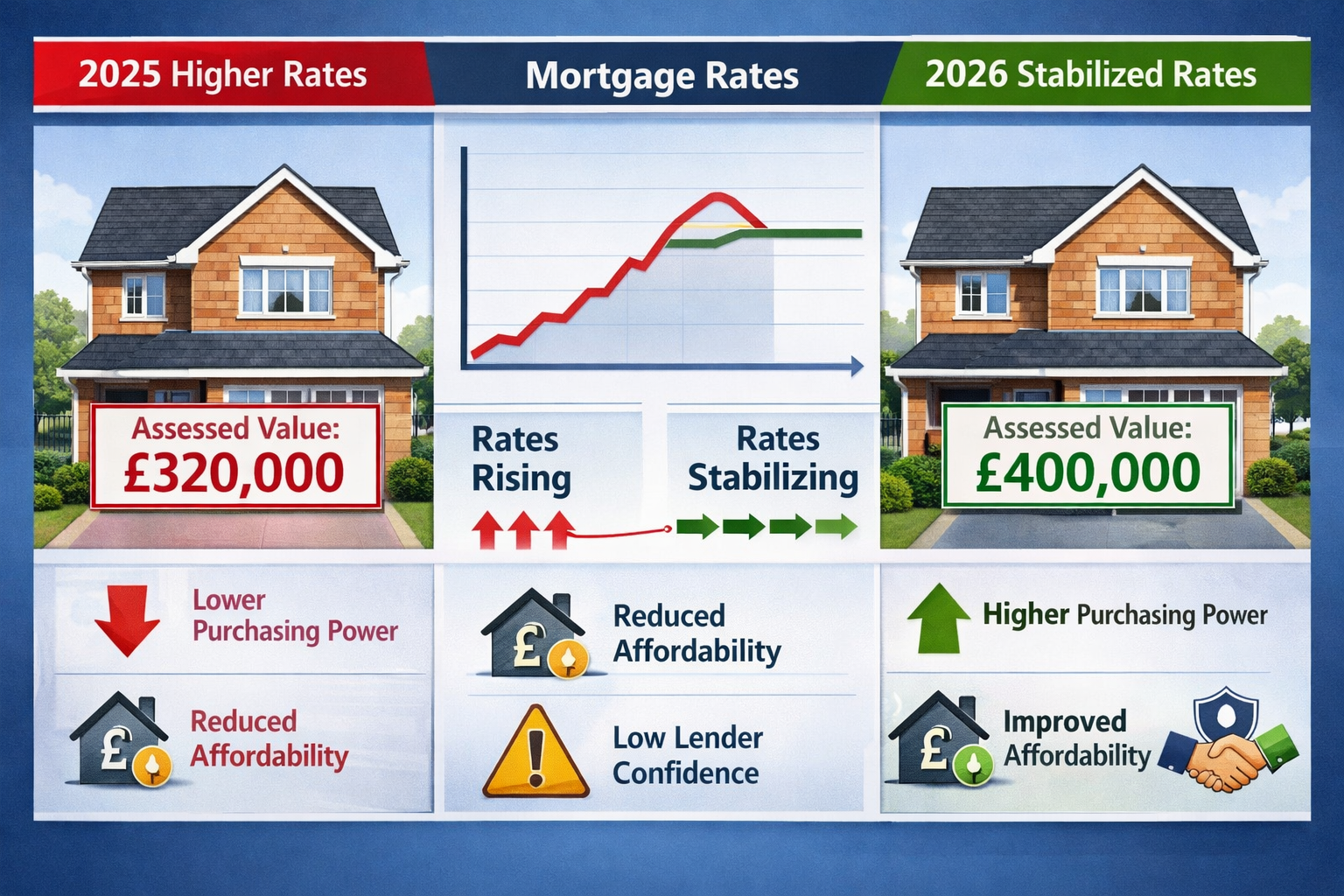

The mathematics of mortgage rate sensitivity are straightforward but powerful. A 1% decrease in mortgage rates can increase a buyer's purchasing power by approximately 10-12%. For a typical property, this translates into significant valuation adjustments.

Consider this comparison:

| Rate Environment | Monthly Payment (£300k mortgage) | Effective Buying Power |

|---|---|---|

| 2025 Peak (6.5%) | £1,896 | £300,000 |

| 2026 Stable (5.0%) | £1,610 | £335,000 |

| Difference | -£286/month | +£35,000 (+11.7%) |

This table illustrates why surveyors cannot simply rely on 2025 comparable sales without adjustment. The same property that struggled to achieve £300,000 in late 2025 may now reasonably command £335,000 in the stabilized 2026 market.

How Chartered Surveyors Adjust Valuation Methodologies for Rate Changes

Recalibrating Comparable Sales Analysis

The cornerstone of property valuation—comparable sales analysis—requires significant adjustment in periods of rate transition. RICS surveyors in 2026 are implementing several key modifications:

Time-Weighted Adjustments

Recent sales carry more weight than historical transactions. Surveyors now apply time-decay factors that reduce the relevance of sales completed during high-rate periods. A property sold six months ago at peak rates may require a 5-10% upward adjustment to reflect current market conditions.

Rate Environment Normalization

Professional valuers are developing rate environment indices that normalize historical sales data. This involves:

- Identifying the prevailing mortgage rate at the time of each comparable sale

- Calculating the affordability differential between that rate and current rates

- Applying proportional adjustments to the sale price

- Weighting adjusted comparables based on similarity to the subject property

Market Velocity Considerations

The speed at which properties sell provides crucial context. In stabilized rate environments, days on market typically decrease, indicating stronger demand. Surveyors factor this velocity into their assessments, recognizing that faster-selling properties in 2026 reflect genuine market value rather than distressed pricing.

Incorporating Buyer Purchasing Power Models

Modern valuation now extends beyond simple price-per-square-foot calculations. London property surveyors are integrating affordability modeling directly into their assessment frameworks.

This approach involves:

- Income-to-mortgage calculations based on current lending rates

- Debt-to-income ratio analysis reflecting 2026 lender criteria

- Deposit requirement adjustments as loan-to-value ratios improve

- Stress testing against potential future rate movements

By understanding what buyers can actually afford at prevailing rates, surveyors provide more accurate valuations that align with real-world transaction capabilities.

Adjusting Investment Property Valuations

For investment properties, rate sensitivity operates through a different mechanism—the yield compression effect. As mortgage rates stabilize at lower levels:

- Net yields become more attractive relative to borrowing costs

- Investor demand increases, driving capital values upward

- Rental yield expectations may adjust as capital appreciation prospects improve

Surveyors valuing investment properties in 2026 must recalibrate their capitalization rates and yield assumptions to reflect this changed landscape. A property that required an 8% gross yield in 2025 may now be marketable at 7% due to improved financing conditions.

The Role of Lender Confidence in 2026 Valuation Adjustments

Understanding Lender Risk Appetite

Lender confidence is perhaps the most underappreciated factor in property valuation. When rates stabilize, financial institutions become more willing to lend, often at higher loan-to-value ratios. This increased lending capacity directly impacts property values.

In 2026, surveyors observe several indicators of improved lender confidence:

- 📋 Reduced documentation requirements for standard mortgage applications

- 💵 Higher LTV offerings (now commonly 90-95% for first-time buyers)

- ⚡ Faster approval processes reducing transaction uncertainty

- 🎯 Expanded lending criteria including self-employed and non-traditional income sources

These factors create a more liquid market where properties can achieve their full value potential, rather than being constrained by financing limitations.

Valuation Conservatism vs. Market Reality

Professional surveyors face a delicate balance. While recognizing improved market conditions, they must avoid over-optimistic valuations that could expose lenders to risk if rates rise again.

The solution lies in scenario-based valuation approaches:

- Base case valuation: Assumes rate stability continues through 2026-2027

- Stress test valuation: Models a 1-2% rate increase scenario

- Recovery premium: Accounts for pent-up demand from the 2025 slowdown

This multi-scenario framework, increasingly standard among chartered surveyors, provides lenders with both an accurate current valuation and an understanding of downside risk.

Regional Variations in Rate Sensitivity

Not all markets respond identically to rate changes. Surveyors in 2026 must account for geographic sensitivity differentials:

High-sensitivity markets (typically first-time buyer dominated):

- Greater London suburbs

- Commuter belt areas like Brentwood and Epping

- Properties in the £250,000-£450,000 range

Moderate-sensitivity markets:

- Established family neighborhoods in Wandsworth and Ealing

- Mid-market properties with diverse buyer profiles

- Areas with strong rental demand

Lower-sensitivity markets:

- Prime central London locations

- High-value properties above £1 million

- Cash-buyer dominated segments

Understanding these variations allows surveyors to apply appropriate adjustment factors based on the specific property's market segment.

Practical Valuation Techniques for the 2026 Market

The Enhanced Comparable Method

The traditional comparable sales method receives several enhancements in the stabilized rate environment:

Step 1: Expanded Comparable Pool 🔍

Rather than limiting analysis to the past 3-6 months, surveyors now examine 12-18 months of data but apply rate adjustment factors to older sales.

Step 2: Affordability Indexing

Each comparable sale is indexed to a standard affordability baseline:

- Calculate monthly payment at the sale date rate

- Recalculate monthly payment at current rates

- Determine the value differential this represents

- Apply adjustment to the sale price

Step 3: Market Momentum Weighting

Recent sales in improving markets receive momentum premiums of 2-5%, recognizing that buyer sentiment and competition are strengthening.

The Income Approach for Rate-Sensitive Markets

For properties in areas where buyers are heavily mortgage-dependent, the income approach provides valuable validation:

- Determine median household income for the target buyer demographic

- Calculate maximum affordable mortgage at current rates (typically 4.5x income)

- Add typical deposit (10-20% depending on buyer type)

- Derive implied property value from affordability ceiling

This approach is particularly valuable when negotiating property prices, as it grounds valuations in financial reality rather than aspirational pricing.

Technology-Assisted Valuation Models

2026 has seen widespread adoption of algorithmic valuation models (AVMs) that incorporate rate sensitivity automatically. However, professional surveyors provide essential oversight:

✅ Validating AVM outputs against local market knowledge

✅ Adjusting for property-specific factors algorithms may miss

✅ Interpreting rate sensitivity assumptions embedded in models

✅ Providing professional judgment on unique circumstances

The combination of technology and professional expertise delivers the most reliable valuations in the current market.

Challenges and Considerations for Surveyors in 2026

Data Quality and Historical Comparability

One significant challenge facing surveyors is the data contamination effect from the 2025 high-rate period. Sales completed under financial stress may not represent true market value, yet they appear in comparable databases.

Professional surveyors address this by:

- Flagging distressed sales and excluding them from standard analysis

- Identifying motivated seller transactions that may undervalue properties

- Weighting recent stabilized-market sales more heavily

- Consulting multiple data sources to identify anomalies

Client Education and Expectation Management

Property owners often struggle to understand why valuations may differ significantly from 2025 assessments. Surveyors must clearly communicate:

- 📈 The mathematical relationship between rates and affordability

- 🔄 How market conditions have fundamentally changed

- 💡 Why higher valuations are now justified by improved buyer capacity

- ⚖️ The balance between optimism and prudent assessment

This educational role is crucial for maintaining professional credibility and ensuring clients make informed decisions.

Regulatory and Professional Standards

The Royal Institution of Chartered Surveyors (RICS) continues to update guidance for rate-sensitive valuation environments. In 2026, key requirements include:

- Explicit disclosure of rate assumptions in valuation reports

- Scenario analysis for properties above certain value thresholds

- Market condition commentary explaining rate environment impacts

- Professional indemnity considerations for rapidly changing markets

Surveyors must stay current with these evolving standards while applying practical judgment to individual properties. Resources like what surveyors do help clients understand this professional responsibility.

The Forward-Looking Challenge

Perhaps the greatest challenge is predicting future rate movements. While 2026 rates have stabilized, surveyors must consider:

- Will rates continue declining? 📉

- Could economic shocks trigger rate increases? 📊

- How long will the current stability last? ⏱️

- What's the appropriate time horizon for valuation assumptions? 🔮

Professional surveyors address this uncertainty through conservative baseline assumptions and clear documentation of the rate environment context for each valuation.

Strategic Implications for Property Stakeholders

For Homebuyers

Understanding mortgage rate sensitivity in valuation empowers buyers to:

- Time purchases strategically when rate-driven value adjustments are favorable

- Negotiate effectively using professional valuation data

- Secure appropriate financing based on realistic property values

- Avoid overpaying in markets where rate impacts are misunderstood

Obtaining a professional RICS survey provides independent valuation confirmation that accounts for current rate conditions.

For Property Sellers

Sellers benefit from understanding that:

- 2026 valuations may exceed 2025 assessments due to improved buyer affordability

- Professional valuation supports asking price justification

- Rate stability creates a more favorable selling environment

- Timing matters: selling while rates remain stable maximizes value realization

For Lenders and Investors

Financial institutions and property investors must recognize:

- Valuation accuracy depends on proper rate sensitivity adjustments

- Risk assessment requires understanding rate volatility impacts

- Portfolio valuation may need systematic recalibration for 2026 conditions

- Due diligence should verify surveyor methodology for rate adjustments

For Property Professionals

Estate agents, mortgage brokers, and other property professionals should:

- Partner with qualified surveyors who understand rate sensitivity

- Educate clients about valuation dynamics in changing rate environments

- Adjust marketing strategies to reflect improved affordability

- Monitor rate trends as a leading indicator of value movements

Conclusion

Mortgage Rate Sensitivity in Valuation: How Surveyors Adjust Property Assessments as Rates Stabilize in 2026 represents more than a technical adjustment—it's a fundamental recalibration of how property value is understood and measured. As mortgage rates stabilize at levels significantly below 2025 peaks, chartered surveyors play a critical role in translating improved affordability and lender confidence into accurate property assessments.

The professional surveyor's toolkit has expanded considerably, incorporating time-weighted comparable analysis, affordability modeling, scenario-based valuations, and technology-assisted approaches. These methodologies ensure that property values reflect genuine market conditions rather than outdated assumptions from higher-rate periods.

For property stakeholders across the spectrum—buyers, sellers, lenders, and investors—understanding these valuation adjustments is essential. The stabilized rate environment of 2026 creates opportunities, but only for those who work with professionals capable of accurately assessing value in this evolved landscape.

Next Steps for Property Stakeholders

If you're buying property in 2026:

- Commission a professional property survey that explicitly addresses rate sensitivity in valuation

- Request scenario analysis showing value implications of potential rate changes

- Ensure your surveyor provides clear documentation of rate assumptions

If you're selling property:

- Obtain an up-to-date professional valuation that accounts for improved 2026 market conditions

- Use rate sensitivity analysis to justify asking prices to potential buyers

- Consider timing your sale while rate stability continues

If you're a property professional:

- Partner with local surveyors who demonstrate expertise in rate-sensitive valuation

- Continuously educate yourself on the relationship between rates and property values

- Communicate these dynamics clearly to clients to manage expectations effectively

The property market's recovery in 2026 is built on a foundation of stabilized mortgage rates and professional valuation practices that accurately reflect this new reality. By understanding and embracing mortgage rate sensitivity in valuation, all stakeholders can make more informed decisions and contribute to a healthier, more transparent property market.