The UK property market has emerged from its most significant correction in over a decade, and institutional investors are now recalibrating their buy-to-let strategies for 2026. With all property capital values recording 1.3% annual growth and total returns projected at an impressive 9-10% for the year ahead, professional landlords face a critical inflection point. Understanding Institutional Buy-to-Let Valuations in 2026 Recovery: Risk Assessment Protocols for Professional Landlords has become essential for navigating this transformed landscape while managing emerging regulatory requirements like Awaab's Law and shifting rental demand patterns.

The recovery that began in summer 2024 following a substantial 25% correction between mid-2022 and mid-2024 has created both opportunities and complexities. Transaction volumes reached £19 billion in Q4 2025—a 20% improvement year-on-year—yet liquidity remains constrained compared to historical averages[1]. For institutional investors, this environment demands sophisticated valuation methodologies that account for regulatory compliance costs, interest rate trajectories, and sector-specific performance variations.

Key Takeaways

- Property capital values grew 1.3% annually in December 2025, with residential sector posting +2.2% year-on-year growth and UK property total returns projected at 9-10% for 2026[1]

- Stamp Duty Land Tax increased to 5% for additional dwellings from April 2025, adding significant acquisition costs that must be factored into institutional valuation models

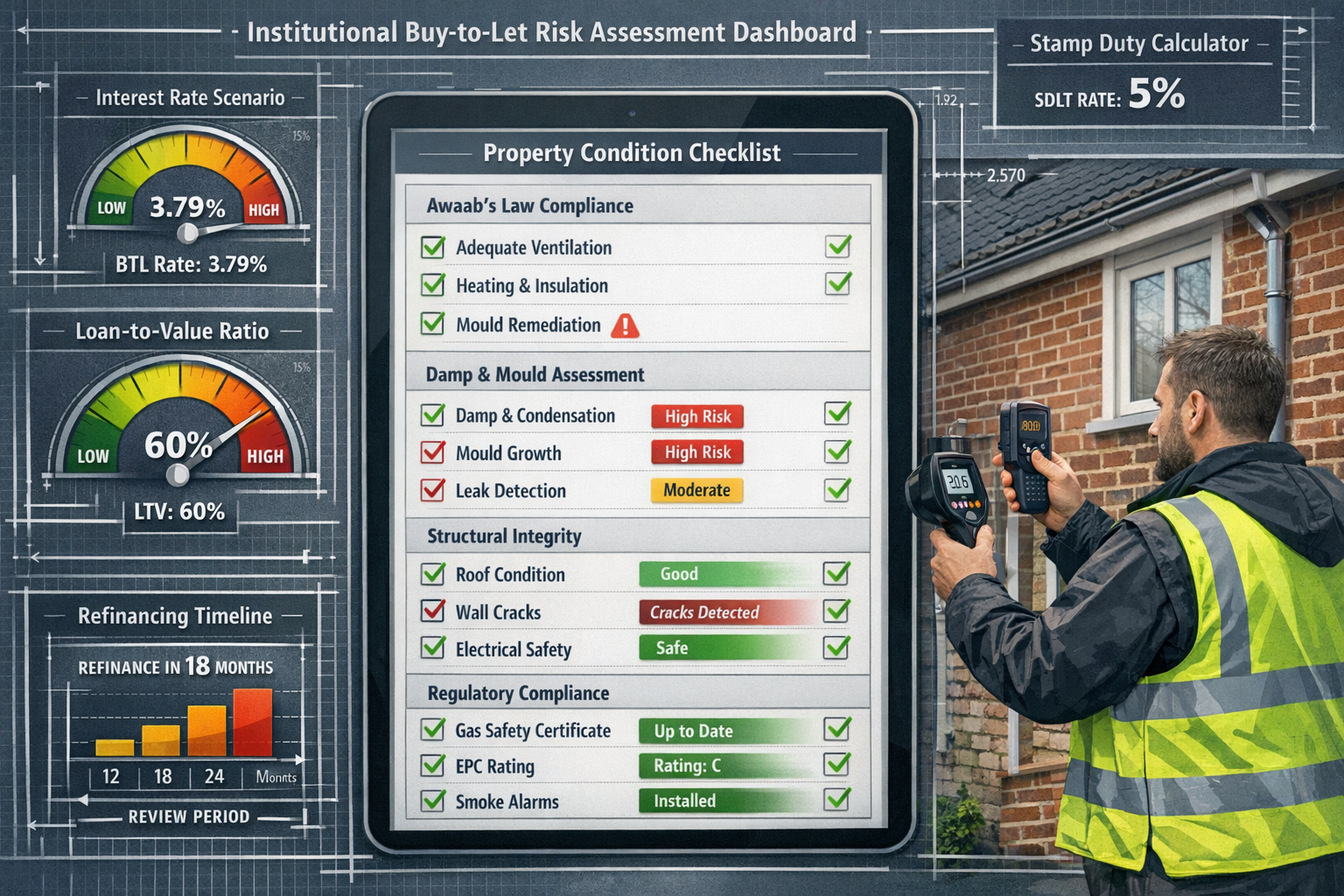

- Awaab's Law compliance requirements mandate comprehensive property condition assessments, particularly for damp and mould issues, fundamentally altering risk protocols for professional landlords

- BTL mortgage rates starting at 3.79% for two-year fixed products at 60% LTV create new refinancing opportunities, though gradual Bank of England rate cuts mean pricing won't decline proportionally[4]

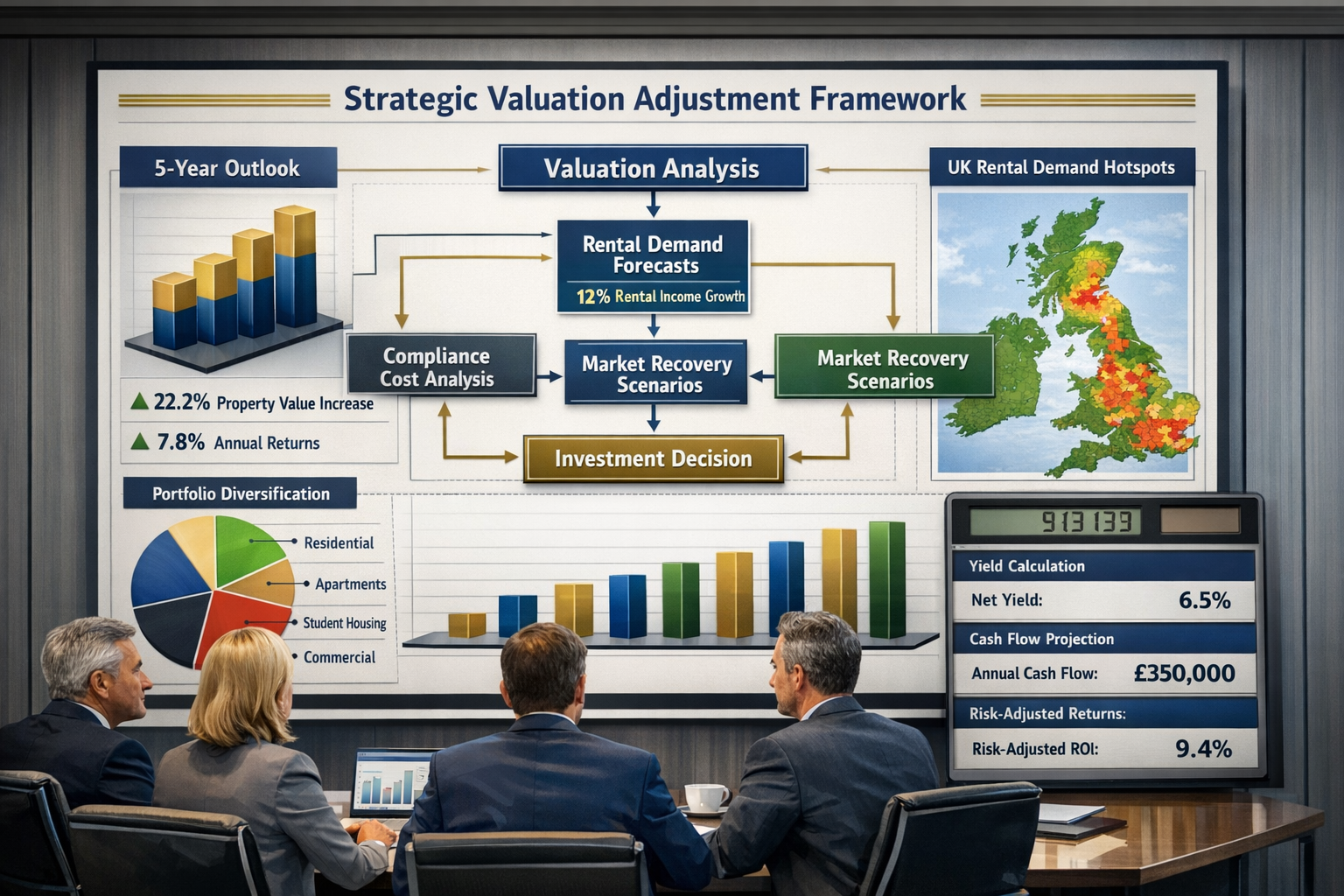

- 22.2% average property value increase forecast over five years with 12% rental income growth requires strategic portfolio positioning and enhanced due diligence protocols[3]

Understanding the 2026 Market Recovery Context

Capital Value Trends Across Property Sectors

The institutional buy-to-let market in 2026 operates within a broader property recovery characterized by significant sectoral divergence. While all property capital values recorded 1.3% annual growth in December 2025, the performance varies dramatically by asset class[1]. The industrial sector leads with robust +3.0% year-on-year growth, followed by residential at +2.2% and retail at +1.7%. However, office values continue their decline at -2.3%, highlighting the importance of sector selection in institutional portfolios.

For professional landlords focused on buy-to-let investments, the residential sector's +2.2% growth represents a substantial improvement from the correction period. This recovery is underpinned by persistent housing shortages, demographic demand from younger households unable to access homeownership, and improving investor sentiment as monetary policy stabilizes.

The projected 9-10% total returns for 2026 significantly exceed the prior 10-year average of 4.3% per annum[1]. This enhanced return environment creates compelling opportunities for institutional investors who can accurately assess property values while managing the regulatory and operational risks that have intensified since 2024.

Transaction Volume Recovery and Liquidity Considerations

Q4 2025 transaction volumes reaching £19 billion marked the strongest quarter since mid-2022, representing a 20% improvement on Q4 2024[1]. This recovery signals returning investor confidence and improved market liquidity. However, full-year 2025 volumes totaled £48 billion—approximately 15-20% below the 10-year average—indicating that liquidity constraints persist in historical context.

For institutional buy-to-let investors, this environment presents both challenges and advantages. Reduced competition from retail investors facing higher stamp duty costs and stricter mortgage criteria creates acquisition opportunities for well-capitalized professional landlords. However, exit strategies must account for continued liquidity constraints that may affect disposal timelines and pricing.

Savills upgraded its five-year outlook, predicting average annual total returns of 7.8% as rental growth strengthens and interest-rate pressures ease[2]. Commercial property investment is expected to rise by 10%, from £50 billion in 2025 to £55 billion in 2026, suggesting broader institutional capital allocation toward UK real estate.

Interest Rate Environment and Financing Considerations

The Bank of England base rate trajectory remains central to institutional buy-to-let valuations in 2026. While two base rate cuts appear plausible during the year, market analysts caution that reductions will be gradual, and a move back to 3% appears ambitious[5]. Critically for professional landlords, even if the base rate falls by 50 basis points, product pricing will not decline proportionally as lenders maintain risk premiums.

BTL mortgage rates starting at 3.79% for two-year fixed purchase products up to 60% loan-to-value with a £1,995 lender fee represent the current financing landscape[4]. These rates, while improved from 2023-2024 peaks, remain substantially higher than the sub-2% environment that prevailed before 2022. Institutional investors must therefore incorporate higher debt servicing costs into their property valuation models and stress-test portfolios against potential rate volatility.

Refinancing activity is increasing as landlords approach refinancing with greater strategic purpose. Some seek to reduce costs and stabilize portfolios, while others leverage lower rates and improved affordability to release equity for portfolio expansion[5]. This refinancing wave creates opportunities for institutional investors to optimize capital structures and improve portfolio yields.

Risk Assessment Protocols for Professional Landlords in 2026

Awaab's Law Compliance and Property Condition Assessment

Awaab's Law, which came into force in 2023 following the tragic death of two-year-old Awaab Ishak from prolonged mould exposure, has fundamentally transformed risk assessment requirements for institutional landlords. The legislation mandates strict timeframes for addressing hazards, particularly damp and mould issues, with landlords required to investigate reported health hazards within 14 days and commence remedial works within a further seven days for emergency hazards.

For institutional buy-to-let valuations in 2026, compliance with Awaab's Law represents both a regulatory obligation and a significant financial consideration. Professional landlords must conduct comprehensive property condition assessments that specifically evaluate:

- Damp and mould risk factors: Building envelope integrity, ventilation adequacy, condensation patterns, and historical moisture issues

- Structural elements affecting habitability: Roof condition, external wall insulation, window quality, and drainage systems

- Mechanical ventilation systems: Functionality and adequacy of extraction systems in bathrooms and kitchens

- Tenant reporting mechanisms: Systems to ensure rapid identification and response to emerging issues

Institutional investors must factor remediation costs into acquisition valuations, particularly for older housing stock where building fabric issues are more prevalent. A property damp assessment should be standard practice before portfolio additions, with remediation budgets allocated based on findings.

The reputational and regulatory risks of non-compliance cannot be overstated. Local authorities possess enforcement powers including unlimited fines for serious breaches, making robust compliance protocols essential for professional landlords managing substantial portfolios.

Financial Risk Assessment Framework

Institutional buy-to-let valuations in 2026 require sophisticated financial risk modeling that extends beyond traditional yield calculations. Professional landlords must implement comprehensive frameworks addressing:

Interest Rate Risk Management: With BTL mortgage rates at 3.79% for optimal products, institutional investors should stress-test portfolios against rate increases of 100-200 basis points. The gradual nature of anticipated base rate reductions means financing costs will remain elevated compared to pre-2022 levels. Portfolio models should incorporate:

- Refinancing schedules aligned with optimal rate environments

- Fixed versus variable rate allocation strategies

- Interest coverage ratio maintenance across different rate scenarios

- Cash reserve requirements for debt servicing during void periods

Stamp Duty Land Tax Impact: The increase to 5% SDLT for additional dwellings from April 2025 represents a substantial acquisition cost that directly affects investment returns[4]. For a £500,000 property, this translates to £25,000 in stamp duty compared to £15,000 under the previous 3% rate—a £10,000 increase that must be recovered through rental income or capital appreciation.

Institutional investors should incorporate SDLT into total acquisition costs when calculating real estate appraisal metrics including:

- Gross and net initial yields adjusted for all transaction costs

- Internal rate of return (IRR) calculations over hold periods

- Break-even rental income requirements

- Capital appreciation thresholds for target returns

Regulatory Compliance Costs: Beyond Awaab's Law, professional landlords face evolving regulatory requirements including Energy Performance Certificate (EPC) standards, electrical safety inspections, gas safety certificates, and potential future regulations. Institutional valuations must allocate annual compliance budgets typically ranging from 0.5-1.0% of property value depending on asset age and condition.

Rental Demand Forecasting and Portfolio Positioning

The projected 12% rental income growth through 2030 creates compelling value propositions for institutional buy-to-let investors[3]. However, capturing this growth requires strategic positioning based on granular rental demand analysis.

Demographic Demand Drivers: The UK's persistent housing affordability crisis continues driving rental demand, particularly among:

- Young professionals priced out of homeownership in urban centers

- Families requiring flexible accommodation before purchasing

- Relocated workers seeking quality rental properties near employment hubs

- International students and workers in major cities

Institutional investors should prioritize geographic markets demonstrating strong employment growth, transport connectivity, and supply constraints. Professional property assessment should evaluate local market fundamentals including:

- Employment diversity and wage growth trajectories

- Housing supply pipeline and planning constraints

- Transport infrastructure investment

- Rental yield spreads relative to purchase prices

Property Type Considerations: Within residential buy-to-let, different property types exhibit varying risk-return profiles:

| Property Type | Typical Yield | Tenant Demand | Management Intensity | Capital Growth Potential |

|---|---|---|---|---|

| City Center Apartments | 4.5-5.5% | High (professionals) | Medium | Moderate |

| Suburban Family Homes | 4.0-5.0% | Stable (families) | Low-Medium | Strong |

| Student Accommodation | 6.0-8.0% | Cyclical (academic) | High | Moderate |

| HMO Properties | 7.0-10.0% | High (multiple tenants) | Very High | Variable |

Institutional portfolios should balance yield optimization with management efficiency and regulatory compliance complexity. The 22.2% average property value increase forecast over five years suggests capital appreciation will contribute substantially to total returns, making property type selection crucial for capturing both income and growth[3].

Valuation Adjustments for Institutional Investors

Market Recovery Valuation Methodologies

Institutional buy-to-let valuations in 2026 recovery require adapted methodologies that account for the transitional market environment. Traditional comparable-based valuations must be supplemented with forward-looking adjustments reflecting:

Recovery Phase Pricing: Properties valued during recovery periods often exhibit pricing inefficiencies as market participants adjust expectations. Professional landlords should employ multiple valuation approaches:

- Comparable Sales Analysis: Adjusted for transaction timing, property condition, and location-specific recovery trajectories

- Income Capitalization: Using current rental income and market-appropriate capitalization rates reflecting the improved return environment

- Discounted Cash Flow: Incorporating rental growth forecasts (12% over five years) and terminal value assumptions based on normalized market conditions

- Replacement Cost Analysis: Particularly relevant given construction cost inflation and supply constraints

The convergence of these methodologies provides valuation ranges that institutional investors can stress-test against different recovery scenarios. Given the 9-10% total return projections for 2026, valuations should reflect improving market sentiment while maintaining conservative assumptions for regulatory compliance costs[1].

Compliance Cost Integration

Awaab's Law and evolving regulatory requirements necessitate explicit compliance cost adjustments in institutional valuations. Professional landlords should implement systematic approaches:

Pre-Acquisition Due Diligence: Comprehensive property inspection guidance should include:

- Detailed building surveys identifying damp, mould, and ventilation issues

- EPC assessments with upgrade cost estimates for sub-standard properties

- Electrical and gas safety evaluations

- Structural integrity assessments for older properties

Compliance Cost Reserves: Institutional valuations should deduct estimated compliance costs from gross property values:

- Immediate remediation: Costs to address identified Awaab's Law issues before tenant occupation

- Ongoing compliance: Annual budgets for mandatory inspections and certifications

- Future upgrades: Anticipated costs for evolving EPC requirements and building standards

For example, a property requiring £15,000 in damp remediation, £5,000 in ventilation improvements, and £8,000 in EPC upgrades should reflect a £28,000 valuation reduction plus an appropriate risk premium for execution uncertainty.

Portfolio-Level Risk Diversification

Institutional buy-to-let investors benefit from portfolio-level risk management unavailable to individual landlords. Strategic diversification across multiple dimensions reduces exposure to localized risks:

Geographic Diversification: Spreading investments across regions with varying economic drivers mitigates local market downturns. The residential sector's +2.2% growth masks substantial regional variation, with some markets significantly outperforming while others lag[1].

Property Type Diversification: Balancing high-yield HMO properties with stable family homes and professional apartments creates income stability while capturing growth opportunities across tenant segments.

Lease Term Diversification: Staggering lease renewal dates prevents concentrated vacancy risk and allows periodic rent adjustments aligned with market conditions.

Financing Diversification: Varying loan maturities and fixed versus variable rate allocations provides flexibility to optimize refinancing timing as interest rates evolve.

Professional landlords should develop portfolio optimization models that maximize risk-adjusted returns while maintaining compliance with regulatory requirements and financing covenants. The projected 7.8% average annual returns through 2030 suggest substantial value creation potential for well-structured institutional portfolios[2].

Technology Integration in Valuation Processes

Modern institutional buy-to-let valuations increasingly leverage technology platforms that enhance accuracy and efficiency:

Automated Valuation Models (AVMs): Machine learning algorithms analyzing comparable transactions, property characteristics, and market trends provide rapid initial valuations for portfolio screening.

Property Management Systems: Integrated platforms tracking rental income, maintenance costs, compliance deadlines, and tenant communications generate real-time performance data informing valuations.

Predictive Analytics: Advanced modeling incorporating economic indicators, demographic trends, and regulatory changes enables forward-looking valuation adjustments.

Digital Inspection Tools: Thermal imaging, moisture meters, and photographic documentation create comprehensive property condition records supporting building surveys and compliance verification.

Institutional investors should integrate these technologies within broader valuation frameworks while maintaining professional surveyor oversight for complex assessments and regulatory compliance verification.

Strategic Implementation for Professional Landlords

Acquisition Strategy in the 2026 Recovery

The current market environment favors selective acquisition strategies targeting properties offering:

Value-Add Opportunities: Properties requiring compliance upgrades or modernization that institutional investors can execute efficiently, creating immediate value through improved rental income and reduced void periods.

Below-Replacement-Cost Pricing: Given construction cost inflation, properties priced below current replacement costs offer inherent value protection and capital appreciation potential as the market normalizes.

Strong Rental Demand Fundamentals: Locations demonstrating employment growth, transport connectivity, and constrained supply where the projected 12% rental income growth is most achievable[3].

Portfolio Synergies: Properties complementing existing holdings through geographic clustering (enabling management efficiencies) or tenant diversification (reducing concentration risk).

Professional landlords should establish clear acquisition criteria incorporating minimum yield thresholds, maximum compliance cost tolerances, and target hold periods aligned with portfolio objectives. The improved transaction volumes in 2026 provide increased deal flow for selective investors[1].

Refinancing and Capital Optimization

The refinancing wave emerging in 2026 creates opportunities for institutional investors to optimize capital structures[5]. Professional landlords should evaluate:

Rate Lock Strategies: With BTL rates at 3.79% for optimal products and potential base rate reductions ahead, timing refinancing to capture favorable rates while maintaining flexibility for future optimization[4].

Equity Release for Portfolio Expansion: Leveraging improved property values and rental income to extract equity for new acquisitions, particularly where portfolio properties have appreciated during the recovery.

Loan-to-Value Optimization: Balancing leverage to maximize returns while maintaining adequate equity buffers for stress scenarios and lender covenant compliance.

Lender Relationship Management: Developing relationships with institutional lenders offering competitive terms and flexible structures for professional landlord portfolios.

Institutional investors should model multiple refinancing scenarios incorporating different interest rate trajectories, property value assumptions, and rental income forecasts to identify optimal timing and structures.

Regulatory Compliance Management Systems

Awaab's Law compliance and evolving regulatory requirements necessitate systematic management approaches for institutional portfolios:

Compliance Calendars: Centralized tracking of inspection deadlines, certification renewals, and regulatory reporting requirements across all portfolio properties.

Tenant Communication Protocols: Standardized systems for receiving, documenting, and responding to tenant-reported issues within Awaab's Law timeframes.

Contractor Networks: Pre-qualified networks of contractors capable of rapid response for emergency remediation and routine maintenance.

Documentation Systems: Comprehensive records of all inspections, remediation works, tenant communications, and compliance certifications for regulatory defense and portfolio management.

Professional landlords should consider dedicated compliance personnel or specialized property management firms with expertise in regulatory requirements for institutional portfolios. The reputational and financial risks of non-compliance far exceed the costs of robust management systems.

Future Outlook and Risk Monitoring

Market Evolution Through 2030

The five-year outlook for institutional buy-to-let investments remains compelling, with Savills predicting 7.8% average annual total returns as rental growth strengthens and interest-rate pressures ease[2]. The projected 22.2% average property value increase through 2030 combined with 12% rental income growth creates substantial value creation potential[3].

However, professional landlords must monitor evolving risk factors:

Regulatory Trajectory: Future governments may introduce additional landlord obligations, tenant protections, or taxation changes affecting returns. Institutional investors should maintain flexibility to adapt portfolios to regulatory evolution.

Interest Rate Volatility: While two base rate cuts appear plausible in 2026, the trajectory beyond remains uncertain. Persistent inflation or economic shocks could alter monetary policy expectations[5].

Supply Response: Increased institutional investment and potential planning reform could increase rental housing supply, moderating rental growth in some markets.

Economic Conditions: Recession risks, employment volatility, or wage stagnation could affect tenant demand and rental affordability.

Professional landlords should implement quarterly risk reviews assessing these factors and adjusting portfolio strategies accordingly. The improved market liquidity in 2026 provides greater flexibility for portfolio rebalancing compared to the constrained environment of 2023-2024[1].

Performance Monitoring and Portfolio Optimization

Institutional buy-to-let investors should establish comprehensive performance monitoring frameworks tracking:

Financial Metrics:

- Gross and net rental yields by property and portfolio

- Occupancy rates and void period durations

- Maintenance and compliance cost ratios

- Debt service coverage ratios

- Total return (income plus capital appreciation)

Operational Metrics:

- Tenant satisfaction and retention rates

- Compliance deadline adherence

- Response times for maintenance requests

- Property condition scores

Market Metrics:

- Local rental rate movements

- Comparable property values

- Supply pipeline developments

- Economic indicator trends

Regular performance reviews enable proactive portfolio optimization, identifying underperforming assets for remediation or disposal and high-performing markets for additional investment. The projected strong returns through 2030 reward institutional investors who maintain disciplined performance management and strategic flexibility[2].

Conclusion

Institutional Buy-to-Let Valuations in 2026 Recovery: Risk Assessment Protocols for Professional Landlords represent a sophisticated discipline combining traditional property valuation methodologies with enhanced regulatory compliance frameworks and forward-looking market analysis. The UK property market's emergence from its 25% correction, with capital values growing 1.3% annually and total returns projected at 9-10% for 2026, creates compelling opportunities for well-positioned institutional investors[1].

However, capturing these returns requires rigorous risk assessment protocols addressing Awaab's Law compliance, elevated financing costs, increased stamp duty burdens, and evolving regulatory requirements. Professional landlords must implement comprehensive property condition assessments, sophisticated financial modeling incorporating multiple stress scenarios, and strategic portfolio positioning aligned with rental demand forecasts projecting 12% income growth through 2030[3].

The institutional advantages of scale, professional management systems, and diversified portfolios position professional landlords to outperform in this recovery environment. By integrating compliance cost adjustments into valuations, leveraging technology for enhanced due diligence, and maintaining disciplined acquisition criteria, institutional investors can achieve the projected 7.8% average annual returns while managing the regulatory and operational risks that have intensified since 2024[2].

Actionable Next Steps for Professional Landlords

- Conduct Portfolio Compliance Audits: Engage qualified surveyors to assess all properties for Awaab's Law compliance, identifying remediation requirements and budgeting accordingly

- Refine Valuation Methodologies: Update acquisition models to incorporate 5% SDLT rates, current BTL financing costs, and compliance expense reserves

- Develop Refinancing Strategies: Evaluate existing financing against current 3.79% BTL rates and model optimal refinancing timing[4]

- Establish Risk Monitoring Systems: Implement quarterly reviews of portfolio performance, market conditions, and regulatory developments

- Engage Professional Advisors: Consult with property surveyors specializing in institutional buy-to-let for comprehensive due diligence on acquisition opportunities

The 2026 recovery presents a generational opportunity for institutional buy-to-let investors who combine strategic vision with rigorous risk management. Professional landlords implementing the protocols outlined in this analysis position themselves to capture substantial returns while navigating the transformed regulatory landscape defining modern residential property investment.

References

[1] Uk Real Estate Market Commentary January 2026 – https://www.schroders.com/en-gb/uk/institutional/insights/uk-real-estate-market-commentary—january-2026/

[2] Are Successful Investors Back In The High Value Property Market For 2026 – https://togethermoney.com/blog/are-successful-investors-back-in-the-high-value-property-market-for-2026

[3] Buy To Let Valuation Surge 2026 Survey Strategies For Institutional Investors In A Recovering Market – https://nottinghillsurveyors.com/blog/buy-to-let-valuation-surge-2026-survey-strategies-for-institutional-investors-in-a-recovering-market

[4] Buy To Let Market Update February 2026 – https://www.nrla.org.uk/news/buy-to-let-market-update-february-2026

[5] What Could Shape Buy To Let In 2026 And The Impact For Advisers – https://mortgagesoup.co.uk/what-could-shape-buy-to-let-in-2026-and-the-impact-for-advisers/