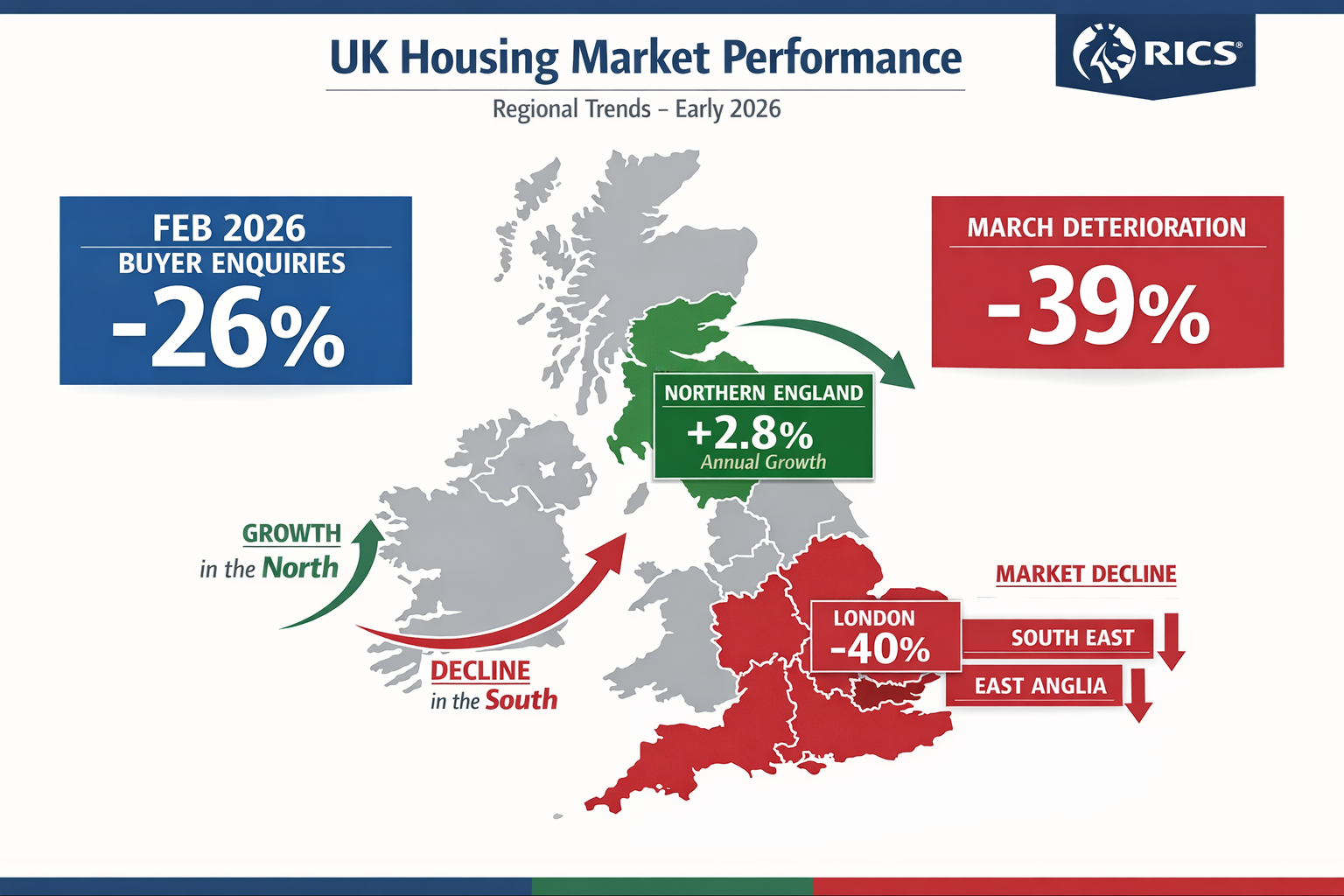

New buyer enquiries plummeted to -26% in February 2026, then crashed further to -39% in March, marking the sharpest deterioration in market confidence since the Middle East conflict escalated—yet 33% of surveyors still expect prices to rise over the next twelve months[1][5]. This striking contradiction between short-term pessimism and long-term optimism defines the complex landscape of Geopolitical Uncertainty in Spring 2026 Valuations: RICS February Survey Insights for Northern England Resilience, where regional divergence has become the defining characteristic of the UK property market.

The Royal Institution of Chartered Surveyors (RICS) February 2026 residential survey reveals a market caught between immediate geopolitical shocks and underlying structural resilience, with Northern England emerging as an unexpected stronghold amid widespread uncertainty. While southern regions face mounting pressure, the North West and North East demonstrate remarkable stability, offering critical lessons for property professionals navigating turbulent conditions.

Key Takeaways

- Buyer enquiries collapsed from -26% in February to -39% in March 2026 as Middle East conflict escalated, representing the weakest market sentiment in the current cycle[1][5]

- Northern England shows exceptional resilience with the North East achieving 2.8% annual price growth—more than double the UK average of 1.3%—while London and the South East face sustained downward pressure[5]

- Near-term price expectations turned sharply negative at -43% for the three-month outlook, yet 12-month expectations remain cautiously optimistic at +33%, creating a strategic valuation paradox[1][5]

- Regional divergence has intensified with London's 12-month price expectations collapsing from +56% to just +7%, while Northern Ireland, Scotland, and the North West maintain firmer trends[1][2]

- First-time buyer segment offers recovery pathway as industry experts identify increased property listings as the "best early sign of activity in 2026," with recovery likely to emerge from entry-level markets[2]

Understanding the February 2026 Market Context and Geopolitical Uncertainty in Spring 2026 Valuations

The RICS February 2026 survey captured a pivotal moment when tentative early-year optimism collided with renewed geopolitical instability. After January showed modest improvement with buyer enquiries at -15%, February's deterioration to -26% signaled renewed weakness amid concerns over the interest rate outlook and broader macroeconomic uncertainty[1][2]. The subsequent March collapse to -39% confirmed that external geopolitical factors—particularly the escalation of Middle East tensions—had fundamentally altered market dynamics.

The Geopolitical Shock Effect

The escalation of the Middle East conflict directly weakened market momentum that had shown tentative signs of recovery at the start of 2026[3][5]. This geopolitical shock manifested through multiple channels:

- Immediate confidence collapse: Prospective buyers delayed decisions amid uncertainty about economic stability and future interest rate trajectories

- Macroeconomic spillover effects: Energy price volatility, inflation concerns, and potential supply chain disruptions created additional hesitancy

- Regional variation in impact: Southern markets with higher price points and greater exposure to international investment flows experienced more severe sentiment deterioration

For property professionals seeking RICS-qualified surveyors to navigate these complex conditions, understanding the distinction between short-term volatility and underlying market fundamentals has become critical.

The Price Expectations Paradox

One of the most striking features of the February 2026 data is the dramatic divergence between near-term and medium-term price expectations. The near-term headline price expectations balance fell to -43% in March 2026 (down sharply from -19% in February), signaling anticipated downward pressure on values over the coming three months[5]. Yet simultaneously, +33% of respondents expect house prices to edge higher over a 12-month horizon[1][3].

This paradox reflects several underlying market realities:

| Timeframe | Price Expectation | Driving Factors |

|---|---|---|

| 3-Month Outlook | -43% (negative) | Geopolitical uncertainty, weak buyer enquiries, seasonal factors |

| 12-Month Outlook | +33% (positive) | Structural housing shortage, demographic demand, interest rate stabilization expectations |

| Regional Variation | High divergence | Northern resilience vs. Southern pressure, local economic conditions |

This temporal split creates significant challenges for property valuation professionals who must balance immediate market conditions against longer-term value trajectories when advising clients on property valuation strategies.

Regional Divergence: Northern England Resilience in Geopolitical Uncertainty and Spring 2026 Valuations

The most compelling narrative emerging from the Geopolitical Uncertainty in Spring 2026 Valuations: RICS February Survey Insights for Northern England Resilience is the stark regional divergence between northern and southern property markets. While London, the South East, and East Anglia face persistent downward pressure, Northern England demonstrates remarkable stability and growth.

North East Performance: The National Outperformer

The North East achieved price growth of 2.8% annually, significantly outperforming the UK average of 1.3%[5]. This exceptional performance stems from several structural advantages:

- Affordability factor: Lower absolute price points maintain accessibility for first-time buyers and local movers

- Committed buyer base: Mainstream demand remains solid with buyers less susceptible to short-term sentiment shifts

- Economic resilience: Diversified local economies with growing sectors in technology, healthcare, and education

- Limited speculative activity: Reduced exposure to international investment flows that amplify volatility in southern markets

💡 Expert Insight: The North East's outperformance demonstrates that affordability-driven demand provides insulation against geopolitical shocks, as committed local buyers continue transacting regardless of broader market sentiment.

North West Stability

The North West of England continues to report firmer price trends alongside Northern Ireland and Scotland, contrasting sharply with southern regions[1][2][3]. Manchester, Liverpool, and surrounding areas benefit from:

- Strong employment markets with diverse industry bases

- Ongoing infrastructure investment including transport connectivity improvements

- University-driven rental demand supporting investment activity

- Regional regeneration programs maintaining development momentum

Southern England's Persistent Pressure

The contrast with southern markets could not be more stark. As of February 2026, the regions facing the strongest downward pressure include:

- London: -40% price sentiment, with 12-month expectations collapsing from +56% to just +7%[1]

- South East: -24% downward pressure[1][2][3]

- East Anglia: -26% negative sentiment[1][2][3]

This southern weakness reflects multiple compounding factors including higher price-to-income ratios, greater exposure to international capital flows affected by geopolitical uncertainty, and increased sensitivity to interest rate changes given higher absolute mortgage amounts.

For buyers considering properties in areas experiencing downward pressure, understanding the implications through a comprehensive homebuyers report becomes even more critical when negotiating in uncertain markets.

Valuation Strategies and Surveyor Insights for Geopolitical Uncertainty in Spring 2026 Valuations

The Geopolitical Uncertainty in Spring 2026 Valuations: RICS February Survey Insights for Northern England Resilience presents both challenges and opportunities for property professionals. Developing robust valuation strategies requires understanding how to balance short-term market disruption against longer-term value fundamentals.

The Supply-Demand Dynamic

Despite weakening buyer enquiries, the supply pipeline remains relatively stable. New instructions posted a net balance of +2%, with market appraisals unchanged, indicating little immediate shift in the pipeline of new stock[1][3]. This stability in supply amid falling demand creates specific valuation considerations:

For sellers: The combination of stable supply and weak demand suggests downward price pressure in the immediate term, particularly in southern regions. Properties may require longer marketing periods or price adjustments to attract committed buyers.

For buyers: Weakening competition creates negotiation opportunities, especially when armed with professional survey evidence. Understanding how to leverage survey findings for price negotiation becomes particularly valuable in softening markets.

First-Time Buyer Segment: The Recovery Leader

Industry expert Tim Green FRICS of Green & Co. (Oxford) Ltd identified "the increased number of properties coming to the market" as "the best early sign of activity in 2026," with recovery "likely to be led from the first-time buyer range"[2]. However, he cautioned that "Spring has not quite arrived yet," suggesting the traditional seasonal uplift may be delayed by geopolitical uncertainty.

This first-time buyer focus creates specific strategic implications:

✅ Entry-level properties (typically under £250,000 in northern markets) demonstrate greater resilience

✅ Affordable regional markets attract committed buyers less influenced by sentiment

✅ Help to Buy and mortgage guarantee schemes provide structural support to this segment

✅ Lower loan-to-value requirements reduce transaction sensitivity to short-term valuation fluctuations

Regional Valuation Strategies

Property professionals must adopt location-specific approaches that recognize the fundamental differences between resilient northern markets and pressure-facing southern regions:

Northern England Strategy

- Emphasize local market fundamentals over national sentiment indicators

- Highlight affordability advantages and sustainable price-to-income ratios

- Focus on committed buyer base rather than speculative demand

- Leverage employment growth and infrastructure investment narratives

- Position properties for long-term value appreciation given structural demand

Southern England Strategy

- Acknowledge near-term pressure while emphasizing 12-month recovery expectations

- Identify value opportunities in temporarily depressed segments

- Emphasize quality and condition as differentiators in competitive markets

- Target committed movers rather than discretionary upgraders

- Utilize professional surveys to justify pricing and identify negotiation leverage

For those navigating complex valuation decisions, understanding the differences between survey levels helps ensure appropriate due diligence matches market conditions and property characteristics.

Transaction Activity and Agreed Sales

Agreed sales remained subdued in February at a net balance of only -12%, indicating weak transaction momentum despite some early-year optimism[1]. This subdued activity level reflects several factors:

- Buyer caution amid geopolitical uncertainty delaying commitment decisions

- Mortgage affordability constraints continuing to limit purchasing power

- Seasonal factors with traditional spring market activity delayed

- Economic uncertainty encouraging wait-and-see approaches

However, the fact that transactions continue—albeit at reduced levels—demonstrates that committed buyers with genuine housing needs continue to move forward, creating opportunities for well-positioned properties and realistic pricing strategies.

Professional Survey Value in Uncertain Markets

The combination of geopolitical uncertainty, regional divergence, and price expectation paradoxes makes professional property surveys more valuable than ever. When market conditions create ambiguity, independent professional assessment provides clarity for both buyers and sellers:

- Risk identification: Structural or condition issues that might justify price adjustments gain greater negotiating weight in softening markets

- Value validation: Professional confirmation of fair market value provides confidence for buyers concerned about overpaying in uncertain conditions

- Investment protection: Thorough assessment protects against purchasing properties with hidden defects that could compound value losses in declining markets

Understanding common myths about property surveys helps buyers and sellers make informed decisions about when and how to commission professional assessments during periods of market uncertainty.

Looking Forward: Spring 2026 and Beyond

As spring 2026 progresses, several key factors will determine whether the cautious 12-month optimism (+33%) proves justified or whether near-term pessimism (-43%) extends into a more prolonged downturn:

Critical Watch Points

🔍 Geopolitical developments: Resolution or further escalation of Middle East tensions will significantly impact confidence trajectories

🔍 Interest rate policy: Bank of England decisions on rate cuts or holds will directly affect mortgage affordability and buyer capacity

🔍 Regional economic performance: Continued strength in northern employment markets versus potential southern weakness will reinforce or moderate divergence trends

🔍 First-time buyer activity: Whether this segment leads recovery as predicted will signal broader market direction

🔍 Supply response: Any significant increase in new instructions could shift the supply-demand balance and pricing dynamics

Opportunities in Uncertainty

While headlines focus on falling enquiries and negative near-term sentiment, the Geopolitical Uncertainty in Spring 2026 Valuations: RICS February Survey Insights for Northern England Resilience reveals genuine opportunities for informed market participants:

For buyers: Reduced competition, motivated sellers, and negotiation leverage create favorable purchasing conditions, particularly in northern markets where fundamentals remain strong. Commissioning comprehensive surveys to identify value opportunities and negotiation points maximizes the advantage.

For sellers: Understanding regional dynamics and pricing appropriately for current conditions—rather than recent peak values—facilitates transactions. Properties in resilient northern markets maintain pricing power, while southern sellers may need to adjust expectations for near-term conditions while emphasizing long-term value.

For investors: Regional divergence creates arbitrage opportunities, with northern markets offering better value, stronger yields, and more stable capital appreciation prospects compared to temporarily depressed southern markets that may offer recovery potential for patient capital.

For professionals: Surveyors, valuers, and estate agents who understand the nuanced regional picture and can articulate the distinction between short-term volatility and medium-term fundamentals provide exceptional value to clients navigating uncertainty.

Conclusion

The Geopolitical Uncertainty in Spring 2026 Valuations: RICS February Survey Insights for Northern England Resilience reveals a UK property market in transition, where external geopolitical shocks have created immediate disruption while underlying structural factors suggest medium-term stability. The dramatic collapse in buyer enquiries—from -26% in February to -39% in March 2026—reflects genuine uncertainty, yet the persistent +33% expectation for 12-month price growth demonstrates professional confidence in fundamental market resilience[1][5].

Most significantly, the stark regional divergence between resilient northern markets and pressure-facing southern regions represents the defining characteristic of the current cycle. The North East's exceptional 2.8% annual growth—more than double the national average—alongside broader Northern England stability demonstrates that affordability, local economic strength, and committed buyer bases provide insulation against geopolitical volatility[5].

Actionable Next Steps

For anyone navigating the spring 2026 property market, consider these strategic actions:

-

Recognize regional realities: Don't apply national sentiment to local markets—Northern England fundamentals differ dramatically from southern dynamics

-

Commission professional surveys: In uncertain markets, independent assessment from qualified RICS surveyors provides clarity, identifies risks, and creates negotiation leverage

-

Focus on fundamentals: Look beyond short-term sentiment to underlying factors including affordability, employment trends, and structural supply-demand balance

-

Target committed segments: First-time buyers and genuine movers continue transacting—position properties and strategies to capture this resilient demand

-

Maintain perspective: The paradox between near-term pessimism and medium-term optimism suggests current conditions represent opportunity rather than crisis for informed participants

-

Act on conviction: If fundamentals support a transaction, don't let short-term volatility prevent sound decisions—but ensure professional due diligence protects your position

The spring 2026 market may not deliver the traditional seasonal uplift amid geopolitical uncertainty, but it offers genuine opportunities for buyers, sellers, and investors who understand the nuanced regional picture and act on evidence rather than sentiment. Northern England's resilience demonstrates that even amid global uncertainty, local fundamentals ultimately determine property market outcomes.

References

[1] Uk Residential Survey February 2026 – https://www.rics.org/news-insights/uk-residential-survey-february-2026

[2] Latest Rics Survey Reveals Global Headwinds Are Weighing On Housing Market Confidence – https://www.buyassociationgroup.com/en-gb/news/latest-rics-survey-reveals-global-headwinds-are-weighing-on-housing-market-confidence/

[3] Uk Residential Market Survey February 2026 – https://www.rics.org/content/dam/ricsglobal/documents/market-surveys/uk-residential-market-survey/UK-Residential-Market-Survey_February-2026.pdf

[4] Valuation Challenges In Weak Buyer Demand Rics February 2026 Survey Analysis And Surveyor Strategies – https://nottinghillsurveyors.com/blog/valuation-challenges-in-weak-buyer-demand-rics-february-2026-survey-analysis-and-surveyor-strategies

[5] Uk Residential Market Survey March 2026 – https://www.rics.org/content/dam/ricsglobal/documents/market-surveys/uk-residential-market-survey/UK-Residential-Market-Survey-March-2026.pdf