One in five UK property transactions is now affected by a valuation that falls short of the agreed purchase price — a figure that has risen sharply as asking prices outpace what comparable evidence can support [6]. For buyers, the result can be a collapsed mortgage offer, a renegotiated deal, or a forced withdrawal. For lenders, it signals risk. For the valuation surveyor caught in the middle, it raises a deceptively difficult professional challenge: how do you deliver an unpopular but accurate opinion in a way that is understood, respected, and acted upon?

Down‑valuations and 'over‑optimistic' asking prices: how UK valuation surveyors can communicate market reality to buyers and lenders is not simply a technical problem — it is a communication problem. The numbers may be correct, but if the reasoning behind them is poorly explained, the result is confusion, disputes, and damaged professional relationships. This article explores the practical strategies surveyors can use to present evidence clearly, manage expectations professionally, and protect the integrity of the valuation process.

Key Takeaways 📌

- A "down‑valuation" is not a mistake — it is the surveyor's evidence-based opinion of market value when an agreed price exceeds what comparable sales support.

- RICS' own position is that there is no such thing as a down‑valuation; there is only market value, which may differ from an aspirational asking price [4].

- Clear communication of comparable evidence, condition factors, and local market nuance is the cornerstone of a defensible valuation.

- Surveyors who structure their reports and client conversations around evidence — not opinion — are far better placed to withstand challenge.

- Proactive expectation management, delivered early and professionally, reduces disputes and supports smoother transactions for all parties.

What a Down‑Valuation Actually Is — and Why the Term Matters

Before exploring communication strategy, it is worth being precise about terminology. A down‑valuation occurs when a lender's surveyor assesses a property's market value as lower than the price the buyer has agreed to pay [1]. The lender will then base its mortgage offer on the surveyor's figure, not the agreed price — leaving the buyer to fund the shortfall from their own resources, renegotiate with the seller, or walk away [2].

💬 "In reality there is no such thing as a down valuation — what people call a down valuation is simply the surveyor's opinion of market value." — HomeOwners Alliance [4]

This framing matters enormously for how surveyors communicate their findings. The word "down" implies that the surveyor has reduced something — that an error has been made or a bias applied. In fact, the surveyor has simply assessed market value using professional methodology. The "gap" exists because the agreed price was set above that value in the first place [4].

When surveyors internalise this distinction and communicate it clearly, they shift the conversation from "why have you valued it lower?" to "what does the market evidence actually show?" That is a far more productive starting point for all parties.

Why Asking Prices Become 'Over‑Optimistic'

Several factors drive asking prices above supportable market values:

- Seller sentiment: Homeowners naturally anchor to the highest price they have heard, seen advertised, or been quoted by an eager agent.

- Estate agent competition: Agents pitching for instructions sometimes quote optimistic figures to win the mandate [7].

- Market momentum assumptions: Sellers in rising markets assume upward trends will continue indefinitely, even when comparable evidence has plateaued [10].

- Emotional value: Improvements, memories, and personal investment lead sellers to overestimate what the open market will pay.

- Thin comparables: In areas with low transaction volumes, a single outlier sale can distort expectations significantly [5].

Understanding these drivers helps surveyors frame their communication with empathy rather than confrontation — acknowledging why a price was set while explaining clearly why the evidence does not support it.

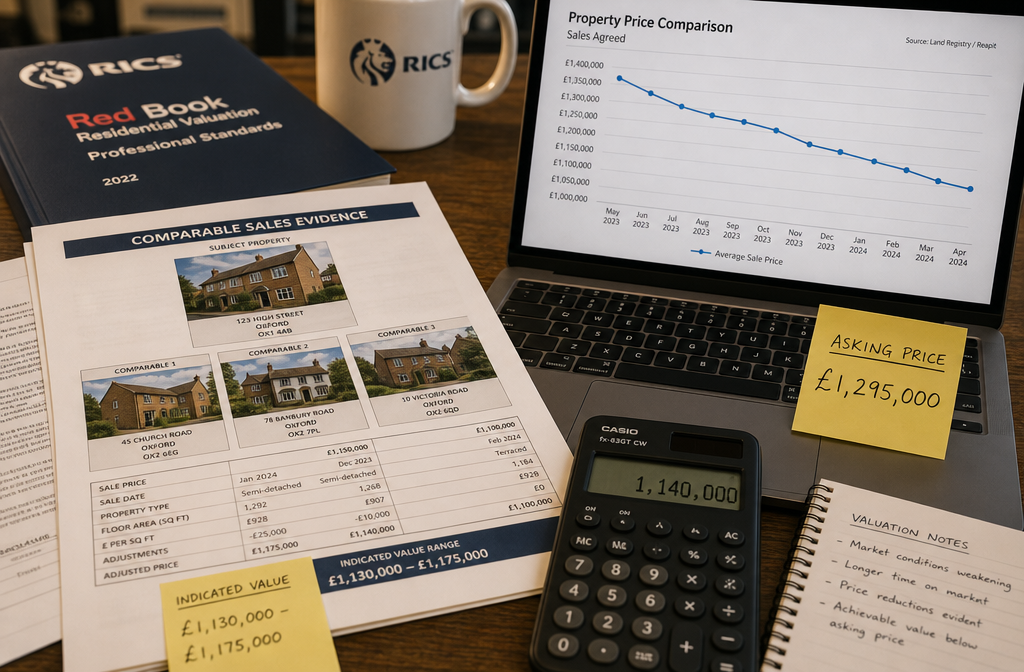

The Evidence Framework: How Surveyors Can Justify Their Position

The most effective defence of any valuation — and the most persuasive communication tool — is a well-constructed body of comparable evidence. This is not simply a matter of listing recent sales; it is about selecting, contextualising, and presenting comparables in a way that a non-specialist buyer or lender can follow.

Selecting and Presenting Comparable Evidence

Effective comparable selection follows a clear hierarchy:

| Priority | Comparable Type | Why It Matters |

|---|---|---|

| 1st | Same street, same property type, last 3–6 months | Closest proxy for current market value |

| 2nd | Same postcode sector, similar specification | Adjusts for micro-location differences |

| 3rd | Adjacent streets, similar age and condition | Used when local supply is thin |

| 4th | Wider area, with explicit adjustments noted | Only used with clear written justification |

When presenting these to buyers or lenders, surveyors should:

✅ Name the comparables explicitly — address, sale date, price per square foot, and brief condition notes.

✅ Explain any adjustments made — if a comparable sold at £450/sq ft but had a new kitchen, note the adjustment applied.

✅ Highlight what is absent — if no comparable supports the agreed price, say so directly and explain why that matters.

✅ Reference data sources — Land Registry, Rightmove Sold Prices, and local agent intelligence should all be cited where used [3].

For buyers seeking to understand the full scope of what a professional assessment covers, reviewing an example of a homebuyers report can clarify how evidence is structured within a formal survey document.

Condition Factors as Value Adjusters

Comparable sales alone rarely tell the complete story. A property's physical condition — relative to the comparables used — is a legitimate and often decisive value adjuster. Surveyors should document and communicate condition factors clearly:

- Structural defects: Subsidence, cracking, or roof deterioration that comparables did not present [see also: should you be worried if walls start cracking].

- Damp and moisture ingress: A significant negative value driver that buyers and lenders often underestimate.

- Deferred maintenance: Kitchens, bathrooms, and heating systems that are beyond their functional life reduce achievable price relative to well-maintained comparables.

- Energy performance: EPC ratings increasingly influence buyer appetite and lender appetite alike in 2026.

Each condition factor should be linked explicitly to its estimated impact on value — not left as a vague observation. A statement such as "the presence of active damp to the rear elevation, requiring remediation estimated at £8,000–£12,000, reduces the adjusted comparable value by approximately 2–3%" is far more defensible and comprehensible than a general note about damp.

For more on how condition findings affect negotiated outcomes, the guide on average price reduction after survey provides useful context for buyers navigating post-survey renegotiations.

Local Market Nuance: Going Beyond the Headline Numbers

National house price indices and regional averages are blunt instruments. A surveyor operating in, say, Merton or Bromley will know that micro-location factors — proximity to a good school, a planned development, a busy road, or a flood zone — can move values by 5–15% within a single postcode [10].

These nuances must be communicated explicitly. Surveyors should:

- Reference specific local market conditions, not just national trends.

- Note any pipeline supply issues (new developments, permitted development conversions) that may suppress future demand.

- Acknowledge seasonal factors where relevant — thin winter transaction volumes can skew apparent comparables.

- Distinguish between list price trends and achieved price trends, which can diverge significantly in a softening market [7].

Communicating Market Reality: Practical Strategies for Down‑Valuations and 'Over‑Optimistic' Asking Prices

The technical quality of a valuation is only part of the professional challenge. Equally important is how that valuation is communicated — to buyers, to lenders, and sometimes to estate agents who have a commercial interest in a different outcome.

Structuring the Valuation Report for Clarity

A well-structured report is the surveyor's primary communication tool. When addressing down‑valuations and 'over‑optimistic' asking prices, the report should follow a logical narrative:

- State the market value figure clearly and early — do not bury it.

- Explain the methodology — RICS Red Book (formally, the RICS Valuation — Global Standards) compliance should be referenced where applicable. For guidance on when a formal Red Book valuation is required, see when you need a Red Book valuation.

- Present the comparable evidence — structured as described above.

- Address condition adjustments — with estimated cost or value impact.

- Acknowledge the agreed price — and explain the gap in neutral, professional language.

- Avoid loaded language — phrases like "the seller is asking too much" are unhelpful; "the agreed price exceeds the market value supported by available evidence" is accurate and professional.

Managing Buyer Expectations Before the Report Lands

Experienced surveyors know that the worst time to deliver bad news is when it arrives unexpectedly in writing. Where a surveyor has early sight of the agreed price and has concerns about supportability, a brief, professional verbal flag to the instructing party — buyer or lender — can significantly reduce the shock of a formal down‑valuation.

This is not about pre-empting the report or compromising independence. It is about professional communication: "Based on what I have seen so far, I want to flag that the comparable evidence in this area may not fully support the agreed price. I will set this out clearly in my report."

That single sentence, delivered early, transforms the conversation from confrontation to informed expectation.

Responding to Challenges from Buyers and Agents

Down‑valuations frequently trigger challenges. Buyers feel their dream home is slipping away; agents feel their valuation has been publicly contradicted. Surveyors should be prepared to:

- Welcome challenges that include new evidence — a comparable the surveyor was unaware of, or a condition factor that has been remediated, may genuinely affect the valuation.

- Decline to revise on the basis of pressure alone — RICS professional standards are explicit that valuations must not be influenced by commercial pressure from any party [4].

- Document all challenges and responses — this protects the surveyor professionally and demonstrates the robustness of the original assessment.

- Explain the difference between a valuation and a survey — buyers sometimes conflate the two. A RICS homebuyer survey or RICS building survey assesses condition; a mortgage valuation assesses lending risk. Both are important but serve different purposes.

The Lender Relationship: Precision and Consistency

Lenders receive large volumes of valuation reports and rely on surveyors to present findings concisely and consistently. When communicating a below-agreed-price valuation to a lender, surveyors should:

- Use standard risk flags clearly — if the property is above a supportable LTV threshold, say so explicitly.

- Quantify uncertainty — where the market is thin or volatile, a valuation range with a central figure is more honest than false precision [10].

- Flag any special assumptions — if the valuation assumes a condition issue will be remediated, this must be stated.

- Avoid over-hedging — excessive caveats undermine confidence in the figure. State the position clearly, support it with evidence, and note material uncertainties concisely.

Lenders are not looking for surveyors to validate agreed prices — they are looking for an independent, evidence-based opinion of market value that protects their security. Surveyors who deliver this consistently, with clear reasoning, build the professional credibility that sustains long-term lender relationships.

When the Market Is the Problem: Navigating Uncertainty in 2026

The UK housing market in 2026 continues to present surveyors with a particularly challenging environment. Mortgage rate volatility, shifting buyer demand, and a persistent gap between seller expectations and buyer capacity have combined to increase the frequency of valuations falling below agreed prices [7]. In some regions, down‑valuations now affect a significant proportion of transactions, with millions of pounds being wiped from agreed deals as surveyors apply evidence-based discipline to an aspirational market [6].

This is not a failure of the valuation profession — it is the profession functioning exactly as it should. The surveyor's role is to provide an independent, evidence-based opinion of market value, not to validate whatever price a motivated seller and an eager buyer have agreed upon [4].

💬 "Down-valuations aren't going away while market uncertainty is with us." — Jonathan Rolande, Estate Agent Today [7]

For surveyors working across London and the South East — areas where price expectations are particularly elevated — local market knowledge is especially critical. Whether operating in Wandsworth, Southwark, or further afield, the ability to articulate micro-market conditions clearly is what separates a defensible valuation from a disputed one.

The Role of Choosing the Right Survey Type

Buyers who understand the difference between a mortgage valuation and an independent survey are better equipped to navigate down‑valuations. A mortgage valuation protects the lender; an independent survey protects the buyer. Encouraging buyers to commission their own survey — whether a Level 2 homebuyer report or a Level 3 building survey — gives them independent evidence that can either support or challenge a lender's figure. For guidance on selecting the right assessment, the homebuyers report or building survey comparison is a useful starting point.

Conclusion: Turning an Uncomfortable Conversation into a Professional Strength

Down‑valuations and 'over‑optimistic' asking prices represent one of the most professionally demanding scenarios a UK valuation surveyor faces. The numbers may be straightforward; the human dynamics rarely are.

The surveyors who navigate this challenge most effectively share a common approach: they lead with evidence, not opinion; they communicate early and clearly; they acknowledge the emotional context without compromising their professional independence; and they treat every challenge as an opportunity to demonstrate the rigour behind their assessment.

Actionable next steps for valuation surveyors:

- ✅ Build a structured comparable evidence template that can be shared with buyers and lenders in plain language.

- ✅ Develop a standard verbal script for early-stage expectation management when a price looks unsupportable.

- ✅ Document all post-report challenges and responses systematically — this protects professional standing and improves future practice.

- ✅ Stay current with micro-market data in your operating areas — national indices are not sufficient justification for local valuations.

- ✅ Familiarise clients with the distinction between mortgage valuations and independent surveys, and encourage buyers to commission their own assessment.

The valuation profession's credibility rests on its independence and its evidence base. When surveyors communicate both clearly, down‑valuations cease to be a source of conflict and become what they always were: an honest, professional service to buyers, lenders, and the market as a whole.

References

[1] What Is Down Valuation – https://housebuyers4u.co.uk/house-worth/what-is-down-valuation/

[2] What To Do If The House You're Buying Gets Down Valued By The Lender – https://davidphillip.co.uk/2022/11/11/what-to-do-if-the-house-youre-buying-gets-down-valued-by-the-lender/

[3] Down Valuations How Buyers Can Challenge A Low Mortgage Valuation – https://www.farrellheyworth.co.uk/blog/down-valuations-how-buyers-can-challenge-a-low-mortgage-valuation/

[4] Down Valuations – https://hoa.org.uk/advice/guides-for-homeowners/i-am-buying/down-valuations/

[5] Survey Down Valuations Silent House Sale Killer – https://www.linkedin.com/pulse/survey-down-valuations-silent-house-sale-killer-property-solvers-rfgle

[6] Surge In Property Down Valuations Wipes Millions From Stagnant UK Housing Market – https://housingindustryleaders.com/surge-in-property-down-valuations-wipes-millions-from-stagnant-uk-housing-market/

[7] Jonathan Rolande: Down Valuations Aren't Going Away While Market Uncertainty Is With Us – https://www.estateagenttoday.co.uk/breaking-news/2025/12/jonathan-rolande-down-valuations-arent-going-away-while-market-uncertainty-is-with-us/

[8] House Valuation Less Than Offer – https://www.housebuyerbureau.co.uk/blog/house-valuation-less-than-offer/

[10] Why Valuations Can Go Down As House Prices Go Up – https://sdlsurveying.co.uk/news/why-valuations-can-go-down-as-house-prices-go-up/