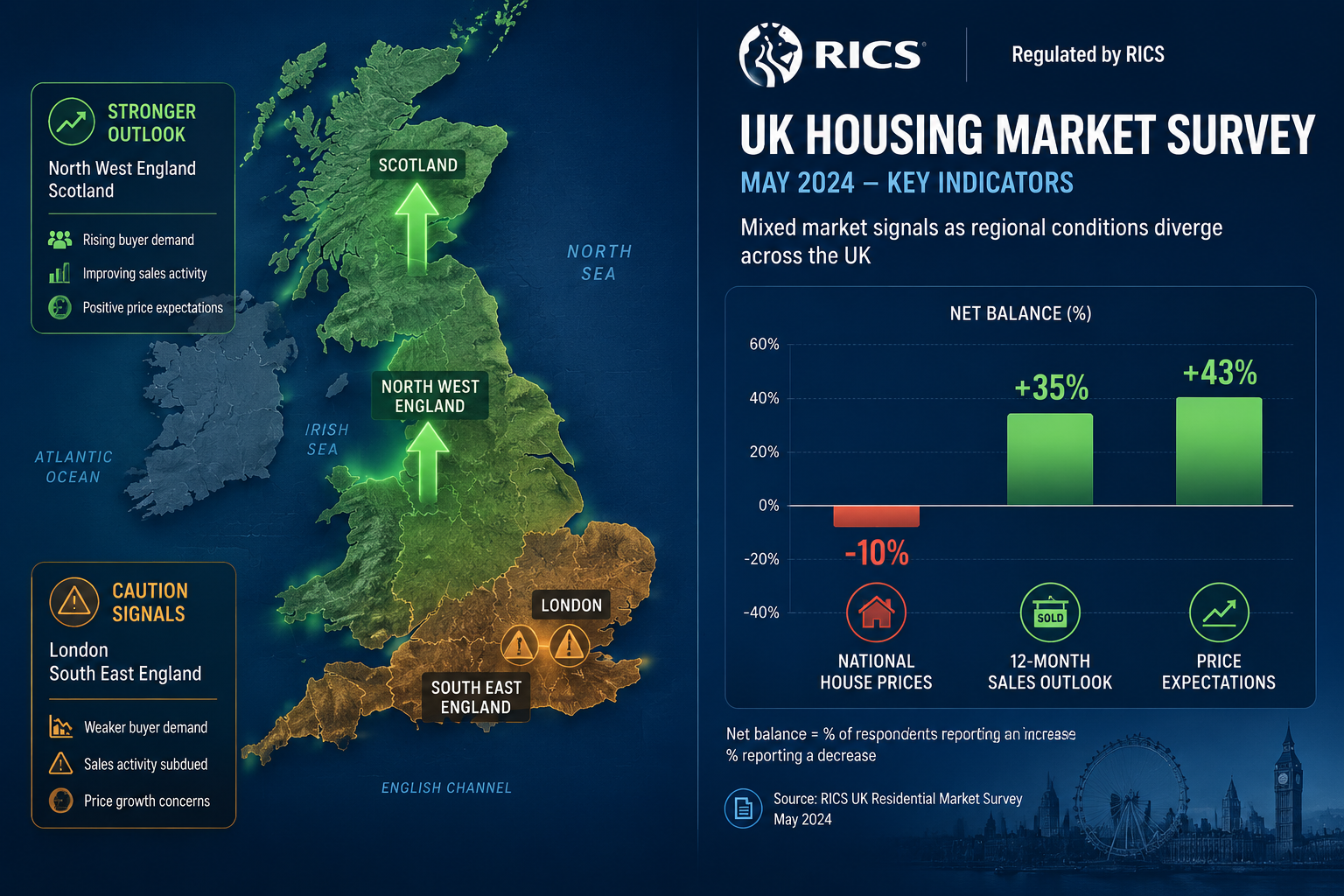

A net balance of +43% of RICS respondents now expect house prices to rise over the next twelve months — the most optimistic reading since February 2025 [1]. That single figure tells a story of a market that has turned a corner, but the story is far from uniform. The RICS January 2026 Survey Insights: Boosting Valuation Confidence in Recovering Regional Markets reveals a UK property landscape split sharply along geographic lines, with the North West surging while London and the South East remain stuck in a cautious holding pattern. For surveyors, valuers, and property professionals, understanding these divergences is not just academic — it directly shapes how building surveys are priced, commissioned, and interpreted in 2026.

Key Takeaways 📌

- National house prices are stabilising: The net balance improved to -10% from a low of -19% in October 2025, signalling a genuine turning point [1].

- Scotland, Northern Ireland, and the North West are leading recovery, while London and the South East continue to lag [1].

- 12-month sales optimism hit +35%, the strongest reading since December 2024, yet short-term caution persists at just +4% [1][2].

- Rental supply remains critically tight: New landlord instructions stand at -24%, pushing near-term rent expectations to +28% [2].

- Surveyors must adapt valuation tactics to account for widening regional disparities when producing building survey reports [6].

What the RICS January 2026 Data Actually Shows

The headline numbers from the January 2026 RICS Residential Market Survey paint a picture of cautious but genuine recovery. New buyer enquiries improved to a net balance of -15%, up from -21% in December and -29% in November [1]. Agreed sales reached a four-month high at -9%, the least negative reading since June 2025 [2]. These are still negative readings, but the direction of travel matters enormously for valuation professionals.

💬 "Green shoots of recovery indicated by January's RICS survey lend tentative support to predictions that house prices will surpass most people's expectations in 2026." — Capital Economics [3]

Breaking Down the Key Metrics

| Metric | January 2026 | Previous Month | Trend |

|---|---|---|---|

| New Buyer Enquiries (net balance) | -15% | -21% | ⬆️ Improving |

| House Prices (3-month net balance) | -10% | -19% (Oct 2025) | ⬆️ Recovering |

| Agreed Sales (net balance) | -9% | Worse | ⬆️ 4-month high |

| 12-Month Sales Outlook | +35% | Lower | ⬆️ Strongest since Dec 2024 |

| 12-Month Price Expectations | +43% | Lower | ⬆️ Best since Feb 2025 |

| Near-Term Sales Expectations | +4% | +22% | ⬇️ Caution |

| New Vendor Instructions | +1% | -1% | ➡️ Flat |

Sources: [1][2]

Supply remains fragile. New vendor instructions were broadly flat at +1%, while appraisal activity remained weaker than a year ago at -11% [2]. This supply constraint is a critical variable for valuers assessing achievable prices in any given postcode.

The North West Surge: Why Regional Divergence Demands Smarter Valuation

The most actionable intelligence from the RICS January 2026 Survey Insights: Boosting Valuation Confidence in Recovering Regional Markets lies in its regional breakdown. Price growth is strongest in Scotland and Northern Ireland, with clear upward momentum also reported across the North West and North of England [1]. Meanwhile, London, the South East, South West, and East Anglia continue to face affordability headwinds and lag behind the national average [6].

This is described as "the most pronounced regional divergence in recent memory" [6] — and it has direct consequences for how chartered surveyors approach building surveys and valuations.

Why the North West Is Outperforming 🏘️

Several structural factors explain the North West's relative strength:

- Relative affordability: Average house prices in cities like Manchester and Liverpool remain significantly below London equivalents, attracting first-time buyers and investors priced out of the South.

- Employment growth: Ongoing investment in digital, creative, and life sciences sectors in Greater Manchester has supported local income growth.

- Investor demand: Buy-to-let investors seeking higher yields have increasingly targeted Northern cities, tightening supply further.

- Infrastructure investment: Ongoing transport and regeneration projects have boosted confidence in long-term capital appreciation.

The Southern Lag: Affordability Remains the Brake

In contrast, London and the South East face a compound problem: prices remain elevated relative to local incomes, mortgage affordability is still stretched despite rate improvements, and buyer confidence has not recovered at the same pace as the North. For surveyors working in these markets — whether in Hammersmith, Richmond, or Bromley — this means valuations must be approached with particular care. Comparable evidence from even six months ago may no longer be reliable.

Surveyor Tactics for Accurate Pricing Amid Early Recovery Signs

The RICS January 2026 Survey Insights: Boosting Valuation Confidence in Recovering Regional Markets is not just a market report — it is a practical tool for calibrating valuation confidence. Here is how property professionals can translate the data into better survey outcomes in 2026.

1. Use Hyper-Local Comparable Evidence 🔍

National averages are almost meaningless in a market with this level of regional divergence. Surveyors should:

- Weight recent comparables more heavily — transactions from Q4 2025 may reflect a different market sentiment than those from Q1 2026.

- Segment by property type and tenure — flats and terraced houses are responding differently to recovery signals than detached family homes.

- Cross-reference with RICS regional data — the monthly survey provides regional net balances that can inform adjustments to comparable evidence.

For those conducting an RICS HomeBuyer Survey, incorporating current regional sentiment data into the market commentary section adds significant value for clients.

2. Adjust for Supply Constraints in the Rental Market

With tenant demand rising to +13% and new landlord instructions at -24%, near-term rent expectations have strengthened to +28% [2]. This rental market tightness has knock-on effects for residential valuations:

- Investment properties in high-demand rental areas command a premium that pure capital value comparables may understate.

- Landlord exit pressure in some markets (driven by regulatory changes) may create pockets of discounted stock — a risk that building surveys should flag explicitly.

- Void risk is lower in supply-constrained markets, which affects income capitalisation approaches.

3. Flag Near-Term vs. Long-Term Market Signals

The gap between near-term caution (+4% short-term sales expectations) and long-term optimism (+35% 12-month outlook) [1][2] creates a specific challenge for valuers: the market may be priced for recovery that has not yet fully materialised.

Practical tactics include:

- Clearly distinguishing between current market value and anticipated market direction in survey reports.

- Advising clients on the risk of over-paying in markets where recovery optimism is priced in ahead of actual transaction evidence.

- Using the RICS survey's 12-month price expectation data (+43%) as a forward-looking context note, not as a valuation input [1].

4. Identify Structural Issues That Affect Value in Recovering Markets

In a recovering market, buyers are more willing to proceed — but they are also more likely to use survey findings to negotiate price. A thorough building survey that helps negotiate property price becomes even more valuable when buyers are stretching affordability to enter the market.

Key structural issues to scrutinise closely in 2026 include:

- Damp and moisture ingress — particularly in older Northern stock where deferred maintenance has accumulated. A detailed damp survey report can quantify remediation costs and support price renegotiation.

- Roof condition — especially relevant in properties that have been on the market for extended periods during the downturn.

- Subsidence indicators — in areas with clay soils or mature tree cover, tree-related subsidence remains a persistent risk.

5. Communicate Uncertainty Clearly to Clients

The January 2026 data contains a built-in contradiction: long-term optimism sits alongside near-term caution. Surveyors must communicate this tension clearly. Clients — whether buyers or sellers — need to understand that:

- Recovery signals are directional, not definitive.

- Regional performance varies so significantly that national headlines may be irrelevant to their specific transaction.

- The fragile supply pipeline (appraisal activity at -11%) means that new stock may not arrive quickly enough to moderate price pressure in high-demand areas [2].

Understanding which home survey is right for you is a conversation that benefits from this market context — a Level 3 Building Survey may be warranted in markets where deferred maintenance has accumulated during the downturn.

The Rental Market: A Parallel Pressure Point

The rental sector deserves separate attention. The RICS January 2026 data shows a market under significant structural stress [2]:

- Tenant demand: +13% (ending two consecutive quarters of flat or negative readings)

- New landlord instructions: -24% (supply continues to shrink)

- Near-term rent expectations: +28%

This dynamic is most acute in high-demand urban areas — precisely the markets where residential valuations are most complex. For surveyors working in areas like Islington or Lewisham, the rental market context is inseparable from residential valuation work.

Key implications for surveyors:

- Rental yield calculations need to reflect rising rent expectations, not just current passing rents.

- Landlord exit valuations may be depressed by buyer caution but supported by strong rental income potential.

- HMO and multi-let properties may attract a premium in supply-constrained markets that standard comparables do not capture.

What Capital Economics Says About 2026 Recovery

Capital Economics has offered a notably optimistic interpretation of the January 2026 RICS data, suggesting that the green shoots of recovery "lend tentative support to predictions that house prices will surpass most people's expectations in 2026" [3]. This view is supported by the improving trajectory across multiple indicators — buyer enquiries, agreed sales, and price expectations all moving in the same direction simultaneously.

However, the word "tentative" is doing significant work in that sentence. The near-term sales expectation reading of just +4% (down sharply from +22%) [2] is a reminder that confidence can reverse quickly if economic conditions deteriorate. Surveyors should treat the Capital Economics view as a plausible scenario, not a certainty.

The balanced view for 2026:

- ✅ Recovery is underway — the direction of travel is clear.

- ⚠️ The pace is uneven — regional divergence is at a historic high.

- 🔍 Supply constraints will amplify price movements — both up and down.

- 📊 Valuation confidence requires hyper-local evidence, not national headlines.

Conclusion: Turning Survey Data into Valuation Confidence

The RICS January 2026 Survey Insights: Boosting Valuation Confidence in Recovering Regional Markets delivers a clear message: the UK housing market is recovering, but recovery is not evenly distributed. Scotland, Northern Ireland, and the North West are pulling ahead. London and the South East are still finding their footing. And the rental market is tightening in ways that will ripple through residential valuations for months to come.

For surveyors and property professionals, the actionable takeaways are straightforward:

- Prioritise hyper-local comparable evidence over national trend data.

- Communicate the near-term vs. long-term tension explicitly in survey reports.

- Scrutinise structural condition carefully — in a recovering market, buyers use survey findings to negotiate, and thorough reports protect all parties.

- Factor rental market dynamics into investment property valuations.

- Stay current with monthly RICS data — the market is moving fast enough that six-month-old assumptions may already be outdated.

The property market is not simply "recovering." It is recovering differently in different places, at different speeds, for different property types. The surveyors who understand that nuance — and translate it into confident, well-evidenced valuations — will be the ones their clients trust most in 2026.

References

[1] UK Resi Survey Jan 2026 Report Shows Early Signs Market Recovery Despite Caution – https://www.rics.org/news-insights/uk-resi-survey-jan-2026-report-shows-early-signs-market-recovery-despite-caution

[2] RICS Residential Market Survey January 2026 – https://www.retaileconomics.co.uk/retail-insights-trends/rics-residential-market-survey-january-2026?slug=retail-economic-news

[3] UK RICS Residential Market Survey Jan 2026 – https://www.capitaleconomics.com/publications/uk-housing-market-update/uk-rics-residential-market-survey-jan-2026

[4] Property Market Turning Corner RICS Survey Suggests – https://todaysconveyancer.co.uk/property-market-turning-corner-rics-survey-suggests/

[5] UK Residential Market Survey January 2026 – https://www.rics.org/content/dam/ricsglobal/documents/market-surveys/uk-residential-market-survey/UK-Residential-Market-Survey_January-2026.pdf

[6] Valuation Adjustments For Widening Regional Disparities RICS January 2026 Survey Insights For Surveyors – https://nottinghillsurveyors.com/blog/valuation-adjustments-for-widening-regional-disparities-rics-january-2026-survey-insights-for-surveyors

[7] Valuation Strategies Amid January 2026 RICS Residential Survey Spotting Early Market Recovery Signals – https://nottinghillsurveyors.com/blog/valuation-strategies-amid-january-2026-rics-residential-survey-spotting-early-market-recovery-signals