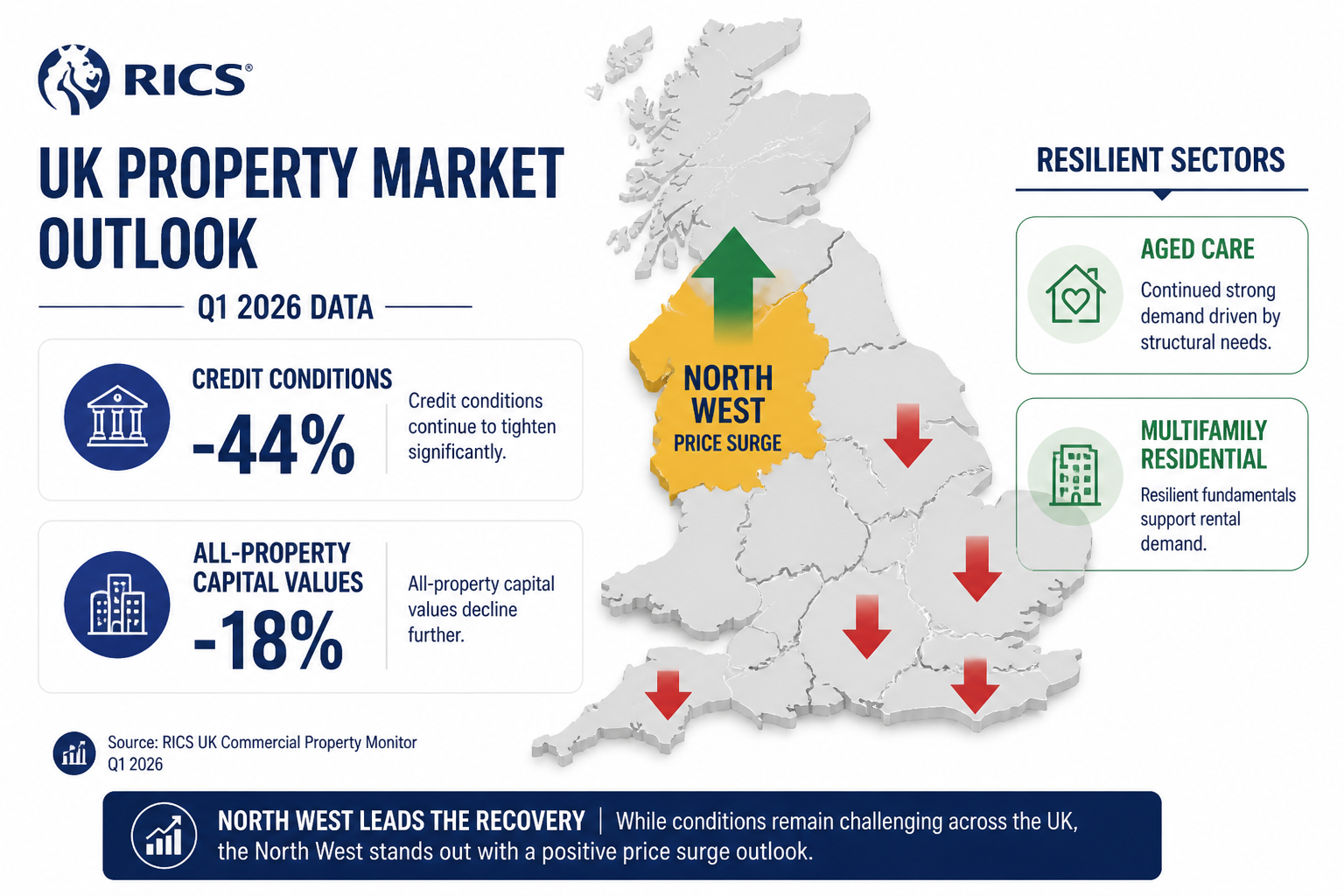

Credit conditions in UK commercial property collapsed to -44% in Q1 2026 — the weakest reading since Q3 2023 — yet surveyors working in Northern England's most active corridors are reporting something quite different on the ground. The Valuation Divergences in RICS Q1 2026 Survey: North West Surge Tactics for Surveyors Targeting Resilient Markets represent one of the most compelling strategic opportunities for property professionals in years: while London bleeds buyer confidence, Manchester, Liverpool, and their surrounding submarkets are quietly outperforming the national mood. Understanding how to leverage this divergence is now a core competency for any surveyor advising lenders, investors, or owner-occupiers seeking certainty in volatile conditions [1][3].

Key Takeaways 📌

- Credit conditions fell sharply to -44% in Q1 2026, signalling the weakest lending environment in over two years — yet regional divergences create pockets of opportunity.

- The North West is outperforming national trends, with residential and select commercial sectors showing relative resilience against a backdrop of declining all-property capital value expectations.

- London faces the steepest downward pressure at -40% net balance on buyer activity, making it the most challenging market for surveyors to deliver confident valuations.

- Aged care, multifamily residential, and life sciences are the standout growth sectors surveyors should prioritise in resilient regional markets.

- Surveyors who refine their valuation models to reflect hyper-local data — rather than relying on national averages — will deliver the lender certainty that commands premium instruction fees.

The RICS Q1 2026 Data Landscape: What the Numbers Actually Mean

The headline figures from the RICS Q1 2026 UK Commercial Property Monitor paint a sobering picture. All-property capital value expectations dropped to -18% on a 12-month outlook, down sharply from -5% in Q4 2025 [3]. That deterioration was driven by a trio of macro pressures: Middle East geopolitical tensions, rising bond yields, and persistent inflation concerns that eroded lender appetite almost overnight.

Breaking down the sector-level data reveals the true complexity:

| Sector | Q4 2025 Capital Value Forecast | Q1 2026 Capital Value Forecast | Expectation Balance |

|---|---|---|---|

| Office | +1.9% | +0.7% | -18% (from -5%) |

| Industrial | +2.0% | +1.2% | -8% (from +9%) |

| Retail | +0.5% | -0.7% | -30% (from -21%) |

| All Property | Positive | -18% outlook | Sharply negative |

Source: RICS UK Commercial Property Monitor Q1 2026 [3]

The retail sector's reversal is particularly notable. A sector that appeared to be stabilising — with +0.5% growth projected just one quarter ago — is now expected to contract by -0.7% in capital values [3]. For surveyors producing Red Book valuations for retail assets, this is not academic. It directly affects the figures placed in front of lenders.

"27% of surveyor respondents now view the commercial property market as being in an early downturn phase — up from just 17% in Q4 2025." [3]

That 10-percentage-point shift in sentiment within a single quarter is a signal that cannot be ignored. When more than one in four RICS professionals believe a downturn has begun, valuation methodology must adapt accordingly.

Residential Market Signals: February 2026

On the residential side, agreed sales posted a net balance of -12% in February 2026, marginally weaker than the -9% recorded the previous month [2]. New buyer enquiries fell substantially in March 2026, with rising borrowing costs and geopolitical uncertainty suppressing confidence across most of England and Wales [1].

Crucially, new instructions held at a +2% net balance, meaning fresh supply continues to enter the market even as demand softens [2]. This supply-demand imbalance creates downward pressure on prices in already-fragile markets — but it also creates negotiating leverage for buyers with survey-backed evidence. Understanding how an RICS survey can help negotiate the price of a property has never been more commercially relevant than in 2026.

Valuation Divergences in RICS Q1 2026 Survey: North West Surge Tactics for Surveyors Targeting Resilient Markets

The most actionable insight buried within the Q1 2026 data is the stark regional divergence between London and the North West. While London is experiencing the strongest downward pressure at -40% net balance on buyer activity [2] — a figure that represents a genuine structural challenge for surveyors working in the capital — Northern England tells a different story.

Why the North West Is Outperforming

Several structural factors explain the North West's relative resilience:

- 🏗️ Lower base valuations mean price corrections are less severe in absolute terms

- 🏥 Strong demand in aged care, life sciences, and multifamily residential — three sectors RICS has specifically identified as expected to deliver modest growth despite broader headwinds [1]

- 🏘️ Rental demand remains elevated in Greater Manchester and Merseyside, supporting income-based valuations even where capital growth stalls

- 🔬 Life sciences and innovation districts (MediaCityUK, Manchester Science Park, Liverpool Knowledge Quarter) continue attracting institutional capital

- 🏦 Lender appetite for North West residential remains comparatively stronger than for London prime, where affordability ratios are at historic extremes

For surveyors, this divergence is not merely interesting — it is commercially significant. Lenders instructing valuations on North West assets need surveyors who can demonstrate genuine local market knowledge, not professionals applying a nationally-derived template.

Tactical Approaches for Surveyors in Resilient Markets

The following tactics are directly applicable for RICS-qualified surveyors targeting North West instructions in 2026:

1. Build Hyper-Local Comparable Databases 📊

National average data is actively misleading in a divergent market. Surveyors should maintain rolling 90-day comparable transaction logs at postcode level — not just local authority level — for the specific asset classes they advise on.

2. Sector-Specific Valuation Overlays

Given that aged care, multifamily residential, and life sciences are the identified growth sectors [1], surveyors should develop sector-specific yield matrices that reflect the different risk profiles of these assets versus mainstream commercial property. A logistics unit in Warrington requires a fundamentally different approach than a retail parade in Wigan.

3. Lender Communication Protocols

With credit conditions at -44% [3], lenders are under pressure to justify every instruction. Surveyors who proactively provide market commentary sections within their reports — contextualising the Q1 2026 data against local evidence — are delivering a service that commands repeat instructions.

4. Red Book Compliance in Volatile Conditions

When markets move quickly, the date of inspection and the date of report can diverge in ways that affect material accuracy. Surveyors should review their Red Book valuation processes and ensure that market movement caveats are appropriately worded for Q1 2026 conditions.

5. Survey Level Selection Guidance

Buyers in resilient North West markets are increasingly sophisticated. Helping clients understand the difference between Level 2 and Level 3 surveys — and recommending the appropriate level for older Victorian stock common in cities like Liverpool and Salford — builds trust and reduces post-survey disputes.

Sector Breakdown: Where Surveyors Should Focus Attention in 2026

Understanding the Valuation Divergences in RICS Q1 2026 Survey: North West Surge Tactics for Surveyors Targeting Resilient Markets requires a granular view of which asset classes are genuinely holding value and which are experiencing structural repricing.

🏭 Industrial: Cautiously Resilient

Industrial remains the most defensible commercial sector despite growth projections falling to 1.2% from 2.0% [3]. Capital value expectations sit at -8% — negative, but significantly better than retail's -30% [3]. For North West surveyors, the logistics and distribution corridor along the M62 and M6 represents the most active industrial market in England outside the Golden Triangle.

Key tactic: When valuing industrial assets, emphasise passing rent versus estimated rental value (ERV) differentials. In a market where capital values are under pressure, income security becomes the primary valuation driver for lenders.

🏢 Office: Selective Opportunity

Office capital values are now expected to grow only 0.7% annually [3], down from 1.9% projected just one quarter ago. However, this national figure masks significant sub-market variation. Grade A, ESG-compliant office space in Manchester city centre continues to attract occupier demand from financial services and tech firms relocating from London.

Key tactic: Apply a clear quality bifurcation in office valuations. Grade A versus Grade B/C is not a stylistic distinction — it is a material valuation differential in 2026 conditions.

🛒 Retail: Proceed With Caution

Retail's reversal to -0.7% capital value decline [3] — from a position of modest expected growth — demands caution. Surveyors should be particularly careful with retail valuations in secondary locations. The -30% expectation balance [3] reflects genuine structural uncertainty about long-term occupier demand.

Key tactic: For retail valuations, surveyors should document footfall data, void rates, and lease expiry profiles as supporting evidence. Lenders will scrutinise retail valuations more heavily than any other sector in 2026.

🏥 Aged Care, Multifamily & Life Sciences: The Growth Pockets

These three sectors are explicitly identified as expected to deliver modest growth despite broader market headwinds [1]. For North West surveyors, this creates a clear strategic priority:

- Aged care: Demographic demand is structurally underpinned; valuation methodology should incorporate operational trading performance alongside property fundamentals

- Multifamily residential (Build to Rent): Manchester and Liverpool are among the UK's most active BTR markets; surveyors should develop expertise in income capitalisation approaches specific to this asset class

- Life sciences: Specialist assets require specialist valuation skills; surveyors targeting this sector should pursue relevant CPD and consider why choosing RICS-qualified surveyors matters to institutional clients in this space

Practical Implications for Surveyors Advising Buyers and Lenders

The valuation divergences documented in Q1 2026 have direct practical implications beyond the commercial sector. Residential surveyors are operating in a market where buyer enquiries are falling, agreed sales are declining, and London faces the sharpest correction [2] — yet North West residential markets are showing comparative stability.

Helping Buyers Navigate the Divergence

For residential surveyors, the current environment demands clear communication about what survey findings mean in a softening market. Buyers who receive a survey highlighting defects now have genuine negotiating leverage in a way they did not in 2021-2023. Understanding how to renegotiate after a poor building survey result is a conversation surveyors should be prepared to have proactively.

Similarly, first-time buyers — who are disproportionately active in North West markets due to relative affordability — benefit enormously from professional guidance. Pointing clients toward resources on booking a building survey as a first-time buyer helps set expectations and reduces transaction fall-throughs.

Choosing the Right Survey for the Right Asset

In a market characterised by divergence, the type of survey matters as much as the surveyor conducting it. Older terraced housing stock in North West cities — much of it Victorian or Edwardian — frequently conceals structural issues, damp, and timber decay that a basic valuation will not capture. Helping clients understand which home survey is right for their property is a professional duty, not an upselling exercise.

For commercial clients, monitoring surveys are increasingly relevant where assets are under development or where structural movement is a concern — particularly in areas of the North West with historic mining activity or clay subsoils.

The Price Negotiation Opportunity

The data is unambiguous: with agreed sales at -12% net balance [2] and buyer enquiries falling, sellers are under more pressure than at any point in recent years. Surveyors who can quantify defect remediation costs with precision — and communicate those figures clearly — are enabling buyers to achieve meaningful average price reductions after survey. In a market where every percentage point of purchase price matters, this is a tangible financial service.

Conclusion: Turning Divergence Into Strategic Advantage

The Valuation Divergences in RICS Q1 2026 Survey: North West Surge Tactics for Surveyors Targeting Resilient Markets are not a temporary anomaly — they reflect deep structural differences in affordability, demographics, and economic diversification between Northern England and the capital. Surveyors who treat these divergences as background noise will produce valuations that fail lenders and clients alike. Those who lean into the regional data, build genuine local expertise, and communicate market context with precision will be the professionals sought out when certainty matters most.

✅ Actionable Next Steps for Surveyors

- Audit your comparable database — ensure it reflects Q1 2026 transaction data at postcode level, not local authority averages

- Review your market commentary templates — generic caveats are insufficient; lenders need Q1 2026-specific context

- Identify your sector focus — aged care, multifamily, and life sciences are the growth pockets; develop CPD and methodology accordingly

- Upskill on survey level guidance — clients in resilient North West markets deserve clear advice on the right survey product for their asset

- Monitor RICS survey releases quarterly — the divergence between regions is likely to widen before it narrows; staying current is a professional obligation

The surveyors who thrive in 2026 will not be those who wait for national conditions to improve. They will be the professionals who understand that the map of UK property value is being redrawn — and who position themselves at the most active points on that map.

References

[1] RICS UK Commercial Property Monitor Q1 2026 – https://www.rics.org/news-insights/rics-uk-commercial-property-monitor-q1-2026

[2] UK Residential Market Survey February 2026 – https://www.rics.org/content/dam/ricsglobal/documents/market-surveys/uk-residential-market-survey/UK-Residential-Market-Survey_February-2026.pdf

[3] Q1 2026 RICS UK Commercial Property Monitor – https://www.rics.org/content/dam/ricsglobal/documents/market-surveys/Q1-2026_RICS-UK-Commercial-Property-Monitor.pdf

[4] Regional Valuation Divergences in 2026 Recovery: RICS Tactics for North-South Price Shifts in Building Surveys – https://nottinghillsurveyors.com/blog/regional-valuation-divergences-in-2026-recovery-rics-tactics-for-north-south-price-shifts-in-building-surveys