The February 2026 RICS Residential Market Survey reveals a stark reality: buyer enquiries plummeted to a net balance of -26%, marking a sharp deterioration from January's -15% and signaling renewed market weakness just as confidence appeared to stabilize. This dramatic shift in Valuation Adjustments from February 2026 RICS Survey: Countering Geopolitical Caution in Buyer Enquiries and Price Expectations reflects how rapidly geopolitical uncertainty can reshape property market dynamics, forcing surveyors and valuers to recalibrate their assessment methodologies amid unprecedented regional divergence and sentiment volatility.[1][2]

The data paints a complex picture where London's price expectations collapsed by 49 percentage points in a single month, while headline national prices remained broadly flat at -12%.[2] For property professionals navigating these turbulent waters, understanding the nuanced valuation adjustments required to counter geopolitical caution has become essential to delivering accurate, defensible property assessments.

Key Takeaways

- 🔻 Buyer enquiries declined sharply to -26% in February, down from -15% in January, representing the most significant deterioration in demand momentum this year

- 🌍 Geopolitical tensions directly impacted market sentiment, with Middle East escalation and macroeconomic concerns tempering activity that had shown early-year promise

- 📍 Regional divergence reached extreme levels, with London posting -40% price pressure while Northern Ireland, Scotland, and North West England maintained firmer trends

- ⏰ Near-term price expectations turned significantly more cautious at -18%, contrasting with resilient 12-month outlooks of +33% expecting modest price increases

- 🏠 Rental market dynamics strengthened, with landlord supply constraints driving +20% rent inflation expectations despite stable tenant demand

Understanding the February 2026 Market Deterioration

The Sharp Decline in Buyer Demand

The February 2026 RICS data reveals a concerning reversal in buyer sentiment. After what appeared to be a stabilizing start to the year, new buyer enquiries posted a net balance of -26%, representing a significant 11-percentage-point decline from January's already-subdued -15%.[1] This deterioration suggests that external factors—particularly geopolitical uncertainty—are exerting stronger influence on purchasing decisions than previously anticipated.

For chartered surveyors conducting property valuations, this shift demands immediate methodological adjustments. When buyer demand weakens so rapidly, comparable evidence becomes less reliable, and valuation confidence intervals must widen to reflect increased market uncertainty.

Key demand indicators from February 2026:

| Metric | February 2026 | January 2026 | Change |

|---|---|---|---|

| New Buyer Enquiries | -26% | -15% | ↓ 11pp |

| Agreed Sales | -12% | N/A | Subdued |

| Near-term Sales Expectations | -2% | N/A | Hesitant |

Geopolitical Factors Driving Market Caution

The heightened uncertainty in the Middle East combined with broader macroeconomic concerns has created a perfect storm of buyer hesitancy.[2] Unlike domestic policy changes that markets can typically price in, geopolitical escalation introduces unpredictable volatility that fundamentally alters risk assessments.

This geopolitical caution manifests in several ways:

- Extended decision-making timelines as buyers wait for clarity

- Increased price sensitivity and negotiation leverage for purchasers

- Higher survey instruction rates as buyers seek professional risk assessment

- Greater emphasis on condition over aspirational features

When conducting homebuyers reports, surveyors must now consider how geopolitical uncertainty affects both current market value and future marketability—particularly for properties in higher price brackets where discretionary purchasing dominates.

Valuation Adjustments from February 2026 RICS Survey: Regional Divergence and Price Pressure

Extreme Geographic Variation in Market Performance

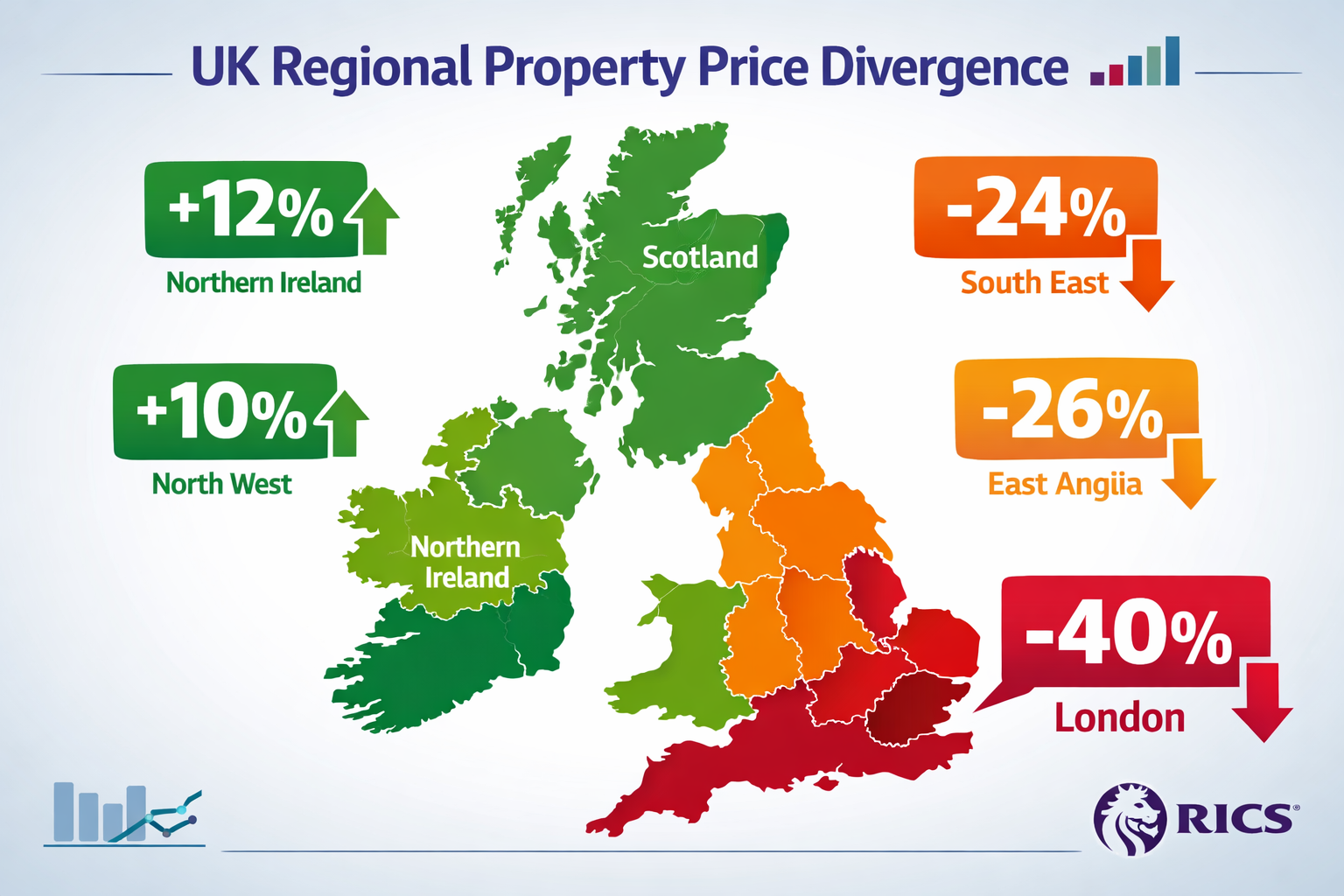

Perhaps the most striking feature of the Valuation Adjustments from February 2026 RICS Survey: Countering Geopolitical Caution in Buyer Enquiries and Price Expectations is the unprecedented regional divergence in price trends. While the national headline figure shows prices broadly flat at -12%, this masks dramatic variations across UK regions.[1]

Regional price pressure breakdown:

- London: -40% (most severe downward pressure)

- South East: -24% (significant weakness)

- East Anglia: -26% (substantial decline)

- Northern Ireland: Positive trend (firmer pricing)

- Scotland: Positive trend (resilient market)

- North West England: Positive trend (continued strength)

This geographic disparity requires property surveyors to abandon one-size-fits-all valuation approaches. A methodology appropriate for assessing a Manchester property would produce misleading results if applied to a comparable London home without substantial adjustments.

London's Dramatic Expectation Revision

The capital experienced the most dramatic shift in sentiment, with 12-month price expectations falling from +56% in January to just +7% in February—a staggering 49-percentage-point decline in a single month.[2] This revision reflects several converging factors:

✅ Affordability constraints reaching critical levels

✅ International buyer caution amid geopolitical uncertainty

✅ Stamp duty considerations affecting transaction volumes

✅ Economic concentration risk in financial services sectors

For surveyors conducting property evaluations in London, this expectation shift necessitates more conservative comparable selection, increased scrutiny of time adjustments, and explicit consideration of downside risk scenarios in valuation reporting.

Valuation Methodology Adjustments for Regional Divergence

When Valuation Adjustments from February 2026 RICS Survey: Countering Geopolitical Caution in Buyer Enquiries and Price Expectations reveal such extreme regional variation, surveyors must implement several tactical adjustments:

1. Tighter Comparable Time Windows

In rapidly changing markets like London, comparables older than 8-12 weeks may no longer reflect current market conditions. Restrict comparable evidence to the most recent transactions and adjust aggressively for time.

2. Increased Weight on Current Listings

When agreed sales data lags market sentiment, current asking prices and recent price reductions provide valuable forward-looking indicators. Cross-reference sold prices with active listing trends.

3. Explicit Uncertainty Disclosure

Professional building surveyor services should include clear statements about valuation confidence levels and the potential impact of continued market deterioration on assessed values.

4. Micro-Location Premium Reassessment

In declining markets, location premiums often compress faster than overall market values. Reassess the differential between prime and secondary locations within the same broader area.

Tactical Surveyor Strategies for Accurate Valuations Amid Uncertainty

Balancing Short-Term Caution with Long-Term Resilience

The February 2026 data presents a fascinating dichotomy: while near-term price expectations turned significantly more cautious at -18% (down from -6% in January), 12-month expectations remained broadly positive at +33%.[1][2] This suggests surveyors must distinguish between temporary sentiment-driven weakness and fundamental value deterioration.

When preparing Level 2 surveys or more comprehensive assessments, consider implementing a dual-timeframe valuation commentary:

Short-term (0-6 months): Reflect current market weakness, reduced buyer competition, and geopolitical uncertainty in the primary valuation figure.

Medium-term (6-18 months): Provide contextual commentary on expected market normalization, assuming geopolitical tensions stabilize and macroeconomic fundamentals improve.

This approach acknowledges current market reality while avoiding excessive pessimism that could undervalue properties with strong fundamental characteristics.

Enhanced Due Diligence for Condition Assessment

In markets characterized by reduced buyer demand and price pressure, purchasers become significantly more condition-sensitive. Properties with deferred maintenance or material defects face disproportionate marketability challenges compared to well-maintained alternatives.

Structural survey importance increases substantially in such environments. Surveyors should:

- Expand defect documentation beyond minimum reporting standards

- Quantify remediation costs with greater precision and cost buffer

- Assess impact on marketability explicitly in valuation commentary

- Consider specialist surveys for specific concerns like damp issues

When buyer enquiries decline by 26%, the pool of potential purchasers willing to overlook property defects shrinks dramatically. Valuation adjustments must reflect this reduced market depth.

Incorporating Geopolitical Risk into Valuation Frameworks

Traditional valuation methodologies rarely explicitly account for geopolitical risk, yet the February 2026 data demonstrates its tangible market impact. Surveyors can integrate this consideration through several mechanisms:

Risk-Adjusted Comparable Selection

Prioritize comparable evidence from periods of similar uncertainty or market stress. If current geopolitical tensions resemble conditions from previous periods, those historical comparables may provide better guidance than more recent transactions conducted under calmer conditions.

Scenario-Based Valuation Ranges

Rather than single-point valuations, consider providing a range reflecting different geopolitical resolution scenarios:

- Optimistic scenario: Rapid tension de-escalation, buyer confidence returns

- Base case: Prolonged uncertainty, gradual market normalization

- Pessimistic scenario: Escalation continues, further demand deterioration

Explicit Assumption Documentation

Clearly state the geopolitical assumptions underpinning the valuation. This protects both surveyor and client by establishing the conditional nature of the assessment and the factors that could materially alter the conclusion.

Leveraging RICS Data for Comparative Context

The Valuation Adjustments from February 2026 RICS Survey: Countering Geopolitical Caution in Buyer Enquiries and Price Expectations provide invaluable benchmarking data for individual property assessments. When conducting property inspections, reference RICS regional data to contextualize local market observations.

Practical applications include:

📊 Validating local agent intelligence against RICS regional trends

📊 Identifying outlier properties that buck broader market trends

📊 Supporting valuation adjustments with authoritative survey data

📊 Educating clients about market context beyond their specific property

For example, if valuing a property in East Anglia where RICS reports -26% price pressure, but local agents claim strong demand, the discrepancy warrants investigation and explicit commentary in the valuation report.

The Rental Market Dynamic: A Contrasting Picture

Stable Demand Meets Constrained Supply

While the sales market deteriorated in February 2026, the rental sector presents a markedly different picture. Tenant demand remained broadly stable with a net balance of +2% over the three months to February, indicating steady if unspectacular demand.[1][2]

However, the supply side tells a more dramatic story. Landlord instructions posted a firmly negative net balance of -27%, signaling an ongoing shortage of rental stock and limited new listings coming to market.[1][2] This supply-demand imbalance has predictable consequences for rental pricing.

Rental market indicators:

| Metric | February 2026 | Trend |

|---|---|---|

| Tenant Demand (3-month) | +2% | Stable |

| Landlord Instructions | -27% | Severe shortage |

| Rent Inflation Expectations (3-month) | +20% | Strong upward pressure |

Implications for Property Investment Valuations

For surveyors assessing investment properties or conducting real estate appraisals for portfolio purposes, this rental market dynamic creates complex valuation considerations:

Yield Compression Risk

As capital values face downward pressure while rental income expectations strengthen, gross yields appear to improve. However, this may prove temporary if capital values stabilize while rental growth moderates.

Tenant Quality Considerations

In tight rental markets, landlords gain pricing power but may face pressure to accept marginal tenants. Assess the sustainability of rental income projections based on local tenant profile and affordability.

Regulatory Headwinds

The -27% landlord instruction figure partly reflects regulatory burden concerns. Factor ongoing and potential future regulatory changes into long-term investment value assessments.

Alternative Use Potential

Properties currently let but facing capital value pressure may warrant consideration of alternative use or disposal strategies. Investment valuations should acknowledge this optionality.

Practical Recommendations for Surveyors and Property Professionals

Immediate Tactical Adjustments

Based on the Valuation Adjustments from February 2026 RICS Survey: Countering Geopolitical Caution in Buyer Enquiries and Price Expectations, property professionals should implement these immediate adjustments:

1. Revise Comparable Databases 🔄

Update comparable evidence databases to reflect February's market shift. Clearly flag comparables agreed before the recent deterioration and apply appropriate time adjustments.

2. Enhance Client Communication 💬

Proactively contact clients with pending instructions to discuss market changes and potential implications for their specific properties. Reference RICS data to provide authoritative context.

3. Adjust Inspection Priorities 🔍

Given increased buyer condition sensitivity, allocate additional inspection time to defect identification and documentation. Consider recommending specific defect surveys where appropriate.

4. Review Fee Structures 💰

The increased complexity and risk associated with valuations in uncertain markets may justify fee adjustments. Ensure fees reflect the additional due diligence required.

5. Document Methodology Changes 📝

Maintain clear internal documentation of methodology adjustments made in response to market changes. This supports consistency across valuations and provides audit trail for professional standards compliance.

Strategic Positioning for Market Recovery

While near-term indicators show weakness, the resilient 12-month outlook of +33% expecting price increases suggests surveyors should position for eventual recovery:[1][2]

✨ Maintain market monitoring discipline through regular RICS survey review

✨ Build regional expertise to capitalize on divergent market performance

✨ Develop geopolitical risk assessment frameworks for future uncertainty

✨ Strengthen relationships with clients navigating challenging markets

✨ Invest in continuing professional development on valuation in uncertain markets

Client Advisory Opportunities

The current market environment creates valuable advisory opportunities beyond traditional survey work. Consider offering:

Market Timing Guidance

Help clients understand whether current conditions favor buying, selling, or waiting. The contrast between near-term weakness (-18% expectations) and medium-term optimism (+33% expectations) suggests timing decisions carry unusual significance.[1][2]

Portfolio Strategy Reviews

For clients with multiple properties or investment portfolios, the extreme regional divergence creates rebalancing opportunities. London weakness may favor selective disposals, while Northern resilience might justify acquisitions.

Risk Mitigation Planning

Assist clients in understanding and mitigating geopolitical and market risks through property selection, diversification, and contractual protections.

Navigating Different Property Types and Price Segments

Prime vs. Secondary Market Divergence

The -26% decline in buyer enquiries affects different market segments unevenly.[1] Prime properties in desirable locations with strong fundamental characteristics typically demonstrate greater resilience than secondary stock.

When conducting building surveys, explicitly consider market segment positioning:

Prime segment characteristics:

- Limited supply, strong location fundamentals

- Less price-sensitive buyer pool

- Greater resilience to short-term uncertainty

- Faster recovery potential

Secondary segment characteristics:

- More abundant supply, location compromises

- Highly price-sensitive buyers

- Disproportionate impact from demand weakness

- Slower recovery trajectory

Valuation adjustments should reflect these segment-specific dynamics rather than applying uniform market-wide corrections.

New Build vs. Resale Considerations

New build properties face distinct challenges in the current environment. Developer pricing often lags market sentiment changes, creating potential overvaluation risk. Additionally, new builds typically attract first-time buyers and chain-free purchasers—segments particularly sensitive to affordability and economic uncertainty.

When valuing new build properties, consider:

- Incentive erosion as developers defend headline prices

- Comparable selection challenges given limited resale evidence

- Completion risk in uncertain markets

- Premium sustainability as resale alternatives become more competitive

Regional Deep Dive: Tactical Approaches by Geography

London and South East Strategy

With London posting -40% price pressure and expectations falling 49 percentage points,[2] surveyors operating in the capital must adopt particularly conservative approaches:

- Apply aggressive time adjustments (minimum 1-2% monthly in declining areas)

- Weight recent price reductions heavily in comparable analysis

- Consider micro-location flight to quality within London boroughs

- Explicitly address international buyer withdrawal in market commentary

For properties in the South East facing -24% pressure, similar but slightly less aggressive adjustments apply, with particular attention to commuter belt dynamics and London employment dependency.

Northern Regions and Scotland Approach

Markets showing resilient or positive trends require different tactical considerations. In Northern Ireland, Scotland, and the North West, where prices remain firmer:

- Maintain standard comparable timeframes without aggressive discounting

- Focus on supply constraints supporting price stability

- Consider relative value migration from southern markets

- Monitor affordability advantages attracting relocating buyers

However, remain alert to contagion risk—if national sentiment continues deteriorating, currently resilient regions may eventually follow.

East Anglia and Regional Outliers

East Anglia's -26% pressure despite historically strong market fundamentals illustrates how geopolitical uncertainty can override local factors.[1] For such regions:

- Investigate specific local drivers beyond national trends

- Assess whether weakness represents temporary sentiment or fundamental shift

- Consider London proximity effects and commuter pattern changes

- Evaluate second home market dynamics if relevant

Conclusion: Adapting Valuation Practice to Market Reality

The Valuation Adjustments from February 2026 RICS Survey: Countering Geopolitical Caution in Buyer Enquiries and Price Expectations demand immediate and substantive changes to surveying practice. The sharp deterioration in buyer enquiries to -26%, combined with extreme regional divergence and geopolitical uncertainty, creates a valuation environment requiring enhanced methodology, explicit risk acknowledgment, and sophisticated market analysis.[1][2]

Surveyors must balance the near-term caution reflected in -18% price expectations with the more optimistic 12-month outlook of +33%, recognizing that current market weakness may prove temporary while avoiding complacency about genuine risks.[1][2] The dramatic 49-percentage-point collapse in London expectations demonstrates how rapidly sentiment can shift, demanding agile response from property professionals.[2]

Actionable next steps for property professionals:

🎯 Update valuation methodologies to reflect February market deterioration

🎯 Implement regional-specific approaches acknowledging extreme geographic divergence

🎯 Enhance geopolitical risk assessment frameworks and documentation

🎯 Strengthen client communication about market uncertainty and valuation confidence

🎯 Monitor RICS monthly data for early indicators of recovery or further deterioration

🎯 Consider specialist surveys like damp assessments as buyer condition sensitivity increases

🎯 Develop scenario-based valuation capabilities for uncertain environments

For property buyers, sellers, and investors navigating this challenging market, engaging experienced chartered surveyors who understand these nuanced adjustments has never been more critical. The difference between accurate, defensible valuations and misleading assessments could mean tens of thousands of pounds in transaction outcomes.

The February 2026 RICS data serves as both warning and opportunity—warning of genuine market challenges requiring professional adaptation, but also opportunity for skilled surveyors to demonstrate value through sophisticated analysis during complex market conditions. Those who master the Valuation Adjustments from February 2026 RICS Survey: Countering Geopolitical Caution in Buyer Enquiries and Price Expectations will be best positioned to serve clients effectively and maintain professional standards through market uncertainty.

References

[1] Uk Residential Survey February 2026 – https://www.rics.org/news-insights/uk-residential-survey-february-2026

[2] Uk Residential Market Survey February 2026 – https://www.rics.org/content/dam/ricsglobal/documents/market-surveys/uk-residential-market-survey/UK-Residential-Market-Survey_February-2026.pdf

[3] Valuation Adjustments For Stabilising Southern Markets Rics Tactics From January 2026 Survey Improvements – https://nottinghillsurveyors.com/blog/valuation-adjustments-for-stabilising-southern-markets-rics-tactics-from-january-2026-survey-improvements