The UK property market is showing its first tentative signs of recovery in early 2026, and for valuation surveyors, this presents both opportunities and challenges. Valuing flats in early 2026 recovery signals requires a nuanced understanding of shifting market dynamics, particularly in lower-priced segments where affordability improvements are creating fresh demand. According to the latest RICS residential market survey, house prices have stabilized nationally, with the net balance improving from -19% in October 2025 to -10% by January 2026[1]. This easing of downward pressure signals that the market may be turning a corner, though regional variations remain stark.

For property professionals, understanding how to accurately value flats during this transitional period is essential. The RICS has been adapting its valuation methodologies to account for these early recovery signals, particularly in markets where lower-priced properties are beginning to attract renewed buyer interest. This shift represents a significant change from the cautious pessimism that dominated 2025.

Key Takeaways

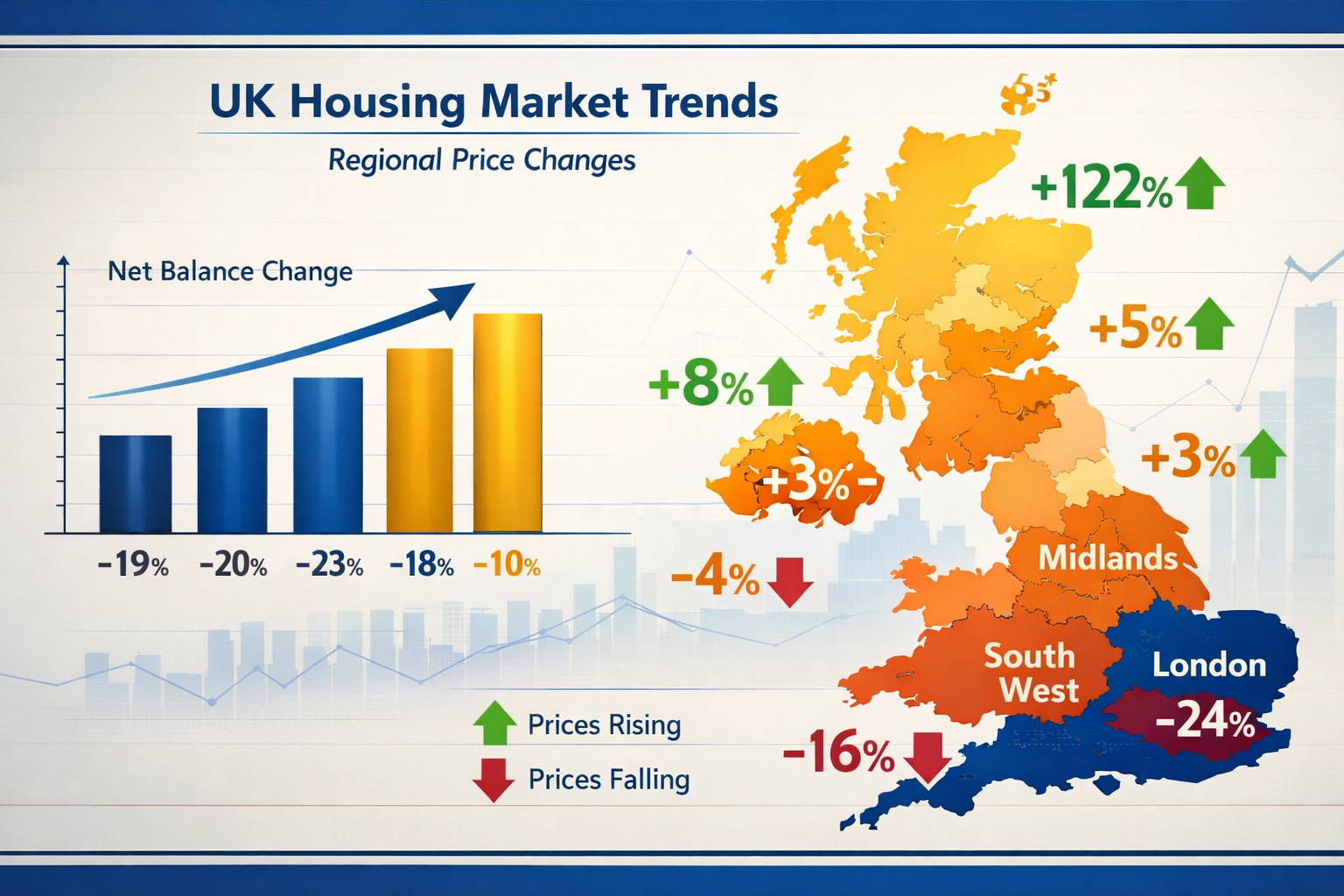

- 📊 National price stabilization: The net balance for house prices improved to -10% in early 2026, signaling reduced downward pressure after months of decline

- 🏘️ Regional divergence intensifies: While Scotland and Northern Ireland show price growth, London (-40%) and the South East (-24%) continue experiencing strong downward pressure

- 🔍 Valuation adjustments required: RICS surveyors are adapting methodologies to account for improving buyer enquiries (+15% net balance) and stabilizing sales activity

- 💷 Lower-priced market opportunities: First-time buyers are finding improved affordability, creating valuation challenges in segments that were previously stagnant

- 📈 Cautious optimism prevails: Twelve-month sales outlook reached +35% in January before moderating to +17% in February, reflecting both hope and uncertainty[1][3]

Understanding the Early 2026 Market Recovery Context

The Shift from Decline to Stabilization

The UK property market entered 2026 carrying the weight of significant challenges from the previous year. However, early 2026 recovery signals are now evident across multiple metrics. The improvement in the net balance for prices over the past three months—from -19% in October 2025 to -10% by January 2026—represents more than just statistical noise[1]. This shift indicates that the intense downward pressure on property values is beginning to ease.

For valuation professionals, this transitional period requires careful consideration. Properties that were valued six months ago may now need reassessment, particularly in segments where buyer sentiment has improved. The RICS property valuations process must now account for these emerging positive signals while remaining grounded in actual transaction data.

Regional Market Disparities

One of the most striking features of the early 2026 market is the significant regional divergence in performance. While headline figures suggest national stabilization, the reality varies dramatically by location:

| Region | Net Balance | Market Condition |

|---|---|---|

| London | -40% | Strong downward pressure |

| South East | -24% | Continued decline |

| East Anglia | -26% | Persistent weakness |

| Scotland | Positive | Price growth |

| Northern Ireland | Positive | Upward trends |

| North West | Improving | Emerging growth |

This regional variation creates specific challenges when valuing flats in early 2026 recovery signals, as surveyors must apply location-specific adjustments rather than relying on national trends[3]. Properties in Scotland and Northern Ireland may warrant more optimistic valuations, while southern markets require continued caution.

Buyer Demand and Sales Activity Trends

The improvement in new buyer enquiries provides one of the clearest early recovery signals. The net balance rose to -15% in January 2026, up from -21% in December 2025 and -29% in November 2025[1]. This steady improvement suggests that potential buyers are returning to the market, though demand remains below historical averages.

Agreed sales posted a net balance of -9% in January—the least negative reading since June 2025. However, this dipped to -12% by February as concerns over interest rates resurfaced[1][2]. For valuation surveyors, these fluctuations highlight the importance of using the most current data when assessing market conditions.

Understanding what to do before an RICS home survey becomes particularly important during transitional market periods, as both buyers and sellers need accurate valuations to make informed decisions.

RICS Valuation Adjustments for Improving Lower-Priced Markets

Adapting Methodologies for Market Transitions

Valuing flats in early 2026 recovery signals requires RICS surveyors to adapt their methodologies to account for changing market dynamics. Traditional comparative methods remain foundational, but additional adjustments are necessary when markets are in transition from decline to potential growth.

The RICS Red Book standards continue to provide the framework for professional valuations, but surveyors must exercise enhanced judgment when selecting comparable properties. In improving markets, recent sales may not fully reflect current buyer sentiment, while older comparables may overstate the degree of price decline.

Key adjustments include:

- ✅ Time-based weighting: Recent comparables receive greater emphasis, with careful consideration of transaction dates

- ✅ Market sentiment factors: Integration of forward-looking indicators like buyer enquiry levels

- ✅ Regional calibration: Application of location-specific adjustments based on local market conditions

- ✅ Property type differentiation: Recognition that lower-priced flats may be recovering faster than premium segments

When conducting RICS homebuyer surveys, valuers must clearly communicate the basis of their valuation and any assumptions made about market direction.

Addressing Affordability-Driven Demand

One of the most significant factors driving the early 2026 recovery in lower-priced markets is improved affordability. After years of price stagnation or decline, entry-level flats are becoming accessible to first-time buyers who were previously priced out of the market[5].

This affordability improvement creates specific valuation challenges:

- Pent-up demand: Properties that struggled to sell in 2024-2025 may now attract multiple interested buyers

- Price floor effects: Lower-priced flats may have reached natural price floors where value cannot decline further without triggering demand

- Buyer profile shifts: First-time buyers entering the market bring different priorities and price sensitivities than previous buyer cohorts

Surveyors must balance these emerging positive factors against the reality that 43% of respondents anticipated higher prices over the year ahead in January, though this optimism moderated by February[1]. Understanding how an RICS survey can help negotiate property prices becomes particularly valuable in these transitional conditions.

Supply Pipeline Considerations

The supply of properties coming to market plays a crucial role in valuation during recovery periods. New instructions for property listings remained in neutral territory at a net balance of +2% in February, indicating a broadly stable flow of fresh listings[2].

For lower-priced flats specifically, this stable supply environment is significant. Unlike previous recovery periods where supply constraints drove rapid price increases, the current market shows more balanced supply-demand dynamics. This suggests that any price recovery will be gradual rather than explosive.

Valuation surveyors must consider:

- Inventory levels: How many similar properties are currently available in the local market

- Time on market trends: Whether properties are selling faster or slower than in previous months

- Listing price adjustments: How often sellers are reducing asking prices to achieve sales

- Completion rates: The proportion of agreed sales that successfully complete

These supply-side factors help surveyors determine whether observed price improvements represent genuine market recovery or temporary fluctuations.

Leasehold-Specific Considerations

Many lower-priced flats in the UK are leasehold properties, which introduces additional complexity when valuing flats in early 2026 recovery signals. Lease length, ground rent obligations, and service charge levels all impact value, and these factors may be weighted differently during market recovery periods.

Properties with short leases may see particular valuation challenges during recovery, as lenders often have strict requirements about remaining lease terms. Surveyors must carefully assess whether improvements in the broader market translate to leasehold properties with complications.

Key leasehold valuation adjustments include:

- 🏢 Remaining lease term: Properties with less than 80 years remaining require marriage value calculations

- 💰 Ground rent levels: Onerous ground rents may limit buyer pool despite general market improvement

- 🔧 Service charge history: Well-managed buildings with stable charges may command premiums

- 📋 Building condition: Shared responsibility for maintenance creates additional valuation considerations

Understanding what to check before buying a leasehold property helps both valuers and buyers navigate these complexities.

Forward-Looking Sentiment and Long-Term Valuation Implications

Interpreting Market Confidence Indicators

The twelve-month sales outlook provides crucial insight into market sentiment. This metric surged to +35% in January 2026—the strongest reading since December 2024—before declining to +17% by February as geopolitical uncertainty and interest rate concerns resurfaced[1][3].

For valuation professionals, these sentiment indicators serve as leading indicators of potential price movements. When market participants expect increased sales activity, this typically precedes price stabilization or growth. However, the February decline highlights the fragility of current confidence.

Near-term sales expectations softened to -2% by February, reflecting little immediate momentum despite longer-term optimism[3]. This divergence between short-term caution and long-term hope characterizes the current market environment and must be reflected in valuation approaches.

Interest Rate Outlook and Valuation Impact

Interest rate expectations continue to significantly influence property valuations, particularly in lower-priced segments where buyers are more sensitive to mortgage costs. The renewed concerns that emerged in February 2026 demonstrate how quickly sentiment can shift based on monetary policy signals[2].

When valuing properties during uncertain interest rate environments, surveyors must consider:

- Mortgage affordability: How rate changes affect typical buyer borrowing capacity

- Alternative investment returns: Whether property remains attractive compared to savings or other investments

- Refinancing risks: How existing owners with maturing fixed-rate mortgages may impact supply

- First-time buyer sensitivity: Lower-priced segments show higher sensitivity to rate changes

These factors influence not just current valuations but also the confidence intervals surveyors should apply when providing valuation ranges.

The Rental Market Connection

The lettings market provides important context for flat valuations, particularly for properties that could serve as either owner-occupied homes or buy-to-let investments. Rental price expectations remain positive, with +20% of survey participants expecting rental prices to rise over the coming three months[2].

This rental market strength creates a price floor for lower-priced flats, as properties that cannot sell at desired prices may be retained as rental investments. Tenant demand edged higher in the three months to January, ending two consecutive quarters of flat or negative readings[1].

However, landlord instructions remain firmly negative at -27% as of February, indicating continued supply constraints in the rental market[2]. For valuation purposes, this suggests that properties suitable for rental use may warrant slight premiums compared to those with characteristics that limit rental potential.

First-Time Buyer Opportunities and Market Impact

First-time buyers are being presented with opportunities not seen in years, with the supply pipeline identified as an important factor in determining how the market develops in 2026[5]. This demographic shift has significant implications for valuing flats in early 2026 recovery signals.

Properties that appeal to first-time buyers—typically one or two-bedroom flats in accessible locations with good transport links—may experience stronger recovery than larger or more expensive properties. Valuation surveyors should consider:

- 🎯 Buyer profile matching: How well the property aligns with first-time buyer priorities

- 🚇 Location accessibility: Proximity to employment centers and transport infrastructure

- 💡 Move-in readiness: First-time buyers often prefer properties requiring minimal immediate work

- 📱 Modern amenities: Contemporary features may command premiums in this buyer segment

Understanding these buyer preferences helps surveyors identify which properties within the lower-priced segment are most likely to benefit from recovery trends.

Practical Valuation Strategies for Early 2026 Conditions

Comparative Analysis in Transitional Markets

When valuing flats in early 2026 recovery signals, selecting appropriate comparable properties becomes more challenging than in stable markets. Surveyors must balance the need for recent comparables against the reality that market conditions are changing rapidly.

Best practices for comparative analysis include:

- Multiple time horizons: Consider comparables from 3, 6, and 12 months to identify trends

- Adjustment transparency: Clearly document any adjustments made for time, condition, or location

- Market direction indicators: Reference broader market data (like RICS survey results) to contextualize comparables

- Property-specific factors: Emphasize unique characteristics that may insulate or expose properties to market trends

The homebuyers report example guide provides insight into how comprehensive valuation reports should present this analysis to clients.

Risk Assessment and Valuation Confidence

During transitional market periods, valuation confidence becomes as important as the valuation figure itself. RICS standards require surveyors to communicate the degree of certainty in their valuations, which may be lower during market transitions.

Factors affecting valuation confidence in early 2026 include:

- ⚠️ Limited transaction evidence: Fewer sales in some segments reduce comparable availability

- 🌍 External uncertainties: Geopolitical factors and interest rate unpredictability

- 📉 Regional variation: Difficulty extrapolating from one area to another

- 🔄 Changing buyer behavior: Shifts in what buyers prioritize may not yet be reflected in sales data

Surveyors should consider providing valuation ranges rather than single-point estimates when uncertainty is elevated, clearly explaining the factors that could push values toward either end of the range.

Technology and Data Integration

Modern valuation practice increasingly incorporates technology and data analytics to supplement traditional methods. In early 2026, this integration becomes particularly valuable for identifying recovery signals that may not yet be visible in completed sales data.

Useful data sources include:

- 📊 Listing price trends: Changes in asking prices can signal seller sentiment shifts

- 👀 Viewing activity: Increased property viewings may precede sales improvements

- ⏱️ Time-to-sale metrics: Reducing time on market indicates strengthening demand

- 💬 Buyer feedback: Estate agent intelligence about buyer reactions and offer patterns

While these indicators don't replace actual transaction evidence, they provide valuable context when valuing flats in early 2026 recovery signals where recent sales may not fully reflect current conditions.

Communication with Clients and Stakeholders

Effective communication becomes crucial when market conditions are uncertain. Whether conducting valuations for mortgage purposes, sale negotiations, or investment decisions, surveyors must clearly explain the basis of their conclusions and the assumptions underlying their valuations.

Key communication principles include:

- Context provision: Explain how current market conditions differ from historical norms

- Assumption transparency: Clearly state assumptions about market direction and recovery timing

- Risk disclosure: Identify factors that could cause actual sale prices to differ from valuations

- Update recommendations: Advise when valuations should be revisited given changing conditions

Understanding price reduction tactics helps surveyors advise clients on realistic pricing strategies in transitional markets.

Sector-Specific Considerations for Lower-Priced Flats

Ex-Local Authority Properties

Many lower-priced flats in the UK are ex-local authority properties that were sold under Right to Buy schemes. These properties often present specific valuation challenges, particularly during market recovery periods.

Considerations include:

- 🏘️ Estate perception: Some ex-local authority estates carry stigma that limits buyer appeal

- 🔨 Building condition: Maintenance standards vary significantly between estates

- 👥 Tenure mix: Proportion of owner-occupied versus social housing affects marketability

- 🏗️ Cladding concerns: Some blocks face significant remediation costs affecting values

During recovery periods, properties in well-maintained ex-local authority blocks may see stronger value growth than private developments if affordability is the primary driver of demand.

New-Build Flat Valuations

New-build flats in the lower-priced segment present unique challenges when valuing flats in early 2026 recovery signals. These properties often carried significant premiums during the construction phase but may face value adjustments as market conditions change.

Key factors include:

- 📅 Help to Buy legacy: Properties purchased with government assistance may now be reselling

- 🏗️ Developer pricing: New-build prices may not reflect secondary market conditions

- ⚡ Warranty coverage: Remaining NHBC or similar warranties add value

- 🌟 Specification levels: Modern energy efficiency and amenities may command premiums

Surveyors must carefully distinguish between new-build premium and genuine market value, particularly when comparable evidence is limited.

Conversion and Permitted Development Flats

The proliferation of permitted development conversions—particularly office-to-residential conversions—has added significant stock to the lower-priced flat market. These properties often have characteristics that differ from traditional residential developments.

Valuation considerations include:

- 🪟 Design compromises: Limited natural light or awkward layouts in some conversions

- 🔇 Sound insulation: Conversion quality varies significantly between developers

- 🏢 Building management: Some conversions lack established management structures

- 🚗 Parking and amenities: Converted buildings may have limited resident facilities

During market recovery, these properties may lag traditional flats if buyers become more selective about quality and design.

Shared Ownership Schemes

Shared ownership properties represent an important segment of the lower-priced market, particularly for first-time buyers. Valuing these properties requires understanding both the specific scheme terms and how shared ownership fits within the broader market recovery.

Valuation factors include:

- 📊 Staircasing provisions: Terms for purchasing additional shares affect value

- 🏠 Rent on retained share: Housing association rent levels impact affordability

- 🔄 Resale restrictions: Some schemes limit resale options affecting marketability

- 💰 Minimum share requirements: Changes in lending criteria for shared ownership

As the market recovers, the relative attractiveness of shared ownership versus traditional ownership may shift, affecting valuations in this segment.

Conclusion

Valuing flats in early 2026 recovery signals requires RICS surveyors to balance emerging positive indicators against persistent uncertainties. The improvement in national price trends—from a net balance of -19% in October 2025 to -10% by January 2026—signals that the intense downward pressure is easing[1]. However, significant regional variations, interest rate concerns, and geopolitical uncertainties mean that recovery remains fragile and uneven.

For lower-priced markets specifically, the combination of improved affordability and returning first-time buyers creates opportunities that were absent during the challenging conditions of 2024-2025[5]. Properties that appeal to this demographic—well-located one and two-bedroom flats with modern amenities and reasonable service charges—are likely to lead any recovery in the coming months.

Actionable Next Steps

For property professionals navigating these conditions, several practical steps can improve valuation accuracy:

- Monitor RICS survey data monthly to track sentiment shifts and market direction changes

- Develop location-specific comparable databases that account for regional variations in recovery timing

- Enhance client communication about valuation uncertainty and the assumptions underlying estimates

- Consider forward-looking indicators like buyer enquiries and viewing activity alongside historical sales data

- Differentiate within the lower-priced segment based on property characteristics that align with first-time buyer preferences

- Review and update valuations regularly as market conditions continue to evolve throughout 2026

The RICS homebuyer survey process provides the framework for comprehensive property assessment during these transitional conditions. By combining traditional valuation methodology with enhanced awareness of market dynamics and recovery signals, surveyors can provide clients with the accurate, well-supported valuations they need to make informed property decisions.

As the year progresses, the balance between cautious optimism and practical realism will define successful valuation practice. Those who adapt their methodologies to account for early 2026 recovery signals while maintaining professional skepticism and rigorous analysis will best serve their clients and uphold the standards of the profession.

The rental market's continued strength—with +20% of participants expecting rental price rises[2]—provides additional context for flat valuations, creating price floors and alternative use considerations. Combined with the twelve-month sales outlook of +17% as of February[3], these indicators suggest that while immediate momentum remains limited, the foundations for sustained recovery are gradually being established.

For buyers, sellers, and investors in the lower-priced flat market, obtaining a professional RICS property valuation has never been more important. The transitional nature of current conditions means that accurate, professionally supported valuations provide essential protection against both overpaying in markets that remain weak and missing opportunities in segments that are genuinely recovering.

References

[1] Uk Resi Survey Jan 2026 Report Shows Early Signs Market Recovery Despite Caution – https://www.rics.org/news-insights/uk-resi-survey-jan-2026-report-shows-early-signs-market-recovery-despite-caution

[2] Uk Residential Market Survey February 2026 – https://www.rics.org/content/dam/ricsglobal/documents/market-surveys/uk-residential-market-survey/UK-Residential-Market-Survey_February-2026.pdf

[3] Latest Rics Survey Reveals Global Headwinds Are Weighing On Housing Market Confidence – https://www.buyassociationgroup.com/en-gb/news/latest-rics-survey-reveals-global-headwinds-are-weighing-on-housing-market-confidence/

[4] Real Estate Valuation Extreme Conditions – https://ww3.rics.org/uk/en/journals/property-journal/real-estate-valuation-extreme-conditions.html

[5] Valuing First Time Buyer Properties In 2026 Rics Tactics Amid Improving Affordability And Supply – https://nottinghillsurveyors.com/blog/valuing-first-time-buyer-properties-in-2026-rics-tactics-amid-improving-affordability-and-supply