The mortgage landscape in 2026 is experiencing a significant shift that's reshaping how property professionals approach valuations and building surveys. With mortgage rates expected to stabilize around 6% or lower this year—down from the mid-6% range in 2025—surveyors face a critical challenge: understanding how these rate environment changes affect property valuations, buyer affordability, and the risk factors they should emphasize in their reports. Valuation Adjustments for Mortgage Rate Changes: How 2026 Rate Cuts Impact Building Survey Recommendations has become essential knowledge for chartered surveyors, property buyers, and real estate professionals navigating this evolving market.

The relationship between mortgage rates and property valuations isn't merely academic—it directly impacts how surveyors assess risk, recommend repairs, and guide clients through purchase decisions. As rates decline, buyer purchasing power increases, potentially inflating property values and changing the calculus around acceptable defects and negotiation strategies.

Key Takeaways

- 📉 Mortgage rates are projected to decline to approximately 5.75-6% in 2026, according to major financial institutions, improving buyer affordability significantly

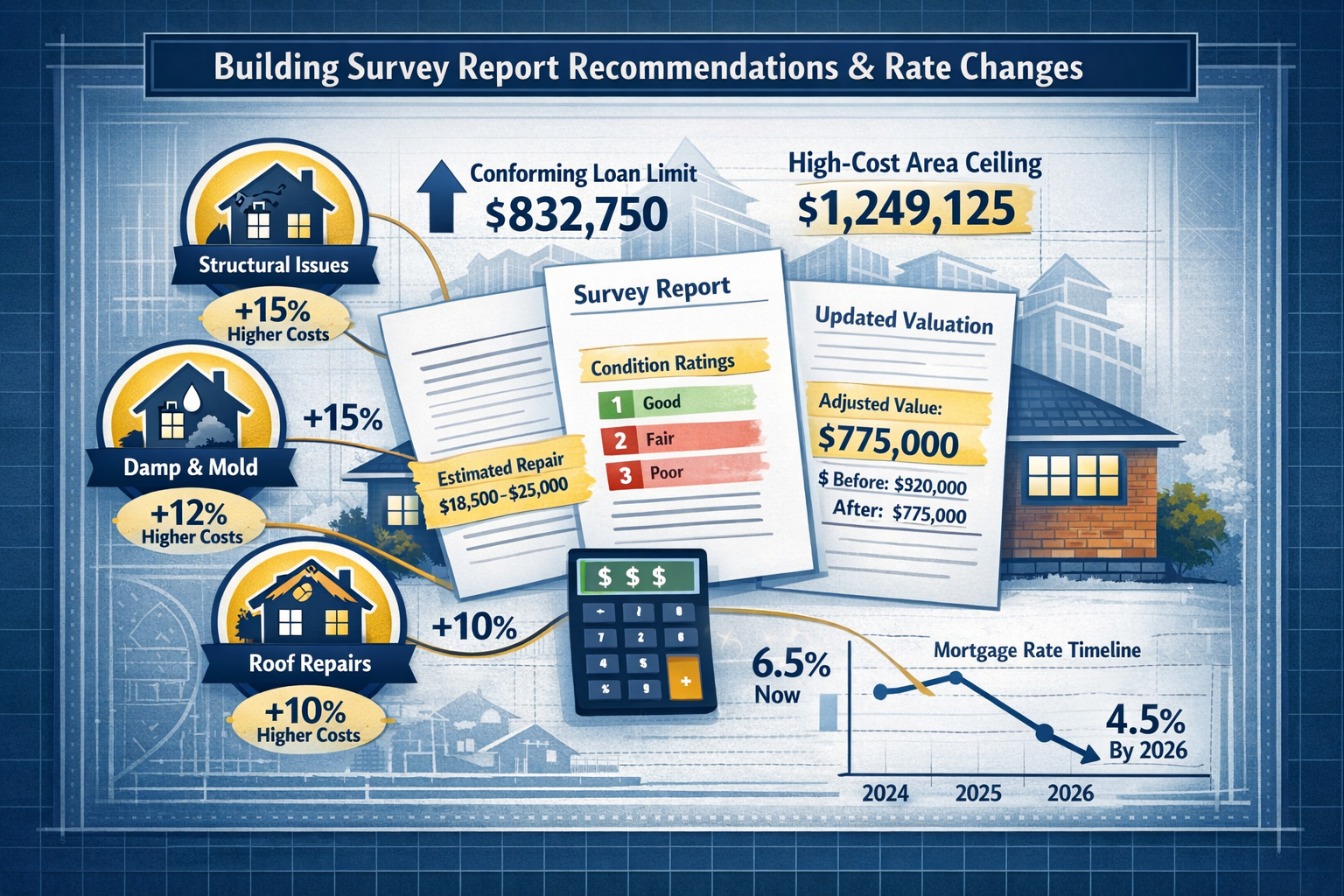

- 🏠 Conforming loan limits increased 3.26% to $832,750 for one-unit properties, expanding access to conventional financing and affecting valuation thresholds

- 🔍 Building survey recommendations must adapt to account for increased buyer leverage in negotiations when rates are favorable

- 💰 Rate reductions affect repair cost negotiations, as buyers with lower monthly payments may have more flexibility to address property defects

- 📊 Surveyors should recalibrate risk assessments based on changing market dynamics and buyer financial capacity in the current rate environment

Understanding the 2026 Mortgage Rate Environment

Current Rate Projections and Market Conditions

The mortgage rate landscape in 2026 represents a marked departure from the volatility experienced in recent years. The National Association of Realtors forecasts rates declining to around 6% [4], while Morgan Stanley strategists predict even more favorable conditions with rates potentially dropping to approximately 5.75% [5]. This stabilization follows a period of significant fluctuation driven by Federal Reserve policy adjustments and inflation concerns.

Several key factors are driving this rate environment:

Federal Reserve Policy: The Fed's cautious approach to monetary policy, balancing inflation control with economic growth, has created conditions for gradual rate reductions [3].

Inflation Moderation: As inflation pressures ease, the underlying drivers of higher mortgage rates have diminished, allowing lenders to offer more competitive terms.

Market Competition: Increased competition among lenders seeking to capture market share in a stabilizing environment has contributed to downward pressure on rates.

The appraisal threshold for higher-priced mortgages increased to $34,200 from $33,500, reflecting a 2.1% CPI-W increase [2]. This adjustment, while seemingly modest, signals regulatory recognition of changing market conditions and property value dynamics.

Conforming Loan Limit Increases

One of the most significant developments affecting property valuations in 2026 is the substantial increase in conforming loan limits. The baseline conforming loan limit (CLL) for one-unit properties rose to $832,750, representing a $26,250 increase from 2025 and a 3.26% year-over-year growth [1]. This increase directly reflects average U.S. home price appreciation between Q3 2024 and Q3 2025.

For high-cost areas, the impact is even more pronounced. The maximum CLL ceiling reached $1,249,125—150% of the baseline limit [1]. This expansion has critical implications for:

- Buyer purchasing power in expensive markets

- Valuation thresholds that determine conventional versus jumbo loan requirements

- Survey recommendations regarding property condition and repair priorities

- Negotiation leverage for buyers seeking price reductions based on defects

These limit increases mean more properties qualify for conventional financing with favorable terms, potentially supporting higher valuations and changing the risk-reward calculation for properties with identified defects.

Valuation Adjustments for Mortgage Rate Changes: Impact on Property Assessments

How Rate Changes Affect Property Values

The relationship between mortgage rates and property values operates through several interconnected mechanisms that chartered surveyors must understand when conducting valuations.

Affordability Dynamics: When rates decline from 6.5% to 5.75%, a buyer's monthly payment on a £500,000 mortgage decreases by approximately £200-250. This additional affordability can translate into:

- Higher maximum purchase prices buyers can afford

- Increased competition for desirable properties

- Upward pressure on property valuations

- Changed tolerance for repair costs and property defects

Market Velocity: Lower rates typically accelerate market activity, creating conditions where properties move faster and sellers have stronger negotiating positions. This affects how building survey findings influence final sale prices.

Investment Calculations: For buy-to-let investors, lower mortgage rates improve yield calculations, potentially supporting higher valuations for rental properties even when significant repairs are identified.

Adjusting Survey Recommendations for Rate Environments

Professional building surveyors must recalibrate their recommendations based on the prevailing rate environment. In 2026's declining rate scenario, several adjustments become necessary:

Repair Cost Contextualization: When presenting findings about property defects, surveyors should help clients understand repair costs in relation to their improved affordability. A £15,000 roof repair represents a different burden when monthly mortgage payments are £250 lower.

Priority Classification: The urgency assigned to various defects may shift. In a low-rate environment with strong buyer demand, clients may prioritize securing the property over negotiating extensive repairs, particularly for cosmetic or non-urgent issues.

Valuation Adjustment Recommendations: Surveyors providing guidance on negotiating purchase prices should account for market strength driven by favorable rates. A defect that might justify a 5% price reduction in a high-rate environment may only support 2-3% when rates are low and demand is strong.

Long-term Value Perspective: With lower financing costs, buyers can better afford to invest in properties requiring renovation. Survey recommendations should emphasize long-term value potential alongside immediate concerns.

Building Survey Recommendations in the 2026 Rate Cut Context

Adapting Survey Methodologies

The declining rate environment of 2026 necessitates methodological adjustments in how building surveys are conducted and reported. Professional surveyors should consider:

Enhanced Financial Context: Modern survey reports should include sections that contextualize findings within current market conditions, including:

| Survey Element | Traditional Approach | 2026 Rate-Adjusted Approach |

|---|---|---|

| Defect Severity | Based solely on structural/safety impact | Includes affordability and market context |

| Repair Urgency | Immediate vs. deferred timeline | Considers buyer financial flexibility |

| Cost Estimates | Standalone repair figures | Compared to monthly payment savings from rates |

| Negotiation Guidance | Standard percentage reductions | Market-adjusted recommendations |

Risk Stratification: Surveyors should clearly differentiate between:

- Critical structural issues requiring immediate attention regardless of market conditions

- Significant defects where timing may be negotiable given favorable financing

- Minor concerns that shouldn't derail transactions in competitive markets

- Cosmetic issues that buyers with improved affordability can address post-purchase

Specific Recommendations for Common Property Issues

When preparing building survey recommendations in 2026's rate environment, surveyors should tailor guidance for common defects:

Damp and Moisture Issues 🌧️

Lower mortgage rates don't reduce the seriousness of damp problems, but they do affect how buyers should approach them. Surveyors should:

- Provide detailed cost estimates for remediation

- Explain how monthly payment savings can offset repair financing

- Recommend specialist investigations where necessary

- Suggest phased repair approaches that align with buyer budgets

Structural Concerns 🏗️

Foundation issues, subsidence, and structural movement remain critical regardless of rates. However, presentation matters:

- Clearly distinguish between progressive and stable defects

- Provide multiple remediation options with cost ranges

- Explain monitoring requirements and timelines

- Help buyers understand long-term implications versus immediate costs

Roofing Defects 🏠

Roof repairs represent significant expenses that buyers must address. In the 2026 context:

- Differentiate between immediate replacement needs and repairs extending useful life

- Provide lifecycle cost analysis showing when replacement becomes economical

- Explain how lower financing costs affect the timing of major roof work

- Recommend appropriate contingency reserves

Mechanical and Electrical Systems ⚡

Aging systems require careful assessment and contextual recommendations:

- Estimate remaining useful life and replacement costs

- Suggest energy efficiency upgrades that lower operating costs

- Explain how modern financing options (including green mortgages) might apply

- Provide phased upgrade strategies aligned with buyer priorities

Strategic Implications for Property Buyers and Professionals

Buyer Decision-Making in a Favorable Rate Environment

The 2026 rate cuts create unique opportunities and challenges for property buyers working with survey findings. Understanding Valuation Adjustments for Mortgage Rate Changes: How 2026 Rate Cuts Impact Building Survey Recommendations enables more strategic decision-making.

Negotiation Positioning: Buyers should recognize that while their affordability has improved, so has competition. Survey findings remain valuable negotiation tools, but expectations must align with market realities:

- Strong buyer position: Properties with significant defects in slower submarkets

- Moderate leverage: Common issues in average-demand areas

- Limited negotiation power: Minor defects in highly competitive markets

Total Cost Analysis: Smart buyers in 2026 should evaluate properties using comprehensive cost modeling that includes:

- Monthly mortgage payments at current rates

- Repair and maintenance costs identified in surveys

- Energy efficiency and operating expenses

- Potential appreciation in a favorable rate environment

- Opportunity costs of waiting versus purchasing with defects

Survey Type Selection: The rate environment influences which survey level provides optimal value. When considering the difference between Level 2 and Level 3 surveys, buyers should weigh:

- Property age and condition

- Purchase price relative to conforming loan limits

- Personal risk tolerance and renovation plans

- Market competition and transaction timeline pressures

Professional Guidance for Surveyors

Chartered surveyors must evolve their practice to remain relevant and valuable in changing market conditions. Key professional considerations include:

Continuing Education: Staying informed about mortgage market trends, financing options, and economic indicators that affect property values and buyer behavior.

Report Enhancement: Developing survey report templates that incorporate market context without compromising professional objectivity. This might include:

- Economic condition summaries

- Financing landscape overviews

- Contextualized repair cost analysis

- Market-specific negotiation guidance

Client Communication: Improving how survey findings are communicated to ensure clients understand both technical issues and market implications. This includes:

- Pre-survey consultations explaining current market dynamics

- Clear executive summaries highlighting critical versus manageable issues

- Follow-up discussions addressing client questions about priorities

- Referrals to qualified specialists for detailed investigations

Cross-Professional Collaboration: Working effectively with mortgage brokers, solicitors, and estate agents to ensure survey findings are properly integrated into transaction decision-making.

Practical Applications and Case Studies

Scenario Analysis: Rate Impact on Survey Outcomes

Consider how Valuation Adjustments for Mortgage Rate Changes: How 2026 Rate Cuts Impact Building Survey Recommendations plays out in real-world situations:

Scenario 1: Victorian Terrace with Damp Issues

- Purchase price: £725,000

- Identified defects: Rising damp, outdated electrical system, roof repairs needed

- Estimated repair costs: £35,000

- Rate impact: At 6.5% rates (2025), monthly payment £4,585; at 5.75% (2026), monthly payment £4,230

- Monthly savings: £355

Survey recommendation adjustment: In 2025's higher-rate environment, surveyors might recommend negotiating a £30,000-35,000 price reduction. In 2026's favorable rates, the recommendation might shift to a £20,000-25,000 reduction with phased repairs, recognizing that the buyer's improved monthly affordability provides flexibility to address issues over time.

Scenario 2: Modern Apartment with Service Charge Concerns

- Purchase price: £550,000

- Identified concerns: Building cladding issues, major works planned

- Estimated contribution: £18,000 over 3 years

- Rate impact: Monthly payment savings of £260 at lower 2026 rates

Survey recommendation adjustment: Rather than recommending buyers avoid the property or demand major price reductions, 2026 surveys might emphasize the improved affordability offsetting future service charges while still highlighting the importance of reviewing building management plans and reserve funds.

Regional Variations and Market Considerations

The impact of rate changes varies significantly across different property markets. When conducting homebuyers surveys, surveyors should consider regional factors:

High-Value Markets (London, Southeast)

- Conforming loan limit increases have greater impact

- Competitive pressure remains intense even with defects

- Survey recommendations should focus on critical issues only

- Buyers may accept minor defects to secure properties

Moderate Markets (Regional cities, suburbs)

- More balanced negotiation opportunities

- Survey findings carry stronger weight in price discussions

- Buyers have time to address defects before or after purchase

- Market velocity varies by specific location and property type

Value Markets (Northern regions, rural areas)

- Rate reductions significantly improve affordability

- Survey findings may identify opportunities for value-add purchases

- Less competition allows thorough defect remediation negotiations

- Buyers can be more selective about property condition

Future Outlook and Emerging Trends

Anticipated Market Evolution

Looking beyond 2026, several trends will continue shaping how Valuation Adjustments for Mortgage Rate Changes: How 2026 Rate Cuts Impact Building Survey Recommendations evolve:

Technology Integration 💻

Advanced survey technologies including thermal imaging, drone inspections, and AI-assisted defect analysis will provide more comprehensive data. This enhanced information must be contextualized within prevailing economic conditions to remain actionable for buyers.

Sustainability Focus 🌱

As energy efficiency becomes increasingly important, survey recommendations will need to address:

- EPC ratings and improvement potential

- Green mortgage eligibility and benefits

- Long-term operating cost projections

- Climate resilience and adaptation requirements

Regulatory Changes

Building safety regulations continue evolving, particularly regarding:

- Fire safety in multi-unit buildings

- Structural integrity standards

- Environmental hazard disclosure

- Lease extension and freehold purchase rights

Preparing for Rate Volatility

While 2026 shows rate stabilization, surveyors and buyers should prepare for potential future volatility by:

Building Flexibility into Recommendations: Survey reports should present multiple scenarios accounting for different market conditions and buyer circumstances.

Emphasizing Fundamental Value: Regardless of rate environments, properties with sound structure, good location, and manageable maintenance requirements retain value.

Maintaining Professional Standards: Economic conditions shouldn't compromise the thoroughness and objectivity of building surveyor services.

Conclusion

The mortgage rate environment of 2026 represents a significant opportunity for property buyers, but it also demands sophisticated understanding of how Valuation Adjustments for Mortgage Rate Changes: How 2026 Rate Cuts Impact Building Survey Recommendations should be interpreted and applied. With rates projected to decline to 5.75-6% and conforming loan limits increasing to $832,750, the financial landscape for property purchases has fundamentally shifted.

For chartered surveyors, this environment requires adapting methodologies to provide contextually relevant recommendations that help clients make informed decisions. Survey findings remain critically important—structural defects, damp issues, and safety concerns don't diminish because rates are favorable—but how these findings are presented and prioritized must reflect current market realities.

Property buyers benefit from understanding that lower rates improve affordability but don't eliminate the need for thorough due diligence. A comprehensive building survey remains essential for identifying defects, estimating costs, and negotiating fair purchase terms, even in competitive markets.

Actionable Next Steps

For Property Buyers:

- Commission appropriate surveys based on property age, type, and condition—don't skip this step even in competitive markets

- Work with experienced professionals who understand current market dynamics and can provide contextualized recommendations

- Develop comprehensive budgets that account for purchase price, repair costs, and ongoing maintenance

- Leverage improved affordability strategically while maintaining realistic expectations about negotiation outcomes

For Property Surveyors:

5. Update report templates to incorporate market context without compromising professional objectivity

6. Enhance client communication to ensure survey findings are properly understood and applied

7. Stay informed about mortgage market trends, financing options, and regulatory changes

8. Collaborate effectively with other professionals in the transaction process

For All Stakeholders:

9. Recognize that rate environments change—make decisions based on long-term property fundamentals, not just current financing conditions

10. Prioritize critical defects while maintaining perspective on manageable issues that shouldn't derail sound purchases

The intersection of favorable mortgage rates and professional building surveys creates optimal conditions for successful property transactions in 2026. By understanding how these elements interact, buyers can make confident decisions, and surveyors can provide the expert guidance that remains invaluable regardless of economic conditions.

References

[1] FHFA Announces Conforming Loan Limit Values for 2026 – https://www.fhfa.gov/news/news-release/fhfa-announces-conforming-loan-limit-values-for-2026

[2] Federal Reserve Board Announces Adjustments to Higher-Priced Mortgage Loan Threshold – https://www.federalreserve.gov/newsevents/pressreleases/bcreg20251215b.htm

[3] Mortgage Rate Trends 2026: What Homebuyers Should Expect – https://7thlvl.com/mortgage-rate-trends-2026-what-homebuyers-should-expect/

[4] Mortgage Rates Forecast for 2026: Experts Predict Whether Rates Will Keep Dropping – https://www.firstcbt.bank/blog/post/mortgage-rates-forecast-for-2026-experts-predict-whether-rates-will-keep-dropping

[5] Mortgage Rates Forecast 2025-2026: Will Mortgage Rates Go Down? – https://www.morganstanley.com/insights/articles/mortgage-rates-forecast-2025-2026-will-mortgage-rates-go-down