The UK lettings market in 2026 presents a fascinating paradox: rental growth is moderating nationally, yet tenant demand remains structurally elevated and supply constraints persist across most regions. For property investors, landlords, and professional surveyors, understanding the nuanced Valuation Techniques for Lettings Market Surge: Surveyor Insights on Tenant Demand and Rental Growth 2026 has never been more critical. With average UK monthly private rents reaching £1,367 and regional variations creating distinct investment opportunities, accurate property valuation requires sophisticated analysis that goes far beyond traditional methods[2].

Recent RICS data reveals that while rental inflation has eased to 3.5% annually (the lowest rate since March 2022), this moderation masks significant geographic disparities and evolving tenant behaviors that directly impact investment yields[2]. Professional surveyors now employ advanced valuation techniques that account for regional performance variations, tenant renewal patterns, property type premiums, and emerging buy-to-let mortgage conditions to provide investors with actionable insights in this recovering market.

Key Takeaways

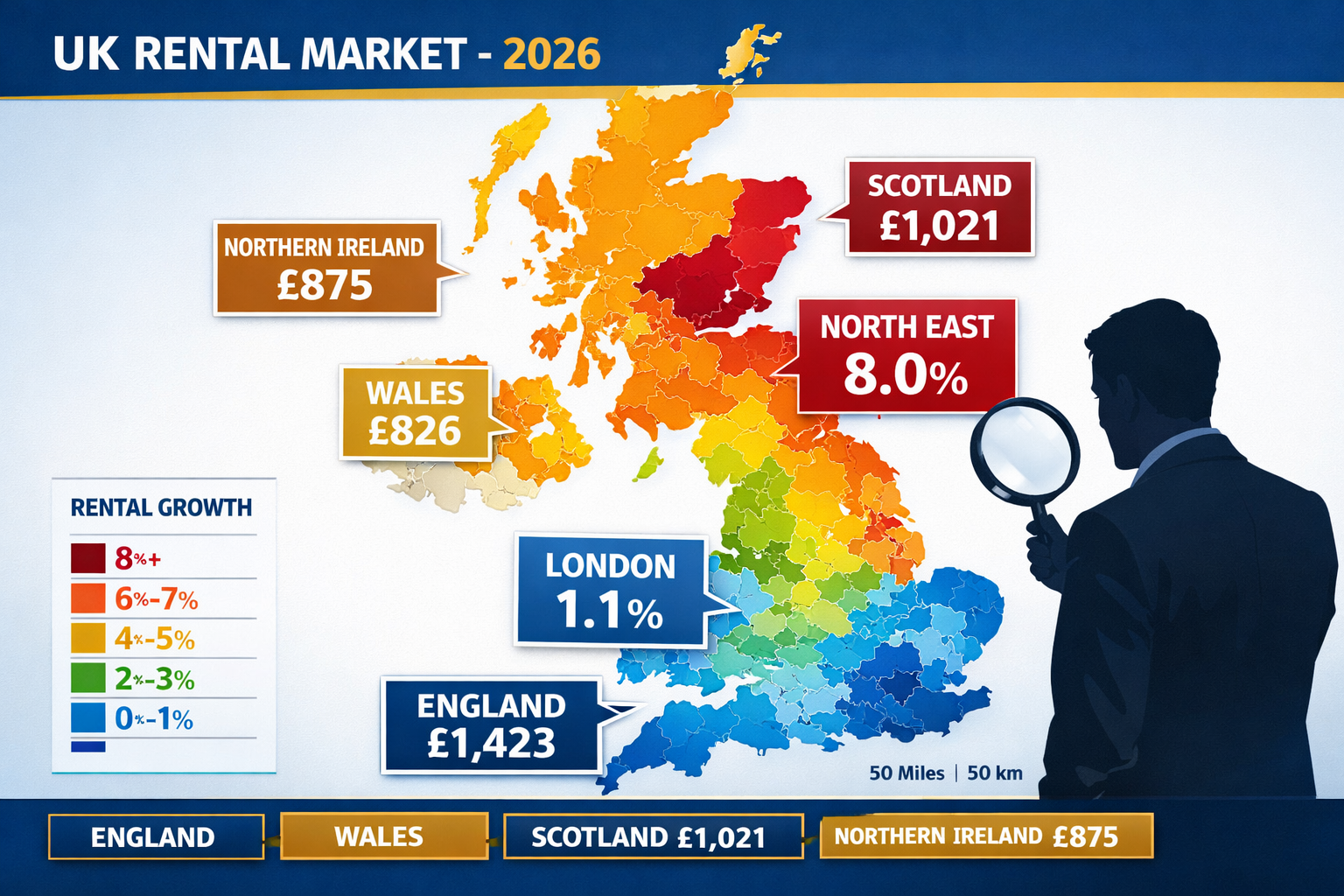

✅ Regional rental growth varies dramatically – The North East leads with 8.0% annual growth while London records just 1.1%, requiring location-specific valuation approaches[2]

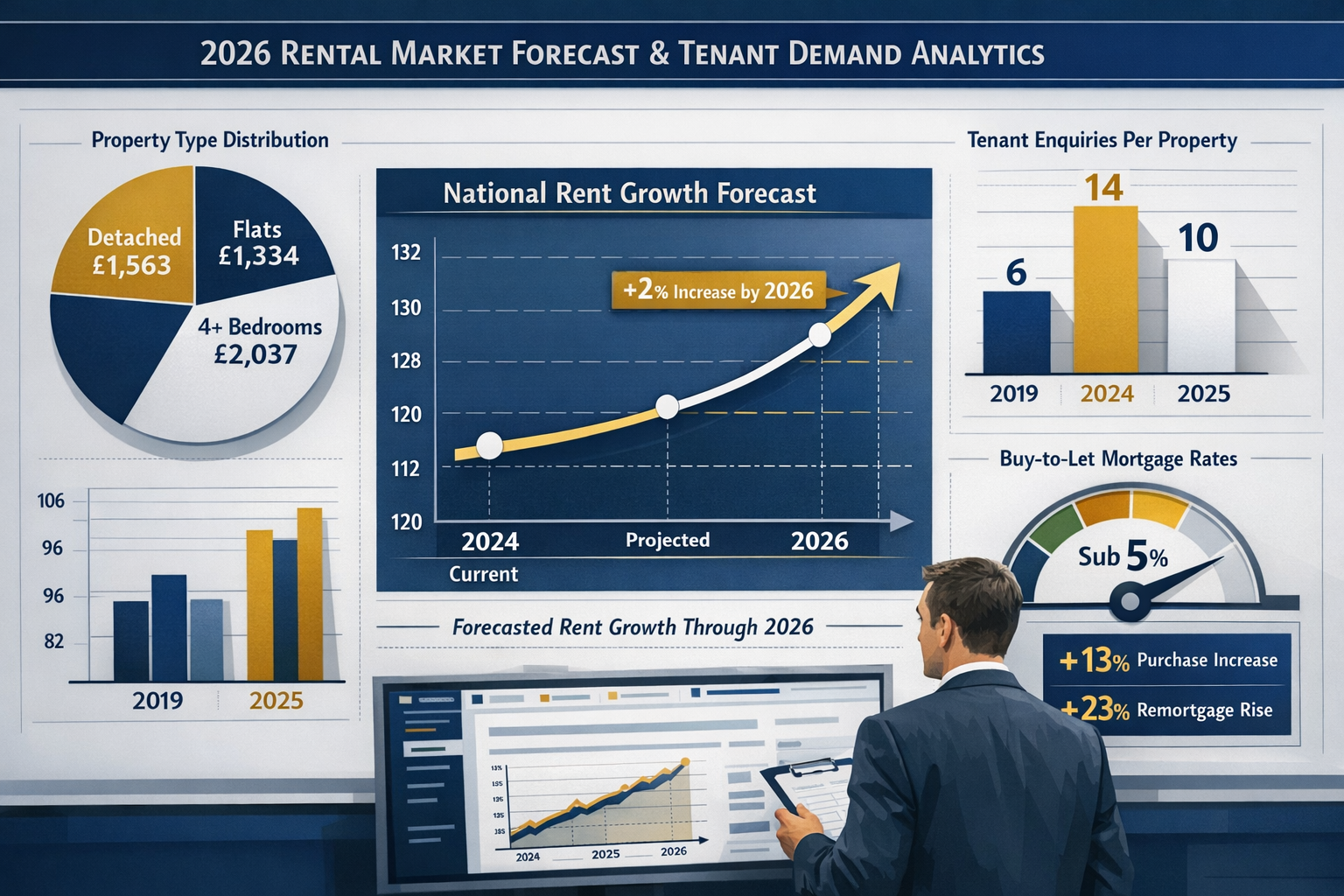

✅ Tenant demand remains elevated despite moderation – National enquiries per property stand at 10 (down from 14 in 2024 but well above the pre-pandemic average of 6), indicating sustained structural demand[4]

✅ Valuation techniques must incorporate renewal vs. new letting dynamics – Tenants renewing contracts experienced 2.8% rent increases while newly let homes declined 0.2% year-on-year[3]

✅ Buy-to-let investment conditions are improving – New purchase mortgages increased 13% and remortgages rose 23%, with rates falling below 5% for many borrowers, stabilizing rental supply prospects[4]

✅ Property type and size command significant rent premiums – Detached properties average £1,563 monthly compared to £1,334 for flats, with four-bedroom properties commanding £2,037 versus £1,109 for one-bedroom units[2]

Understanding the 2026 UK Lettings Market Landscape

Current Rental Growth Patterns and Geographic Variations

The UK rental market in 2026 demonstrates significant geographic fragmentation that challenges traditional nationwide valuation models. Average monthly private rents increased to £1,367, representing a 3.5% annual growth in the 12 months to January 2026, down from 4.0% in December 2025[2]. This represents the lowest annual inflation rate since March 2022, signaling a clear moderation from the rapid growth experienced in previous years.

However, this national average conceals dramatic regional variations that professional surveyors must incorporate into their valuation frameworks:

| Region | Average Monthly Rent | Annual Growth Rate |

|---|---|---|

| North East | Data varies by locality | 8.0% 📈 |

| England | £1,423 | 3.5% |

| Wales | £826 | 5.8% |

| Scotland | £1,021 | 2.6% |

| Northern Ireland | £875 | 5.6% (to Nov 2025) |

| London | Higher than national average | 1.1% 📉 |

The North East's exceptional 8.0% annual growth contrasts sharply with London's modest 1.1% increase, creating vastly different investment propositions that require distinct valuation approaches[2]. For chartered surveyors conducting rental property assessments, these regional disparities necessitate localized comparable analysis rather than relying on national benchmarks.

The London Rental Decline Phenomenon

Inner London has experienced 13 consecutive months of annual rental decline, with Outer London recording 8 months and the South East 4 months of year-on-year decreases[3]. This sustained downturn in regions that collectively account for approximately one-third of Britain's rental homes represents a fundamental shift in market dynamics.

Professional valuers must recognize that this London-centric decline significantly influences national statistics while masking strength in other markets. When conducting RICS property valuations for investment purposes, surveyors now segment London properties separately, applying different growth assumptions and yield expectations compared to regional markets.

Tenant Demand Metrics and Market Fundamentals

Despite moderating rental growth, tenant demand remains structurally elevated compared to pre-pandemic norms. National rental demand stood at 10 enquiries per property in 2025, down from the peak of 14 in 2024 but significantly above the 2019 average of 6 enquiries[4].

This sustained demand elevation indicates that the UK lettings market's fundamental characteristic remains supply constraint rather than demand collapse. For surveyors evaluating investment potential, this distinction is crucial: properties in well-supplied markets may face pricing pressure, while those in supply-constrained areas can command premium valuations despite national growth moderation.

The structural undersupply identified across most UK regions supports continued rental stability and provides a foundation for conservative growth projections in valuation models[4]. Professional building surveyor services increasingly incorporate supply-demand analysis into their rental property assessments, recognizing that local market tightness directly impacts achievable rents and investment yields.

Valuation Techniques for Lettings Market Surge: Professional Surveyor Methodologies

The Comparative Rental Analysis Method

The comparative rental analysis (also known as the rental comparables method) forms the foundation of most lettings property valuations. This technique involves identifying recently let properties with similar characteristics—location, size, condition, amenities—and using their achieved rents to establish market value for the subject property.

In 2026's fragmented market, surveyors must refine this traditional approach by:

🔍 Geographic Micro-Segmentation

Rather than comparing properties across broad regions, professional valuers now analyze hyper-local rental markets down to specific neighborhoods or postcodes. For example, while London overall shows 1.1% growth, specific boroughs may demonstrate entirely different trajectories[2].

📊 Property Type Stratification

The significant rent premiums between property types require careful like-for-like comparison:

- Detached properties: £1,563 average monthly rent

- Flats and maisonettes: £1,334 average monthly rent

- One-bedroom properties: £1,109 average monthly rent

- Four+ bedroom properties: £2,037 average monthly rent[2]

A surveyor valuing a four-bedroom detached property in the North East would apply entirely different comparables and growth assumptions than one assessing a one-bedroom flat in Inner London.

⏱️ Temporal Adjustment Factors

Given the rapid market evolution, comparables from six months ago may require significant adjustment. Surveyors apply time-based correction factors reflecting current growth rates—for instance, applying the regional 8.0% annual growth rate pro-rata when using older comparables in the North East[2].

When conducting property assessments for buy-to-let investments, professional surveyors typically examine 5-10 comparable lettings within the past 3-6 months, adjusting for property-specific features, market timing, and local demand conditions.

The Investment (Income Capitalization) Method

For buy-to-let investors, the investment method provides the most relevant valuation framework by directly linking rental income to capital value. This technique calculates property value based on the income stream it generates, adjusted for risk and market conditions.

The fundamental formula is:

Property Value = Net Annual Rental Income ÷ Capitalization Rate (Yield)

In 2026's market, professional surveyors apply sophisticated variations of this approach:

Gross Rental Yield Calculation:

Gross Yield = (Annual Rental Income ÷ Property Purchase Price) × 100

For example, a property generating £1,367 monthly rent (£16,404 annually) valued at £270,000 (the UK average house price) would produce:

Gross Yield = (£16,404 ÷ £270,000) × 100 = 6.08%

Net Rental Yield Adjustment:

Professional valuations account for operating expenses, void periods, maintenance costs, and management fees:

Net Yield = [(Annual Rent - Annual Expenses) ÷ Property Value] × 100

Typical expense assumptions for 2026 include:

- Maintenance and repairs: 10-15% of rental income

- Management fees: 8-12% of rental income

- Void periods: 4-8 weeks annually

- Insurance and compliance: £500-£1,500 annually

Market-Adjusted Capitalization Rates:

Surveyors apply different capitalization rates based on location, property quality, and tenant security:

- Prime London locations: 3.5-4.5% (higher values, lower yields)

- Regional city centers: 5.0-6.5%

- High-growth regions (North East): 6.5-8.0%

- Secondary locations: 7.0-9.0%

The improving buy-to-let mortgage conditions—with rates falling below 5% for many borrowers and new purchase mortgages increasing 13%—directly impact yield expectations[4]. Surveyors now incorporate financing cost analysis into their valuations, recognizing that improved mortgage accessibility enhances investment viability and supports capital values.

For comprehensive investment analysis, professional London property surveyors combine yield calculations with capital appreciation forecasts, creating total return projections that guide investment decisions.

The Residual Valuation Technique for Conversion Opportunities

With tenant demand elevated and rental supply constrained, many investors seek property conversion opportunities—transforming single-family homes into HMOs (Houses in Multiple Occupation) or converting commercial spaces to residential lettings.

The residual valuation method calculates the maximum price an investor should pay for a property requiring conversion or significant improvement:

Residual Value = Completed Property Value – (Conversion Costs + Developer's Profit + Fees)

Example Calculation:

A three-bedroom house could be converted to a five-bedroom HMO in a high-demand area:

- Completed HMO rental value: £2,500 monthly (£30,000 annually)

- Capitalization at 7% yield: £428,571 completed value

- Conversion costs: £80,000

- Professional fees (10%): £8,000

- Developer's profit (15%): £64,286

- Total deductions: £152,286

- Maximum purchase price: £276,285

Professional surveyors conducting residual valuations in 2026 must account for:

🏗️ Regulatory Compliance Costs

HMO licensing, fire safety requirements, energy efficiency standards (EPC ratings), and planning permissions add significant expense that varies by local authority.

📈 Market Timing Risk

The 2026 forecast of 2% national rent increase suggests modest growth, requiring conservative assumptions about completed property values[4].

🔧 Condition Assessment

Detailed building surveys identify hidden defects that could inflate conversion costs, directly impacting residual value calculations.

The Discounted Cash Flow (DCF) Analysis

For sophisticated investors evaluating long-term lettings portfolios, the discounted cash flow method provides the most comprehensive valuation framework. This technique projects future rental income streams and capital appreciation, discounting them to present value using an appropriate discount rate.

DCF Components for Rental Properties:

-

Projected Rental Income Streams (Years 1-10)

- Year 1: Current market rent

- Years 2-10: Rent escalated at projected growth rates (2% nationally for 2026, adjusted regionally)[4]

-

Operating Expense Projections

- Annual maintenance, management, void periods

- Escalated at inflation rates

-

Terminal Value Calculation

- Projected property value at end of holding period

- Based on rental income capitalization or comparable sales

-

Discount Rate Application

- Reflects investment risk, financing costs, and opportunity cost

- Typically 8-12% for residential lettings

Example DCF Framework:

| Year | Gross Rent | Net Income | Discount Factor (10%) | Present Value |

|---|---|---|---|---|

| 1 | £16,404 | £13,123 | 0.909 | £11,929 |

| 2 | £16,732 | £13,386 | 0.826 | £11,057 |

| 3 | £17,067 | £13,654 | 0.751 | £10,254 |

| … | … | … | … | … |

| 10 | £19,478 | £15,582 | 0.386 | £6,015 |

| Terminal | – | £324,000 | 0.386 | £125,064 |

Total Present Value = Sum of Discounted Cash Flows + Discounted Terminal Value

Professional surveyors apply DCF analysis particularly for:

- Portfolio acquisitions involving multiple properties

- Development-to-hold strategies where conversion adds value over time

- Institutional investment requiring detailed return projections

- Comparative investment analysis evaluating lettings against alternative assets

The DCF method's sophistication allows incorporation of complex scenarios including tenant renewal patterns (where renewals show 2.8% rent increases versus 0.2% decline for new lettings)[3], regional growth variations, and changing market conditions over extended holding periods.

Surveyor Insights on Tenant Demand and Rental Growth 2026

Analyzing Tenant Renewal vs. New Letting Dynamics

One of the most significant insights from 2026 market data concerns the divergence between tenant renewal and new letting performance. This bifurcation creates distinct valuation considerations for surveyors assessing rental property investment potential.

Key Performance Metrics:

- Newly let homes: Declined 0.2% year-on-year to £1,366 monthly average

- Tenant renewals: Increased 2.8% overall

- Renewals outside London: Rose 5.2% year-on-year[3]

This pattern reveals several critical insights for property valuation:

💼 Tenant Retention Premium

Properties with established, satisfied tenants command higher effective yields than those requiring frequent re-letting. The 2.8% renewal increase versus 0.2% decline for new lettings demonstrates that landlords can achieve better rental growth by retaining existing tenants[3].

Surveyors conducting investment valuations now apply tenant stability adjustments, adding 5-10% to valuations for properties with long-term tenants on periodic tenancies (allowing regular rent reviews) compared to properties requiring new tenant acquisition.

🔄 Void Period Impact

The moderation in new letting rents suggests increased competition for new tenants, potentially extending void periods. Professional valuers increase void period assumptions from the traditional 2-4 weeks to 4-8 weeks in competitive markets, directly reducing net rental income projections.

📍 Geographic Renewal Patterns

The 5.2% renewal growth outside London versus overall 2.8% national renewal increase indicates that regional markets offer superior retention-based growth prospects[3]. Surveyors valuing properties in areas like Croydon, Bromley, or Wandsworth apply more optimistic renewal-based growth assumptions than those assessing Inner London properties.

Property Type and Size Valuation Premiums

The 2026 rental market demonstrates substantial premiums based on property type and bedroom count, requiring surveyors to apply sophisticated stratification in their valuation models.

Property Type Rental Hierarchy:

🏡 Detached Properties: £1,563 monthly average

- Premium over average: +14.3%

- Target demographic: Families, professional couples

- Valuation consideration: Scarcity in urban areas drives premium

🏘️ Semi-Detached/Terraced: Approximately £1,400-£1,500 (interpolated)

- Near national average

- Broad market appeal

🏢 Flats and Maisonettes: £1,334 monthly average

- Discount from average: -2.4%

- High supply in urban areas

- Valuation consideration: Lower maintenance appeal offset by competitive pricing[2]

Bedroom Count Rental Stratification:

| Bedrooms | Average Monthly Rent | Premium/Discount |

|---|---|---|

| 1 Bedroom | £1,109 | -18.9% |

| 2 Bedrooms | ~£1,250 (interpolated) | -8.6% |

| 3 Bedrooms | ~£1,400 (interpolated) | +2.4% |

| 4+ Bedrooms | £2,037 | +49.0% 🌟 |

The dramatic 49% premium for four-bedroom properties reflects acute supply constraints for larger family homes in the rental sector[2]. Surveyors valuing larger properties apply lower capitalization rates (higher multiples) recognizing this scarcity premium and typically stronger tenant retention.

Investment Strategy Implications:

Professional valuers advise investors that:

- One-bedroom flats offer lower entry costs but face highest competition and lowest growth potential

- Three-bedroom houses provide balanced risk-return profiles with broad tenant appeal

- Four-bedroom properties command premium rents but require larger capital investment and may experience longer void periods due to smaller tenant pool

When conducting property inspections for valuation purposes, surveyors pay particular attention to features that enhance property type appeal—private gardens for detached homes, parking for family properties, proximity to transport for flats.

Regional Investment Opportunity Analysis

The Valuation Techniques for Lettings Market Surge: Surveyor Insights on Tenant Demand and Rental Growth 2026 must incorporate detailed regional analysis, as geographic location now represents the single most significant valuation variable.

High-Growth Investment Regions:

🔺 North East England (8.0% Annual Growth)

- Valuation approach: Apply aggressive growth assumptions (6-8% annually)

- Yield expectations: 7-9% gross yields achievable

- Investment thesis: Undersupply meeting sustained demand from employment growth

- Risk factors: Smaller capital appreciation potential, economic sensitivity

🏴 Wales (5.8% Annual Growth, £826 Average Rent)

- Valuation approach: Moderate growth projections (4-6% annually)

- Yield expectations: 8-10% gross yields in secondary cities

- Investment thesis: Affordable entry points with strong rental demand

- Risk factors: Lower absolute rents limit income potential[2]

Stabilizing Investment Regions:

🏴 Scotland (2.6% Annual Growth, £1,021 Average Rent)

- Valuation approach: Conservative growth assumptions (2-3% annually)

- Yield expectations: 5-7% gross yields

- Investment thesis: Stable, mature market with regulatory clarity

- Risk factors: Additional regulatory requirements, tenant protection legislation

Challenging Investment Regions:

🏙️ Inner London (13 Consecutive Months of Decline)

- Valuation approach: Flat or negative growth assumptions for 2026

- Yield expectations: 3-4% gross yields (capital appreciation focus)

- Investment thesis: Long-term capital growth in prime locations

- Risk factors: High entry costs, sustained rental pressure, tenant affordability constraints[3]

🌆 Outer London (8 Months of Decline)

- Valuation approach: Minimal growth (0-1% annually)

- Yield expectations: 4-5% gross yields

- Investment thesis: Potential value recovery as market stabilizes

- Risk factors: Uncertain recovery timeline, competition from regional markets

Professional surveyors conducting valuations for areas like Newham, Islington, or Camden apply more conservative assumptions than those valuing properties in Brent or Harrow, recognizing the geographic performance variations within Greater London.

Extreme Market Examples: Highest and Lowest Rental Areas

Understanding the rental market extremes provides valuable context for relative valuation assessments:

Highest Rental Markets:

- Kensington and Chelsea, London: £3,640 monthly average (166% above national average)

- Oxford (excluding London): £1,923 monthly average (41% above national average)[2]

Lowest Rental Markets:

- Dumfries and Galloway, Scotland: £549 monthly average (60% below national average)[2]

These extremes demonstrate the £3,091 monthly differential between the highest and lowest rental markets—a 563% variation that underscores the critical importance of location-specific valuation techniques.

Surveyors use these benchmarks to:

- Validate local market data against national extremes

- Assess relative value of mid-market properties

- Identify arbitrage opportunities where rental yields significantly exceed local property prices

- Contextualize client expectations about achievable rents and investment returns

Advanced Valuation Adjustments for 2026 Market Conditions

Buy-to-Let Mortgage Market Impact on Valuations

The 13% increase in new buy-to-let purchase mortgages and 23% rise in landlord remortgages, combined with many two-year buy-to-let rates falling below 5%, represents a fundamental shift in investment viability that directly impacts property valuations[4].

Financing Cost Integration:

Professional surveyors now incorporate debt service coverage ratios (DSCR) into their valuation assessments:

DSCR = Net Operating Income ÷ Annual Debt Service

Lenders typically require DSCR of 125-145% for buy-to-let mortgages. A property generating £16,404 annual rent with 75% loan-to-value at 5% interest on a £202,500 mortgage would require:

- Annual debt service: £10,125 (interest-only)

- Net operating income (assuming 25% expenses): £12,303

- DSCR: 1.22 (122%)

This falls slightly below typical lender requirements, suggesting the property might require larger deposit or higher rent to secure financing. Surveyors conducting RICS property valuations for investment purposes now routinely include financing feasibility analysis.

Improved Mortgage Accessibility Impact:

The sub-5% rate environment and increased lending activity create several valuation implications:

📈 Enhanced Investment Demand: More accessible financing increases buyer competition for rental properties, supporting capital values

💰 Improved Cash Flow Viability: Lower interest costs enhance net yields, making previously marginal investments viable

🏦 Refinancing Opportunities: The 23% increase in remortgages suggests landlords are extracting equity for portfolio expansion, increasing demand[4]

Surveyors apply financing-adjusted valuations by calculating maximum supportable purchase prices based on achievable rents and current mortgage terms, ensuring valuations reflect real-world investment viability.

Supply Constraint Valuation Premium

The fundamental structural undersupply characterizing the UK rental market justifies valuation premiums for properties in supply-constrained locations[4]. Professional surveyors identify supply constraints through:

📊 Supply-Demand Ratio Analysis

- Properties available per 100 searching tenants

- New rental property construction rates

- Landlord exit/entry rates in local market

⏱️ Time-to-Let Metrics

- Average days on market before letting

- Void period trends over 12-24 months

- Seasonal variation patterns

🎯 Enquiry-to-Viewing Conversion

- Number of enquiries per property (national average: 10)[4]

- Viewing-to-application conversion rates

- Multiple application frequency

Properties in markets demonstrating:

- High enquiry volumes (12+ per property)

- Rapid letting times (under 2 weeks)

- Low void periods (under 3 weeks annually)

- Limited new supply (minimal new build rental stock)

…justify 5-15% valuation premiums over comparable properties in balanced markets, reflecting superior income security and growth potential.

Rental Growth Forecast Integration

The 2% national rent increase forecast for 2026 provides a baseline for growth assumptions, but professional surveyors apply sophisticated regional and property-type adjustments[4]:

Tiered Growth Projection Framework:

Tier 1 – High Growth Markets (5-8% annually):

- North East England

- Selected Welsh cities

- Supply-constrained regional centers

- Properties with tenant retention advantages

Tier 2 – Moderate Growth Markets (2-4% annually):

- Midlands regions

- Northern Ireland

- Outer London (recovery phase)

- National average properties

Tier 3 – Low Growth Markets (0-2% annually):

- Inner London

- Oversupplied urban centers

- Properties requiring significant capital expenditure

- Markets with landlord exodus

Tier 4 – Declining Markets (negative growth):

- Specific Inner London submarkets

- Areas with major economic disruption

- Properties with regulatory compliance issues

Surveyors conducting valuations for areas like Richmond, Kingston, or Hammersmith carefully assess local market conditions against these tiers, avoiding blanket application of national forecasts.

Multi-Year Projection Models:

Professional valuations incorporate declining growth rate assumptions over extended periods:

- Years 1-2: Current market growth rates

- Years 3-5: Regression toward long-term mean (3-4% annually)

- Years 6-10: Long-term sustainable growth (2.5-3% annually)

This conservative approach prevents over-valuation based on temporary market conditions while recognizing near-term growth opportunities.

Property Condition and Improvement Valuation Impact

The relationship between property condition and rental value has intensified in 2026's competitive market, requiring surveyors to apply detailed condition-based adjustments.

Energy Performance Certificate (EPC) Rating Impact:

| EPC Rating | Rental Premium/Discount | Tenant Appeal |

|---|---|---|

| A-B | +8-12% premium | Highest demand |

| C | +3-5% premium | Strong demand |

| D | Baseline | Average demand |

| E | -5-8% discount | Declining appeal |

| F-G | -15-25% discount | Limited lettability |

With increasing tenant awareness of energy costs and regulatory pressure toward higher efficiency standards, surveyors conducting building surveys now emphasize EPC ratings in their rental valuations.

Modernization and Presentation Impact:

Professional surveyors apply condition-based multipliers to rental values:

- Recently refurbished (within 2 years): +10-15%

- Good condition (5-10 years since update): +5-8%

- Average condition (10-15 years): Baseline

- Dated but functional (15-25 years): -8-12%

- Poor condition (requiring significant work): -20-30%

Strategic Improvement Analysis:

When valuing properties with improvement potential, surveyors calculate improvement-adjusted values:

Improved Value = Current Value + (Improvement Cost × Return Multiple)

Typical return multiples for rental property improvements:

- Kitchen replacement: 1.5-2.0× (£15,000 cost → £22,500-£30,000 value increase)

- Bathroom upgrade: 1.3-1.8× (£8,000 cost → £10,400-£14,400 value increase)

- Energy efficiency improvements: 2.0-3.0× (£5,000 cost → £10,000-£15,000 value increase)

- Additional bedroom conversion: 2.5-4.0× (£25,000 cost → £62,500-£100,000 value increase)

These calculations inform investment decisions about whether to purchase and improve properties or acquire turnkey rental investments.

Practical Application: Case Studies in Lettings Valuation 2026

Case Study 1: North East Regional Investment Property

Property Profile:

- Location: Newcastle upon Tyne suburb

- Type: 3-bedroom semi-detached house

- Current condition: Good (recently updated kitchen)

- Current market rent: £950 monthly (£11,400 annually)

- Purchase price: £165,000

Surveyor Valuation Analysis:

Comparative Method:

- Recent comparable lettings: £920-£980 monthly

- Adjustment for updated kitchen: +£30

- Indicated market rent: £950 ✓ (validates asking rent)

Investment Method:

- Gross rental yield: (£11,400 ÷ £165,000) × 100 = 6.91%

- Estimated expenses (20%): £2,280

- Net annual income: £9,120

- Net rental yield: 5.53%

- Regional capitalization rate: 6.5-7.5%

- Indicated value range: £121,600-£140,308

Growth-Adjusted DCF (5-year hold):

- Annual rent growth assumption: 7% (regional high growth)[2]

- Projected Year 5 rent: £15,986

- Cumulative net income (discounted at 10%): £38,642

- Terminal value (Year 5 at 7% cap rate): £228,371

- Discounted terminal value: £141,738

- Total present value: £180,380

Surveyor Conclusion:

At £165,000 purchase price, property offers attractive investment value with:

- Solid current yield (6.91% gross, 5.53% net)

- Strong growth potential (7% annually in high-growth region)

- Positive DCF valuation (£180,380 vs £165,000 cost)

- Recommendation: Proceed with acquisition

Case Study 2: Inner London Flat Investment Challenge

Property Profile:

- Location: Zone 2 Inner London

- Type: 2-bedroom flat

- Current condition: Average

- Current market rent: £1,800 monthly (£21,600 annually)

- Purchase price: £485,000

Surveyor Valuation Analysis:

Comparative Method:

- Recent comparable lettings: £1,750-£1,850 monthly

- Market showing rental decline trend (13 months negative)[3]

- Indicated market rent: £1,775 (below current £1,800)

Investment Method:

- Gross rental yield: (£21,600 ÷ £485,000) × 100 = 4.45%

- Estimated expenses (25% due to London costs): £5,400

- Net annual income: £16,200

- Net rental yield: 3.34%

- London capitalization rate: 3.5-4.5%

- Indicated value range: £360,000-£462,857

Growth-Adjusted DCF (5-year hold):

- Annual rent growth assumption: 0% (flat market)[2]

- Projected Year 5 rent: £21,600 (unchanged)

- Cumulative net income (discounted at 10%): £61,424

- Terminal value (Year 5 at 4% cap rate): £405,000

- Discounted terminal value: £251,415

- Total present value: £312,839

Surveyor Conclusion:

At £485,000 purchase price, property shows significant overvaluation:

- Low current yield (4.45% gross, 3.34% net)

- Negative growth outlook (0% assumption conservative)

- Negative DCF valuation (£312,839 vs £485,000 cost = -35% overvaluation)

- Recommendation: Avoid acquisition unless price reduces to £320,000-£350,000 range

Case Study 3: Regional HMO Conversion Opportunity

Property Profile:

- Location: Manchester suburb

- Type: 4-bedroom detached house (conversion to 6-bedroom HMO)

- Current condition: Requires conversion work

- Purchase price: £280,000

- Conversion cost estimate: £65,000

Surveyor Valuation Analysis:

Residual Method:

- Post-conversion rental: 6 rooms × £450 monthly = £2,700 monthly (£32,400 annually)

- Regional HMO capitalization rate: 8%

- Completed property value: £32,400 ÷ 0.08 = £405,000

- Conversion costs: £65,000

- Professional fees (architect, planning, licensing): £8,000

- Developer's profit (15%): £60,750

- Total deductions: £133,750

- Maximum supportable purchase price: £271,250

Investment Method (Post-Conversion):

- Gross rental yield: (£32,400 ÷ £345,000 total cost) × 100 = 9.39%

- HMO expenses (higher at 35%): £11,340

- Net annual income: £21,060

- Net rental yield: 6.11%

- Debt service coverage (75% LTV at 5%): £12,938 annual interest

- DSCR: 21,060 ÷ 12,938 = 1.63 ✓ (exceeds lender requirements)

Risk-Adjusted Analysis:

- Market rent assumption: Conservative (£450 vs potential £475-500)

- Conversion cost contingency: +15% (£74,750 total)

- Extended void during conversion: 6 months (£16,200 lost income)

- Risk-adjusted total cost: £370,950

- Risk-adjusted yield: 8.74% gross, 5.68% net

Surveyor Conclusion:

At £280,000 purchase price, HMO conversion offers viable investment:

- Purchase price within residual value (£271,250-£280,000 = modest premium acceptable)

- Strong post-conversion yield (9.39% gross, 6.11% net)

- Adequate financing coverage (DSCR 1.63)

- Risk-adjusted returns remain attractive (5.68% net yield)

- Recommendation: Proceed with detailed building survey to validate conversion cost assumptions

Implementing Professional Valuation Standards and Best Practices

RICS Valuation Standards (Red Book) Compliance

Professional surveyors conducting lettings market valuations must adhere to RICS Valuation – Global Standards (commonly known as the Red Book), which establishes mandatory practices and ethical standards.

Key Red Book Requirements for Rental Property Valuation:

📋 Terms of Engagement

- Clear identification of valuation purpose (investment, financing, taxation)

- Specification of valuation basis (Market Value, Investment Value, Fair Value)

- Confirmation of inspection scope and limitations

- Statement of assumptions and special assumptions

🔍 Inspection and Investigation

- Physical inspection of property (internal and external where possible)

- Review of title documents and lease terms

- Investigation of planning permissions and building regulations compliance

- Assessment of environmental and contamination risks

📊 Market Research and Analysis

- Collection of comparable rental evidence

- Analysis of local market conditions and trends

- Review of economic factors affecting rental demand

- Consultation of published market data and indices

📝 Valuation Report Content

- Executive summary with valuation figure

- Property description and location analysis

- Market commentary and comparable evidence

- Valuation methodology explanation

- Assumptions, special assumptions, and limitations

- Professional qualifications and declarations

Professional chartered surveyors ensure their lettings valuations meet these standards, providing clients with defensible, transparent assessments suitable for investment decisions, financing applications, or legal proceedings.

Data Sources and Market Intelligence

Accurate Valuation Techniques for Lettings Market Surge: Surveyor Insights on Tenant Demand and Rental Growth 2026 depend on comprehensive, current market data from authoritative sources.

Primary Data Sources:

🏛️ Official Statistics:

- Office for National Statistics (ONS): Index of Private Housing Rental Prices

- HM Land Registry: Property transaction data

- Valuation Office Agency: Council tax and rating information

- Department for Levelling Up: Housing supply and planning statistics

🏢 Industry Research:

- Rightmove: Rental market reports and tenant demand metrics

- Zoopla: Rental value estimates and market trends

- HomeLet: Rental index and regional analysis

- RICS: Residential market surveys and member data

💼 Specialist Databases:

- CoStar: Commercial and residential investment data

- EGi: Property market intelligence

- Dataloft: Rental market analytics

- LonRes: London-specific residential data

Professional surveyors subscribe to multiple data sources, cross-referencing information to validate market trends and identify anomalies. When conducting valuations for areas like Fulham, Battersea, or Paddington, they combine national statistics with hyper-local data from letting agents and property managers.

Technology Integration in Modern Valuation Practice

The 2026 lettings market valuation landscape increasingly incorporates advanced technology and data analytics to enhance accuracy and efficiency.

🤖 Automated Valuation Models (AVMs):

Machine learning algorithms analyze thousands of comparable transactions, adjusting for property characteristics, location attributes, and market timing to generate instant valuations. Professional surveyors use AVMs as:

- Initial screening tools for portfolio valuations

- Validation checks against manual valuations

- Market trend indicators for rapid market movement detection

Limitations: AVMs struggle with unique properties, recent market shifts, and localized supply-demand imbalances, requiring professional surveyor oversight.

📱 Digital Inspection Tools:

- Laser measuring devices: Accurate floor area calculations

- Thermal imaging cameras: Energy efficiency and insulation assessment

- Drone photography: Roof and exterior condition evaluation

- 360° cameras: Comprehensive property documentation

📊 Data Analytics Platforms:

Modern valuation software integrates multiple data sources, automatically:

- Identifying comparable properties within defined parameters

- Adjusting comparables for property differences

- Calculating yield and return metrics

- Generating valuation reports with charts and visualizations

🌐 Geographic Information Systems (GIS):

Mapping technology enables surveyors to:

- Visualize rental value gradients across neighborhoods

- Identify transport accessibility and amenity proximity

- Analyze development pipeline impact on supply

- Assess environmental and flood risks

Professional surveyors combine these technological tools with traditional expertise, ensuring valuations benefit from data-driven insights while incorporating qualitative judgment about property condition, tenant appeal, and market dynamics.

Quality Assurance and Peer Review

Leading surveying practices implement quality assurance protocols to ensure valuation accuracy and consistency:

✅ Internal Review Process:

- Junior surveyor valuations: Reviewed by senior chartered surveyor

- Complex or high-value properties: Subject to partner review

- Contentious valuations: Independent internal peer review

📋 Valuation Checklist Compliance:

- Verification of all comparable evidence sources

- Confirmation of calculation accuracy

- Review of assumptions and special assumptions

- Validation of market commentary against published data

🔄 Post-Valuation Monitoring:

- Tracking of subsequent lettings to validate projections

- Analysis of valuation variance against actual outcomes

- Continuous refinement of methodology based on performance

📚 Continuing Professional Development (CPD):

RICS-registered valuers complete mandatory annual CPD, ensuring knowledge of:

- Latest market trends and data

- Regulatory and legislative changes

- Emerging valuation methodologies

- Technology and software developments

This commitment to professional standards ensures that RICS property valuations for lettings investments provide reliable, defensible assessments that clients can confidently use for investment decisions.

Strategic Investment Guidance for 2026 Lettings Market

Portfolio Diversification Strategies

The regional variations in Valuation Techniques for Lettings Market Surge: Surveyor Insights on Tenant Demand and Rental Growth 2026 suggest sophisticated investors should pursue geographic and property-type diversification.

Recommended Portfolio Allocation Framework:

🎯 Core Holdings (50-60% of portfolio value):

- Stable, moderate-growth regions (Midlands, Scotland, Wales)

- 3-bedroom family homes in established residential areas

- Strong tenant retention characteristics

- Target yields: 5-6% net

- Risk profile: Low-moderate

📈 Growth Holdings (25-35% of portfolio value):

- High-growth regions (North East, selected regional cities)

- Mixed property types (2-4 bedrooms)

- Supply-constrained markets with structural demand

- Target yields: 6-8% net

- Risk profile: Moderate

🚀 Opportunistic Holdings (10-20% of portfolio value):

- Value-add opportunities (HMO conversions, refurbishments)

- Recovery markets (selective Outer London locations)

- Emerging rental hotspots (transport infrastructure improvements)

- Target yields: 8-10%+ net

- Risk profile: Moderate-high

This diversification approach balances income stability from core holdings with growth potential from targeted regional investments and enhanced returns from value-add opportunities.

Timing Considerations for 2026 Market Entry

The current market dynamics create specific timing opportunities for different investor profiles:

✅ Favorable Entry Conditions:

Immediate Acquisition (Q1-Q2 2026):

- High-growth regional markets: North East, Wales showing sustained momentum[2]

- Buy-to-let mortgage market: Sub-5% rates creating financing advantage[4]

- Tenant demand: Elevated enquiries (10 per property) supporting occupancy[4]

Delayed Entry (Q3-Q4 2026):

- London recovery plays: Waiting for stabilization signals in Inner/Outer London[3]

- Interest rate sensitivity: Monitoring for potential further rate reductions

- Market oversupply concerns: Areas with significant new build pipeline

⚠️ Cautionary Timing Signals:

Surveyors advise delaying investment in markets showing:

- Sustained rental decline (13+ months like Inner London)[3]

- Deteriorating tenant demand (falling enquiry-to-property ratios)

- Landlord exodus indicators (high portfolio sale volumes)

- Regulatory uncertainty (pending legislation affecting landlord obligations)

Risk Mitigation Strategies

Professional surveyors recommend comprehensive risk management for lettings investments in 2026's evolving market:

🛡️ Tenant Default Protection:

- Rent guarantee insurance: Covers tenant non-payment (typically 6-12 months)

- Comprehensive tenant referencing: Credit checks, employment verification, previous landlord references

- Deposit protection: Statutory compliance plus adequate deposit levels (5-6 weeks rent)

🏗️ Property Condition Risk:

- Pre-purchase building survey: Identifying defects before acquisition (see which home survey is right for you)

- Maintenance reserve fund: 10-15% of annual rent for repairs and replacements

- Regular property inspections: Quarterly or bi-annual condition assessments

📜 Regulatory Compliance Risk:

- Licensing compliance: HMO licenses, selective licensing schemes

- Safety certification: Gas safety, electrical safety, EPC requirements

- Legal advice: Professional review of tenancy agreements and procedures

💰 Financial Risk:

- Conservative financing: Maximum 75% LTV to maintain equity buffer

- Interest rate hedging: Fixed-rate mortgages protecting against rate increases

- Void period reserves: 6-12 months operating expenses in liquid reserves

📍 Market Risk:

- Geographic diversification: Avoiding concentration in single local market

- Property type variation: Balancing flats, houses, and different bedroom counts

- Exit strategy planning: Identifying disposal options before acquisition

Implementing these risk mitigation strategies ensures lettings investments remain resilient through market cycles and regulatory changes.

Future Outlook: Lettings Market Beyond 2026

Structural Factors Shaping Long-Term Rental Demand

Several fundamental trends will continue influencing UK lettings valuations beyond the immediate 2026 forecast period:

🏘️ Housing Supply Constraints:

The UK's chronic housing undersupply—estimated at 300,000+ units annually below demand—ensures continued rental market tightness. New build construction rates remain below this requirement, supporting long-term rental demand and value stability.

👥 Demographic Shifts:

- Delayed homeownership: Rising house prices relative to incomes extend rental periods

- Population growth: Migration and household formation increasing tenant numbers

- Aging population: Growing demand for accessible, maintenance-free rental accommodation

💼 Employment Patterns:

- Flexible working: Reduced location dependence enabling regional market growth

- Gig economy: Increasing self-employed workers preferring rental flexibility

- Urban-to-suburban shift: Continued demand for space and affordability outside city centers

🌍 Environmental Regulations:

- EPC minimum standards: Likely progression toward C-rating minimum (currently E)

- Carbon reduction targets: Pressure for improved energy efficiency

- Green finance incentives: Preferential mortgage rates for efficient properties

These structural factors suggest the Valuation Techniques for Lettings Market Surge: Surveyor Insights on Tenant Demand and Rental Growth 2026 framework will remain relevant with evolutionary adjustments rather than fundamental revision.

Technology and Valuation Methodology Evolution

The surveying profession continues advancing toward data-driven, technology-enhanced valuation approaches:

🔮 Emerging Valuation Technologies:

Artificial Intelligence and Machine Learning:

- Predictive analytics: Forecasting rental growth with greater accuracy

- Image recognition: Automated property condition assessment from photographs

- Natural language processing: Extracting insights from property descriptions and reviews

Blockchain and Property Data:

- Transparent transaction records: Immutable comparable evidence

- Smart contracts: Automated lease management and rent collection

- Tokenization: Fractional property ownership creating new investment models

Big Data Integration:

- Alternative data sources: Social media sentiment, employment statistics, transport usage

- Real-time market monitoring: Continuous valuation updates rather than point-in-time assessments

- Granular segmentation: Hyper-local valuations at street or building level

Professional surveyors will increasingly combine these technological capabilities with traditional expertise, creating hybrid valuation models that leverage data analytics while incorporating qualitative professional judgment.

Regulatory and Policy Considerations

The lettings market regulatory landscape continues evolving, with implications for property valuations:

📋 Anticipated Regulatory Developments:

Tenant Protection Enhancements:

- Rent control discussions: Potential caps on annual rent increases in certain markets

- Security of tenure: Extended minimum tenancy periods

- Eviction restrictions: Further limitations on Section 21 "no fault" evictions

Landlord Obligations:

- Property standards: Minimum space standards and amenity requirements

- Safety regulations: Enhanced fire safety, electrical safety, carbon monoxide detection

- Licensing expansion: Extended selective and additional licensing schemes

Taxation Changes:

- Capital gains tax: Potential alignment with income tax rates

- Stamp duty: Possible adjustments to additional property surcharge

- Corporation tax: Treatment of property investment companies

Surveyors conducting long-term investment valuations incorporate regulatory risk premiums into their assessments, adjusting yields upward for markets with anticipated regulatory tightening.

Conclusion: Mastering Lettings Valuation in a Dynamic Market

The Valuation Techniques for Lettings Market Surge: Surveyor Insights on Tenant Demand and Rental Growth 2026 landscape demands sophisticated, multi-faceted analysis that extends far beyond traditional property appraisal methods. As this comprehensive guide demonstrates, professional surveyors must integrate:

✅ Regional performance analysis recognizing the dramatic 8.0% growth in the North East versus 1.1% in London[2]

✅ Property-type stratification accounting for the 49% premium four-bedroom properties command over one-bedroom units[2]

✅ Tenant behavior insights incorporating the 2.8% renewal growth versus 0.2% decline for new lettings[3]

✅ Financial market conditions leveraging the improved buy-to-let mortgage environment with sub-5% rates[4]

✅ Technology-enhanced methodologies combining automated valuation models with professional expertise

The 2026 lettings market presents selective opportunities rather than uniform growth, with the North East, Wales, and supply-constrained regional markets offering superior investment prospects compared to Inner London's sustained decline. The national 2% rental growth forecast for 2026 represents controlled expansion following the moderation from previous years' rapid increases[4].

For property investors, the key to successful lettings investment lies in accurate, professional valuation that identifies properties offering:

- Sustainable yields (5-8% net returns depending on risk profile)

- Growth potential (regional markets with structural demand)

- Tenant appeal (property types and locations with proven demand)

- Financial viability (adequate debt service coverage and cash flow)

Actionable Next Steps for Property Investors and Landlords

🎯 Immediate Actions (Next 30 Days):

- Engage professional surveyor: Commission RICS property valuation for properties under consideration

- Research target markets: Analyze regional growth data for North East, Wales, and regional cities

- Review financing options: Obtain buy-to-let mortgage quotes to confirm sub-5% rate availability

- Assess current portfolio: Evaluate existing holdings against 2026 market conditions

📊 Medium-Term Strategy (Next 3-6 Months):

- Portfolio optimization: Consider disposing of underperforming London properties and redeploying capital to high-growth regions

- Property improvement planning: Identify EPC upgrade opportunities to enhance rental values and tenant appeal

- Tenant retention focus: Implement strategies to maximize renewal rates and capture 2.8% renewal growth premium[3]

- Market monitoring: Track monthly rental indices to identify emerging trends and opportunities

🏗️ Long-Term Planning (Next 12+ Months):

- Diversification implementation: Build geographically and property-type diversified portfolio

- Value-add opportunities: Explore HMO conversions and refurbishment projects in high-demand areas

- Regulatory preparation: Ensure compliance with evolving standards and anticipate future requirements

- Exit strategy development: Plan disposal timelines for properties approaching optimal holding periods

📞 Professional Support Resources:

- Building surveys: Commission detailed building surveys before acquisition

- Valuation services: Obtain professional property assessments for investment decisions

- Regional expertise: Consult local surveyors in target areas like Enfield, Barking, or Bexley

- Market intelligence: Subscribe to rental market reports and indices for ongoing monitoring

The UK lettings market in 2026 rewards informed, strategic investment supported by professional valuation expertise. By applying the comprehensive techniques outlined in this guide—from comparative rental analysis and investment method calculations to DCF modeling and risk-adjusted assessments—investors can identify opportunities that deliver sustainable returns while navigating the market's regional complexities and evolving dynamics.

The fundamental principle remains constant: accurate valuation forms the foundation of successful property investment. Whether acquiring a single buy-to-let property or building a substantial portfolio, engaging qualified chartered surveyors who understand the nuances of Valuation Techniques for Lettings Market Surge: Surveyor Insights on Tenant Demand and Rental Growth 2026 provides the professional insight necessary to make confident, profitable investment decisions in this dynamic market environment.

References

[1] Uk Rents Rise 3 5 As House Price Growth Slows – https://www.property118.com/uk-rents-rise-3-5-as-house-price-growth-slows/

[2] February2026 – https://www.ons.gov.uk/economy/inflationandpriceindices/bulletins/privaterentandhousepricesuk/february2026

[3] Rental Market Update – https://www.buyassociationgroup.com/en-us/news/rental-market-update/

[4] Uk Rental Market Outlook 2026 National Trends North West Growth Analysis – https://www.farrellheyworth.co.uk/blog/uk-rental-market-outlook-2026-national-trends-north-west-growth-analysis/

[5] Uk Vacation Rental Market Report – https://hello.pricelabs.co/blog/uk-vacation-rental-market-report/?amp=1

[6] What Is Currently Happening In The Uk Property Market 47 – https://bebeez.eu/2026/02/20/what-is-currently-happening-in-the-uk-property-market-47/

[7] Countdown To May Uk Rental Market Update 19 February 2026 – https://blog.lightwork.co/countdown-to-may-uk-rental-market-update-19-february-2026/

[8] mpamag – https://www.mpamag.com/uk/news/general/rent-and-house-price-inflation-ease-but-market-pressures-persist/565735