The UK property market has entered a new era of regional divergence that demands fresh thinking from valuation professionals. While London struggles with negative growth and the South East stagnates, Northern England is experiencing a remarkable resurgence that's reshaping the national landscape. The Valuation Challenges in Northern England 2026: Surveyor Strategies Amid 5% Price Growth and Southern Slump represent both unprecedented opportunities and complex assessment dilemmas for RICS-qualified professionals navigating this transformed market.

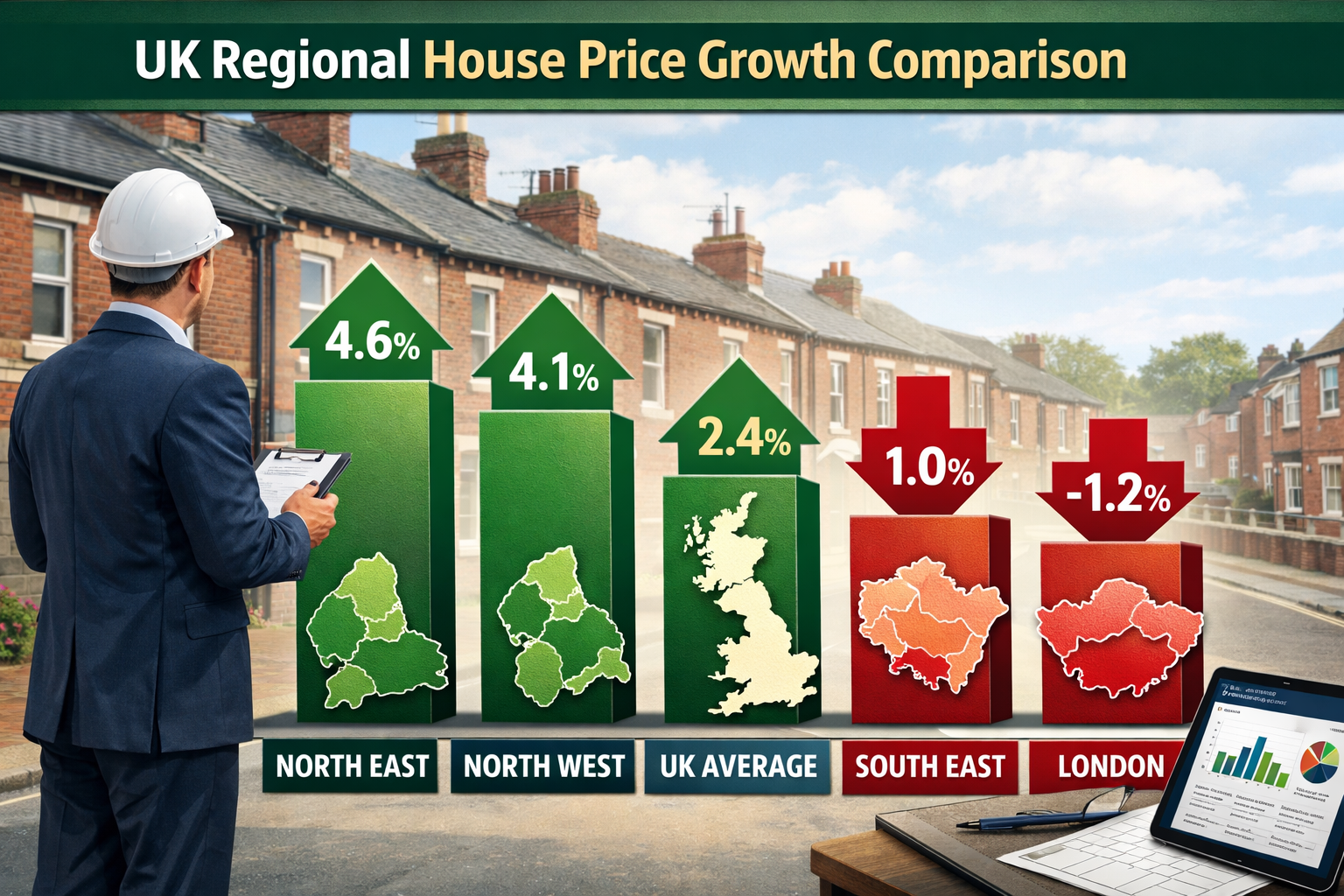

In the 12 months to December 2025, the North East recorded the highest house price inflation among English regions at 4.6%, while the North West followed closely with 4.1% annual growth—a stark contrast to London's -1.2% decline and the South East's modest 1.0% increase.[2][4] This north-south divide isn't just a statistical curiosity; it's fundamentally changing how surveyors must approach property valuations, comparable analysis, and market forecasting.

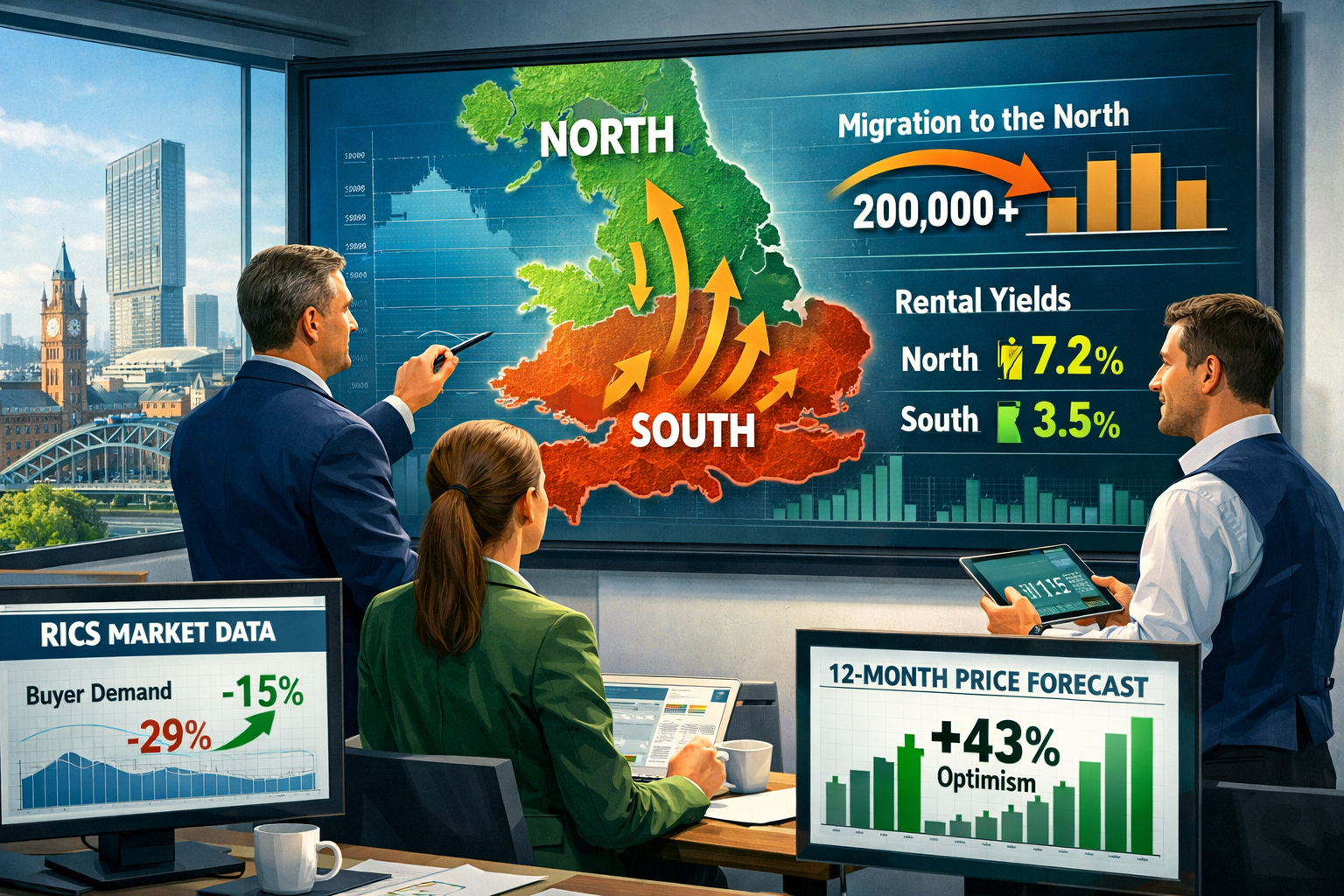

The implications extend beyond simple price movements. Private rents in the North East have surged 8.0% annually—the highest rate nationally—creating complex affordability dynamics that influence both residential and buy-to-let valuations.[2] Meanwhile, buyer demand is improving, with new enquiries reaching -15% in January 2026, up from -29% in November 2025, suggesting the market is finding firmer footing.[3]

Key Takeaways

🔑 Regional Performance Gap: Northern England regions are outperforming the South by 3-6 percentage points, with the North East leading at 4.6% annual growth versus London's -1.2% decline.

🔑 Rental-Sales Price Divergence: North East rental inflation (8.0%) significantly exceeds house price growth (4.6%), creating unique valuation challenges for buy-to-let properties and investor assessments.

🔑 Market Sentiment Improving: RICS surveyors report +43% optimism for price growth over the next 12 months—the most positive outlook since February 2025—with buyer demand steadily recovering.

🔑 Affordability-Driven Migration: Southern homebuyers are increasingly targeting Northern markets for better value, requiring surveyors to adapt comparable analysis methods and understand cross-regional buyer behavior.

🔑 Strategic Valuation Adjustments: Professionals must incorporate regional growth trajectories, rental yield differentials, and local economic indicators into their assessment frameworks to deliver accurate 2026 valuations.

Understanding the North-South Divide: Market Fundamentals Driving Regional Divergence

The Valuation Challenges in Northern England 2026: Surveyor Strategies Amid 5% Price Growth and Southern Slump begin with understanding the fundamental economic forces reshaping regional property markets. This isn't a temporary fluctuation—it represents a structural shift in UK housing dynamics that will influence valuation methodologies for years to come.

The Numbers Behind Northern Outperformance

The data paints a clear picture of regional divergence. The North East's 4.6% annual house price inflation represents nearly four times the South East's growth rate and a remarkable 5.8 percentage point advantage over London's declining market.[2] The North West's 4.1% growth similarly outpaces southern counterparts, positioning these regions as the UK's growth engines outside traditional hotspots.

| Region | Annual Price Growth | Rental Inflation | Market Position |

|---|---|---|---|

| North East | 4.6% | 8.0% | Strongest growth |

| North West | 4.1% | Data pending | Second strongest |

| UK Average | 2.4% | 5.8% | Baseline |

| South East | 1.0% | 5.5% | Below average |

| London | -1.2% | 6.2% | Declining |

This regional performance gap creates immediate challenges for surveyors conducting valuations. Traditional comparable analysis often relies on recent sales within a defined geographic area, but when regional markets are moving at different speeds, the timeframe and geographic scope of comparables become critical variables that can significantly impact final valuations.

Affordability Migration: The Driving Force

The primary driver behind Northern England's outperformance is affordability-driven migration. Average house prices in the UK reached £270,000 in December 2025, but this national figure masks enormous regional variation.[2] Properties in Northern England typically cost 30-50% less than equivalent homes in London and the South East, making them increasingly attractive to buyers priced out of southern markets.

This migration pattern creates unique valuation challenges. When a significant portion of buyers are relocating from different regional markets, their price expectations and willingness to pay may not align with traditional local market norms. Surveyors must understand these cross-regional dynamics to accurately assess market value versus inflated buyer enthusiasm.

Paula Higgins, CEO of HomeOwners Alliance, forecasts UK house prices will be approximately 2% higher in 2026, supported by easing mortgage rates and steady wage growth rather than sharp rebounds.[4] However, this national average conceals the reality that Northern regions will likely exceed this benchmark while southern areas may continue to underperform.

Economic Fundamentals Supporting Northern Growth

Beyond affordability, several economic factors support sustained Northern growth:

- Employment growth in regional cities like Manchester, Leeds, and Newcastle

- Infrastructure investment including High Speed 2 (HS2) connections and regional transport improvements

- Remote work flexibility allowing professionals to maintain London salaries while living in lower-cost Northern locations

- University retention as graduates increasingly remain in Northern cities rather than migrating south

- Commercial development attracting businesses to lower-cost Northern locations

For surveyors, these fundamentals must inform market commentary and valuation assumptions. A property's value isn't just determined by recent comparables—it's influenced by the trajectory of the local economy, employment prospects, and infrastructure development. Understanding how an RICS survey can help buyers negotiate becomes even more critical when regional markets are in flux.

The Southern Slump: Understanding Declining Markets

While Northern England thrives, London's -1.2% annual decline and the South East's anemic 1.0% growth present different valuation challenges.[2][4] Declining markets require surveyors to:

✅ Weight recent comparables more heavily than historical sales

✅ Adjust for market direction when comparable sales occurred in a different market phase

✅ Consider absorption rates and time-on-market trends

✅ Evaluate vendor motivation and realistic pricing expectations

✅ Account for potential further declines in forward-looking assessments

The contrast between Northern growth and Southern stagnation means that national valuation standards and methodologies must be applied with greater regional sensitivity. A 10% adjustment for market conditions might be appropriate in London, while Northern markets may require upward adjustments to reflect strengthening demand.

Surveyor Strategies for Accurate Northern England Valuations in 2026

The Valuation Challenges in Northern England 2026: Surveyor Strategies Amid 5% Price Growth and Southern Slump demand sophisticated approaches that go beyond traditional comparable sales analysis. Surveyors operating in high-growth Northern markets must adapt their methodologies to capture rapidly changing market dynamics while maintaining professional standards and accuracy.

Comparable Sales Analysis in Rapidly Appreciating Markets

Traditional comparable sales analysis assumes relatively stable market conditions where recent sales provide reliable indicators of current value. However, when markets are appreciating at 4-5% annually, a comparable sale from six months ago may undervalue current market conditions by 2-2.5% or more.

Strategic approaches for Northern England valuations include:

1. Time-Adjusted Comparables 📊

Apply systematic adjustments to comparable sales based on the time elapsed since completion. In a market growing at 4.6% annually, properties sold six months ago should be adjusted upward by approximately 2.3% to reflect current market conditions. This requires tracking monthly or quarterly price indices specific to local submarkets rather than relying on national or regional averages.

2. Weighted Recent Sales

Prioritize comparables from the most recent 3-6 months over older sales, even if older transactions appear more similar in property characteristics. In rapidly moving markets, timing is often more important than physical similarity when establishing current market value.

3. Pending Sales Analysis

Where possible, incorporate analysis of properties currently under offer or in the conveyancing process. While these haven't completed and aren't technically "comparables," they provide valuable insight into current buyer behavior and price expectations. Professional judgment is required to estimate likely completion prices based on survey results and negotiation patterns.

4. Price Per Square Foot Trending

Track price per square foot trends across property types and locations within your target area. This metric can reveal subtle market movements that individual sales might obscure, particularly in areas with diverse housing stock. When conducting property valuations, systematic tracking of this data provides crucial context.

Rental Yield Considerations for Buy-to-Let Valuations

The North East's 8.0% rental inflation significantly exceeding its 4.6% house price growth creates unusual dynamics for buy-to-let property valuations.[2] This divergence suggests several important trends:

Strong Rental Demand 💰

Rental growth outpacing capital appreciation indicates robust tenant demand, potentially driven by affordability challenges preventing renters from purchasing. This supports higher valuations for investment properties based on income capitalization approaches.

Yield Compression Risk

Conversely, if house prices begin accelerating to catch up with rental growth, yields may compress, potentially making current valuations appear optimistic in retrospect. Surveyors must balance current income against potential capital appreciation scenarios.

Investor Migration

Southern buy-to-let investors facing declining yields and regulatory pressures are increasingly targeting Northern markets. This capital influx can drive prices above levels supported by local buyer fundamentals alone, creating potential overvaluation risks that surveyors must identify.

For buy-to-let valuations, consider:

- Gross rental yields of 5-7% in Northern markets versus 3-4% in London

- Tenant demand indicators including void periods and rental growth trajectories

- Regulatory environment including selective licensing schemes and energy efficiency requirements

- Comparable investment sales rather than owner-occupier transactions

- Exit strategy viability for investors seeking capital appreciation versus income

Incorporating Market Sentiment and Forward Indicators

RICS survey data reveals +43% of surveyors anticipating higher prices over the next 12 months—the most positive outlook since February 2025.[3] This professional optimism, combined with improving buyer demand (-15% in January 2026 versus -29% in November 2025), suggests market momentum is building.[3]

Surveyors should incorporate these forward indicators into their market commentary and valuation assumptions:

Buyer Demand Trends 📈

Improving enquiry levels suggest increasing competition for available properties, supporting firmer pricing. Properties in high-demand areas or property types may command premiums above strict comparable analysis would suggest.

Agreed Sales Momentum

The net balance for agreed sales reached -9% in January 2026, the least negative reading since June 2025.[3] This indicates transaction volumes are recovering, which typically supports price stability and growth.

Surveyor Confidence

The +35% optimism regarding sales over the next 12 months represents professional consensus that market conditions are improving.[3] While individual valuations must be based on evidence rather than sentiment, understanding market direction helps contextualize current pricing.

Technology and Data Integration

Modern valuation practice increasingly relies on technology to enhance accuracy and efficiency:

Automated Valuation Models (AVMs) 🖥️

While AVMs shouldn't replace professional judgment, they provide useful benchmarks and can identify when a manual valuation deviates significantly from statistical expectations. In rapidly changing markets, regularly updated AVMs can capture trends faster than traditional comparable analysis.

Geographic Information Systems (GIS)

Mapping tools help visualize price gradients across neighborhoods, identify emerging hotspots, and understand how location factors influence value. This is particularly valuable in Northern cities where regeneration and infrastructure investment create localized value uplift.

Market Data Platforms

Subscription services providing real-time market data, rental comparables, and transaction volumes enable surveyors to maintain current market knowledge without relying solely on Land Registry data, which can lag by several months.

Digital Survey Tools

Laser measuring devices, thermal imaging cameras, and digital floor plan software improve inspection efficiency and accuracy, allowing surveyors to focus more time on analysis and market research. Understanding what to do before an RICS home survey helps clients prepare for these modern assessment techniques.

Regional Specialization and Local Market Knowledge

The Valuation Challenges in Northern England 2026: Surveyor Strategies Amid 5% Price Growth and Southern Slump underscore the importance of genuine local expertise. Surveyors attempting to operate across multiple regions without deep local knowledge risk misunderstanding subtle market dynamics that significantly impact valuations.

Successful Northern England surveyors:

✅ Maintain databases of local comparables updated weekly or monthly

✅ Develop relationships with local estate agents to understand off-market activity

✅ Track local economic indicators including employment, wages, and business investment

✅ Understand neighborhood-specific factors including school catchments, transport links, and regeneration plans

✅ Participate in local RICS branches and professional networks to share market intelligence

This local specialization enables surveyors to identify when a property is genuinely exceptional versus merely benefiting from general market uplift, and to distinguish sustainable price growth from speculative bubbles.

Navigating Specific Valuation Scenarios in Northern England's Growing Markets

Beyond general strategies, surveyors face specific scenarios that require tailored approaches. The Valuation Challenges in Northern England 2026: Surveyor Strategies Amid 5% Price Growth and Southern Slump manifest differently across property types, transaction purposes, and client needs.

New Build Valuations in High-Growth Areas

Northern England has seen significant new build development, particularly in city centers and regeneration areas. Valuing new builds in appreciating markets presents unique challenges:

Developer Premium Assessment 🏗️

New builds typically command a premium over equivalent second-hand properties due to warranties, modern specifications, and energy efficiency. However, this premium varies significantly by location and developer reputation. In strong markets, the premium may be 10-15%, while in weaker areas it might be only 5-7%.

Surveyors must assess whether the developer premium is justified by genuine quality advantages or represents marketing inflation that won't be supported in the resale market. Understanding whether you need a building survey for a new build helps buyers understand the inspection requirements even for recently constructed properties.

Help to Buy and Shared Ownership Complications

Many Northern new builds involve government assistance schemes that can complicate valuations. Surveyors must understand how these schemes affect market value, particularly when the property is being refinanced or sold after the initial purchase.

Completion Risk

For off-plan purchases, surveyors must assess completion risk and whether the property will be worth the agreed price when construction finishes, potentially 12-24 months after the valuation date. In rapidly appreciating markets, this actually favors buyers, but construction delays or market shifts can create problems.

Period Property Valuations: Victorian and Terraced Housing

Northern England's housing stock includes substantial Victorian and Edwardian terraced housing, which presents specific valuation considerations:

Modernization Premiums 🏘️

The value difference between modernized and unmodernized period properties can be substantial—often 20-30% or more. Surveyors must accurately assess the quality and extent of renovations, as superficial cosmetic improvements don't justify the same premiums as comprehensive structural and systems upgrades.

Structural Considerations

Period properties may have issues including subsidence, damp, outdated electrical systems, and inadequate insulation. These defects can significantly impact value, but their severity and remediation costs vary widely. Detailed inspection and accurate cost assessment are essential. Resources on what to do after a bad building survey report help clients understand their options when significant defects are identified.

Conservation Area Constraints

Many Northern city centers include conservation areas that restrict alterations and can affect both value and marketability. Properties with original features may command premiums from certain buyers while deterring others who want modern conveniences.

Buy-to-Let Investment Valuations

The strong rental growth in Northern England (8.0% in the North East)[2] makes investment properties particularly attractive, but valuations must reflect both income and capital considerations:

Income Capitalization Approach 💼

For investment properties, the income approach may be more appropriate than pure comparable sales analysis. Calculate net annual rental income and apply an appropriate yield (typically 5-7% in Northern markets) to derive capital value. This should be cross-checked against comparable sales to ensure consistency.

Tenant Quality and Lease Terms

Properties with sitting tenants on assured shorthold tenancies may be valued differently than vacant properties, depending on rent levels relative to market rates and tenant reliability. Long-term tenancies at below-market rents can significantly depress investment value.

Regulatory Compliance

Ensure properties meet current Energy Performance Certificate (EPC) requirements (minimum E rating for lettings), electrical safety standards, and any local licensing requirements. Non-compliance can severely impact value or prevent letting entirely.

Portfolio Considerations

Investors acquiring multiple properties may pay premiums for properties that complement their existing portfolio geographically or by property type. Conversely, they may seek discounts for bulk purchases. Surveyors must understand whether they're valuing for single-asset or portfolio purposes.

First-Time Buyer Market Dynamics

Northern England's affordability attracts substantial first-time buyer activity, creating specific market dynamics:

Affordability-Driven Pricing 🏠

First-time buyers often stretch to maximum affordability based on mortgage multiples. In strong markets, this can drive prices above levels supported by traditional comparable analysis, particularly for smaller properties and flats. Understanding first-time buyer considerations when booking a building survey helps these buyers make informed decisions.

Leasehold Complications

Many Northern flats are leasehold with varying ground rents and service charges. Surveyors must assess whether these charges are reasonable and whether lease lengths are sufficient (generally 80+ years for mortgageability). Short leases can severely impact value.

Help to Buy Impact

Government assistance schemes can inflate first-time buyer budgets, potentially driving prices above open market levels. Surveyors must distinguish between market value (what a willing buyer would pay without special assistance) and actual transaction prices that may include government support.

Mortgage Valuation Versus Market Valuation

Lenders commissioning valuations have different priorities than buyers or sellers:

Conservative Approach 🏦

Mortgage valuations typically adopt conservative assumptions to protect lender interests. In rapidly appreciating markets, this may mean valuations lag current market sentiment, potentially creating conflicts with agreed purchase prices.

Forced Sale Considerations

Lenders are concerned with forced sale values in the event of repossession. In strong markets, this discount may be minimal (5-10%), but surveyors must still consider how quickly the property could be sold and what price it would achieve under distressed circumstances.

Lending Policy Constraints

Different lenders have varying policies regarding property types, locations, and construction methods. Some may decline to lend on ex-local authority properties, non-standard construction, or properties above commercial premises. Surveyors must understand these constraints when conducting mortgage valuations.

Cross-Regional Buyer Considerations

The affordability migration from South to North creates unique valuation challenges:

Price Expectation Calibration 🔄

Southern buyers may have inflated price expectations based on their home region's market, potentially driving Northern prices above local norms. Surveyors must assess whether prices reflect genuine local market dynamics or temporary distortions from cross-regional demand.

Comparable Selection

When significant numbers of buyers are relocating from other regions, local comparables may not fully capture current market dynamics. Surveyors should track the proportion of buyers from outside the region and assess whether this is creating sustainable price uplift or speculative bubbles.

Rental Versus Owner-Occupier Markets

Some Northern locations attract primarily local owner-occupiers while others draw investor and relocating buyer interest. These different buyer profiles can create submarkets with distinct pricing dynamics within the same postal code.

Risk Management and Professional Standards in Volatile Regional Markets

The Valuation Challenges in Northern England 2026: Surveyor Strategies Amid 5% Price Growth and Southern Slump create professional liability risks that surveyors must carefully manage. Rapidly changing markets increase the potential for valuations to be challenged, whether by disappointed buyers, frustrated sellers, or lenders facing losses.

RICS Red Book Compliance in Dynamic Markets

The RICS Valuation – Global Standards (Red Book) provides the professional framework for all valuations, but application in volatile markets requires particular care:

Market Value Definition 📋

The Red Book defines market value as "the estimated amount for which an asset should exchange on the valuation date between a willing buyer and a willing seller in an arm's length transaction, after proper marketing and where the parties had each acted knowledgeably, prudently and without compulsion."[1]

In rapidly appreciating Northern markets, this definition requires careful interpretation:

- "Should exchange" versus "would exchange": Surveyors must assess what a property should be worth based on market evidence, not what an enthusiastic buyer might pay

- "Proper marketing": Consider whether current marketing periods are adequate or whether rushed sales are inflating prices

- "Knowledgeably and prudently": Assess whether buyers understand local market dynamics or are making decisions based on Southern market expectations

Assumptions and Special Assumptions

In volatile markets, clearly state all assumptions underpinning the valuation, including:

✅ Market conditions on the valuation date

✅ Assumed marketing period

✅ Anticipated buyer profile

✅ Economic conditions and interest rate assumptions

✅ Any special assumptions regarding property condition or legal status

Uncertainty and Material Uncertainty Declarations

When market conditions are changing rapidly or reliable comparable evidence is limited, surveyors may need to declare material uncertainty:

When to Declare Material Uncertainty ⚠️

Material uncertainty should be declared when market conditions are so volatile that the valuer has less confidence than usual in the valuation. This isn't an admission of incompetence—it's professional transparency about market conditions.

In Northern England's current market, material uncertainty might be appropriate when:

- Comparable evidence is sparse or contradictory

- Market direction is unclear despite recent price growth

- External factors (economic policy, interest rates, regulatory changes) create unusual uncertainty

- The property is unique with limited comparable evidence

- Cross-regional buyer activity is creating unusual pricing dynamics

Wording Material Uncertainty

When declaring material uncertainty, be specific about the causes and implications. Generic statements like "the market is uncertain" are unhelpful. Instead, explain precisely what factors create uncertainty and how they might affect the valuation range.

Professional Indemnity Insurance Considerations

Valuation work in volatile markets increases professional liability exposure:

Higher Claims Risk 🛡️

When markets are moving rapidly, valuations are more likely to be challenged. A valuation that seems reasonable on the valuation date may appear incorrect six months later if market conditions change. Ensure your professional indemnity insurance provides adequate coverage for your valuation work volume and property values.

Documentation Standards

Maintain comprehensive records of all valuations, including:

- Comparable evidence considered and rejected

- Market data and research consulted

- Photographs and inspection notes

- Client instructions and any limitations on scope

- Draft valuations and revisions

- Correspondence regarding valuation queries or challenges

This documentation is essential if a valuation is later challenged and you need to demonstrate your professional judgment was reasonable based on information available at the time.

Client Communication and Expectation Management

Clear communication helps prevent disputes and manages client expectations:

Explaining Market Dynamics 💬

Many clients don't understand regional market differences or how rapidly changing conditions affect valuations. Take time to explain:

- Why Northern and Southern markets are performing differently

- How recent comparable sales inform current valuations

- What factors could cause values to change in the near future

- The difference between market value and mortgage lending value

- Why valuations are point-in-time assessments, not guarantees

Managing Disappointed Clients

When valuations come in below purchase prices or client expectations, explain the reasoning clearly and provide supporting evidence. Understand that average price reductions after surveys are common and help buyers negotiate fair prices.

Scope Limitations

Clearly define what the valuation does and doesn't include. A mortgage valuation isn't a building survey, and clients may not understand the difference. Explain inspection limitations and recommend additional investigations where appropriate.

Continuing Professional Development

Markets are changing rapidly, and surveyors must maintain current knowledge:

Regional Market Training 📚

Attend RICS regional events and local property market briefings to understand specific Northern England dynamics. National trends don't always apply locally, and regional expertise is increasingly valuable.

Valuation Methodology Updates

Stay current with evolving valuation techniques, particularly regarding technology integration, data analytics, and automated valuation models. These tools complement rather than replace professional judgment.

Economic and Policy Awareness

Understand how broader economic factors—interest rates, employment, government housing policy, taxation—affect property markets. This context is essential for informed market commentary and valuation assumptions.

Why choosing RICS surveyors matters becomes increasingly clear in complex markets. RICS-qualified professionals maintain rigorous standards and continuing education that ensure competent, ethical practice.

Future Outlook: Sustaining Accuracy as Northern Markets Evolve

The Valuation Challenges in Northern England 2026: Surveyor Strategies Amid 5% Price Growth and Southern Slump will continue evolving as market conditions change throughout 2026 and beyond. Surveyors must anticipate future developments and adapt their approaches accordingly.

Predicted Market Trajectories for 2026-2027

Current indicators suggest several likely scenarios for Northern England markets:

Continued Outperformance 📊

Most forecasts predict Northern regions will continue outperforming the South throughout 2026, though growth rates may moderate from current levels. The 2% national average growth forecast by HomeOwners Alliance[4] likely masks 3-4% growth in Northern regions versus flat or slightly declining Southern markets.

Rental Growth Moderation

The North East's 8.0% rental inflation[2] is probably unsustainable long-term. As rental growth moderates toward 4-5% annually, the gap between rental and capital appreciation should narrow, creating more balanced investment metrics.

Transaction Volume Recovery

Improving buyer demand (-15% in January 2026 versus -29% in November 2025)[3] suggests transaction volumes will continue recovering. Higher volumes typically support price stability and provide more comparable evidence for valuations.

Interest Rate Stabilization

Mortgage rates are expected to stabilize or decline modestly through 2026, supporting affordability and buyer demand. However, rates are unlikely to return to the ultra-low levels of 2020-2021, meaning affordability constraints will persist.

Emerging Valuation Challenges

Several emerging issues will create new valuation challenges:

Energy Efficiency Requirements 🌱

Increasing focus on energy efficiency and net-zero targets will affect property values. Properties with poor EPC ratings may face value discounts or become unmortgageable, while highly efficient properties command premiums. Surveyors must understand energy assessment and retrofit costs.

Climate Risk Assessment

Flood risk, coastal erosion, and extreme weather events are increasingly affecting property values and insurability. Northern England includes flood-prone areas where climate risk significantly impacts value. Surveyors should incorporate climate risk assessment into their valuation frameworks.

Remote Work Permanence

The extent to which remote and hybrid work patterns persist will significantly affect regional markets. If remote work proves permanent, Northern England's affordability advantage strengthens. If employers mandate office returns, some of the current migration may reverse.

Infrastructure Investment Impact

Planned infrastructure improvements—particularly transport links—can significantly affect local property values. Surveyors should track infrastructure announcements and assess their likely impact on specific locations and property types.

Technology Integration and Automation

Valuation practice will continue evolving technologically:

Enhanced AVMs 🖥️

Automated Valuation Models are becoming more sophisticated, incorporating more data sources and using machine learning to improve accuracy. While they won't replace professional surveyors for complex or high-value properties, they'll increasingly handle straightforward residential valuations.

Data Integration Platforms

Emerging platforms integrate multiple data sources—Land Registry, rental comparables, planning applications, economic indicators—into unified dashboards that help surveyors make more informed decisions quickly.

Virtual Inspections

Technology enabling remote property inspections (high-resolution photography, video tours, 3D scanning) may become more common for certain valuation types, though physical inspections will remain essential for detailed assessments.

Blockchain and Property Records

Distributed ledger technology may eventually streamline property transactions and create more transparent, accessible comparable evidence. This could significantly improve data availability for valuations.

Professional Specialization Trends

The complexity of modern valuation practice is driving increased specialization:

Regional Specialists 🎯

Surveyors focusing on specific Northern regions or cities can develop deep local expertise that commands premium fees and attracts sophisticated clients. This specialization helps differentiate professional services in competitive markets.

Asset Class Specialists

Focus on specific property types—period properties, new builds, buy-to-let investments, commercial conversions—enables surveyors to develop nuanced understanding that generalists can't match.

Purpose-Specific Expertise

Some surveyors specialize in particular valuation purposes—matrimonial, probate, tax, lending—where specialized knowledge of legal and regulatory frameworks adds significant value.

Building Resilient Valuation Practices

Successful surveyors will build practices that can adapt to changing market conditions:

Diversified Client Base 💼

Avoid over-dependence on any single client type (e.g., only mortgage valuations or only buy-to-let investors). Diversification provides stability when specific market segments weaken.

Continuous Market Monitoring

Implement systematic processes for tracking market indicators, comparable sales, and economic data. This ongoing research ensures valuations reflect current conditions rather than outdated assumptions.

Professional Networks

Maintain strong relationships with estate agents, mortgage brokers, property developers, and fellow surveyors. These networks provide market intelligence and business development opportunities.

Quality Over Volume

In competitive markets, resist pressure to compromise quality for speed or volume. Thorough, well-documented valuations protect professional reputation and minimize liability risk, even if they take longer and limit throughput.

Conclusion: Mastering Valuation in Northern England's Dynamic 2026 Market

The Valuation Challenges in Northern England 2026: Surveyor Strategies Amid 5% Price Growth and Southern Slump represent both significant opportunities and complex professional demands for RICS-qualified surveyors. Northern England's 4-5% annual price growth contrasts sharply with London's -1.2% decline and the South East's 1.0% stagnation, creating a transformed regional landscape that requires sophisticated valuation approaches.[2][4]

Successful navigation of this market demands:

✅ Time-adjusted comparable analysis that accounts for rapid price movements

✅ Rental yield integration recognizing the 8.0% rental inflation in the North East[2]

✅ Forward-looking market assessment incorporating the +43% surveyor optimism for price growth[3]

✅ Technology adoption including AVMs, GIS mapping, and data integration platforms

✅ Regional specialization with deep local market knowledge

✅ Rigorous professional standards including Red Book compliance and comprehensive documentation

The improving market sentiment—with buyer demand recovering from -29% in November 2025 to -15% in January 2026**[3]—suggests Northern England's outperformance will continue throughout 2026. Surveyors who develop expertise in these high-growth markets will be well-positioned to serve the increasing numbers of buyers, investors, and lenders targeting Northern regions.

Actionable Next Steps for Surveyors

Immediate Actions (Next 30 Days):

- Audit your comparable database: Ensure you have current sales data for your target areas, updated within the last 3-6 months

- Review recent valuations: Assess whether your recent work adequately accounts for market appreciation and whether adjustments are needed

- Strengthen local networks: Connect with estate agents and fellow surveyors in Northern England to share market intelligence

- Update professional indemnity insurance: Ensure coverage is adequate for increasing property values and valuation volumes

Medium-Term Development (Next 3-6 Months):

- Invest in technology: Evaluate AVM platforms, GIS tools, and data integration services that can enhance your valuation practice

- Pursue specialized training: Attend RICS courses on valuation methodology, regional markets, or specific property types

- Develop market commentary: Create regular market updates for clients demonstrating your expertise and market knowledge

- Refine documentation processes: Ensure your valuation reports, inspection notes, and comparable analysis are comprehensive and defensible

Strategic Positioning (Next 6-12 Months):

- Build regional specialization: Focus on specific Northern cities or property types where you can develop recognized expertise

- Expand service offerings: Consider complementary services like building surveys, homebuyer reports, or investment analysis

- Strengthen professional credentials: Pursue RICS fellowship or specialized accreditations that differentiate your practice

- Develop thought leadership: Write articles, speak at events, or contribute to professional discussions about Northern England markets

The Valuation Challenges in Northern England 2026: Surveyor Strategies Amid 5% Price Growth and Southern Slump are reshaping the UK property landscape. Surveyors who embrace these changes, develop regional expertise, and maintain rigorous professional standards will thrive in this dynamic market. The opportunities are substantial—Northern England's sustained outperformance creates demand for skilled valuation professionals who can navigate complex, rapidly evolving markets with confidence and competence.

By combining traditional surveying excellence with modern technology, deep local knowledge, and forward-looking market analysis, surveyors can deliver exceptional value to clients while building resilient, successful practices positioned for long-term growth in Northern England's transformed property market.

References

[1] Valuation Surveys In The 2026 Market Recovery Regional Strategies For Scotland Northern Ireland And Northern England Growth – https://nottinghillsurveyors.com/blog/valuation-surveys-in-the-2026-market-recovery-regional-strategies-for-scotland-northern-ireland-and-northern-england-growth

[2] February2026 – https://www.ons.gov.uk/economy/inflationandpriceindices/bulletins/privaterentandhousepricesuk/february2026

[3] Uk Resi Survey Jan 2026 Report Shows Early Signs Market Recovery Despite Caution – https://www.rics.org/news-insights/uk-resi-survey-jan-2026-report-shows-early-signs-market-recovery-despite-caution

[4] House Price Forecast – https://hoa.org.uk/advice/guides-for-homeowners/i-am-buying/house-price-forecast/

[5] Residential Forecast – https://www.cushmanwakefield.com/en/united-kingdom/insights/residential-forecast

[6] Watch – https://www.youtube.com/watch?v=jLxh-kuQaDg